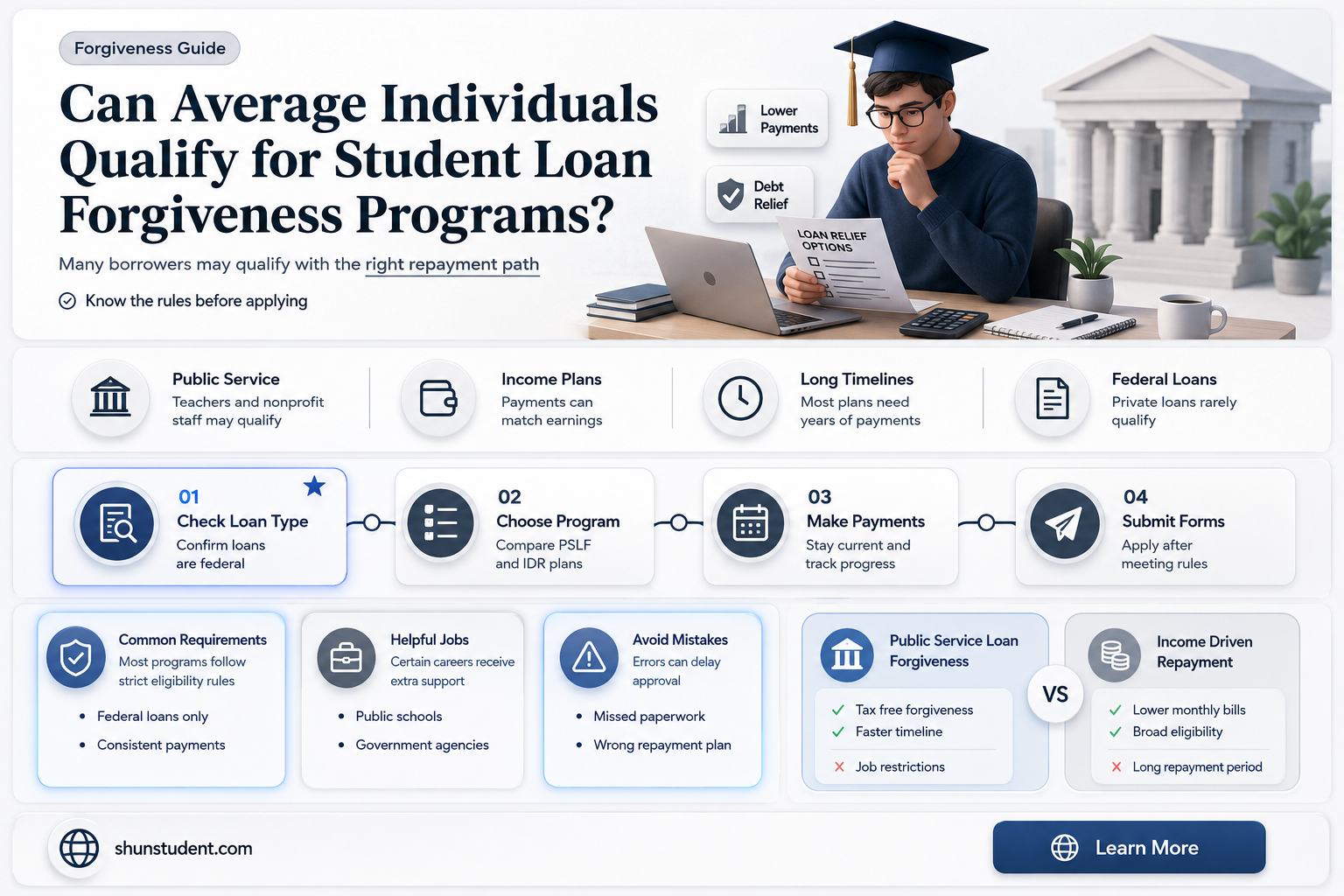

Student loan forgiveness has become a hot topic in recent years, with many borrowers seeking relief from the burden of their educational debt. While programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment plans offer pathways to forgiveness, there’s often confusion about whether a normal person without a career in public service or a specific profession can qualify. The answer lies in understanding the eligibility criteria and exploring options such as income-driven repayment plans, which can lead to loan forgiveness after 20–25 years of consistent payments, regardless of the borrower’s occupation. Additionally, recent policy changes and temporary relief measures have expanded opportunities for forgiveness, making it crucial for borrowers to stay informed about their options.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Yes, but depends on specific programs and criteria. |

