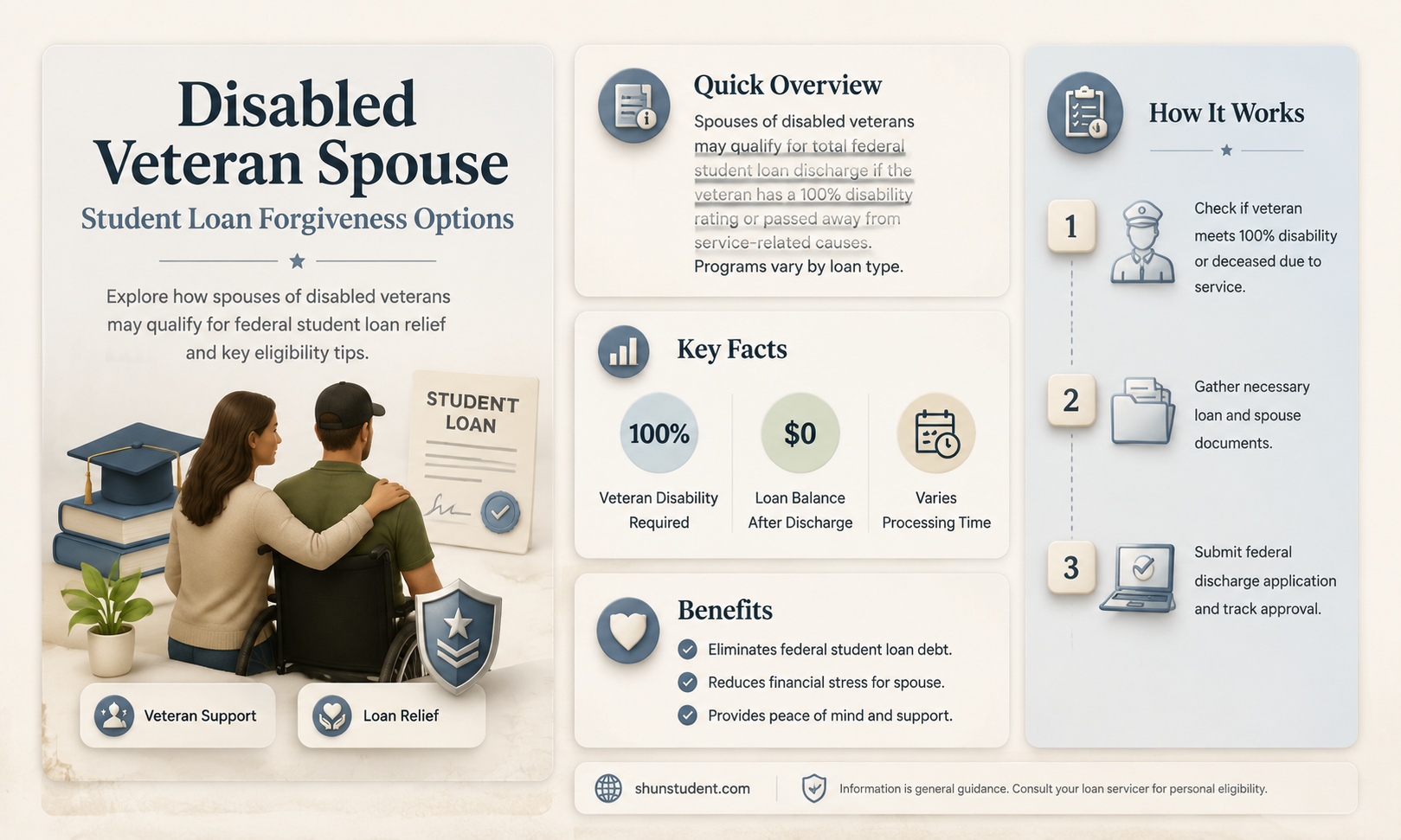

Disabled veterans and their spouses often face unique financial challenges, and one pressing concern is the burden of student loan debt. Many are unaware that certain programs and benefits exist to provide relief, including potential student loan forgiveness. For spouses of disabled veterans, understanding eligibility criteria and available options is crucial. Programs like the Total and Permanent Disability (TPD) discharge and Public Service Loan Forgiveness (PSLF) may offer pathways to debt relief, depending on the veteran’s disability status and the spouse’s employment or financial situation. Exploring these opportunities can significantly ease financial strain and improve overall well-being for families who have sacrificed so much in service to their country.

