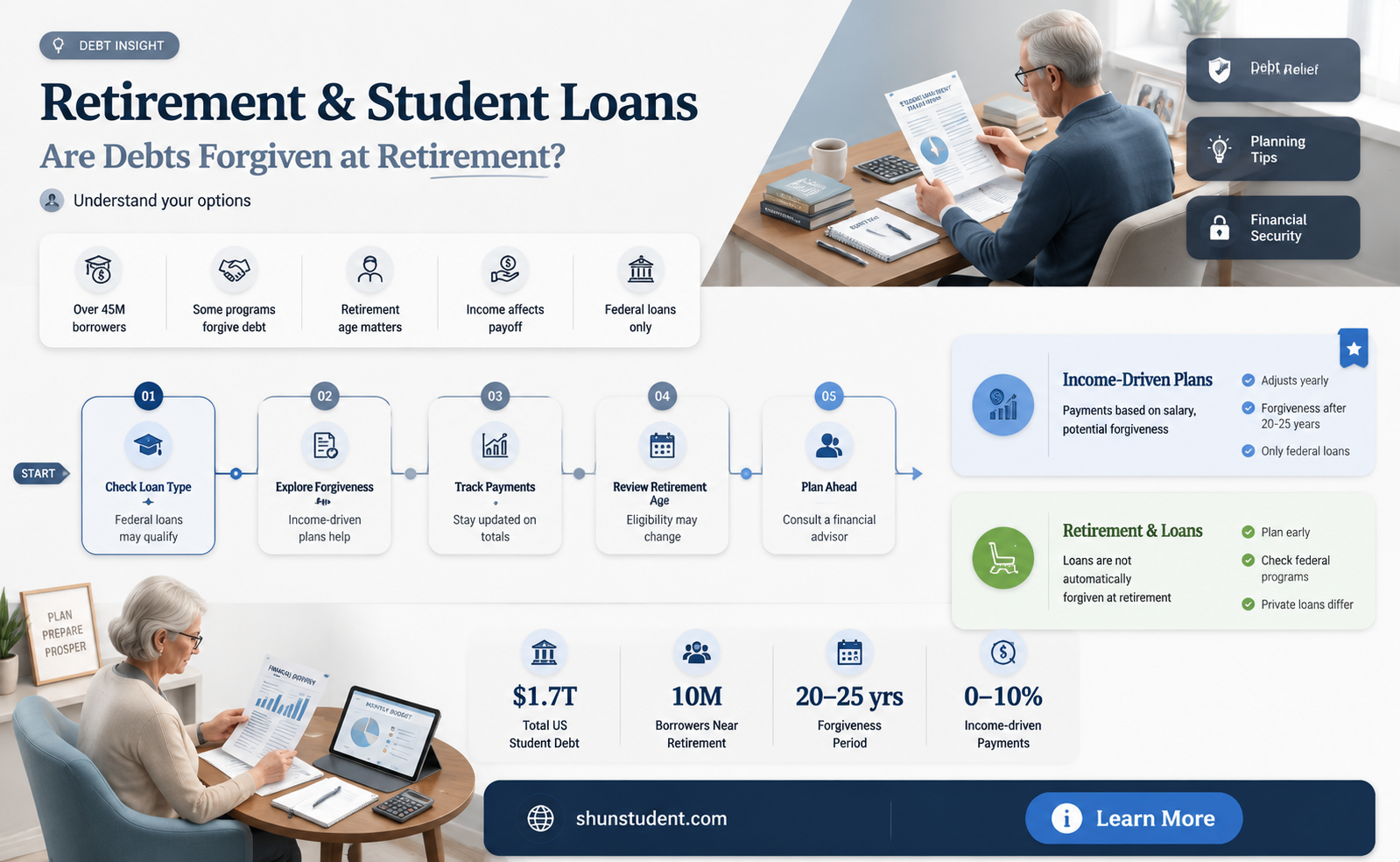

As individuals approach retirement, many carry the burden of outstanding student loan debt, raising the question: are student loans forgiven when you retire? The answer is not straightforward, as it depends on various factors such as the type of loan, repayment plan, and individual circumstances. Federal student loans, for instance, may be eligible for forgiveness under certain programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, which can lead to loan discharge after a specified period. However, private student loans typically do not offer forgiveness options, and retirees may still be responsible for repaying these debts. Furthermore, retirees with federal student loans may face challenges, as their loan payments can be deducted from their Social Security benefits, affecting their overall financial stability. Understanding the nuances of student loan forgiveness in retirement is crucial for effective financial planning and ensuring a secure future.

