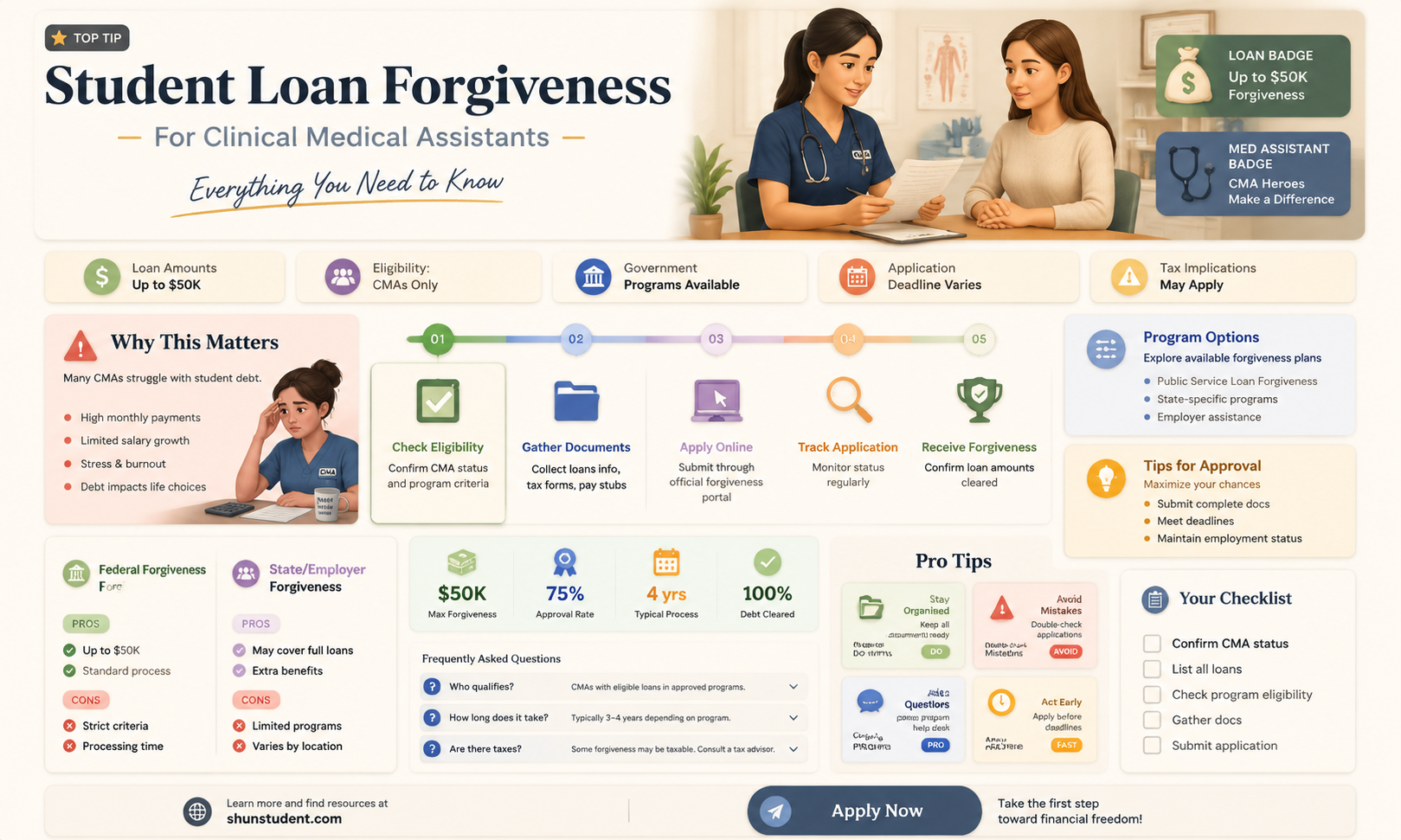

Student loan forgiveness for clinical medical assistants is a topic of significant interest, particularly as healthcare professionals seek financial relief amidst rising educational costs. While clinical medical assistants play a crucial role in healthcare settings, they are generally not eligible for the same broad loan forgiveness programs available to other medical professionals, such as doctors or nurses. However, they may qualify for certain federal programs like Public Service Loan Forgiveness (PSLF) if they work for a qualifying employer, such as a government or non-profit organization, and meet specific criteria. Additionally, some states and employers offer loan repayment assistance programs tailored to healthcare workers, including medical assistants, to address workforce shortages and support those in underserved areas. Understanding these options requires careful research and consultation with financial advisors to navigate the complexities of loan forgiveness programs.

| Characteristics | Values |

|---|---|

| Eligibility for Loan Forgiveness | Clinical Medical Assistants (CMAs) may be eligible for student loan forgiveness through specific programs, but it is not automatic. |

| Primary Forgiveness Programs | 1. Public Service Loan Forgiveness (PSLF): Requires 120 qualifying payments while working full-time for a qualifying employer (e.g., government, non-profit, or certain healthcare organizations). 2. Income-Driven Repayment (IDR) Forgiveness: After 20-25 years of payments under an IDR plan, remaining balance may be forgiven, but taxable as income. |

| Employer Requirements | Must work for a qualifying employer (e.g., 501(c)(3) non-profit, government, or specific healthcare facilities) for PSLF. |

| Loan Type Eligibility | Only federal student loans (e.g., Direct Loans) qualify for PSLF and IDR forgiveness; private loans are ineligible. |

| Certification Process | Annual submission of the PSLF Employment Certification Form is recommended to track eligibility. |

| Tax Implications | PSLF forgiveness is tax-free, but IDR forgiveness is taxed as income. |

| State-Specific Programs | Some states offer loan repayment assistance programs (LRAPs) for healthcare workers, including CMAs, based on location and employer. |

| Additional Requirements | Must maintain full-time employment and make consistent, qualifying payments during the forgiveness period. |

| Private Loan Options | No forgiveness programs for private loans; CMAs with private loans may explore refinancing or employer-based repayment assistance. |

