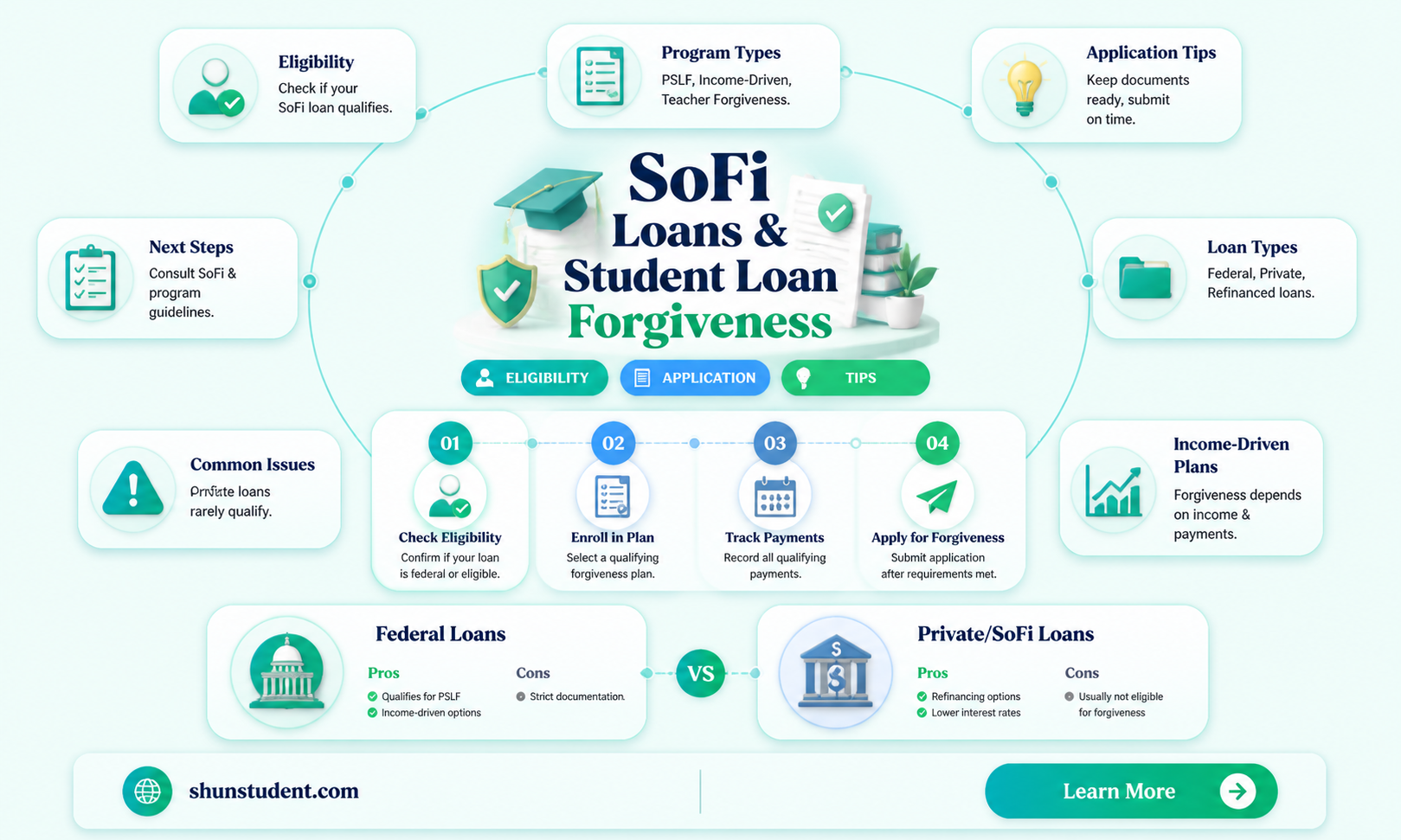

The question of whether SoFi loans are eligible for student loan forgiveness is a critical concern for many borrowers navigating the complexities of debt relief programs. SoFi, a prominent fintech company, offers private student loans and refinancing options, but its products differ significantly from federal student loans, which are typically the focus of forgiveness initiatives like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans. Since SoFi loans are private, they generally do not qualify for federal forgiveness programs. However, borrowers may explore alternative strategies, such as refinancing with SoFi to lower interest rates or seeking employer-based repayment assistance programs. Understanding the distinctions between private and federal loans is essential for borrowers to make informed decisions about managing their student debt and exploring potential avenues for relief.

