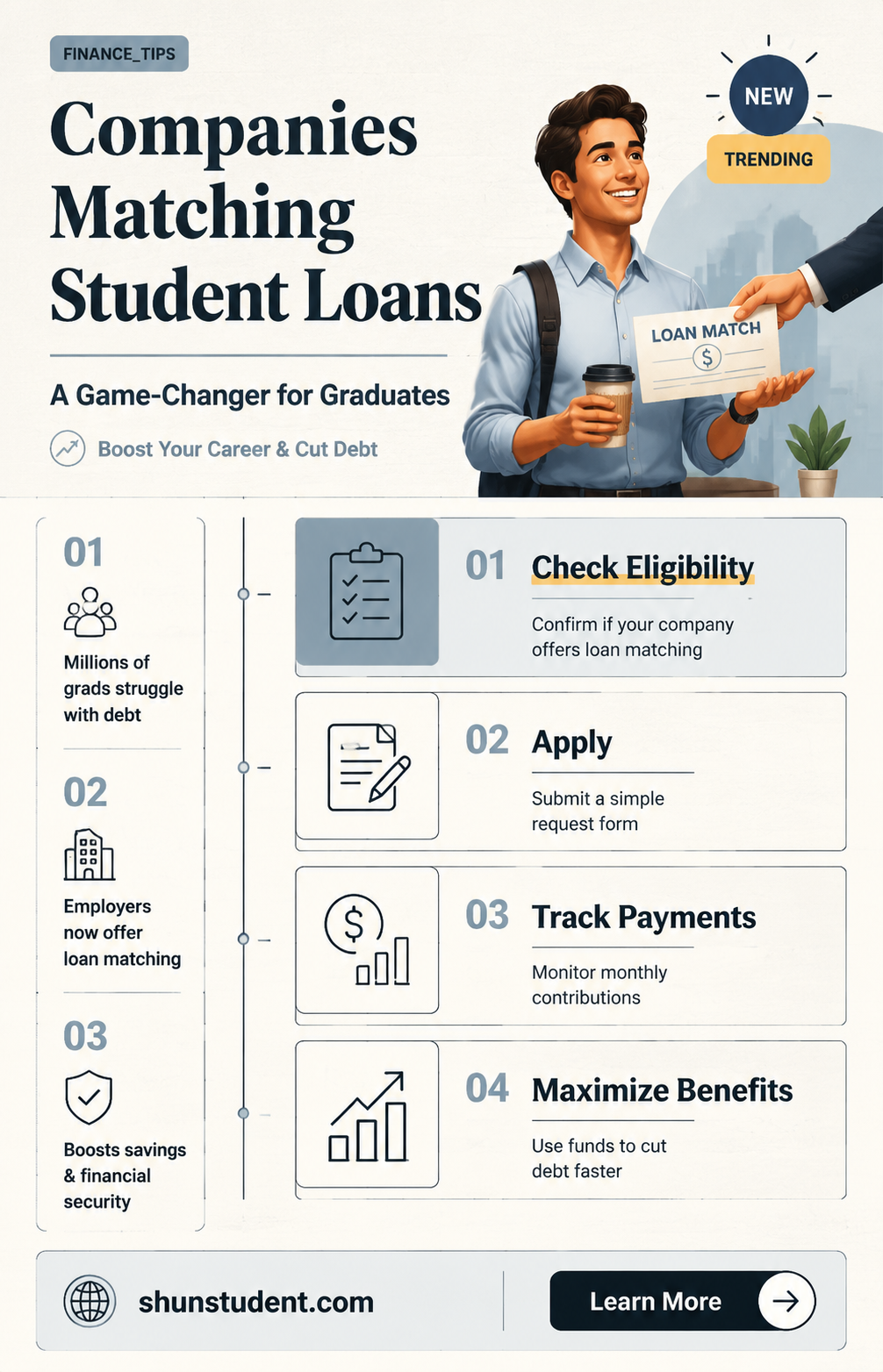

In recent years, the burden of student loan debt has become a pressing issue for many graduates, prompting a growing number of companies to offer innovative benefits to attract and retain talent. One such benefit gaining traction is the student loan repayment assistance program, where employers agree to match or contribute to their employees' student loan payments. This perk not only helps alleviate financial stress for employees but also positions companies as forward-thinking and employee-centric. As the job market becomes increasingly competitive, organizations across various industries are exploring this option, raising the question: Are there companies that will match student loan payments, and how can this benefit both employers and employees?