| Recent Updates | As of 2023, no new federal programs specifically target CMAs for loan forgiveness, but existing programs remain available. |

Explore related products

What You'll Learn

![]()

Federal vs. Private Loan Forgiveness

Clinical medical assistants seeking student loan forgiveness face starkly different paths depending on whether their loans are federal or private. Federal loans offer structured forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, which can eliminate debt after 10–25 years of qualifying payments. For instance, working full-time in a nonprofit hospital or government clinic could qualify a medical assistant for PSLF, provided they make 120 eligible payments. Private loans, however, rarely offer forgiveness options. Lenders like Sallie Mae or Discover typically require full repayment unless borrowers negotiate a settlement, which is uncommon and often requires financial hardship proof. This fundamental difference underscores the importance of understanding loan type before pursuing forgiveness.

To maximize forgiveness opportunities, clinical medical assistants should prioritize federal loans during their education. Federal Direct Loans, for example, are eligible for PSLF, whereas private loans are not. A strategic approach involves borrowing exclusively through federal programs and certifying employment annually for PSLF. For those already burdened with private loans, refinancing into a federal loan is not possible, but exploring employer-assisted repayment programs or state-based loan repayment assistance programs (LRAPs) can provide partial relief. For instance, the National Health Service Corps offers up to $50,000 in loan repayment for two years of service in a Health Professional Shortage Area (HPSA).

Income-driven repayment plans, such as Revised Pay As You Earn (REPAYE), offer another federal forgiveness avenue. These plans cap monthly payments at 10–20% of discretionary income and forgive remaining balances after 20–25 years. For a medical assistant earning $35,000 annually, REPAYE could reduce monthly payments to as low as $150, with forgiveness kicking in after 240 payments. Private loans, in contrast, often lock borrowers into fixed or variable rates without income-based adjustments, making long-term repayment more burdensome. This disparity highlights why federal loans are the preferred choice for those anticipating a career in public service or low-income healthcare roles.

