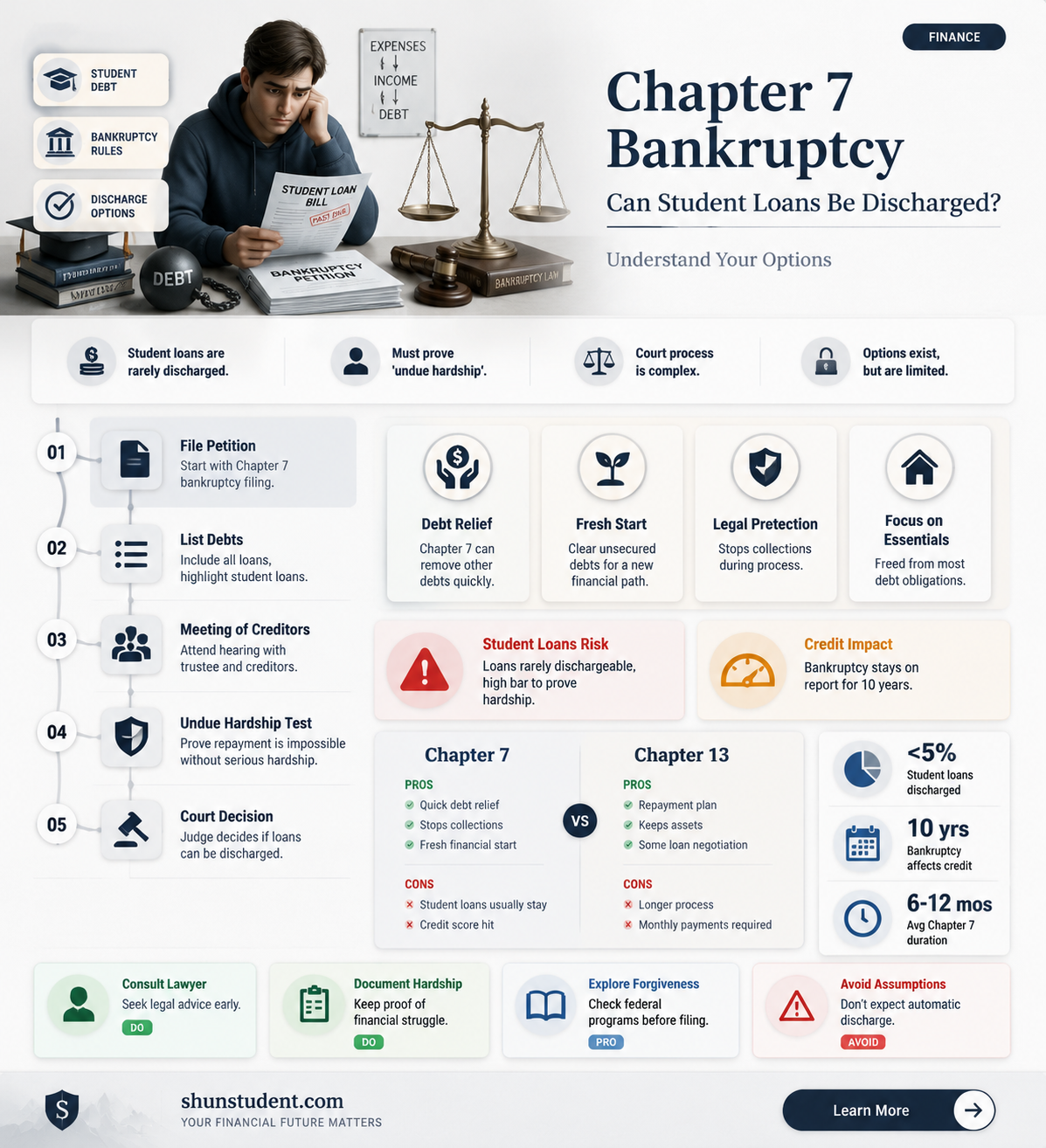

Chapter 7 bankruptcy is often seen as a last resort for individuals overwhelmed by debt, but it raises important questions for those burdened by student loans. One of the most pressing concerns is whether student loans can be discharged or forgiven through this process. Unlike other types of unsecured debt, such as credit card balances, student loans are notoriously difficult to eliminate in bankruptcy. Under current U.S. law, discharging student loans in Chapter 7 requires proving undue hardship, a stringent standard that is rarely met. This means that, in most cases, student loans survive bankruptcy, leaving borrowers still responsible for repayment. As a result, individuals considering Chapter 7 must carefully weigh their options, as it may not provide the relief they seek from student loan debt.