| Characteristics | Values |

|---|---|

| Federal Student Loan Forgiveness at Retirement | Generally, federal student loans are not automatically forgiven upon retirement. However, remaining balances may be discharged if the borrower dies or becomes permanently disabled. |

| Income-Driven Repayment (IDR) Forgiveness | Under IDR plans, any remaining balance is forgiven after 20–25 years of qualifying payments. For retirees, this could apply if they’ve been on an IDR plan and reach the forgiveness period at retirement. |

| Public Service Loan Forgiveness (PSLF) | Borrowers with Direct Loans who work full-time for a qualifying employer (e.g., government, non-profit) for 10 years may have loans forgiven, regardless of age or retirement status. |

| Loan Discharge for Total and Permanent Disability (TPD) | Loans may be discharged if the borrower becomes permanently disabled, regardless of age. |

| Death of Borrower | Federal student loans are discharged upon the borrower’s death. |

| Private Student Loans | Private loans are not forgiven at retirement and typically do not offer forgiveness programs. Borrowers remain responsible for repayment. |

| Tax Implications | Forgiven loan amounts may be considered taxable income, except for PSLF or TPD discharges. |

| Age-Based Repayment Plans | No specific age-based forgiveness exists, but retirees with low income may qualify for lower payments or $0 payments under IDR plans. |

| Default Consequences | Retirees in default may face garnishment of Social Security benefits or wages, but not retirement accounts like 401(k)s or IRAs. |

| Bankruptcy Discharge | Student loans are rarely dischargeable in bankruptcy, regardless of age or retirement status. |

| State-Specific Programs | Some states offer loan repayment assistance programs (LRAPs) for retirees in specific professions (e.g., teachers, healthcare workers), but these are not universal. |

Explore related products

What You'll Learn

![]()

Federal Loan Forgiveness Programs

Retirees burdened by federal student loans may find relief through specific forgiveness programs, but eligibility hinges on meeting stringent criteria. The Public Service Loan Forgiveness (PSLF) program, for instance, forgives remaining loan balances after 120 qualifying payments for those employed full-time in public service roles. While retirement itself doesn’t automatically trigger forgiveness, individuals who worked in eligible sectors (e.g., government, nonprofits) before retiring can still qualify if they’ve met the payment threshold. This program underscores the importance of consistent employment in qualifying roles, even if retirement follows.

Another pathway is the Income-Driven Repayment (IDR) Plan Forgiveness, which forgives remaining balances after 20–25 years of qualifying payments, depending on the plan. Retirees who enrolled in IDR plans earlier in their careers may reach this milestone post-retirement, effectively eliminating their debt. However, forgiven amounts may be taxed as income, so retirees should consult a tax professional to plan accordingly. This option highlights the long-term strategy required to benefit from such programs.

For retirees aged 65 or older with limited income, the Financial Hardship Discharge may be an option, though it’s rarely granted. This requires proving inability to repay loans due to income and asset constraints. While not a forgiveness program per se, it offers a last-resort solution for those in dire financial straits. Retirees considering this route should gather detailed financial documentation to support their case.

Comparatively, the Teacher Loan Forgiveness Program forgives up to $17,500 for educators who teach full-time for five consecutive years in low-income schools. Retirees who spent their careers in education may have already benefited from this program, reducing their loan burden before retirement. This example illustrates how career choices can directly impact loan forgiveness outcomes.

In summary, federal loan forgiveness programs for retirees are not automatic but require strategic planning and adherence to specific criteria. Whether through PSLF, IDR forgiveness, or targeted programs like Teacher Loan Forgiveness, retirees can explore these avenues to alleviate their student debt burden. Proactive research and documentation are key to maximizing these opportunities.

Biden's Potential Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans

Retirees burdened by student loan debt often find solace in Income-Driven Repayment (IDR) plans, which adjust monthly payments based on income and family size. These plans can significantly reduce financial strain, especially for those on fixed incomes. For instance, the Revised Pay As You Earn (REPAYE) plan caps payments at 10% of discretionary income, while the Income-Based Repayment (IBR) plan limits payments to 10% or 15%, depending on when the loan was taken out. Such adjustments ensure that retirees, often living on Social Security or pensions, aren’t overwhelmed by unmanageable payments.

One critical aspect of IDR plans is their pathway to loan forgiveness. After 20 or 25 years of qualifying payments, depending on the plan, any remaining balance is forgiven. For retirees, this means that even if they haven’t paid off their loans by retirement age, they may qualify for forgiveness shortly thereafter. However, it’s essential to note that forgiven amounts may be taxed as income, though retirees in lower tax brackets may owe less than expected. For example, a retiree in the 12% tax bracket would owe $1,200 on $10,000 of forgiven debt.

