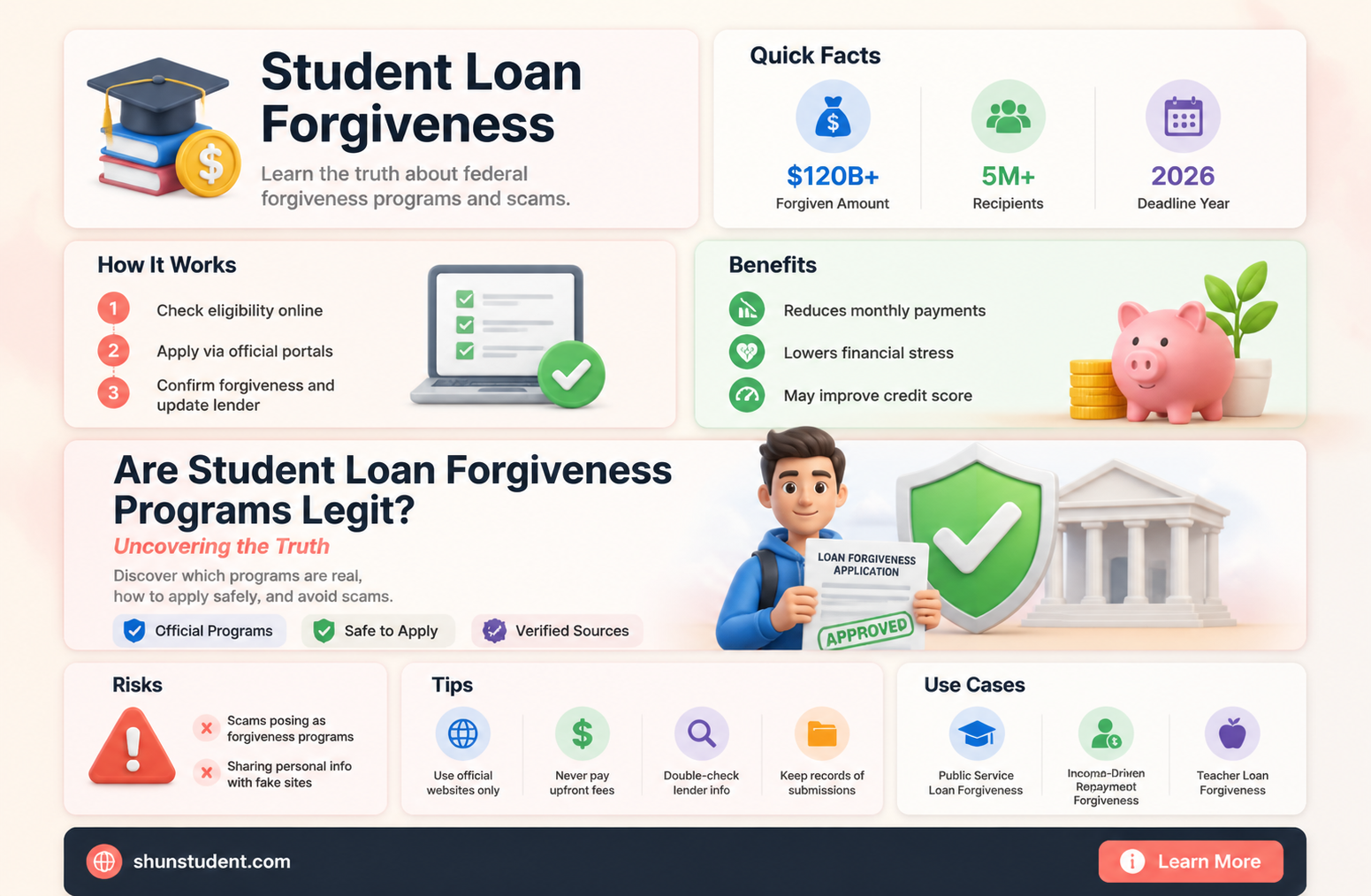

Student loan forgiveness programs have become a hot topic in recent years, as millions of borrowers seek relief from the burden of mounting debt. While the idea of having a portion of your loans forgiven sounds appealing, many borrowers are left wondering: are these programs legitimate? With various federal and state initiatives, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment plans, it's essential to understand the eligibility requirements, application processes, and potential pitfalls. As the debate surrounding student loan debt continues to intensify, it's crucial to separate fact from fiction and explore the legitimacy of these programs, ensuring borrowers make informed decisions about their financial future.