| Characteristics | Values |

|---|---|

| Eligibility for Discharge | Extremely rare; requires proving "undue hardship" via the Brunner Test. |

| Brunner Test Criteria | 1. Cannot maintain minimal living standard if forced to repay. |

| 2. Circumstances unlikely to change. | |

| 3. Made good-faith effort to repay loans. | |

| Chapter 7 Bankruptcy Role | Discharges most unsecured debts but does not automatically discharge student loans. |

| Legal Process | Requires filing an adversary proceeding within the bankruptcy case. |

| Success Rate | Low; less than 0.1% of debtors attempt, and fewer succeed. |

| Impact on Credit | Bankruptcy stays on credit report for 10 years; student loans remain. |

| Alternatives | Income-Driven Repayment (IDR), Public Service Loan Forgiveness (PSLF), or Chapter 13 bankruptcy. |

| Recent Changes (as of 2023) | No significant changes to discharge criteria; DOE reviews "undue hardship" cases more flexibly. |

| Documentation Required | Extensive financial records, medical evidence (if applicable), and repayment history. |

| Legal Representation | Highly recommended due to complexity of proving undue hardship. |

Explore related products

What You'll Learn

- Eligibility criteria for student loan discharge in Chapter 7 bankruptcy

- Undue hardship requirements for forgiving student loans in bankruptcy

- Differences between Chapter 7 and Chapter 13 for loan forgiveness

- Role of the Brunner Test in student loan discharge cases

- Alternatives to bankruptcy for managing or reducing student loan debt

![]()

Eligibility criteria for student loan discharge in Chapter 7 bankruptcy

Student loans are notoriously difficult to discharge in bankruptcy, but Chapter 7 offers a narrow path for those facing insurmountable financial hardship. The eligibility criteria are stringent, requiring borrowers to prove that repaying their student loans would impose an "undue hardship" on them and their dependents. This standard, known as the Brunner Test, is a three-part legal hurdle that few successfully clear. First, the borrower must demonstrate that they cannot maintain a minimal standard of living if forced to repay the loans. Second, they must show that this financial hardship is likely to persist for a significant portion of the loan repayment period. Lastly, there must be evidence of good faith efforts to repay the loans in the past. Meeting these criteria often requires extensive documentation, including financial records, medical evidence, and testimony, making it a complex and resource-intensive process.

Consider the case of a 45-year-old single parent with $80,000 in student loan debt, earning $30,000 annually as a teacher’s aide. Despite working full-time, her income barely covers rent, groceries, and childcare, leaving no room for loan payments. Her chronic health condition limits her ability to take on additional work or pursue higher-paying roles. In this scenario, she might meet the first criterion of the Brunner Test, as repaying the loans would force her below a minimal standard of living. However, she would also need to prove that her financial situation is unlikely to improve—perhaps through medical records showing her condition is permanent—and provide a history of unsuccessful attempts to make payments or enroll in income-driven repayment plans.

For those considering this route, it’s critical to understand that success is not guaranteed. Bankruptcy courts interpret "undue hardship" conservatively, and the burden of proof lies entirely with the borrower. Hiring an experienced bankruptcy attorney is essential, as they can help gather the necessary evidence and navigate the legal process. Additionally, borrowers should explore all other options first, such as income-driven repayment plans or loan forgiveness programs, which may provide relief without the need for bankruptcy.

A comparative analysis reveals that Chapter 7 discharge is far more challenging for student loans than for other types of debt, such as credit card debt or medical bills. While unsecured debts are typically wiped out in Chapter 7, student loans are treated as a special category, reflecting their status as a government-backed investment in the borrower’s future earning potential. This distinction underscores the need for a compelling case to overcome the presumption that student loans are nondischargeable.

In conclusion, while Chapter 7 bankruptcy can discharge student loans, the eligibility criteria are exacting and the process demanding. Borrowers must be prepared to demonstrate severe and lasting financial hardship, backed by robust evidence and legal representation. For those facing truly insurmountable odds, it remains a viable, though rare, option for relief.

Police Officers and Student Loan Forgiveness: Eligibility Explained

You may want to see also

Explore related products

![]()

Undue hardship requirements for forgiving student loans in bankruptcy

Student loans are notoriously difficult to discharge in bankruptcy, but Chapter 7 offers a narrow path through the "undue hardship" exception. This legal standard, rooted in the Brunner test, requires debtors to prove three elements: (1) inability to maintain a minimal standard of living if forced to repay the loans, (2) persistence of this condition for most of the repayment period, and (3) good faith efforts to repay the debt. Courts interpret these criteria strictly, often favoring lenders, but successful cases highlight the importance of thorough documentation and strategic legal argumentation.

