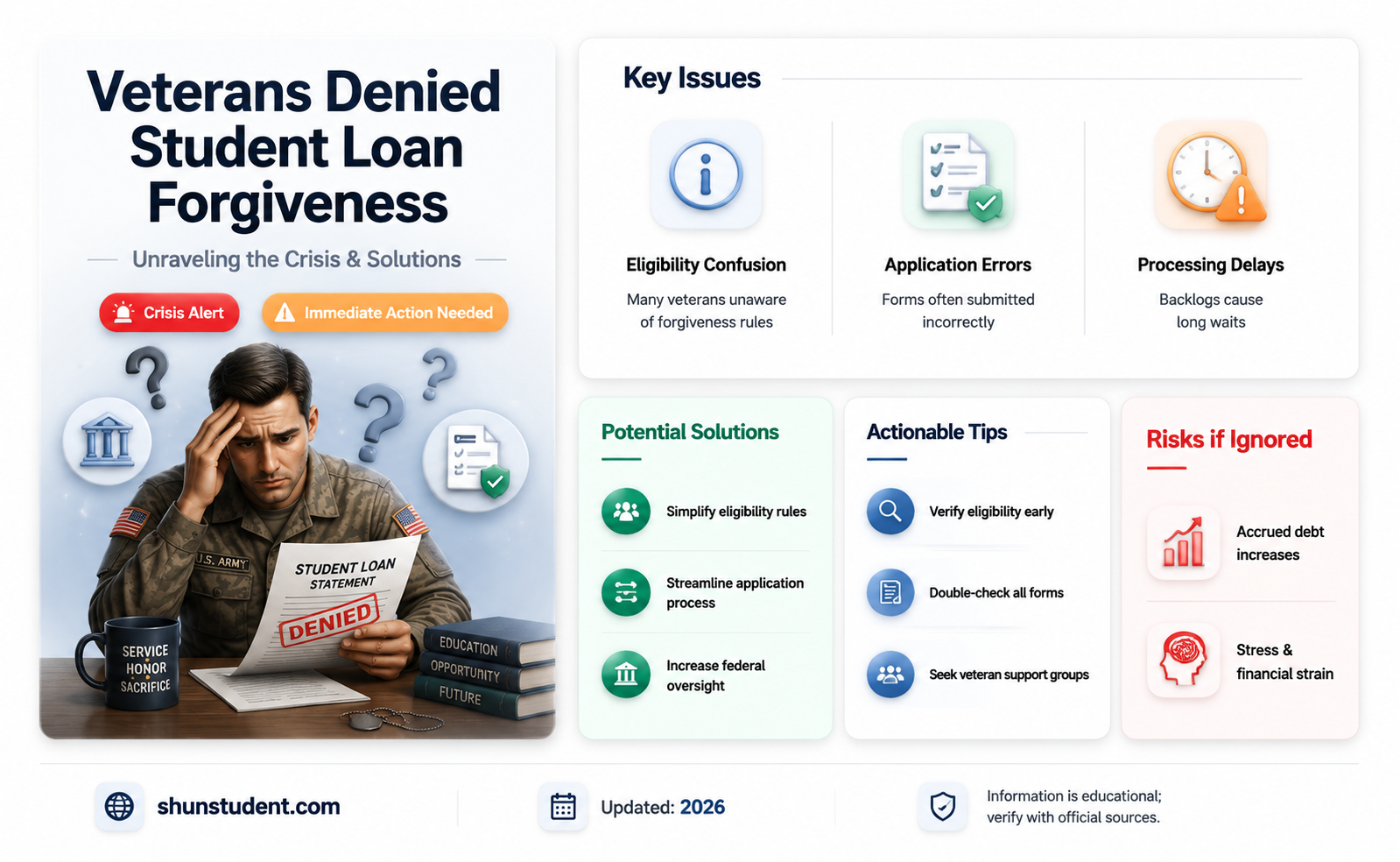

The issue of whether veterans are being turned down for student loan forgiveness has sparked significant concern and debate. Despite federal programs like the Public Service Loan Forgiveness (PSLF) and the Total and Permanent Disability (TPD) discharge, many veterans report facing barriers to accessing these benefits. Challenges include complex application processes, stringent eligibility criteria, and insufficient outreach or guidance from loan servicers. Additionally, some veterans who have served in qualifying public service roles, such as military service, struggle to meet technical requirements or face delays in processing their applications. Advocacy groups argue that these hurdles disproportionately affect veterans, who often rely on loan forgiveness to alleviate financial burdens after their service. As a result, calls for reform and increased transparency in the system have grown, highlighting the need to ensure that veterans receive the support and relief they were promised.