| Characteristics | Values |

|---|---|

| Legitimacy | Yes, legitimate programs exist, but scams are prevalent. |

| Types of Programs | Federal programs (e.g., Public Service Loan Forgiveness, Income-Driven Repayment Plans), state-based programs, employer-based programs. |

| Eligibility Criteria | Varies by program; common criteria include employment type, income level, loan type, and repayment history. |

| Application Process | Typically requires submitting forms, documentation, and proof of eligibility. |

| Common Scams | Upfront fees, promises of immediate forgiveness, fake government affiliations. |

| Verification Methods | Check official government websites (e.g., studentaid.gov), contact loan servicers directly. |

| Timeframe for Forgiveness | Varies; e.g., PSLF requires 10 years of qualifying payments, IDR plans may take 20-25 years. |

| Tax Implications | Some forgiven amounts may be taxable, depending on the program and circumstances. |

| Impact on Credit Score | Generally neutral, but missed payments or defaults before forgiveness can harm credit. |

| Recent Updates (as of 2023) | Expanded eligibility for PSLF, one-time adjustments for IDR plans, and temporary waivers for certain requirements. |

| Warning Signs of Scams | Unsolicited offers, pressure to act immediately, requests for personal or financial information. |

| Cost to Apply | Legitimate programs are free to apply for; avoid programs requiring upfront fees. |

| Success Rate | Varies; PSLF approval rates have improved but remain low due to strict eligibility rules. |

| Alternatives to Forgiveness | Loan consolidation, refinancing (private loans only), repayment assistance programs. |

Explore related products

What You'll Learn

![]()

Eligibility criteria for loan forgiveness programs

Student loan forgiveness programs can be a lifeline for borrowers, but not everyone qualifies. Eligibility criteria vary widely depending on the program, making it crucial to understand the specifics before applying. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to work full-time in a qualifying public service job for 10 years while making 120 eligible payments. In contrast, income-driven repayment (IDR) plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), offer forgiveness after 20–25 years of payments, but eligibility is tied to income and family size. Knowing these differences is the first step in determining whether a program is legit and applicable to your situation.

To navigate eligibility, start by identifying your loan type. Federal student loans, such as Direct Loans, are eligible for most forgiveness programs, while private loans rarely qualify. For example, the Teacher Loan Forgiveness program requires borrowers to have Direct Subsidized or Unsubsidized Loans and to teach full-time for five consecutive years in a low-income school. Private loans, on the other hand, may only be forgiven through lender-specific programs or bankruptcy, which is rare and comes with severe financial consequences. Always verify your loan type through your servicer or the National Student Loan Data System (NSLDS) before proceeding.

Another critical factor is employment status and occupation. Programs like PSLF and the National Health Service Corps (NHSC) Loan Repayment Program are designed for specific professions, such as teachers, nurses, and government employees. For instance, the NHSC program requires a two-year commitment to work in a Health Professional Shortage Area (HPSA), while PSLF covers a broader range of public service jobs, including nonprofit and government roles. If you’re considering a career change, research whether your new position aligns with forgiveness program requirements to maximize your chances of eligibility.

Income and family size play a significant role in IDR plans, which calculate monthly payments based on these factors. For example, a single borrower earning $40,000 annually with $50,000 in loans might pay as little as $100 per month under REPAYE, with forgiveness kicking in after 20 years. However, if your income increases significantly, your payments will rise accordingly, potentially reducing the amount forgiven. Use online calculators, such as those provided by the Department of Education, to estimate your payments and forgiveness timeline based on your unique financial situation.

Finally, beware of scams that prey on borrowers seeking relief. Legitimate programs are free to apply for and do not require upfront fees. If a company promises immediate forgiveness or asks for payment to "qualify," it’s likely a scam. Stick to official government websites and consult with your loan servicer or a certified financial advisor for guidance. By understanding eligibility criteria and staying informed, you can determine whether a student loan forgiveness program is both legit and right for you.

Understanding Your Student Loan Forgiveness Charge Percentage: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Types of federal and private forgiveness options

Federal student loan forgiveness programs are legitimate, but they come with specific eligibility criteria and application processes. Understanding the types of forgiveness options available—both federal and private—can help borrowers navigate their repayment strategies effectively. Here’s a breakdown of the key programs and their unique features.