| Common Programs | Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) Plans, Teacher Loan Forgiveness, etc. |

| PSLF Requirements | 120 qualifying payments while working full-time for a government or nonprofit organization. |

| IDR Forgiveness | Remaining balance forgiven after 20–25 years of qualifying payments (depending on the plan). |

| Teacher Loan Forgiveness | Up to $17,500 for eligible teachers working in low-income schools for 5 consecutive years. |

| Income Requirements | Varies by program; IDR plans require income-based payments. |

| Loan Type Eligibility | Federal student loans (Direct Loans, FFEL, Perkins Loans) are eligible; private loans are not. |

| Employment Requirements | Specific jobs (e.g., public service, teaching) may be required for certain programs. |

| Tax Implications | PSLF is tax-free; IDR forgiveness may be taxable (though temporarily waived under certain acts). |

| Application Process | Requires submitting forms (e.g., PSLF form, IDR recertification) and meeting program criteria. |

| Recent Updates (2023) | Temporary waivers and expanded eligibility under the Biden administration (e.g., IDR Account Adjustment). |

| Private Loan Forgiveness | Not available; private loans do not qualify for federal forgiveness programs. |

| Bankruptcy Discharge | Extremely rare and difficult to achieve for student loans. |

| State-Specific Programs | Some states offer loan repayment assistance programs for certain professions (e.g., healthcare, law). |

| Military Service Forgiveness | Service members may qualify for loan forgiveness through programs like the Army Loan Repayment Program. |

Explore related products

What You'll Learn

![]()

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans are a lifeline for borrowers struggling to manage federal student loan payments. These plans adjust monthly payments based on income and family size, often reducing them to as little as $0 if earnings are low. The key to forgiveness lies in the plan’s structure: after 20–25 years of qualifying payments, any remaining balance is forgiven, though borrowers may owe taxes on the forgiven amount. This makes IDR a viable path to forgiveness for "normal" individuals who earn modest incomes or work in public service.

To qualify, borrowers must recertify their income and family size annually, ensuring payments stay aligned with their financial situation. For example, a single borrower earning $30,000 annually with $50,000 in loans might see payments drop from $500 to $150 per month under the Revised Pay As You Earn (REPAYE) plan. Over time, this not only makes loans manageable but also sets the stage for forgiveness. However, it’s critical to choose the right IDR plan—options like Income-Based Repayment (IBR) or Pay As You Earn (PAYE) have different eligibility rules and forgiveness timelines.

One common misconception is that IDR plans are only for low-income earners. While they’re ideal for those with limited income, even middle-income borrowers can benefit. For instance, a married couple earning $70,000 combined with $100,000 in loans might still qualify for reduced payments under IBR. The trade-off? Longer repayment terms and potential tax implications on forgiven debt. Borrowers should weigh these factors against the relief of lower monthly payments.

Navigating IDR requires vigilance. Missed recertification deadlines can lead to payment spikes or loss of progress toward forgiveness. Additionally, switching jobs or experiencing income fluctuations demands prompt updates to avoid setbacks. Practical tip: set calendar reminders for recertification and keep detailed records of payments and correspondence. For those in public service, combining IDR with the Public Service Loan Forgiveness (PSLF) program can shorten the forgiveness timeline to 10 years, making it a powerful dual strategy.

In essence, income-driven repayment plans democratize access to student loan forgiveness by tailoring payments to individual circumstances. They’re not a quick fix but a long-term strategy for borrowers who need breathing room. By understanding the nuances of each plan and staying proactive, even "normal" borrowers can chart a path to financial freedom.

Does Student Loan Forgiveness Cover Graduate Degrees? Key Facts Explained

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF)

The eligibility criteria for PSLF are specific but manageable for those in qualifying roles. First, ensure your employer meets the program’s definition of public service; this includes federal, state, local, or tribal government organizations, 501(c)(3) non-profits, and some other non-profits providing public services. Second, enroll in an income-driven repayment plan, which caps your monthly payments at a percentage of your discretionary income. Third, make 120 qualifying payments—these must be on-time, full payments while employed in a qualifying role. Keep detailed records of your employment and payments, as documentation is critical for approval.

One common misconception about PSLF is that it’s only for teachers or government employees. In reality, the program encompasses a wide range of professions, from healthcare workers at non-profit hospitals to lawyers in public interest law firms. For example, a nurse working at a rural clinic or a social worker at a community non-profit can both qualify. The key is not the specific job title but the employer’s status and the borrower’s commitment to public service. This flexibility makes PSLF accessible to a broader audience than many realize.

