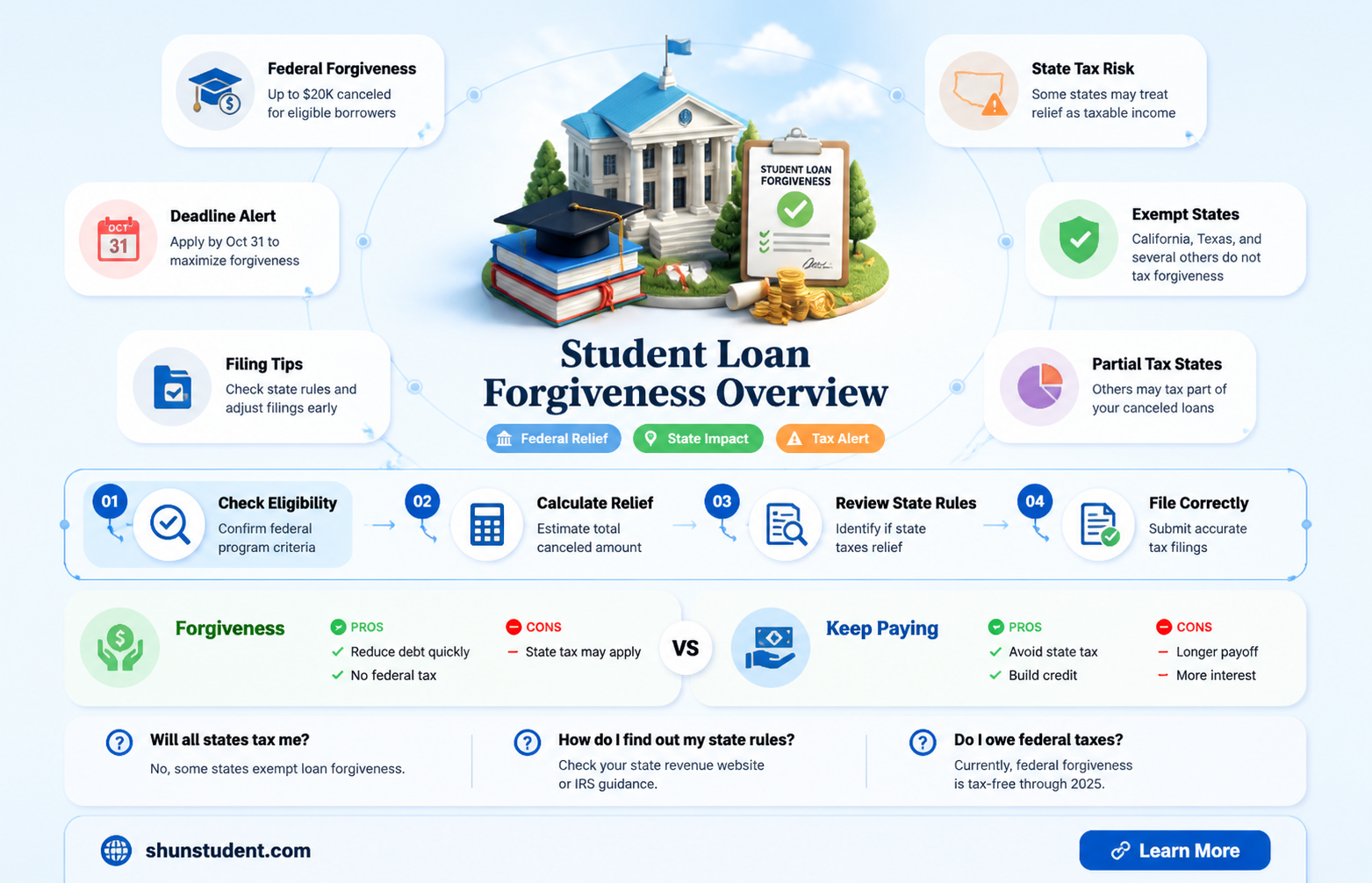

The recent wave of student loan forgiveness initiatives has sparked a critical debate: are states taxing the forgiven debt as income? While the federal government has deemed forgiven student loans tax-free under the American Rescue Plan Act of 2021, some states have not aligned their tax codes accordingly. This discrepancy means borrowers in certain states may face unexpected tax liabilities on their forgiven debt, potentially undermining the financial relief intended by these programs. As a result, borrowers must navigate a complex patchwork of state tax laws, raising questions about equity and the true impact of loan forgiveness efforts.

