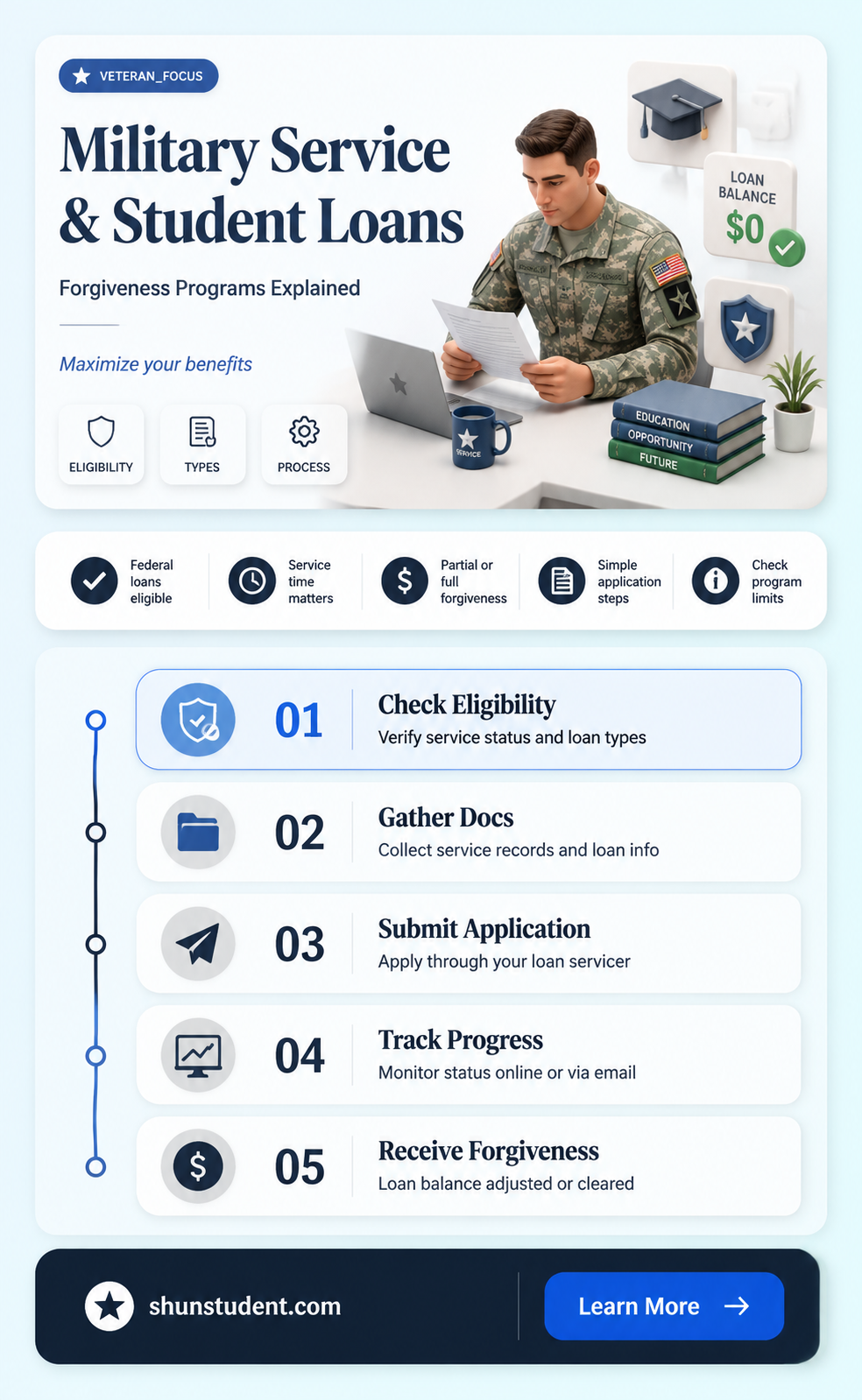

Student loan forgiveness for military service is a critical benefit offered to those who serve in the armed forces, providing financial relief in recognition of their dedication and sacrifice. Under programs like the Public Service Loan Forgiveness (PSLF) and the Department of Defense’s Loan Repayment Program (LRP), eligible service members may have a portion or all of their federal student loans forgiven after completing a specified term of service. Additionally, the Servicemembers Civil Relief Act (SCRA) offers interest rate caps on loans taken out prior to military service. These initiatives aim to ease the financial burden on military personnel, making it easier for them to focus on their duties while pursuing long-term financial stability. However, eligibility criteria and application processes can vary, requiring careful review to maximize these benefits.