| Characteristics | Values |

|---|---|

| Eligibility for Federal Forgiveness | No, SoFi loans are private loans and do not qualify for federal forgiveness programs like PSLF, IDR forgiveness, or loan cancellation. |

| Loan Type | Private student loans. |

| Lender | SoFi (Social Finance, Inc.). |

| Forgiveness Options | Limited; SoFi may offer temporary relief or forbearance in hardship cases but does not provide loan forgiveness. |

| Federal Programs Applicability | Ineligible for federal programs such as PSLF, Teacher Loan Forgiveness, or income-driven repayment (IDR) forgiveness. |

| Refinancing Impact | Refinancing federal loans with SoFi makes them ineligible for federal forgiveness programs. |

| State-Specific Programs | May be eligible for state-specific repayment assistance programs (varies by state). |

| Employer Assistance | Some employers may offer student loan repayment benefits, but this is not specific to SoFi loans. |

| Hardship Relief | SoFi may offer temporary payment pauses or reduced payments in cases of economic hardship, but this is not forgiveness. |

| Loan Discharge | No discharge options unless in cases of borrower death or permanent disability (terms apply). |

| Latest Update (as of 2023) | No changes to eligibility for federal forgiveness programs for private loans like SoFi. |

Explore related products

$8.99 $19.95

What You'll Learn

![]()

Sofi Loan Types Covered

SoFi offers a variety of loan products, but not all are eligible for federal student loan forgiveness programs. Understanding which SoFi loans qualify is crucial for borrowers seeking debt relief. Primarily, SoFi refinances federal student loans into private loans, which generally disqualifies them from programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. However, SoFi’s Student Loan Refinancing and Parent PLUS Loan Refinancing may still be attractive options for borrowers prioritizing lower interest rates or simplified repayment terms, even if it means forgoing federal forgiveness benefits.

For borrowers with private student loans originally issued by SoFi, forgiveness options are limited. Private loans are not eligible for federal forgiveness programs, regardless of the lender. SoFi does not offer its own forgiveness programs, so borrowers must rely on external initiatives like state-based forgiveness programs or employer-sponsored repayment assistance. For example, nurses or teachers in certain states may qualify for state-specific forgiveness programs, but these are independent of SoFi’s offerings.

A notable exception is SoFi’s medical resident refinancing program, which provides tailored terms for medical professionals in residency. While this program doesn’t offer forgiveness, it reduces monthly payments during residency, easing financial strain. Borrowers in this category should weigh the long-term trade-off of losing federal forgiveness eligibility against the immediate benefits of lower payments and interest rates.

Borrowers considering SoFi loans should carefully evaluate their career paths and financial goals. For instance, a public sector worker aiming for PSLF should avoid refinancing federal loans with SoFi, as this would render them ineligible. Conversely, a high-earning professional with no intention of pursuing federal forgiveness might benefit from SoFi’s competitive rates and flexible terms. Practical tip: Use SoFi’s online rate calculator to compare potential savings against the loss of federal benefits before committing to a refinance.

In summary, SoFi loans are not eligible for federal student loan forgiveness programs due to their private nature. Borrowers must decide whether the advantages of refinancing—such as lower interest rates or single monthly payments—outweigh the loss of federal protections. Always review your long-term financial strategy and consult resources like the Department of Education’s Federal Student Aid website before refinancing federal loans with SoFi or any private lender.

Navient Student Loan Forgiveness: Understanding Your Timeline for Debt Relief

You may want to see also

Explore related products

![]()

Eligibility Criteria for Forgiveness

SoFi loans, being private student loans, generally do not qualify for federal student loan forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. These programs are exclusively designed for federal student loans, such as Direct Loans or Federal Family Education Loans (FFEL) that have been consolidated into the Direct Loan program. Since SoFi loans are privately funded and serviced, they fall outside the scope of federal forgiveness initiatives. However, understanding the eligibility criteria for forgiveness can help borrowers explore alternative strategies to manage their SoFi loan debt effectively.