To navigate this process, debtors must first gather evidence demonstrating their financial incapacity. This includes income statements, medical records (if applicable), and expense documentation. For instance, a 45-year-old debtor with chronic illness, earning $24,000 annually and supporting two dependents, might illustrate how loan payments would leave them below the federal poverty line. Such specifics are critical, as vague claims rarely satisfy the Brunner test. Additionally, debtors should avoid common pitfalls, like failing to exhaust income-driven repayment plans, which courts may view as a lack of good faith.

Persuasively, the undue hardship standard is not just about current financial strain but also about future prospects. A 30-year-old with a degree in a low-paying field, earning $30,000 annually, might argue that their earning potential is unlikely to improve significantly. However, courts often scrutinize younger debtors more closely, expecting them to adapt or retrain. In contrast, older debtors with limited job prospects or disabilities may have a stronger case, as evidenced by rulings like *Hema v. Navient Solutions* (2018), where a 50-year-old with no assets and declining health succeeded.

Comparatively, the undue hardship standard differs from other bankruptcy exemptions, which are more objective. For example, medical debt is often discharged without such rigorous proof. Student loans, however, require a quasi-adversarial process, where debtors must counter lenders' arguments. Hiring an attorney experienced in bankruptcy litigation is advisable, as they can craft arguments tailored to the debtor's unique circumstances and anticipate lender objections. Pro se litigants often struggle to meet the evidentiary burden, underscoring the need for professional guidance.

In conclusion, while the undue hardship requirement is stringent, it is not insurmountable. Debtors must approach it methodically: document financial incapacity, demonstrate long-term hardship, and prove good faith efforts. Practical tips include maintaining detailed financial records, exploring all repayment options beforehand, and seeking legal counsel early. Success stories, though rare, provide a roadmap for those facing insurmountable student debt, proving that with the right strategy, relief is possible.

SCOTUS Decision on Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Differences between Chapter 7 and Chapter 13 for loan forgiveness

Student loan forgiveness under bankruptcy is a complex process, and the type of bankruptcy filed—Chapter 7 or Chapter 13—plays a critical role in determining outcomes. Chapter 7 bankruptcy, often referred to as liquidation bankruptcy, involves selling non-exempt assets to pay off creditors, with any remaining unsecured debts potentially discharged. However, student loans are not automatically discharged in Chapter 7; borrowers must meet the stringent requirements of the Brunner Test, which demands proof of undue hardship. This test is notoriously difficult to pass, making student loan forgiveness under Chapter 7 rare.

In contrast, Chapter 13 bankruptcy, known as reorganization bankruptcy, allows debtors to restructure their debts into a manageable repayment plan over three to five years. While student loans are not typically discharged under Chapter 13, this chapter offers unique advantages. For instance, it can pause collection efforts and reduce the financial burden by prioritizing other debts. Additionally, Chapter 13 provides a mechanism for borrowers to address student loans indirectly by freeing up income through the restructuring of other obligations. This can make it easier to manage student loan payments post-bankruptcy.

One key difference lies in the treatment of disposable income. Under Chapter 7, any disposable income is not directly allocated to student loan repayment, as the focus is on liquidating assets. In Chapter 13, however, disposable income is used to fund the repayment plan, which may indirectly benefit student loan management by reducing overall debt pressure. This distinction highlights how Chapter 13 can offer a more structured approach to financial recovery, even if it doesn’t directly forgive student loans.

Another critical factor is the long-term impact on credit. Chapter 7 remains on a credit report for 10 years, while Chapter 13 stays for 7 years. Borrowers must weigh the immediate relief of Chapter 7 against the potential for a quicker credit recovery under Chapter 13. For those seeking to rebuild credit while managing student loans, Chapter 13’s structured repayment plan may be more advantageous, despite its longer duration.

Ultimately, the choice between Chapter 7 and Chapter 13 for student loan forgiveness depends on individual circumstances. Chapter 7 offers a slim chance of discharge through the Brunner Test but provides immediate debt relief. Chapter 13, while not forgiving student loans, offers tools to manage debt more effectively over time. Borrowers should consult with a bankruptcy attorney to evaluate their financial situation and determine the most strategic path forward.

Are Student Loans Being Forgiven? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Role of the Brunner Test in student loan discharge cases

Student loan debt is a significant burden for many, and Chapter 7 bankruptcy is often seen as a potential solution. However, discharging student loans through bankruptcy is notoriously difficult. This is where the Brunner Test comes into play—a critical legal standard that determines whether a debtor can have their student loans forgiven under Chapter 7.