| Characteristics | Values |

|---|---|

| Loan Forgiveness Programs | Public Service Loan Forgiveness (PSLF), Military Service-Connected Disability Discharge, Army Loan Repayment Program, Navy Loan Repayment Program, Air Force College Loan Repayment Program, National Guard Loan Repayment Program |

| Eligibility Requirements | Active duty service, completion of required service period, specific military branches, enrollment in income-driven repayment plans (for PSLF) |

| Loan Types Covered | Federal student loans (Direct Loans, FFEL, Perkins Loans) |

| Forgiveness Amount | Up to $65,000 (varies by branch and program), full discharge for permanent disability |

| Service Commitment | Typically 3-4 years of active duty service |

| Application Process | Submit application through the Department of Education or military branch |

| Tax Implications | Forgiveness may be tax-free for military service-connected disability discharge; other programs may have taxable income |

| Impact on Credit Score | No negative impact; forgiven loans are reported as paid in full |

| Availability for Veterans | Yes, for service-connected disabilities or through specific veteran programs |

| Recent Updates (as of 2023) | Expanded eligibility for PSLF and temporary waivers for military personnel |

| Private Loan Forgiveness | Not applicable; only federal student loans are eligible |

| Repayment Assistance | Loan repayment programs offer up to 33% of loan balance annually |

| Disability Discharge Requirements | 100% service-connected disability verified by the Department of Veterans Affairs |

| Program Duration | Varies; PSLF requires 10 years of qualifying payments, military programs are shorter |

| Branch-Specific Benefits | Army, Navy, Air Force, and National Guard offer unique loan repayment programs |

Explore related products

$15.74 $20

What You'll Learn

![]()

Active Duty Loan Forgiveness

Serving in the military offers a unique pathway to student loan forgiveness through the Active Duty Loan Forgiveness program, a benefit designed to ease the financial burden on service members. This program is part of the broader Public Service Loan Forgiveness (PSLF) initiative but with specific criteria tailored for military personnel. To qualify, individuals must serve in the military full-time, which includes active duty in the Army, Navy, Air Force, Marine Corps, or Coast Guard. Each year of full-time service can contribute toward the 120 qualifying payments required for PSLF, significantly accelerating the timeline for loan forgiveness. For example, a service member who completes four years of active duty could potentially reduce their required payments from 10 years to six years, provided they meet all other PSLF criteria.

The process to leverage Active Duty Loan Forgiveness begins with ensuring your loans are eligible. Only Direct Loans qualify for PSLF, so consolidating other federal loans into a Direct Consolidation Loan may be necessary. While on active duty, service members can also take advantage of the Servicemembers Civil Relief Act (SCRA), which caps interest rates on federal student loans at 6% during service. This reduces the overall cost of the loan while the borrower focuses on making qualifying payments. It’s crucial to submit an Employer Certification Form annually or when changing duty stations to document your service and ensure your payments count toward forgiveness.

One of the most compelling aspects of Active Duty Loan Forgiveness is its flexibility. Unlike traditional PSLF, which requires 10 years of payments, military service members can combine their active duty years with civilian public service employment to meet the 120-payment threshold. For instance, a veteran who serves four years on active duty and then works six years in a qualifying public service role could achieve loan forgiveness. This hybrid approach maximizes the benefit of military service while providing a clear path to financial freedom.

However, there are pitfalls to avoid. First, ensure your loan servicer is accurately tracking your qualifying payments. Errors in payment counting are common, so regularly review your account and submit certification forms on time. Second, be mindful of the tax implications of loan forgiveness. While PSLF is tax-free, forgiven amounts under other programs, such as income-driven repayment plans, may be taxable. Lastly, stay informed about policy changes. Military-specific benefits, like the Military Service Loan Deferment, can complement active duty forgiveness but require proactive management to avoid unnecessary interest accrual.

In conclusion, Active Duty Loan Forgiveness is a powerful tool for military service members seeking to eliminate student debt. By understanding eligibility requirements, combining benefits like SCRA interest caps, and strategically planning qualifying payments, service members can maximize this opportunity. Whether serving four years or a full career, this program offers a tangible way to honor the sacrifices of military personnel while providing a pathway to financial stability.

Does Biden's Loan Forgiveness Include Private Student Loans?