| Characteristics | Values |

|---|---|

| Federal Tax Treatment | Student loan forgiveness is generally not considered taxable income at the federal level under the American Rescue Plan Act of 2021 (through 2025). |

| State Tax Treatment | Varies by state; some states follow federal guidelines, while others may tax forgiven student loans as income. |

| States Taxing Forgiveness (as of 2023) | Arkansas, Mississippi, North Carolina, and Wisconsin (may require recipients to pay state taxes on forgiven amounts). |

| States Not Taxing Forgiveness | Most states align with federal rules and do exclude forgiven student loans from taxable income. |

| Public Service Loan Forgiveness (PSLF) | Typically not taxed at the federal level; state treatment varies. |

| Income-Driven Repayment (IDR) Forgiveness | Federal tax exclusion applies; state treatment depends on local laws. |

| State Legislation Trends | Some states are considering or have passed laws to conform to federal exclusion, while others maintain taxation. |

| Impact on Borrowers | Borrowers in taxing states may face unexpected state tax liabilities despite federal exclusion. |

| Advocacy Efforts | Organizations and lawmakers are pushing for state-level conformity to federal tax-free treatment. |

| Future Changes | State tax policies may evolve as federal student loan forgiveness programs expand or change. |

Explore related products

$10.1 $16.99

What You'll Learn

![]()

Federal vs. State Tax Treatment

The federal government's exclusion of student loan forgiveness from taxable income under the American Rescue Plan Act of 2021 created a uniform rule, but states have responded with varying degrees of conformity. This divergence stems from how states align with federal tax codes, with some automatically adopting federal changes and others maintaining independent tax laws. For instance, states like California and New York have conformed to the federal exclusion, ensuring residents aren’t taxed on forgiven amounts. Conversely, states like North Carolina and Wisconsin have not conformed, treating forgiven student loans as taxable income. This patchwork of state responses underscores the importance of understanding local tax laws to accurately plan for potential liabilities.

Analyzing the rationale behind state decisions reveals a tension between fiscal priorities and taxpayer relief. States that tax forgiven loans often cite revenue needs, particularly in the wake of economic challenges like the COVID-19 pandemic. For example, Indiana, which taxes forgiven student loans, has defended its stance by emphasizing the need to fund public services. In contrast, states like Pennsylvania, which excludes forgiven loans from taxation, argue that aligning with federal policy reduces administrative burdens and provides financial relief to residents. This divide highlights how state tax treatment of student loan forgiveness reflects broader economic and political priorities.

For taxpayers, navigating this federal-state discrepancy requires proactive steps. First, determine your state’s conformity status by consulting its Department of Revenue or a tax professional. If your state taxes forgiven loans, calculate the potential liability using the forgiven amount and your state’s tax rate. For example, if $10,000 is forgiven and your state tax rate is 5%, you’d owe $500. Second, explore mitigation strategies, such as contributing to tax-advantaged accounts or claiming deductions to offset the additional liability. Finally, stay informed about legislative changes, as state policies can evolve in response to federal actions or local advocacy.

A comparative analysis of state approaches reveals trends tied to political leanings and economic conditions. Blue states, like Massachusetts and Illinois, are more likely to conform to federal exclusions, aligning with a broader policy of supporting debt relief. Red states, such as Mississippi and Arkansas, often diverge, reflecting a preference for limited government intervention and fiscal conservatism. However, exceptions exist, such as Utah, a red state that excludes forgiven loans, demonstrating that local factors like education policy and taxpayer demographics also play a role. This comparison underscores that while federal policy sets a baseline, state treatment of student loan forgiveness is shaped by a complex interplay of ideology and practicality.

In conclusion, the federal exclusion of student loan forgiveness from taxable income has not eliminated state-level taxation, creating a landscape where outcomes vary widely by location. Taxpayers must research their state’s stance, calculate potential liabilities, and explore strategies to minimize impact. Policymakers, meanwhile, face the challenge of balancing revenue needs with the goal of providing relief to borrowers. As student debt remains a pressing issue, the federal-state divide in tax treatment will likely continue to evolve, making it a critical area to watch for both individuals and advocates.

Qualifying for Student Loan Forgiveness: Is It Really That Easy?

You may want to see also

Explore related products

![]()

State-Specific Tax Laws on Forgiveness

The tax treatment of student loan forgiveness varies significantly across states, creating a patchwork of rules that borrowers must navigate. While federal law generally excludes forgiven student loans from taxable income through 2025, states are not bound by this provision. As a result, some states align with federal guidelines, offering tax-free forgiveness, while others treat forgiven amounts as taxable income. This disparity underscores the importance of understanding your state’s specific tax laws to avoid unexpected liabilities.

For instance, states like California, New York, and Pennsylvania have conformed to federal law, ensuring that forgiven student loans remain tax-exempt at the state level. Borrowers in these states can breathe easier, knowing their financial relief won’t be offset by additional taxes. However, states like Indiana and North Carolina take a different approach, taxing forgiven amounts as income. This divergence highlights the need for borrowers to consult state-specific tax codes or a tax professional to determine their obligations.