Despite federal programs’ advantages, pitfalls exist. PSLF requires meticulous documentation, and errors in payment counting or employer certification can disqualify applicants. For example, payments made under the wrong repayment plan (e.g., Graduated Repayment instead of an IDR plan) do not count toward PSLF. Similarly, IDR forgiveness triggers taxable income, potentially resulting in a substantial bill unless borrowers plan ahead. Private loans, while less forgiving, offer simplicity: borrowers know exactly what they owe and when. For clinical medical assistants, the trade-off between federal forgiveness complexity and private loan predictability hinges on career trajectory and financial discipline.

In conclusion, federal loans provide clinical medical assistants with viable pathways to loan forgiveness, particularly through PSLF and IDR plans, but require careful navigation. Private loans offer no such relief, making them a riskier choice for those in low-paying healthcare roles. By strategically selecting federal loans, certifying employment, and enrolling in IDR plans, medical assistants can position themselves for long-term financial relief. For those already in private debt, exploring state or employer-based programs remains the best alternative, though options are limited. The key takeaway: federal loans are not just a funding source but a tool for career sustainability in healthcare.

Discover If You Qualify for Student Loan Forgiveness: A Guide

You may want to see also

Explore related products

$7.99 $14.99

![]()

Income-Driven Repayment Plans Availability

Clinical medical assistants often face the challenge of managing student loan debt while earning entry-level wages. Income-driven repayment (IDR) plans offer a lifeline by capping monthly payments at a percentage of discretionary income, typically 10-20%. For example, a medical assistant earning $35,000 annually with $40,000 in loans might see payments drop from $400 to $200 per month under the Revised Pay As You Earn (REPAYE) plan. This adjustment not only eases immediate financial strain but also aligns repayment with long-term earning potential.

To qualify for an IDR plan, applicants must demonstrate partial financial hardship, defined as having a federal student loan payment exceeding what they’d pay on a 10-year Standard Repayment Plan. For instance, a borrower with $50,000 in loans at 5% interest would owe $530 monthly on the standard plan. If their IDR payment is $250, they’d qualify. Documentation, such as recent tax returns or pay stubs, is required to verify income. Recertification is mandatory annually, as payment amounts adjust based on updated financial data.

A critical yet underutilized feature of IDR plans is the pathway to loan forgiveness. After 20-25 years of qualifying payments, remaining balances are forgiven, though borrowers may owe taxes on the forgiven amount. For medical assistants, this timeline aligns with career progression; those who start in their early 20s could see forgiveness in their 40s or 50s. However, choosing an IDR plan requires careful consideration, as lower monthly payments extend the repayment period, accruing more interest over time.

One caution: IDR plans are not a one-size-fits-all solution. Borrowers must select the plan best suited to their circumstances. For example, the Income-Based Repayment (IBR) plan caps payments at 10-15% of discretionary income and forgives loans after 20-25 years, while the Pay As You Earn (PAYE) plan limits payments to 10% and forgives after 20 years. Medical assistants should use the Federal Student Aid Loan Simulator to compare scenarios and project long-term costs. Additionally, staying in an IDR plan requires discipline; missing recertification deadlines can lead to payment spikes or capitalization of interest.

In practice, combining IDR plans with strategic career moves amplifies their benefits. Medical assistants pursuing certifications or advanced roles, such as registered nursing or healthcare administration, can leverage higher future earnings to manage loan forgiveness timelines. For instance, a borrower earning $40,000 initially might see payments capped at $300 monthly, but a $60,000 salary later could accelerate forgiveness by increasing discretionary income calculations. Proactive planning—such as enrolling in auto-debit for a 0.25% interest rate reduction—further optimizes outcomes. Ultimately, IDR plans demand vigilance but offer a structured path to financial stability for clinical medical assistants burdened by student debt.