Federal Forgiveness Programs: Structured Relief for Public Servants and Educators

The Public Service Loan Forgiveness (PSLF) program is one of the most well-known federal options, offering tax-free forgiveness after 120 qualifying payments for borrowers working full-time in government or nonprofit roles. For educators, the Teacher Loan Forgiveness program provides up to $17,500 in relief for those teaching full-time in low-income schools for five consecutive years. Income-Driven Repayment (IDR) plans, such as PAYE or REPAYE, also offer forgiveness after 20–25 years of payments, though the forgiven amount may be taxable. Each program requires meticulous documentation and adherence to specific terms, making it essential to track payments and employment certifications.

Private Loan Forgiveness: Limited but Not Impossible

Private student loans rarely offer forgiveness programs, but exceptions exist. Some lenders, like SoFi or Laurel Road, provide borrower assistance programs for hardships such as disability or death. Additionally, nonprofit organizations like the National Health Service Corps offer loan repayment assistance for private loans in exchange for service commitments. Borrowers should also explore employer-based repayment assistance programs, which some companies offer as a benefit. While less structured than federal options, these avenues require proactive research and negotiation.

Comparing Federal and Private Options: Trade-offs to Consider

Federal forgiveness programs are more comprehensive but demand long-term commitment and strict eligibility. For instance, PSLF requires a decade of public service, while IDR plans tie forgiveness to income and family size. Private options, though rarer, often focus on immediate relief for specific circumstances, such as medical emergencies or career-specific service. Borrowers must weigh the stability of federal programs against the flexibility of private solutions, often combining strategies like refinancing private loans to lower payments while pursuing federal forgiveness.

Practical Steps to Maximize Forgiveness Opportunities

To leverage these programs, borrowers should first identify their loan type—federal or private—and research applicable options. Federal loan holders should consolidate if necessary, enroll in an IDR plan, and submit employment certifications for PSLF. Private loan borrowers should contact lenders directly to inquire about hardship programs or explore third-party assistance. Regularly reviewing program updates and maintaining detailed records of payments and eligibility criteria is crucial. While the process can be complex, strategic planning can turn these programs into powerful tools for debt relief.

Understanding Student Loan Forgiveness: Payments and Eligibility Explained

You may want to see also

Explore related products

![]()

Common scams and red flags to avoid

Scammers often exploit the desperation of student loan borrowers by promising quick relief or complete forgiveness for a fee. One common tactic is the advance fee scam, where fraudsters charge upfront fees for services they claim will eliminate or reduce your debt. Legitimate loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, never require payment to apply. If a company demands money before providing any service, it’s a major red flag. Always verify the program’s legitimacy through official government websites like StudentAid.gov.

Another red flag is unsolicited communication claiming to offer exclusive or time-sensitive forgiveness opportunities. Scammers often use aggressive tactics, such as threatening calls or emails, to pressure borrowers into acting quickly. Legitimate programs do not operate this way. If you receive an unexpected call, email, or text about loan forgiveness, do not provide personal information. Instead, contact your loan servicer directly to confirm the details. Remember, if it feels urgent and suspicious, it’s likely a scam.

Fake debt relief companies often use official-sounding names or logos to appear legitimate. They may claim to be affiliated with the Department of Education or your loan servicer, but these are often ruses to gain your trust. To avoid falling victim, research any company offering loan forgiveness services. Check their credentials, read reviews, and look for complaints with the Better Business Bureau or Federal Trade Commission. A legitimate company will never ask for your FSA ID or pressure you into sharing sensitive information.

Lastly, be wary of promises that sound too good to be true, such as guaranteed forgiveness or immediate debt elimination. Scammers prey on borrowers’ desire for quick solutions, but legitimate forgiveness programs have specific eligibility requirements and timelines. For example, PSLF requires 120 qualifying payments and employment in public service. If a company claims they can bypass these criteria, they’re likely fraudulent. Stick to official channels and consult with your loan servicer or a certified financial advisor for guidance.

Does OSLA Qualify for Student Loan Forgiveness? Key Details Explained

You may want to see also

Explore related products

![]()

Repayment plans tied to forgiveness benefits

However, navigating these plans requires vigilance. Borrowers must recertify their income and family size annually to maintain eligibility, a step often overlooked. Missing this deadline can result in payment increases or removal from the plan, jeopardizing progress toward forgiveness. Additionally, forgiven amounts may be taxed as income, though the American Rescue Plan Act of 2021 temporarily exempts forgiven student loans from taxation through 2025. Borrowers should consult a tax professional to plan for potential liabilities post-2025.