One critical aspect of eligibility for forgiveness is the type of loan and its servicer. Federal forgiveness programs require borrowers to have eligible federal loans and often mandate specific repayment plans, such as IDR plans. SoFi loans, being private, do not meet these criteria. Borrowers with SoFi loans should instead focus on refinancing options or employer-based repayment assistance programs (LRAPs) that may offer partial or full loan repayment in exchange for specific employment commitments, such as working in public service or high-need fields like healthcare or education.

Another factor to consider is the borrower’s employment and income. Federal forgiveness programs like PSLF require 10 years of qualifying payments while working full-time for a government or nonprofit organization. While SoFi loans don’t qualify for PSLF, borrowers in public service roles may still benefit from state-based LRAPs or SoFi’s own assistance programs, if available. For example, some states offer loan repayment assistance for teachers, nurses, or lawyers working in underserved areas. Researching these programs and aligning career choices with their requirements can provide a pathway to debt relief.

Lastly, borrowers should explore SoFi’s unique offerings, such as unemployment protection or career support services, which can indirectly aid in loan management. While not forgiveness in the traditional sense, these benefits can provide temporary relief during financial hardship, allowing borrowers to stay current on payments and avoid default. Additionally, refinancing with SoFi or another lender at a lower interest rate can reduce overall debt burden, making repayment more manageable without relying on forgiveness programs.

In summary, SoFi loans are not eligible for federal student loan forgiveness programs due to their private nature. However, borrowers can still pursue alternative strategies like employer-based repayment assistance, state-specific LRAPs, or SoFi’s own support programs to alleviate their debt. By understanding these options and aligning them with their financial and career goals, borrowers can effectively navigate their repayment journey.

Maryland's Tax Treatment of Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Federal vs. Private Loan Rules

Understanding the distinction between federal and private student loans is crucial when exploring eligibility for loan forgiveness programs. Federal loans, backed by the U.S. Department of Education, come with specific benefits, including access to income-driven repayment plans and forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment forgiveness. These programs are designed to provide relief to borrowers based on their income, profession, or repayment history. For instance, PSLF forgives the remaining balance on federal Direct Loans after 120 qualifying payments for those working full-time in eligible public service jobs.

Private loans, such as those offered by SoFi, operate under entirely different rules. SoFi loans are not eligible for federal forgiveness programs because they are not federally backed. Private lenders like SoFi focus on competitive interest rates, flexible repayment terms, and refinancing options rather than forgiveness. Borrowers with SoFi loans must rely on the lender’s specific policies, which may include temporary forbearance or deferment options but lack the structured forgiveness pathways available for federal loans.

A key takeaway is that refinancing federal loans with a private lender like SoFi can eliminate access to federal forgiveness programs. For example, if a borrower refinances their federal Direct Loans with SoFi, they forfeit eligibility for PSLF or income-driven repayment forgiveness. This trade-off requires careful consideration, as refinancing may lower monthly payments or interest rates but comes at the cost of losing federal protections.

To navigate this landscape, borrowers should assess their long-term financial goals. If pursuing a career in public service or anticipating difficulty repaying loans, retaining federal loans might be advantageous. Conversely, if prioritizing lower interest rates and faster repayment, refinancing with a private lender could be beneficial. Always review the terms of both federal and private loans before making a decision, and consult resources like the Federal Student Aid website for detailed guidance on forgiveness programs.

Are Forgiven Student Loans in Virginia Considered Taxable Income?

You may want to see also

Explore related products

![]()

Application Process for Forgiveness

SoFi loans, being private student loans, are generally not eligible for federal student loan forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. However, understanding the application process for forgiveness is still crucial for borrowers exploring all possible avenues for debt relief. Here’s a focused guide on navigating this process, even if your SoFi loans don’t qualify directly.

Step-by-Step Application Process for Forgiveness

If you’re considering forgiveness programs, start by confirming your loan type. Federal loans have specific forgiveness pathways, but private loans like SoFi’s require alternative strategies. For federal loans, the process begins with consolidating eligible loans into a Direct Consolidation Loan, if necessary. Next, enroll in an income-driven repayment plan to align payments with your earnings. After 20–25 years of qualifying payments, depending on the plan, forgiveness may be granted. Documentation is key—keep records of payments, employment (for PSLF), and annual income certifications. For SoFi borrowers, the focus shifts to refinancing or exploring employer-based repayment assistance programs, as these are the closest alternatives to traditional forgiveness.