New York State Tax Rules for Student Loan Forgiveness Explained

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness Eligibility

Clinical medical assistants seeking student loan forgiveness often overlook the Public Service Loan Forgiveness (PSLF) program, assuming it’s reserved for higher-credentialed roles like physicians or nurses. However, eligibility hinges on employment, not job title. To qualify, you must work full-time for a qualifying employer—such as a government agency, 501(c)(3) nonprofit, or specific tribal organizations—and make 120 qualifying payments under an income-driven repayment plan. For clinical medical assistants employed by eligible entities, this pathway is viable, though meticulous documentation of payments and employer certification is critical.

The first step to leveraging PSLF is confirming your employer’s eligibility. Use the Federal Student Aid Employer Search Tool to verify that your workplace qualifies. Nonprofit hospitals, community health centers, and government-run clinics often meet the criteria, making them ideal workplaces for clinical medical assistants. If your employer qualifies, submit the Employment Certification Form (ECF) annually or whenever you switch jobs to ensure each payment counts toward the 120 required. This proactive approach prevents disqualifications due to technicalities, such as incorrect repayment plan enrollment or unverified employment periods.

Income-driven repayment plans are the backbone of PSLF, as they cap monthly payments at a percentage of your discretionary income, often lowering costs significantly. For clinical medical assistants earning modest salaries, plans like Revised Pay As You Earn (REPAYE) or Income-Based Repayment (IBR) can reduce payments to as little as $0, with each month still counting toward forgiveness. However, beware of tax implications: forgiven amounts may be treated as taxable income, though temporary waivers under the PSLF program have occasionally excluded this liability.

A common pitfall is assuming all federal loans qualify for PSLF. Only Direct Loans are eligible; Federal Family Education Loans (FFEL) or Perkins Loans must be consolidated into a Direct Consolidation Loan to qualify. Consolidation resets the payment counter, so time this step strategically to avoid losing progress. Additionally, partial employment (e.g., part-time work at a qualifying employer) does not count unless you meet the full-time threshold, typically 30 hours per week.

Finally, persistence and vigilance are key. The PSLF program has a reputation for complexity, with many applicants denied due to minor errors. Keep detailed records of payments, employer certifications, and correspondence with loan servicers. Utilize the PSLF Help Tool for guidance and consider consulting a student loan advisor to navigate nuances. For clinical medical assistants committed to public service, PSLF offers a tangible path to debt relief, but success demands diligence and informed decision-making.

Navigating the New Student Loan Forgiveness Program: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Employer-Sponsored Repayment Assistance Options

Clinical medical assistants often face significant student loan burdens, but a growing trend offers a glimmer of hope: employer-sponsored repayment assistance programs. These initiatives, increasingly adopted by healthcare facilities, directly tackle the financial strain of educational debt. Unlike traditional loan forgiveness programs tied to public service or lengthy commitments, employer-sponsored assistance provides immediate, tangible relief. For instance, a hospital might offer $200 monthly contributions toward an employee's student loans, reducing the principal balance faster and saving on interest over time. This approach not only eases financial stress but also fosters loyalty and retention among skilled professionals.

Implementing such a program requires careful planning. Employers typically structure contributions as part of a benefits package, often tied to performance or tenure. For example, a medical assistant might receive $100 per month after one year of service, increasing to $200 after three years. Some organizations partner with third-party platforms like Goodly or Gradifi to streamline payments and ensure compliance with tax regulations. It’s crucial to communicate these benefits clearly during recruitment, as they can be a decisive factor for candidates weighing job offers. Additionally, employers should consider capping contributions to avoid excessive costs while still providing meaningful support.

From the employee’s perspective, maximizing these programs involves strategic financial management. First, ensure your loans are eligible for employer contributions—federal loans are typically covered, but private loans may require additional steps. Second, allocate the extra funds wisely. Instead of reducing monthly payments, apply the employer’s contribution directly to the principal to accelerate debt repayment. For example, a $200 monthly contribution on a $30,000 loan at 6% interest could shave off nearly two years of payments and save over $2,500 in interest. Finally, stay informed about program updates and advocate for expansions if possible.