You may want to see also

Explore related products

$14.85 $19.99

$13.97 $22.95

![]()

National Guard Repayment Programs

Serving in the National Guard can unlock unique opportunities to manage or reduce student loan debt through specialized repayment programs. Unlike active-duty military, National Guard members often balance civilian careers with part-time service, making these programs particularly valuable for those seeking financial relief without full-time military commitment. The National Guard Student Loan Repayment Program (SLRP) stands out as a cornerstone initiative, offering up to $50,000 in loan repayment for eligible members. To qualify, individuals must enlist for a minimum of six years, score 50 or higher on the Armed Services Vocational Aptitude Battery (ASVAB), and have existing federal student loans. This program is not automatic; applicants must opt in during the enlistment process, emphasizing the importance of proactive planning.

While the SLRP is a powerful tool, it’s not the only option. The National Guard Educational Assistance Program (GEAP) provides additional financial support for tuition, fees, and other educational expenses, indirectly easing the burden of student loans. Though GEAP funds cannot be directly applied to loan repayment, they free up personal finances by covering educational costs. Another lesser-known benefit is the Loan Interest Payment Program (LIPP), which caps interest rates at 6% for eligible Guard members called to active duty. This prevents loan balances from ballooning during service, offering long-term savings. Each program has distinct eligibility criteria, requiring careful review to maximize benefits.

Comparing these programs reveals a strategic approach to debt management. SLRP offers direct repayment but requires a longer service commitment, while GEAP and LIPP provide indirect relief with shorter-term obligations. For example, a Guard member with $30,000 in loans might prioritize SLRP for substantial reduction, whereas someone nearing loan payoff could benefit more from LIPP’s interest caps. Practical tips include verifying loan eligibility (only federal loans qualify for SLRP) and maintaining good standing in the Guard to avoid benefit forfeiture. Combining these programs with federal initiatives like Public Service Loan Forgiveness (PSLF) can further accelerate debt-free goals.

A critical caution is the potential tax implications of SLRP payments, which are considered taxable income. Recipients should budget accordingly or consult a tax professional to avoid unexpected liabilities. Additionally, Guard members must remain vigilant about program deadlines and documentation, as missed paperwork can delay or disqualify benefits. Despite these complexities, National Guard repayment programs offer a structured pathway to financial freedom for those willing to navigate their intricacies. By aligning service commitments with financial goals, Guard members can turn their student debt into a manageable—or even forgivable—burden.

Navient Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) Eligibility

Military service members and veterans often wonder if their student loans can be forgiven as a benefit of their service. While there are specific programs tailored for military personnel, such as the Military Service Member Loan Forgiveness and the Department of Defense Education Benefits, another pathway to loan forgiveness is the Public Service Loan Forgiveness (PSLF) program. This federal initiative offers a unique opportunity for those who commit to public service careers, including military service, to have their student loans forgiven after meeting certain criteria. Understanding PSLF eligibility is crucial for maximizing this benefit.

To qualify for PSLF, borrowers must make 120 qualifying payments while working full-time for a qualifying employer. For military service members, this includes employment with the federal government, the U.S. military, or a 501(c)(3) nonprofit organization. Active-duty service members often meet the full-time employment requirement, even if their work hours vary due to deployment or training. It’s essential to ensure your loans are in the Direct Loan Program, as only these loans are eligible for PSLF. If you have Federal Family Education Loans (FFEL) or Perkins Loans, consolidating them into a Direct Consolidation Loan is a necessary step to qualify.

One common misconception is that military service automatically qualifies for PSLF. While military service can count toward the required 10 years of public service, it’s not automatic. Borrowers must actively submit the Employer Certification Form periodically to confirm their employment qualifies. This form is critical for tracking progress and ensuring payments are counted toward forgiveness. Additionally, payments made under certain repayment plans, such as the Standard Repayment Plan, do not qualify; borrowers must enroll in an income-driven repayment plan to ensure their payments count.

For military spouses, PSLF eligibility can also be a viable option if they work in qualifying public service roles. This flexibility allows families to strategize their loan repayment, potentially doubling the benefits if both partners pursue PSLF. However, careful planning is required, as switching jobs or repayment plans can disrupt the 120-payment count. Using tools like the PSLF Help Tool provided by the U.S. Department of Education can simplify the process and ensure compliance with program requirements.

In conclusion, while military service itself does not guarantee student loan forgiveness, it can be a significant step toward achieving PSLF. By understanding the eligibility criteria, consolidating loans if necessary, and maintaining consistent qualifying employment and payments, service members can leverage this program to eliminate their student debt. Proactive management and regular certification of employment are key to success in the PSLF program.

Steps to Obtain Your Student Loan Forgiveness Copy Easily

You may want to see also

Explore related products

$26.99 $42.93

![]()

Loan Deferment During Deployment

Military deployment often brings financial strain, but student loan deferment can provide a crucial lifeline. During active duty, service members are eligible for mandatory deferment, which pauses federal student loan payments without accruing interest. This benefit, outlined in the Higher Education Act, applies to loans taken out before enlistment and remains in effect for the duration of service plus an additional 13 months. To initiate deferment, submit a copy of your military orders to your loan servicer, ensuring uninterrupted relief during deployment.