Enrolling in an IDR plan requires annual recertification of income and family size, which can be a hassle but is crucial for maintaining eligibility. Retirees should gather documentation like tax returns and benefit statements to streamline this process. Additionally, those with Parent PLUS Loans must consolidate them into a Direct Consolidation Loan to qualify for IDR plans. This step is often overlooked but can open the door to lower payments and eventual forgiveness.

While IDR plans offer relief, they aren’t without drawbacks. Interest accrual can cause loan balances to grow, especially if payments don’t cover the full interest amount. Retirees should weigh this against the benefits of reduced monthly payments and potential forgiveness. For example, a retiree with $50,000 in loans at 6% interest might see their balance increase by $3,000 annually if payments are insufficient, but the lower monthly burden could outweigh this concern.

In practice, retirees should explore IDR plans as part of a broader strategy to manage student loan debt. Combining these plans with careful budgeting and tax planning can minimize financial stress. For instance, a retiree earning $30,000 annually with $40,000 in loans might see payments drop to $200 per month under an IDR plan, making repayment far more manageable. By understanding the nuances of these plans, retirees can navigate their student loan obligations with greater confidence and clarity.

Erase Student Debt: Guide to Forgiving 23-Year-Old Loans

You may want to see also

Explore related products

$19.95 $19.95

$15.45 $14.95

$10.1 $16.99

![]()

Age-Based Loan Discharge Rules

Retiring with student loan debt is a growing concern for many older Americans, but age-based loan discharge rules offer a potential lifeline. These rules, part of federal student loan programs, provide a pathway to forgiveness for borrowers who reach a certain age and meet specific criteria. Understanding these rules is crucial for retirees or those nearing retirement age who are still burdened by student loans.

Eligibility Criteria for Age-Based Discharge

To qualify for age-based loan discharge, borrowers typically must be at least 65 years old (though some programs may have different age thresholds). Additionally, they must demonstrate financial hardship, often through income-driven repayment plans. For example, the Income-Contingent Repayment (ICR) plan for federal Direct Loans allows for loan forgiveness after 25 years of qualifying payments, with no age restriction. However, for older borrowers, this timeline can align with retirement age, effectively acting as an age-based discharge. It’s essential to review your loan type and repayment plan to determine eligibility, as not all federal loans or repayment plans qualify.

Practical Steps to Pursue Age-Based Discharge

If you’re nearing retirement and struggling with student loans, start by consolidating your federal loans into a Direct Consolidation Loan if necessary, as this is required for certain forgiveness programs. Next, enroll in an income-driven repayment plan, such as ICR or Income-Based Repayment (IBR), which caps monthly payments based on income and family size. Keep detailed records of your payments, as forgiveness typically occurs after 20 to 25 years of qualifying payments. For retirees with limited income, these payments may be as low as $0, which still count toward the forgiveness timeline.

Cautions and Limitations

While age-based discharge rules can provide relief, they are not without pitfalls. For instance, forgiven amounts may be considered taxable income, potentially increasing your tax liability in the year of discharge. Additionally, private student loans are not eligible for these programs, leaving retirees with private debt to explore other options like refinancing or settlement negotiations. It’s also important to stay current on payments, as defaulting on loans can disqualify you from forgiveness programs and lead to wage garnishment or Social Security offsets.

Comparative Analysis: Age-Based vs. Other Forgiveness Programs

Age-based discharge differs from other forgiveness programs like Public Service Loan Forgiveness (PSLF) or Teacher Loan Forgiveness, which require specific employment or service commitments. While these programs offer faster forgiveness (e.g., 10 years for PSLF), they may not be accessible to retirees. Age-based discharge, on the other hand, is more inclusive for older borrowers but requires a longer repayment period. For retirees, this option may be the most viable, especially if they’ve already made significant payments over their working years.

Takeaway: Planning for Retirement with Student Loans

For retirees or those approaching retirement, age-based loan discharge rules can provide a much-needed financial reprieve. By understanding eligibility criteria, taking proactive steps, and being aware of potential drawbacks, borrowers can navigate this complex landscape effectively. Consulting with a financial advisor or student loan specialist can also help tailor a strategy to your unique situation, ensuring you maximize available benefits and minimize long-term financial strain.

Student Loan Forgiveness: Boosting Financial Freedom and Quality of Life

You may want to see also

Explore related products

![]()

Private Loan Retirement Policies

Private student loans, unlike their federal counterparts, do not offer standardized retirement forgiveness programs. This means retirees burdened by private student loan debt—whether their own or cosigned for a child or grandchild—face a stark reality: repayment typically continues until the loan is fully satisfied. Lenders like Sallie Mae, Navient, and Discover have no legal obligation to discharge loans due to age or retirement status, leaving borrowers with limited options for relief.