| Characteristics | Values |

|---|---|

| Companies Offering Matching Programs | Fidelity Investments, Aetna, Penguin Random House, CarMax, etc. |

| Eligibility Criteria | Full-time employees, minimum tenure (e.g., 1 year), active loan repayment |

| Maximum Annual Contribution | Typically $1,000–$2,000 per employee per year |

| Lifetime Cap | Often $10,000–$20,000 per employee |

| Loan Types Covered | Federal and private student loans |

| Tax Implications | Contributions may be taxable income for employees |

| Program Duration | Varies by company; some offer indefinite programs |

| Industry Prevalence | Common in tech, finance, healthcare, and publishing sectors |

| Employee Retention Impact | High; improves retention and attracts younger talent |

| Recent Trends | Increasing adoption post-pandemic; part of competitive benefits packages |

| Legal Requirements | No federal mandate; offered voluntarily by employers |

| Public vs. Private Sector | More common in private sector companies |

| Additional Benefits | Often paired with financial wellness programs or counseling |

Explore related products

What You'll Learn

![]()

Employer-Sponsored Repayment Programs

As the burden of student loan debt continues to weigh on millions of Americans, a growing number of companies are stepping in to alleviate this financial strain through Employer-Sponsored Repayment Programs. These initiatives, which often involve direct contributions to employees’ student loans, are becoming a critical tool in talent recruitment and retention. For instance, companies like Fidelity Investments, Aetna, and Penguin Random House offer programs where they contribute a fixed amount—typically $100 to $200 per month—toward employees’ student loan balances, often with a lifetime cap of $10,000 to $20,000. This not only reduces employees’ debt but also improves their financial well-being, fostering loyalty and productivity.

Analyzing the structure of these programs reveals a strategic win-win for both employers and employees. Employers benefit from a competitive edge in hiring, particularly among younger workers who prioritize financial stability. Employees, on the other hand, experience faster debt reduction and lower interest costs. For example, a $100 monthly contribution over five years can reduce a $30,000 loan balance by nearly $6,000, assuming a 6% interest rate. However, it’s crucial for employees to understand the tax implications: while the CARES Act of 2020 allows employers to contribute up to $5,250 annually tax-free through 2025, not all programs are structured this way. Always verify the tax treatment with your employer or a financial advisor.

Implementing an Employer-Sponsored Repayment Program requires careful planning. Companies should start by assessing their workforce’s needs—for instance, younger employees with higher debt burdens may benefit more than older workers. Next, decide on the contribution structure: monthly payments, lump-sum bonuses, or a combination of both. Pairing these programs with financial wellness workshops can amplify their impact, teaching employees budgeting and debt management skills. Caution should be taken to ensure the program complies with legal and tax regulations, as missteps can lead to unintended liabilities.

Comparatively, these programs stand out from traditional benefits like 401(k) matching, which often exclude employees focused on immediate debt relief. While retirement savings remain essential, student loan repayment assistance addresses a pressing, short-term financial challenge. Companies like PwC report that their student loan repayment program has increased employee satisfaction and retention rates by over 30%. This highlights the program’s dual role: a benefit for employees and a strategic investment for employers.

In conclusion, Employer-Sponsored Repayment Programs are reshaping the employee benefits landscape by directly tackling student loan debt. By offering tangible financial relief, companies not only attract top talent but also cultivate a more engaged and stable workforce. For employees, these programs provide a pathway to financial freedom, reducing stress and enabling better long-term planning. As this trend continues to grow, both employers and employees stand to gain from this innovative approach to workplace benefits.

Unlock Student Debt Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Corporate Student Loan Matching Policies

A growing number of companies are recognizing the burden of student loan debt on their employees and are implementing corporate student loan matching policies as a strategic benefit. These policies, often structured as a dollar-for-dollar match up to a certain limit, effectively reduce employees’ out-of-pocket loan payments. For instance, Fidelity Investments offers up to $10,000 over five years, while Aetna provides $2,000 annually, capped at $10,000. Such programs not only alleviate financial stress but also enhance employee loyalty and retention, making them a win-win for both parties.

Designing an effective student loan matching policy requires careful consideration of budget, eligibility criteria, and administrative logistics. Companies must decide whether to cap contributions annually or over a multi-year period, as well as determine eligibility based on tenure, full-time status, or other factors. For example, Kronos Incorporated requires employees to work at least 20 hours per week and have been with the company for at least one year to qualify. Additionally, integrating the program with existing payroll systems and ensuring compliance with tax regulations are critical steps to avoid legal pitfalls.