Explore related products

$26.87 $29.99

What You'll Learn

![]()

Eligibility Criteria for Veterans

Veterans seeking student loan forgiveness often face a labyrinth of eligibility criteria that can determine their financial future. One critical requirement is the Public Service Loan Forgiveness (PSLF) program, which mandates that veterans work full-time for a qualifying employer, such as a government organization or 501(c)(3) nonprofit, for at least 10 years while making 120 eligible payments. For veterans transitioning to civilian careers, understanding this criterion is essential, as it directly impacts their ability to qualify for forgiveness.

Another key eligibility factor is the Total and Permanent Disability (TPD) discharge, which offers immediate loan forgiveness for veterans with service-related disabilities. To qualify, veterans must provide documentation from the Department of Veterans Affairs (VA) certifying a disability rating of 100% or individual unemployability. This pathway is particularly vital for veterans whose disabilities prevent them from working, yet many remain unaware of this option or struggle with the documentation process.

The Veterans Education Assistance Program (VEAP) and Post-9/11 GI Bill also play a role in eligibility, though indirectly. While these programs primarily fund education, veterans who exhaust these benefits and take out loans may still qualify for forgiveness under broader programs like PSLF or income-driven repayment plans. However, the interplay between these programs can be confusing, often leading to veterans being turned down due to misunderstandings or misapplications.

A lesser-known criterion is the income-driven repayment (IDR) plan forgiveness, which forgives remaining loan balances after 20–25 years of qualifying payments. Veterans with lower incomes, especially those in public service roles, may benefit from this option. However, enrolling in the correct IDR plan and maintaining eligibility over decades requires meticulous record-keeping and annual recertification, which can be a barrier for some.

Practical tips for veterans navigating these criteria include: (1) consulting a VA benefits advisor to ensure all service-related disabilities are properly documented; (2) using the PSLF Help Tool provided by the U.S. Department of Education to verify employer eligibility; and (3) keeping detailed records of all loan payments and employment certifications. By proactively addressing these criteria, veterans can increase their chances of securing the forgiveness they deserve.

Erasing Old Student Loan Debt: A Guide to Forgiveness Removal

You may want to see also

Explore related products

![]()

Common Reasons for Denial

Veterans seeking student loan forgiveness often face denials due to administrative errors in their applications. A single misplaced digit in a Social Security number or an incorrect date can derail the entire process. For instance, the Public Service Loan Forgiveness (PSLF) program requires precise documentation of qualifying payments, and even a minor discrepancy can lead to rejection. To avoid this, veterans should double-check all forms, use certified mail for submissions, and retain copies of every document. A small investment in meticulousness can save months of frustration.

Another common pitfall is failing to meet the stringent employment certification requirements. Many veterans assume their military service automatically qualifies them for forgiveness, but programs like PSLF demand proof of full-time employment in a qualifying public service role post-service. For example, a veteran working part-time at a nonprofit or in a non-eligible position will be denied. Veterans should verify their employer’s eligibility using the PSLF Help Tool and submit Employment Certification Forms annually to track progress. Proactive documentation is key to avoiding this denial reason.

Income-driven repayment (IDR) plan miscalculations also frequently lead to denials. Veterans enrolled in IDR plans must recertify their income and family size annually, but missed deadlines or incorrect income reporting can reset their forgiveness clock. For instance, a veteran who fails to update their income after a raise may see their payments increase, throwing off their eligibility timeline. To prevent this, set calendar reminders for recertification deadlines and use the IRS Data Retrieval Tool for accurate income reporting. Staying on top of these details ensures steady progress toward forgiveness.