Despite its benefits, PSLF has faced criticism for its complex application process and low approval rates. Borrowers often struggle with determining employer eligibility or ensuring their payments qualify. To navigate these challenges, use the PSLF Help Tool provided by the U.S. Department of Education to assess your employer’s eligibility and submit the Employment Certification Form annually. Additionally, stay informed about temporary waivers or policy changes, such as the 2021 Limited PSLF Waiver, which allowed previously ineligible payments to count toward forgiveness. Proactive management of your PSLF journey can significantly increase your chances of success.

In conclusion, PSLF is a viable option for student loan forgiveness for those in public service roles, offering a clear path to debt relief after 10 years of commitment. By understanding the eligibility criteria, documenting your progress, and staying informed about program updates, you can maximize your chances of qualifying. While the process requires diligence, the potential to eliminate thousands of dollars in student debt makes PSLF a valuable opportunity for eligible borrowers.

Congress Children's Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness Programs

Teachers, often burdened by student loan debt, have access to specialized forgiveness programs designed to alleviate their financial strain while rewarding their commitment to education. The Teacher Loan Forgiveness Program offers up to $17,500 in loan forgiveness for eligible educators who teach full-time for five consecutive years in low-income schools. To qualify, teachers must have Federal Direct Loans or FFEL Program loans, and their employment must be in a school serving students from low-income families, as determined by the Department of Education’s directory. Secondary school teachers in math, science, or special education are eligible for the maximum $17,500, while other eligible teachers can receive up to $5,000. This program not only reduces debt but also incentivizes teaching in underserved communities, addressing both financial and societal needs.

Beyond the federal program, many states and districts offer their own teacher loan forgiveness initiatives tailored to local needs. For instance, the Mississippi Teacher Loan Repayment Program provides up to $3,000 annually for teachers in critical shortage areas, while the Illinois Student Loan Repayment Program offers up to $5,000 per year for teachers in low-income schools. These state-specific programs often have additional eligibility criteria, such as teaching in specific subjects or geographic regions. Teachers should research their state’s offerings to maximize their benefits, as combining federal and state programs can significantly reduce or eliminate student loan debt.

However, navigating these programs requires careful planning and documentation. Teachers must submit an Employer Certification Form annually to track their qualifying years of service and ensure compliance with program rules. Additionally, loan forgiveness is considered taxable income under federal law, so recipients should budget for potential tax liabilities. For those with multiple loans, prioritizing repayment of non-eligible loans while focusing on forgiveness for eligible ones can optimize financial outcomes. Practical tips include maintaining detailed records of employment and loan payments, as well as consulting with a financial advisor to align forgiveness strategies with long-term financial goals.

While teacher loan forgiveness programs offer substantial relief, they are not without limitations. For example, private loans are ineligible, and teachers must commit to multi-year contracts in often challenging environments. Moreover, the forgiveness process can be bureaucratic, requiring patience and persistence. Despite these challenges, the programs remain a lifeline for educators, enabling them to focus on their passion for teaching without being overwhelmed by debt. By understanding and leveraging these opportunities, teachers can transform their financial futures while making a lasting impact in the classroom.

Veterans Denied Student Loan Forgiveness: Unraveling the Crisis and Solutions

You may want to see also

Explore related products

$9.99 $12.99

![]()

Disability Discharge Options

For individuals with disabilities, student loan forgiveness through a disability discharge can be a lifeline, offering financial relief and a fresh start. This option, while not widely known, is a critical component of federal student aid programs, designed to support borrowers who face significant physical or mental impairments. The process, however, requires thorough documentation and understanding of the eligibility criteria, which are stringent but not insurmountable.

To qualify for a disability discharge, borrowers must prove they are permanently and totally disabled, a status determined by the U.S. Department of Education. This can be established through one of three methods: a physician’s certification, receipt of Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) benefits, or a determination by the Department of Veterans Affairs (VA) for veterans. For physician certification, the doctor must complete a form provided by the loan servicer, confirming the borrower’s inability to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously for at least 60 months or result in death. Borrowers receiving SSDI or SSI benefits can submit a notice of award from the Social Security Administration, while veterans must provide documentation of their VA disability rating.