While employer-sponsored repayment assistance is not universal loan forgiveness, it represents a practical, immediate solution for clinical medical assistants. Its success hinges on mutual benefit: employees gain financial relief, while employers attract and retain talent in a competitive market. As healthcare facilities increasingly recognize the value of this approach, it’s likely to become a standard component of compensation packages. For medical assistants burdened by debt, seeking out such opportunities—or negotiating for them—could be a game-changer in achieving financial stability.

Does PSLF Forgive Graduate Student Loans? A Comprehensive Guide

You may want to see also

Explore related products

![]()

State-Specific Loan Forgiveness Programs

Clinical medical assistants seeking student loan forgiveness often overlook state-specific programs, which can provide targeted relief based on geographic location and employment commitments. Unlike federal programs, these initiatives are tailored to address local healthcare workforce shortages, offering a unique pathway to debt reduction. For instance, California’s Bachelor of Science in Nursing Loan Repayment Program extends benefits to medical assistants working in underserved areas, provided they commit to a minimum of two years of service. Eligibility typically hinges on employment in federally designated Health Professional Shortage Areas (HPSAs), with repayment amounts varying by state funding and demand.

To navigate these programs effectively, start by identifying your state’s Department of Health or Higher Education website, where most loan forgiveness opportunities are listed. For example, New York’s State Loan Repayment Program offers up to $20,000 annually for two years to healthcare professionals, including medical assistants, working in underserved communities. Be prepared to submit proof of employment, loan balances, and a service commitment agreement. Some states, like Texas, require applicants to work full-time (minimum 32 hours per week) in a qualifying facility, while others may accept part-time commitments with prorated repayment amounts.

A comparative analysis reveals that state programs often have fewer applicants than federal options, increasing the likelihood of approval for qualified candidates. However, they come with stricter geographic and employment requirements. For instance, Florida’s Nursing Student Loan Forgiveness Program excludes medical assistants unless they are enrolled in a bridge program to become nurses, highlighting the importance of verifying eligibility criteria. Additionally, some states, such as Illinois, require recipients to maintain licensure and certification throughout the service period, adding a layer of compliance.

Persuasively, state-specific programs offer a double benefit: debt relief and the opportunity to contribute to local healthcare needs. For medical assistants in rural or urban underserved areas, these programs can be life-changing. Take Minnesota’s Rural Physician Associate Program, which includes medical assistants working in primary care settings and provides up to $30,000 in loan repayment for a two-year commitment. To maximize success, applicants should pair state programs with federal options like the Public Service Loan Forgiveness (PSLF) program, ensuring dual eligibility where possible.

In conclusion, state-specific loan forgiveness programs are a strategic yet underutilized resource for clinical medical assistants. By aligning employment with local healthcare priorities, applicants can access substantial repayment benefits while making a meaningful impact. Research thoroughly, meet all eligibility requirements, and consider combining state and federal programs for comprehensive debt relief. This approach not only alleviates financial burden but also fosters professional growth in high-need areas.

Understanding Grade Forgiveness Policies for Undergraduate Students: How Many?

You may want to see also

Frequently asked questions

Student loan forgiveness for clinical medical assistants is possible through specific programs like Public Service Loan Forgiveness (PSLF) if they work full-time for a qualifying employer, such as a government or nonprofit organization, for 10 years while making eligible payments.

Clinical medical assistants may also qualify for loan forgiveness through state-based programs, employer repayment assistance programs, or income-driven repayment plans that forgive remaining balances after 20–25 years of payments.

The CARES Act and related COVID-19 relief measures primarily apply to federal student loans, offering temporary payment pauses and interest waivers. Clinical medical assistants with federal loans may benefit from these provisions but are not automatically eligible for forgiveness unless they meet specific program criteria.