Lastly, veterans often overlook the importance of loan type in forgiveness eligibility. Only federal Direct Loans qualify for programs like PSLF or IDR forgiveness; Federal Family Education Loans (FFEL) or Perkins Loans do not. A veteran with a FFEL loan might spend years making payments, only to discover their loan type disqualifies them. The solution? Consolidate ineligible loans into a Direct Consolidation Loan to become eligible. This single step can open the door to forgiveness opportunities otherwise out of reach.

Student Loan Forgiveness: Boosting Financial Freedom and Quality of Life

You may want to see also

Explore related products

![]()

Impact of Military Service on Applications

Military service often complicates the student loan forgiveness process for veterans, creating unique barriers that civilians don’t face. One significant issue is the documentation required to prove eligibility. Veterans must provide detailed records of their service, discharge status, and sometimes even specific deployment dates. These documents, often stored in military archives, can be difficult to retrieve, especially for older veterans or those with incomplete records. Without them, applications are frequently denied, leaving veterans in limbo despite their sacrifices.

Another challenge arises from the intersection of military service and income-driven repayment plans. Veterans transitioning to civilian life often face unstable employment or lower-paying jobs initially, making them prime candidates for income-driven plans. However, the Public Service Loan Forgiveness (PSLF) program, which many veterans rely on, requires 120 qualifying payments while working full-time for a qualifying employer. Military service, though public, is not always recognized as qualifying employment, and veterans may struggle to align their service years with the program’s strict criteria. This gap leaves many veterans ineligible for forgiveness they believed they earned.

The complexity of military benefits further muddies the waters. Veterans may receive education benefits like the GI Bill, which can reduce their reliance on student loans but also create confusion about eligibility for forgiveness programs. For instance, if a veteran uses the GI Bill to cover tuition but still takes out loans for living expenses, they may assume their service qualifies them for forgiveness. However, the Department of Education evaluates loan forgiveness based on repayment history and employment, not on the use of military benefits. This misunderstanding leads to denied applications and frustration.

Practical steps can mitigate these challenges. Veterans should start by requesting a complete DD-214 and military service records through the National Archives or their branch’s personnel office. They should also consult with a certified student loan advisor who specializes in veteran cases to navigate the PSLF or income-driven repayment plans. Additionally, veterans should keep detailed records of their loan payments and employment history, ensuring they meet the 120-payment threshold for PSLF. Finally, advocacy groups like the Veterans Education Project can provide resources and support to challenge denials and clarify eligibility criteria.

In conclusion, military service introduces unique complexities to student loan forgiveness applications, from documentation hurdles to eligibility misunderstandings. By understanding these challenges and taking proactive steps, veterans can improve their chances of securing the forgiveness they deserve. The system may be flawed, but with persistence and the right resources, veterans can navigate it successfully.

Teacher Loan Forgiveness: A Step-by-Step Guide to Debt Relief

You may want to see also

Explore related products

![]()

Appeal Process for Rejected Claims

Veterans facing rejection of their student loan forgiveness claims often feel disheartened, but the appeal process offers a critical second chance. Understanding this pathway is essential for those determined to secure the benefits they’ve earned. The first step involves reviewing the denial letter carefully to identify the specific reason for rejection, whether it’s incomplete documentation, eligibility criteria misinterpretation, or procedural errors. This clarity is the foundation for a targeted appeal.

Once the reason for denial is understood, gather all necessary evidence to address the issue. For instance, if the rejection cites missing service records, obtain certified copies from the National Archives or the Department of Defense. If the denial stems from a misinterpretation of the Public Service Loan Forgiveness (PSLF) program’s requirements, compile detailed employment records and payment histories to prove eligibility. Organizing this documentation chronologically and labeling each piece clearly can significantly strengthen the appeal.

The appeal itself should be a concise, formal letter that directly addresses the denial reason. Begin by acknowledging the initial decision and then methodically refute it using the evidence gathered. For example, if the rejection claims insufficient qualifying payments, include a spreadsheet detailing each payment date, amount, and servicer. Persuasive language is key; frame the appeal as a request for reconsideration based on factual corrections rather than a complaint.