Once approved, the discharge process includes a three-year monitoring period during which borrowers must meet certain conditions to avoid reinstatement of their loans. These conditions include not earning income above the poverty guideline for a family of two in their state, not receiving a new federal student loan, and not having their disability status reviewed and revoked. During this period, borrowers are also required to provide annual documentation of their earnings and, in some cases, undergo a medical review. While these requirements may seem burdensome, they are designed to ensure the program’s integrity and protect against fraud.

A key advantage of the disability discharge is its tax-free status, unlike other forms of loan forgiveness that may result in taxable income. This makes it a particularly valuable option for eligible borrowers, as it provides complete relief without additional financial burden. However, it’s essential to act promptly, as delays in applying can prolong financial stress. Borrowers should contact their loan servicer immediately if they believe they qualify, as the application process can take several months to complete.

In conclusion, while the disability discharge option is tailored to a specific subset of borrowers, it exemplifies how student loan forgiveness programs can address unique financial challenges. By understanding the eligibility criteria and application process, individuals with disabilities can navigate this pathway to financial freedom, alleviating the burden of student debt and focusing on their well-being. This option underscores the importance of exploring all available resources when seeking relief from student loans.

Forgiving Student Loans for Domestic Violence Survivors: A Path to Recovery

You may want to see also

Explore related products

![]()

Loan Forgiveness for Specific Careers

Certain careers offer pathways to student loan forgiveness, providing a lifeline for borrowers in specific fields. For instance, the Public Service Loan Forgiveness (PSLF) program forgives remaining loan balances after 120 qualifying payments for those working full-time in government or nonprofit organizations. Teachers, nurses, and social workers often qualify, but the key is consistent employment in eligible sectors and adherence to program rules. This isn’t a handout—it’s a structured reward for committing to careers that serve the public good.

Consider the Teacher Loan Forgiveness Program, which offers up to $17,500 in forgiveness for educators teaching full-time for five consecutive years in low-income schools. To qualify, ensure your school is listed in the Teacher Cancellation Low Income Directory and that you’re teaching in a high-need subject like math, science, or special education. Documentation is critical—keep employment verification and payment records to avoid disqualification. This program isn’t automatic; you must apply after completing the service requirement.

Healthcare professionals have unique opportunities, such as the National Health Service Corps (NHSC) Loan Repayment Program, which repays up to $50,000 of student loans for two years of service in underserved areas. Physicians, nurse practitioners, and dentists can benefit, but the trade-off is working in locations with limited access to care. Similarly, the Nurse Corps Loan Repayment Program covers 60% of unpaid nursing student loans after two years of service, with an option for an additional 25% for a third year. Both programs prioritize high-need areas, so research locations carefully before committing.

Lawyers aren’t left out—the Loan Repayment Assistance Program (LRAP) helps those in public interest or nonprofit law. While not federal, many states and organizations offer LRAPs to ease the burden of law school debt. Eligibility often depends on income and employer type, so check state bar associations for specifics. For example, New York’s LRAP provides up to $7,500 annually for attorneys earning under $75,000. These programs require annual reapplication, so stay organized and monitor deadlines.

Before pursuing career-specific forgiveness, weigh the long-term commitment against immediate financial relief. For example, PSLF requires a decade of service, while healthcare programs often mandate working in challenging environments. Research thoroughly, as some programs have limited funding or competitive selection processes. Pairing these opportunities with income-driven repayment plans can further reduce monthly payments during the service period. Ultimately, loan forgiveness for specific careers isn’t a quick fix—it’s a strategic choice for those passionate about their field and willing to meet stringent requirements.

Parent PLUS Loans and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

Yes, a normal person can qualify for student loan forgiveness through programs like Public Service Loan Forgiveness (PSLF), income-driven repayment (IDR) plans, or specific career-based forgiveness programs, depending on eligibility criteria.

PSLF forgives the remaining balance on federal student loans after 120 qualifying payments (10 years) for those working full-time in eligible public service jobs, such as government or nonprofit organizations.

Not necessarily. While some forgiveness programs are career-specific (e.g., teachers, nurses, or lawyers), others like PSLF and IDR plans are available to borrowers in any field, provided they meet the program requirements.

Private student loans are not eligible for federal forgiveness programs. However, some private lenders offer forgiveness or assistance programs, and borrowers may explore options like refinancing or settlement.

Income-driven repayment (IDR) plans cap monthly payments based on income and family size. After 20–25 years of qualifying payments, the remaining loan balance is forgiven, though the forgiven amount may be taxed as income.