One particularly complex scenario arises in states that partially conform to federal law or have unique exemptions. For example, Massachusetts exempts forgiven student loans only if the borrower works in certain public service professions. Such conditional exemptions require careful scrutiny of eligibility criteria. Borrowers in these states must not only track their loan forgiveness status but also ensure they meet any additional requirements to qualify for tax relief.

Practical steps for borrowers include monitoring state legislative updates, as tax laws can change annually. Tools like state tax agency websites or tax software can provide current information. Additionally, maintaining detailed records of loan forgiveness documentation is crucial for both federal and state tax filings. For those in states with unfavorable tax treatment, exploring deductions or credits may help offset the burden. Ultimately, proactive research and planning are key to managing the state tax implications of student loan forgiveness.

Am I Eligible for Federal Student Loan Forgiveness? A Guide

You may want to see also

Explore related products

![]()

Impact on State Revenue Streams

The taxation of student loan forgiveness by states introduces a complex dynamic into their revenue streams, blending fiscal policy with social equity considerations. When the federal government forgives student debt, the forgiven amount is often treated as taxable income at the federal level. However, states vary in their treatment of this income, creating a patchwork of outcomes. Some states, like California and New York, conform to federal tax laws, automatically taxing forgiven student loans as income. Others, such as Pennsylvania and Massachusetts, exclude forgiven student debt from taxable income, either through specific exemptions or broader tax structures. This divergence directly impacts state revenue, with conforming states gaining additional tax dollars and non-conforming states forgoing potential income to align with equity goals.

Consider the scale of impact: if a state with 100,000 residents eligible for $10,000 in student loan forgiveness conforms to federal taxation, it could generate millions in additional revenue, depending on state tax rates. For example, a 5% state income tax rate would yield $50 million in revenue from this cohort alone. Conversely, states opting not to tax forgiven loans sacrifice this revenue but may prioritize alleviating financial burdens on residents. Policymakers must weigh these trade-offs, balancing immediate fiscal gains against long-term economic benefits of debt-free households, such as increased consumer spending and homeownership rates.

A comparative analysis reveals strategic considerations for states. For instance, states with high student debt burdens, like New Hampshire and Maine, might face greater pressure to exempt forgiven loans from taxation to retain younger, educated residents. In contrast, states with robust budgets or lower debt averages may view taxation as a low-risk revenue opportunity. Additionally, states with progressive tax structures could mitigate the regressive impact of taxing forgiveness by reinvesting the revenue into education or financial aid programs, creating a feedback loop of support for lower-income residents.

Practical steps for states navigating this issue include conducting fiscal impact analyses to quantify potential revenue gains or losses, engaging stakeholders like higher education institutions and advocacy groups, and exploring hybrid approaches. For example, a state might tax forgiven loans above a certain threshold, exempting modest amounts to protect low-income borrowers. Transparency in decision-making is critical, as residents need to understand how state policies will affect their financial obligations. States should also monitor federal developments, as changes in federal tax treatment of forgiven loans could necessitate state-level adjustments.

Ultimately, the taxation of student loan forgiveness is not merely a revenue question but a reflection of a state’s priorities. States must decide whether to align with federal policy for fiscal consistency or diverge to address local economic and social needs. By carefully assessing their unique contexts and adopting targeted strategies, states can navigate this issue in a way that supports both their revenue streams and their residents’ financial well-being.

Trump's Student Loan Forgiveness: What It Means for VA Borrowers

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![]()

Borrower Tax Liability Variations

The tax implications of student loan forgiveness vary significantly across states, creating a patchwork of borrower liabilities that demand careful navigation. While the federal government excludes forgiven student loans from taxable income through 2025 under the American Rescue Plan Act, state tax laws diverge sharply. For instance, states like California and New York align with federal treatment, exempting forgiven amounts from state income tax. In contrast, states such as Mississippi and North Carolina treat forgiven loans as taxable income, potentially saddling borrowers with unexpected state tax bills. This disparity underscores the importance of understanding state-specific rules to avoid financial surprises.

Consider the case of a borrower in Indiana, where forgiven student loans are subject to state income tax. If a borrower receives $50,000 in loan forgiveness, they could face a state tax liability of approximately $2,500, assuming a 5% state tax rate. Conversely, a borrower in Pennsylvania would owe no state tax on the same forgiven amount. Such variations highlight the need for borrowers to consult state tax codes or a tax professional to accurately estimate their liability. Practical tip: Use online tax calculators or state revenue department resources to model potential tax obligations based on your location and forgiven amount.