Cautions and Limitations

While the application process for federal forgiveness is structured, it’s not without pitfalls. Missing a single qualifying payment can reset the forgiveness clock, so consistency is critical. Additionally, forgiven amounts may be taxed as income, though temporary exclusions exist under certain conditions (e.g., PSLF). For SoFi borrowers, refinancing to a lower interest rate can reduce overall debt burden, but it eliminates access to federal forgiveness programs if the loans were previously federal. Always weigh the long-term implications before refinancing private loans.

Practical Tips for Maximizing Relief

Even without direct forgiveness eligibility, SoFi borrowers can take proactive steps. First, negotiate with employers for student loan repayment benefits, which can offset debt. Second, explore state-based forgiveness programs for specific professions, such as healthcare or education. Third, maintain a budget that prioritizes extra payments toward high-interest loans. Finally, stay informed about legislative changes—new policies could expand forgiveness options for private loans in the future.

The application process for forgiveness demands precision and persistence, whether you hold federal or private loans. For SoFi borrowers, the path is less direct but not impossible. By combining refinancing, employer assistance, and strategic repayment, you can mitigate debt effectively. Remember, the goal is not just forgiveness but financial stability—choose the tools that align best with your long-term objectives.

Ultimate Guide to Applying for Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Impact on Credit Score

Taking out a SoFi loan to refinance student debt can indirectly influence your credit score, but the impact depends on how you manage the new loan. Initially, refinancing triggers a hard credit inquiry, which may cause a slight dip in your score—typically around 5 to 10 points. However, this effect is temporary and diminishes within 12 months. The real credit score implications arise from your payment behavior post-refinancing. Consistently making on-time payments on your SoFi loan can positively impact your score by demonstrating financial responsibility. Conversely, missed or late payments will harm your credit, potentially offsetting any benefits of refinancing.

One often-overlooked factor is the loan term. Refinancing with SoFi allows you to choose a shorter repayment period, which can save on interest but requires higher monthly payments. If you opt for a longer term to lower monthly payments, you’ll pay more interest over time, and your credit utilization ratio may remain higher for an extended period. Credit utilization—the amount of credit you’re using compared to your total available credit—accounts for 30% of your FICO score. Paying off your original student loans reduces this ratio, but if your SoFi loan balance is similar or larger, the improvement may be minimal.

Another consideration is the mix of credit types in your profile, which makes up 10% of your FICO score. Closing multiple student loan accounts and replacing them with a single SoFi loan simplifies your debt but reduces the diversity of your credit portfolio. While this impact is minor, it’s worth noting if you’re actively working to improve your score. For instance, if you have few other credit accounts (e.g., credit cards or auto loans), the reduction in credit mix could slightly lower your score.

To maximize the positive impact on your credit score, follow these practical steps: First, ensure your budget accommodates the new monthly payment to avoid late payments. Second, monitor your credit report regularly to catch any discrepancies or errors. Third, avoid opening new credit accounts simultaneously, as multiple hard inquiries can compound the initial score drop. Finally, consider paying more than the minimum due when possible to reduce the loan balance faster, thereby lowering your credit utilization ratio sooner.

In summary, SoFi loans themselves are not eligible for student loan forgiveness programs, but refinancing with SoFi can indirectly affect your credit score based on your financial management. By understanding the nuances—from hard inquiries to credit utilization—you can navigate refinancing in a way that strengthens, rather than weakens, your credit profile. The key is to treat the new loan as an opportunity to demonstrate consistent, responsible financial behavior.

Layoffs and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

No, SoFi loans are private student loans and are not eligible for federal student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment forgiveness.

No, refinancing SoFi loans into federal loans is not possible. Once a federal loan is refinanced with a private lender like SoFi, it loses eligibility for federal forgiveness programs.

No, SoFi does not offer loan forgiveness programs. Borrowers must rely on federal programs or other repayment options, which are not available for private loans like those from SoFi.