From a persuasive standpoint, corporate student loan matching policies are a powerful tool for attracting and retaining top talent, particularly among younger generations burdened by educational debt. Studies show that 86% of employees would commit to an employer for five years if student loan assistance were offered. Companies like PwC, which provides up to $1,200 annually for eligible employees, have reported significant improvements in recruitment and retention rates. By framing this benefit as an investment in employees’ financial futures, employers can differentiate themselves in a competitive job market.

Comparatively, student loan matching programs stand out from traditional benefits like 401(k) matches or health insurance by addressing a pressing, age-specific financial challenge. While retirement plans focus on long-term savings, student loan assistance provides immediate relief, making it particularly appealing to millennials and Gen Z, who hold the majority of student debt. For example, Staples offers a $100 monthly contribution, which, while modest, can save employees thousands in interest over time. This targeted approach not only fosters goodwill but also aligns with broader corporate social responsibility goals.

To maximize the impact of a student loan matching policy, companies should pair it with financial wellness initiatives, such as debt counseling or refinancing partnerships. For instance, Hulu provides employees with access to SoFi’s student loan refinancing services alongside its matching program. Employers should also communicate the benefit clearly, emphasizing its value in reducing debt faster and saving on interest. Practical tips include automating contributions, tracking progress through a dedicated platform, and regularly soliciting employee feedback to refine the program. By taking a holistic approach, companies can ensure their policies deliver meaningful, lasting benefits.

Are Firstmark Student Loans Eligible for Forgiveness? Key Insights

You may want to see also

Explore related products

![]()

Industries Offering Loan Assistance Benefits

A growing number of industries are recognizing the burden of student loan debt on their employees and are stepping up with innovative solutions. This trend is particularly prominent in sectors facing fierce competition for top talent, where loan assistance benefits have become a powerful recruitment and retention tool.

For instance, the technology sector, known for its high demand for skilled workers, has seen companies like Google, Fidelity Investments, and Aetna implement student loan repayment programs. These programs often match employee contributions up to a certain amount, providing much-needed financial relief. This strategic move not only attracts millennials and Gen Z, who are disproportionately affected by student debt, but also fosters loyalty and improves employee satisfaction.

The healthcare industry, grappling with staffing shortages, is another key player in this arena. Hospitals and healthcare systems are increasingly offering loan repayment assistance as part of their benefits packages. Programs like the National Health Service Corps Loan Repayment Program provide substantial financial support to healthcare professionals working in underserved areas. This not only addresses the debt burden but also incentivizes professionals to serve communities in need, creating a win-win situation.

Additionally, the public sector is witnessing a surge in loan assistance programs, particularly at the state and local levels. Governments are recognizing the value of attracting and retaining talented individuals in public service roles. Programs like the Public Service Loan Forgiveness (PSLF) program offer loan forgiveness after a certain period of qualifying employment, making public service careers more financially viable for those burdened by student debt.

While these industries are leading the charge, the trend is spreading across various sectors. Companies in finance, consulting, and even retail are beginning to explore student loan repayment benefits as a way to differentiate themselves and attract top talent. As the student debt crisis continues to loom large, we can expect to see even more industries embrace loan assistance programs as a crucial component of their employee benefits packages. This shift not only benefits individual employees but also contributes to a more financially stable and productive workforce.

Supreme Court Ruling: Student Loan Forgiveness Program's Fate Decided

You may want to see also

Explore related products

![]()

Eligibility Criteria for Matching Programs

Companies offering to match student loan payments often set stringent eligibility criteria to ensure alignment with their goals and resources. These programs typically require employees to have federally-backed student loans, as private loans may not qualify due to varying terms and conditions. For instance, Fidelity Investments’ Student Debt Program mandates that participants have loans eligible under the U.S. Department of Education’s repayment plans. This specificity ensures administrative ease and compliance with federal regulations, while also maximizing the program’s impact on employees’ financial well-being.

Beyond loan type, employment tenure is a common eligibility factor. Many companies, like Aetna and Penguin Random House, require employees to complete a probationary period—often 6 to 12 months—before enrolling in matching programs. This criterion serves a dual purpose: it incentivizes long-term retention and ensures that only committed employees benefit from the financial support. For example, Kronos Incorporated requires one year of service before employees can access their $500 annual contribution, balancing generosity with strategic workforce planning.