Caution must be exercised to adhere to strict deadlines, typically 60 to 90 days from the denial notice, depending on the program. Missing this window can result in forfeiture of appeal rights. Additionally, avoid overwhelming the reviewer with excessive documentation; focus on the most relevant evidence. Finally, consider consulting a student loan attorney or veterans’ advocate for guidance, especially in complex cases. Their expertise can ensure the appeal is both comprehensive and compliant with procedural rules.

In conclusion, the appeal process for rejected student loan forgiveness claims is a structured yet nuanced pathway. By meticulously addressing the denial reason, organizing compelling evidence, and crafting a persuasive argument, veterans can significantly improve their chances of overturning an unfavorable decision. Persistence and attention to detail are paramount in this endeavor.

Are State Workers Taxed on Student Loan Forgiveness Benefits?

You may want to see also

Explore related products

![]()

Alternatives to Loan Forgiveness Programs

Veterans facing hurdles in securing student loan forgiveness can explore alternative strategies to manage their debt effectively. One viable option is income-driven repayment (IDR) plans, which adjust monthly payments based on income and family size. For instance, the Pay As You Earn (PAYE) plan caps payments at 10% of discretionary income and forgives remaining balances after 20 years of qualifying payments. Veterans with lower incomes or unstable employment can benefit significantly from these plans, as they provide immediate financial relief and a clear path to eventual forgiveness.

Another alternative is refinancing student loans through private lenders. While this option eliminates eligibility for federal forgiveness programs, it can offer lower interest rates and more manageable terms. Veterans with strong credit scores or stable incomes may qualify for rates as low as 3-5%, reducing overall debt burden. However, this approach requires careful consideration, as it removes access to federal protections like deferment, forbearance, and IDR plans. Veterans should weigh the long-term savings against the loss of these benefits.

Employer-sponsored repayment assistance programs (LRAPs) present a third alternative, particularly for veterans working in public service or high-demand fields. Companies like Aetna and Fidelity offer up to $2,000-$10,000 annually in student loan contributions as part of their benefits packages. Veterans should research potential employers to identify those with robust LRAPs, as this can significantly offset loan payments without relying on federal forgiveness programs.

Lastly, veterans can leverage state-specific loan repayment assistance programs tailored to their profession or location. For example, the Health Professions Loan Repayment Program in California offers up to $50,000 in loan repayment for veterans working in healthcare in underserved areas. Similarly, the Veterans Education Assistance Program (VEAP) provides matching contributions for education expenses, indirectly reducing loan reliance. Veterans should explore state and local resources to uncover these lesser-known but impactful opportunities.

By combining these alternatives—IDR plans, refinancing, employer LRAPs, and state programs—veterans can create a multifaceted strategy to address student loan debt, even if federal forgiveness remains out of reach. Each option requires careful evaluation based on individual circumstances, but together, they offer a roadmap to financial stability.

Cares Act Student Loan Forgiveness: Step-by-Step Application Guide

You may want to see also

Frequently asked questions

No, veterans are not automatically eligible for student loan forgiveness. Eligibility depends on specific programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, and veterans must meet the program requirements.

Veterans may be turned down if they do not meet program criteria, such as having the wrong type of loan (e.g., private loans instead of federal loans), failing to make qualifying payments, or not working in a qualifying public service job for programs like PSLF.

While there is no exclusive program for veterans, they may qualify for the Total and Permanent Disability (TPD) discharge if they have a service-related disability. Additionally, veterans can benefit from PSLF or income-driven repayment plans if they meet the requirements.

Military service itself does not directly count toward loan forgiveness, but veterans can use their time in service to meet requirements for programs like PSLF if they work in a qualifying public service job afterward.

Veterans denied forgiveness should review the denial reason, ensure all paperwork is accurate, and explore other options like appealing the decision, consolidating loans, or switching to an income-driven repayment plan. Consulting a student loan advisor or VA representative can also help.