One potential strategy involves negotiating directly with the lender. Some private loan servicers may agree to a modified repayment plan or settlement, particularly if the borrower can demonstrate financial hardship. For instance, a 65-year-old retiree with a fixed income and $30,000 in private student loans might propose a lump-sum payment of $15,000 to settle the debt. Success here depends on the lender’s policies and the borrower’s ability to negotiate effectively. Hiring a debt settlement attorney or financial advisor can improve outcomes, though this incurs additional costs.

Another approach is leveraging retirement assets strategically, though this carries significant risks. Retirees with substantial savings in 401(k)s or IRAs might consider using a portion of these funds to pay off high-interest private loans. However, withdrawals before age 59½ trigger penalties, and reducing retirement savings can jeopardize long-term financial security. For example, a 67-year-old with a $50,000 private loan might withdraw $20,000 from their IRA, but this would incur a 10% penalty and taxes, effectively reducing the net amount available for repayment.

Bankruptcy, while rarely successful for student loans, remains a theoretical option. The "undue hardship" standard is extremely difficult to meet, requiring proof that repayment would prevent maintaining a minimal standard of living. For retirees, this might involve demonstrating reliance on Social Security as sole income and inability to work due to age or health. However, private lenders aggressively contest such claims, making this a last-resort option with no guarantee of success.

In summary, private loan retirement policies offer no automatic forgiveness, leaving retirees to navigate a complex landscape of negotiation, strategic asset use, or extreme measures like bankruptcy. Proactive planning—such as refinancing to lower interest rates before retirement or prioritizing loan repayment during working years—remains the most effective strategy to avoid carrying this debt into later life. For those already retired, careful evaluation of financial resources and professional guidance are essential to minimize the impact of private student loans on retirement stability.

Understanding Federal Student Loan Forgiveness: A Comprehensive Guide to Eligibility and Process

You may want to see also

Explore related products

![]()

Tax Implications of Forgiveness

Retiring with student loan debt can feel like carrying a backpack full of bricks into what should be a carefree phase of life. While forgiveness programs exist, they often come with a hidden cost: taxes. The IRS considers forgiven debt as taxable income, meaning a significant portion of your forgiven student loans could end up on your tax bill. This isn't just a theoretical concern; it's a real financial hurdle for retirees on fixed incomes.

For example, if $50,000 of your student loans are forgiven, that amount is added to your taxable income for the year, potentially pushing you into a higher tax bracket and resulting in a larger tax liability.

Understanding the tax implications requires a deep dive into the specifics of forgiveness programs. Income-Driven Repayment (IDR) plans, for instance, offer forgiveness after 20-25 years of qualifying payments, but the forgiven amount is generally taxable as income. Public Service Loan Forgiveness (PSLF), on the other hand, is tax-free, making it a more attractive option for those eligible. However, the PSLF program has stringent requirements, including 10 years of qualifying payments and employment in a qualifying public service job.

To mitigate the tax burden, retirees should consider strategic planning. One approach is to time forgiveness to coincide with years of lower income, such as the year you retire or a year with significant deductions. Another strategy is to set aside funds in a tax-advantaged account, like a Health Savings Account (HSA) or a Roth IRA, which can help offset the tax liability. Consulting a tax professional is crucial; they can help you navigate the complexities and identify opportunities to minimize your tax burden.

Comparing the tax implications of different forgiveness programs highlights the importance of choosing the right path. While IDR plans offer flexibility, the tax consequences can be steep. PSLF, though more restrictive, provides a tax-free solution for those who qualify. For retirees, the decision often hinges on their financial situation, employment history, and long-term goals. Weighing these factors carefully can make the difference between a smooth retirement and a financially stressful one.

In conclusion, while student loan forgiveness can provide much-needed relief for retirees, the tax implications cannot be overlooked. By understanding the rules, planning strategically, and seeking professional advice, retirees can navigate this complex landscape and secure a more stable financial future. The key is to approach forgiveness not just as a solution to debt, but as a component of a comprehensive retirement strategy.

Does the NSA Offer Student Loan Forgiveness? What You Need to Know

You may want to see also

Frequently asked questions

No, student loans are not automatically forgiven upon retirement. Borrowers must still repay their loans unless they qualify for a specific forgiveness program or meet certain criteria, such as having federal loans and making qualifying payments under an income-driven repayment plan.

Yes, retirees can qualify for student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or forgiveness under income-driven repayment plans, if they meet the eligibility requirements. However, forgiveness is not guaranteed solely based on retirement status.

If you retire and cannot afford student loan payments, you may be able to switch to an income-driven repayment plan, which caps payments based on your income and family size. After 20–25 years of qualifying payments, any remaining balance may be forgiven, though you may owe taxes on the forgiven amount.