Income-based eligibility is another layer some companies introduce to target those most in need. For instance, Abbott’s Freedom 2 Save program matches 5% of an employee’s 401(k) contributions if they allocate at least 2% of their salary to student loan repayment. This approach ensures that lower- to middle-income employees, who often face the greatest financial strain, receive prioritized support. Similarly, some programs cap annual household incomes to $100,000 or less, ensuring resources are directed to those with the most significant financial challenges.

Documentation and verification processes are critical to maintaining program integrity. Employees must typically provide proof of loan balances, repayment history, and enrollment in qualifying repayment plans. For example, Chevron requires participants to submit annual loan statements to verify eligibility and track progress. This meticulous approach prevents misuse and ensures that funds are allocated transparently. Prospective applicants should prepare to furnish detailed financial records, including loan servicer information and repayment schedules, to streamline the application process.

Finally, some companies tie eligibility to broader financial wellness initiatives, encouraging holistic fiscal responsibility. PwC, for instance, requires employees to complete financial education modules before accessing their $1,200 annual student loan contribution. This not only ensures participants are equipped to manage their finances effectively but also aligns with the company’s goal of fostering long-term financial stability. Such integrated approaches underscore the importance of pairing relief with education, creating a more sustainable impact on employees’ economic futures.

Unique Perspectives: My Contributions to the Program and Cohort

You may want to see also

Explore related products

![]()

Tax Implications of Loan Matching Benefits

As companies increasingly offer student loan matching benefits to attract and retain talent, understanding the tax implications becomes crucial for both employers and employees. These programs, while beneficial, can have complex tax consequences that require careful navigation.

Tax Treatment for Employers:

Employers offering student loan matching benefits can generally deduct these contributions as a business expense. This deduction falls under the category of employee compensation, similar to salary or health insurance contributions. However, it's crucial to ensure the program meets IRS guidelines for "educational assistance programs" to qualify for this tax benefit. This typically involves having a written plan outlining eligibility criteria, contribution limits, and permissible loan types.

Consulting with a tax professional is highly recommended to ensure compliance and maximize tax advantages.

Taxable Income for Employees:

Unfortunately, the IRS currently considers employer contributions to student loan matching programs as taxable income for employees. This means the matched amount is added to the employee's gross income, subject to federal, state, and local income taxes, as well as payroll taxes like Social Security and Medicare. This can significantly reduce the perceived value of the benefit for employees.

For example, a $100 monthly employer contribution could result in an additional $30-$40 in taxes for the employee, depending on their tax bracket.

Potential Legislative Changes:

Recognizing the burden of student loan debt, there have been proposals to make employer student loan contributions tax-free for employees. The Employer Participation in Repayment Act, reintroduced in 2021, aims to exclude up to $5,250 in annual employer contributions from taxable income. While this legislation has not yet passed, it highlights a growing awareness of the need for tax incentives to encourage these beneficial programs.

Employees should stay informed about potential legislative changes that could increase the net benefit of loan matching programs.

Strategies for Mitigating Tax Impact:

While the current tax treatment may seem discouraging, there are strategies to maximize the benefit:

- Negotiate Salary Adjustments: Employees can negotiate a slight salary reduction in exchange for the loan matching benefit, potentially offsetting the tax burden.

- Utilize Pre-Tax Deductions: If the employer offers a 401(k) or other pre-tax deduction plans, employees can allocate more of their income to these accounts, reducing their taxable income and potentially lowering their overall tax liability.

- Explore Alternative Benefits: Some companies offer alternative student loan assistance programs, such as tuition reimbursement for continuing education, which may have different tax implications.

Understanding the tax implications of student loan matching benefits is essential for both employers and employees. While the current tax treatment presents challenges, strategic planning and potential legislative changes can help maximize the value of these programs in addressing the student debt crisis.

Will College Students Receive Stimulus Checks Under the Heroes Act?

You may want to see also

Frequently asked questions

Yes, some companies offer student loan repayment assistance programs where they match or contribute to employees' student loan payments as a benefit.

The amount varies by company, but common contributions range from $50 to $200 per month, with annual caps often between $1,000 and $5,000.

No, this benefit is not universal. It’s more commonly found in industries like tech, finance, healthcare, and government, but it’s becoming increasingly popular.

Yes, unless the payments are made through a qualified employer plan, the contributions are typically considered taxable income for the employee.

It depends on the company’s policy. Some companies extend this benefit to all employees, while others may require full-time status or a minimum tenure before eligibility.