While deferment offers immediate financial breathing room, it’s not a one-size-fits-all solution. For instance, interest continues to accrue on unsubsidized loans during deferment, potentially increasing the total repayment amount. Service members with such loans may consider paying the interest during deployment to avoid capitalization. Additionally, private student loans are not bound by federal deferment rules, requiring borrowers to negotiate terms directly with lenders. Understanding these nuances ensures deferment serves as a strategic tool rather than a temporary band-aid.

Deferment also intersects with other military benefits, such as the Public Service Loan Forgiveness (PSLF) program. Each month in deferment counts toward the 120 qualifying payments required for PSLF, provided the borrower is employed full-time by a qualifying employer, such as the military. This synergy can accelerate loan forgiveness for those planning long-term military careers. However, meticulous record-keeping and timely recertification of employment are essential to avoid disqualifications.

Practical steps maximize the benefits of deferment during deployment. First, confirm eligibility by reviewing your loan type and enlistment date. Next, notify your loan servicer promptly with official military orders to activate deferment. For private loans, contact lenders early to explore deferment or forbearance options. Finally, monitor your loan status regularly, even while deployed, to address any administrative errors or unexpected interest accrual. Proactive management transforms deferment from a passive benefit into an active financial strategy.

How Consolidating Student Loans Impacts Loan Forgiveness Eligibility Explained

You may want to see also

Explore related products

![The Royal Edinburgh Military Tattoo 2010 [DVD]](https://m.media-amazon.com/images/I/71VfXOpGP9L._AC_UY218_.jpg)

![]()

Veterans Total and Permanent Disability Discharge

For veterans grappling with total and permanent disabilities, the burden of student loan debt can exacerbate financial strain during an already challenging period. Fortunately, the Total and Permanent Disability (TPD) Discharge program offers a pathway to relief, specifically tailored to those whose service-related injuries or illnesses have left them unable to work. This federal initiative, administered by the U.S. Department of Education, eliminates federal student loan debt for eligible veterans, providing a critical safety net for those who have sacrificed for their country.

To qualify, veterans must demonstrate that their disability is both total and permanent, a designation typically confirmed by the U.S. Department of Veterans Affairs (VA). A VA disability rating of 100% Permanent and Total (P&T) automatically qualifies a veteran for TPD discharge. Alternatively, veterans can submit documentation from a physician certifying their inability to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously for at least 60 months or result in death. This process requires precision; incomplete applications are a common pitfall, so veterans should ensure all medical and VA documentation is thorough and up-to-date.

Once approved, the discharge covers Direct Loans, Federal Family Education Loan (FFEL) Program loans, and Perkins Loans, but not private student loans. Veterans should also be aware of the post-discharge monitoring period, during which they must refrain from earning above the poverty guideline for a family of two in their state and avoid taking new federal student loans or TEACH Grant service obligations. Failure to comply could result in loan reinstatement, though this monitoring period is waived for veterans with a 100% P&T rating from the VA.

A lesser-known benefit is the tax-free status of TPD discharges for veterans. Unlike other loan forgiveness programs, discharged amounts are not considered taxable income for those with a 100% P&T rating, alleviating a potential financial burden. Veterans should consult a tax professional to ensure compliance with any state-specific tax laws, as some states may treat discharged debt differently.

In summary, the Veterans Total and Permanent Disability Discharge is a vital resource for disabled veterans, offering not just debt relief but also a measure of financial stability. By understanding the eligibility criteria, application process, and post-discharge requirements, veterans can navigate this program effectively, securing the support they deserve. For those who have given so much, this program stands as a testament to the nation’s commitment to honoring their service.

PA Social Workers: Student Loan Forgiveness Options Explained

You may want to see also

Frequently asked questions

No, only federal student loans are eligible for forgiveness through military service programs like the Public Service Loan Forgiveness (PSLF) or specific military-related forgiveness options. Private student loans are not covered.

Requirements vary by program. For example, the Army Loan Repayment Program (LRP) may offer up to $65,000 in loan repayment over three years of active duty service, while other programs like PSLF require 10 years of qualifying service, including military service in a public service role.

Yes, National Guard and Reserve members may qualify for student loan forgiveness through programs like the National Guard Student Loan Repayment Program (SLRP), which offers up to $50,000 in loan repayment for six years of service, or through federal programs like PSLF if their service meets the criteria.