The Brunner Test, established in the 1987 case *Brunner v. New York State Higher Education Services Corp.*, sets a high bar for student loan discharge. It requires debtors to prove three elements: (1) that maintaining a minimal standard of living is impossible if forced to repay the loans, (2) that this financial hardship will persist for a significant portion of the repayment period, and (3) that the debtor has made good faith efforts to repay the loans. This three-pronged test is stringent, reflecting the policy priority given to ensuring repayment of educational debt.

To illustrate, consider a hypothetical case: a 35-year-old debtor with $100,000 in student loans, earning $30,000 annually, and supporting a child. Under the Brunner Test, they would need to demonstrate that their income is insufficient to cover basic living expenses and loan payments, that this situation is unlikely to improve, and that they’ve attempted to make payments or explore repayment plans. Without meeting all three criteria, their request for discharge would likely be denied.

Practical tips for navigating the Brunner Test include maintaining detailed financial records, documenting all attempts to repay loans, and consulting a bankruptcy attorney experienced in student loan cases. Additionally, debtors should explore alternative repayment options, such as income-driven plans, before pursuing bankruptcy. While the Brunner Test is challenging to satisfy, understanding its requirements and preparing thoroughly can increase the likelihood of a successful discharge.

In conclusion, the Brunner Test serves as a gatekeeper for student loan discharge in Chapter 7 bankruptcy, ensuring that only those facing extreme and persistent hardship qualify for relief. Its rigorous standards underscore the complexity of seeking forgiveness for educational debt, making it essential for debtors to approach this process with careful planning and professional guidance.

Terminal Illness and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Alternatives to bankruptcy for managing or reducing student loan debt

Student loans are rarely discharged in Chapter 7 bankruptcy, requiring debtors to prove "undue hardship" through the stringent Brunner Test. This legal hurdle leaves many borrowers seeking alternative strategies to manage or reduce their debt. Income-driven repayment (IDR) plans, for example, cap monthly payments at a percentage of discretionary income—typically 10-20%—and forgive remaining balances after 20-25 years of consistent payments. For instance, a borrower earning $40,000 annually with $60,000 in loans might pay $300 monthly under the Revised Pay As You Earn (REPAYE) plan, with forgiveness after 240 payments. This approach provides immediate relief and a long-term path to debt elimination without bankruptcy.

Another viable option is pursuing Public Service Loan Forgiveness (PSLF), which forgives federal student loans after 120 qualifying payments while working full-time for a government or nonprofit employer. Teachers, nurses, and social workers often benefit from this program. For example, a teacher earning $50,000 annually could have $50,000 in loans forgiven after 10 years, provided they remain in eligible employment and make payments under an IDR plan. Caution is advised, however, as strict eligibility rules require meticulous documentation and adherence to program guidelines.

Refinancing with a private lender can lower interest rates or monthly payments for borrowers with strong credit and stable income. For instance, refinancing $30,000 in loans from 7% to 4% could save over $5,000 in interest over 10 years. However, this strategy risks losing federal protections like IDR and forgiveness programs. Borrowers should weigh the immediate financial benefits against long-term flexibility before committing to private refinancing.

Employer-assisted repayment programs are an emerging alternative, with companies like Aetna and Fidelity offering contributions toward employee student loans. For example, an employer might contribute $100 monthly toward an employee’s loans, reducing a $30,000 balance by $12,000 over 10 years. Employees should inquire about such benefits during job negotiations or annual reviews, as these programs can significantly accelerate debt repayment without personal financial strain.

Finally, strategic side hustles or gig work can generate extra income to pay down loans faster. A borrower earning $500 monthly from freelance writing or ride-sharing could apply this entirely to principal, reducing a $20,000 loan by $6,000 in a year. This approach requires discipline but offers control over debt reduction timelines without relying on external programs or legal processes. Each alternative demands careful consideration of individual circumstances, but collectively, they provide pathways to manage student debt outside the uncertain realm of bankruptcy.

Can Federal Student Aid Center Assist with Loan Forgiveness?

You may want to see also

Frequently asked questions

No, student loans are not automatically forgiven in Chapter 7 bankruptcy. They are typically considered nondischargeable unless you can prove undue hardship through an adversary proceeding.

The undue hardship test (Brunner Test) requires proving: (1) you cannot maintain a minimal standard of living if forced to repay, (2) your financial situation is unlikely to change, and (3) you’ve made good faith efforts to repay the loans.

Yes, filing for Chapter 7 triggers an automatic stay, which temporarily halts most collection actions, including wage garnishments and lawsuits related to student loans.

No, it is rare. The undue hardship standard is very strict, and most borrowers do not meet the criteria. Only a small percentage of cases result in full or partial student loan discharge.

Yes, Chapter 7 can discharge unsecured debts like credit cards and medical bills, potentially freeing up income to manage student loan payments, but the student loans themselves remain unless forgiven through undue hardship.