Another layer of complexity arises from states that partially conform to federal tax treatment. For example, Massachusetts excludes forgiven student loans from state tax only if the borrower works in certain public service professions. Borrowers in such states must scrutinize eligibility criteria to determine their tax liability. Caution: Misinterpreting state-specific rules can lead to underpayment penalties and interest charges. Always verify the latest tax laws, as states may update their policies in response to federal changes or economic conditions.

To mitigate state tax liabilities, borrowers can explore strategic planning options. For instance, timing the recognition of forgiven income to align with lower-income years can reduce tax brackets and, consequently, state tax obligations. Additionally, borrowers in high-tax states may consider relocating to a state with more favorable tax treatment, though this decision should weigh factors like cost of living and employment opportunities. Takeaway: Proactive tax planning and awareness of state variations are essential to managing the financial impact of student loan forgiveness.

In summary, borrower tax liability variations across states create a complex landscape for those benefiting from student loan forgiveness. By understanding state-specific rules, leveraging planning strategies, and seeking professional guidance, borrowers can navigate this terrain effectively. Ignoring these differences risks unforeseen tax burdens, while informed action ensures financial stability in the wake of loan forgiveness.

Is Forgiven Student Loan Debt Taxable? What Borrowers Need to Know

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![]()

Legislative Responses to Tax Concerns

As the federal government implements student loan forgiveness programs, a patchwork of state-level tax policies has emerged, creating confusion and inequity for borrowers. Some states, such as Indiana and North Carolina, have explicitly exempted forgiven student loan debt from state taxation, aligning with the federal tax-free treatment under the American Rescue Plan Act. However, other states, like Mississippi and Wisconsin, have not taken legislative action, leaving borrowers subject to state taxes on forgiven amounts. This disparity highlights the need for clear and consistent legislative responses to address tax concerns related to student loan forgiveness.

To mitigate the tax burden on borrowers, several states have introduced legislation to conform to federal tax treatment. For instance, California passed Assembly Bill 1279, which exempts forgiven student loan debt from state taxation for tax years 2021 through 2025. Similarly, New York enacted Senate Bill S7507C, providing a state tax exclusion for forgiven student loans. These legislative actions demonstrate a proactive approach to ensuring that borrowers do not face unexpected tax liabilities. States considering similar measures should carefully review their tax codes and consult with stakeholders to craft targeted solutions that balance fiscal responsibility with borrower relief.

A comparative analysis of state responses reveals two primary approaches: full conformity with federal tax treatment and partial or conditional exemptions. States like Pennsylvania and Virginia have adopted full conformity, ensuring seamless alignment with federal policy. In contrast, states such as Arkansas and Minnesota have implemented partial exemptions, often limiting the exclusion to specific types of loans or income thresholds. While partial exemptions may address budgetary constraints, they can also introduce complexity and reduce the overall benefit to borrowers. Policymakers must weigh these trade-offs when designing legislative responses, prioritizing clarity and fairness.

Advocates for borrower-friendly tax policies argue that states should prioritize long-term economic benefits over short-term revenue gains. By exempting forgiven student loan debt from taxation, states can stimulate local economies as borrowers redirect savings toward consumer spending, housing, and entrepreneurship. For example, a study by the Roosevelt Institute estimates that widespread student debt cancellation could boost GDP by $86 billion to $108 billion annually. To maximize these benefits, states should consider pairing tax exemptions with complementary initiatives, such as financial literacy programs or small business grants, to support borrowers in achieving financial stability.

Despite progress in some states, challenges remain in achieving uniform legislative responses. States with limited budgets or competing priorities may hesitate to forgo tax revenue, even if it means burdening vulnerable borrowers. Additionally, the temporary nature of some federal tax exclusions complicates state-level decision-making, as policymakers must anticipate future changes. To address these challenges, federal and state governments should collaborate on long-term solutions, such as extending the tax-free treatment of student loan forgiveness or providing financial incentives for states to adopt borrower-friendly policies. By working together, they can create a more equitable and supportive environment for student loan borrowers nationwide.

Student Loan Debt Forgiveness: Has the Process Finally Begun?

You may want to see also

Frequently asked questions

It depends on your state. Some states follow federal tax treatment and exclude forgiven student loans from taxable income, while others may tax the forgiven amount. Check your state’s tax laws or consult a tax professional for clarity.

As of recent updates, states like Mississippi, North Carolina, and Arkansas have indicated they may tax forgiven student loans. However, this can change, so verify with your state’s revenue department or a tax expert.

If your state taxes forgiven loans, there’s typically no way to avoid it unless you qualify for a state-specific exemption. Review your state’s tax code or seek advice from a tax professional to explore any potential options.

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)