Critics argue that these plans can prolong debt, as low monthly payments may not cover accruing interest, particularly for high-balance borrowers. For instance, someone with $100,000 in loans at 6% interest might see their balance grow under an IDR plan if payments fall short of interest charges. To mitigate this, borrowers should consider making extra payments when possible, targeting loans with the highest interest rates first. This strategy reduces overall interest and shortens the time until forgiveness.

Despite challenges, repayment plans tied to forgiveness benefits remain a viable option for many. Public Service Loan Forgiveness (PSLF) offers a faster route, forgiving remaining balances after 10 years of qualifying payments for those working full-time in government or nonprofit roles. Combining PSLF with an IDR plan can maximize savings, as payments are lower, and forgiveness arrives sooner. Borrowers should use tools like the Department of Education’s Loan Simulator to model scenarios and choose the best plan for their circumstances.

In conclusion, repayment plans tied to forgiveness benefits are legitimate and effective for managing student debt, but success hinges on understanding the rules and staying proactive. By choosing the right plan, recertifying annually, and strategizing payments, borrowers can turn these programs into a lifeline rather than a trap. For those overwhelmed by debt, these plans offer a clear path to financial freedom, provided they commit to the process and leverage available resources.

Teacher Loan Forgiveness: Can Educators Erase Their Student Debt?

You may want to see also

Explore related products

![]()

Success rates and program reliability

Student loan forgiveness programs often promise relief, but their success rates vary widely. For instance, the Public Service Loan Forgiveness (PSLF) program, designed to forgive debt after 10 years of qualifying payments, has historically approved only about 2% of applicants. This low rate stems from stringent eligibility rules, such as requiring employment in a specific public service sector and adherence to precise payment guidelines. Borrowers must meticulously document their payments and employer certifications to avoid disqualification, making the process complex and error-prone.

Analyzing these programs reveals a stark contrast between their intent and execution. Income-Driven Repayment (IDR) plans, which forgive remaining balances after 20–25 years of payments, have higher theoretical success rates but face practical challenges. Many borrowers experience servicing errors, such as misapplied payments or incorrect term calculations, delaying their progress toward forgiveness. A 2021 audit found that some servicers failed to track qualifying payments accurately, leaving borrowers unaware of their standing until it was too late to rectify.

To navigate these pitfalls, borrowers should adopt a proactive strategy. First, verify eligibility for forgiveness programs by consulting official government resources, not third-party services that may charge fees for misinformation. Second, maintain detailed records of all payments and correspondence with loan servicers. Third, annually submit employment certification forms for programs like PSLF to ensure progress is accurately tracked. Finally, consider consolidating loans into a single Direct Loan, as only this type qualifies for most forgiveness programs.

Comparatively, state-based forgiveness programs often boast higher reliability due to their narrower focus and simpler criteria. For example, New York’s “Get on Your Feet” program forgives up to $24,000 for recent graduates earning under $50,000 annually, with a straightforward application process and clear guidelines. Such programs demonstrate that success rates improve when eligibility rules are transparent and administration is localized. Borrowers should explore these options alongside federal programs to maximize their chances of relief.

Ultimately, the reliability of student loan forgiveness programs hinges on borrower diligence and program design. While federal initiatives like PSLF and IDR offer substantial benefits, their complexity and administrative hurdles dampen success rates. State programs, though smaller in scope, provide a more accessible alternative. By understanding these nuances and taking proactive steps, borrowers can tilt the odds in their favor and secure the relief they were promised.

Understanding Student Loan Forgiveness: A Comprehensive Guide for Borrowers

You may want to see also

Frequently asked questions

Yes, legitimate student loan forgiveness programs exist, such as Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment (IDR) plans. However, it’s crucial to verify the program’s authenticity through official government websites like the U.S. Department of Education.

Scams often require upfront fees, promise immediate forgiveness, or ask for personal information like your FSA ID. Legitimate programs are free to apply for and are administered through official government channels.

No, you do not need to pay anyone to apply for student loan forgiveness. You can complete the process yourself through the official Federal Student Aid website or your loan servicer.

No, eligibility varies by program. For example, PSLF requires 10 years of qualifying payments while working full-time for a government or nonprofit organization. Research the specific requirements for each program to determine if you qualify.

No, most federal student loan forgiveness programs, like PSLF and IDR forgiveness, apply only to federal student loans. Private loans are not eligible for these programs, though some private lenders may offer their own relief options.