| Characteristics | Values |

|---|---|

| Eligibility for Spouse | Spouses of disabled veterans may qualify for student loan forgiveness under specific programs. |

| Total and Permanent Disability (TPD) Discharge | If the veteran spouse is deemed totally and permanently disabled, the spouse may apply for TPD discharge on their own federal student loans. |

| Documentation Required | Proof of the veteran’s disability (e.g., VA disability rating) and marriage certificate. |

| Loan Types Covered | Federal student loans (Direct Loans, FFEL, Perkins Loans) are eligible for TPD discharge. |

| Tax Implications | TPD discharge may be tax-free for discharges granted after December 31, 2017, and before January 1, 2026. |

| Application Process | Submit an application through the U.S. Department of Education or loan servicer, including disability documentation. |

| Monitoring Period | After approval, a 3-year monitoring period may apply to ensure no significant income is earned. |

| Private Loans | Private student loans are not eligible for TPD discharge; forgiveness options vary by lender. |

| Additional Programs | Spouses may also explore Public Service Loan Forgiveness (PSLF) or income-driven repayment plans if eligible. |

| Veterans Affairs (VA) Assistance | The VA does not directly forgive spouse loans, but disability benefits may indirectly assist in repayment. |

| State-Specific Programs | Some states offer additional loan forgiveness programs for spouses of disabled veterans. |

| Recent Updates | As of 2023, no new federal programs specifically target spouses of disabled veterans for loan forgiveness. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Spouses

Spouses of disabled veterans seeking student loan forgiveness must navigate a complex web of eligibility criteria tied to specific programs. The Total and Permanent Disability (TPD) Discharge program, for instance, extends to spouses if the veteran’s disability is service-connected and deemed permanent by the Department of Veterans Affairs (VA). Here, the spouse’s loans—both federal and, in some cases, private—may qualify for discharge, but only if the veteran’s disability status meets VA standards. This criterion hinges on the veteran’s VA disability rating, which must be 100% permanent and total (P&T).

Beyond the TPD program, spouses may explore the Public Service Loan Forgiveness (PSLF) program if they work in qualifying public service roles. While not exclusive to spouses of disabled veterans, this program forgives remaining federal loan balances after 120 qualifying payments. Spouses must maintain full-time employment in sectors like government, education, or nonprofits and adhere to strict repayment plan requirements, such as income-driven plans. Combining this with the veteran’s disability status can strengthen the spouse’s case, particularly if the veteran’s condition impacts household finances.

A lesser-known pathway is the Disability Discharge via Physician’s Certification, which applies if the spouse themselves has a qualifying disability. However, if the spouse is healthy, they must rely on the veteran’s disability status. In such cases, documentation is critical: spouses must submit VA disability award letters, physician statements, and loan servicer forms to prove eligibility. Missteps in paperwork often delay or derail applications, so precision is paramount.

Comparatively, state-specific programs may offer additional relief. For example, Texas provides the Hazlewood Act exemption for spouses of disabled veterans, which waives tuition at public colleges but does not directly address student loans. Meanwhile, California’s CalVet program offers loan assistance for spouses, though eligibility varies by county. These regional options underscore the importance of researching local benefits alongside federal programs.

In conclusion, spouses of disabled veterans must strategically align their applications with program-specific criteria. Whether leveraging the veteran’s VA disability rating, pursuing public service roles, or exploring state-level aid, understanding these nuances is key. Proactive documentation, coupled with awareness of regional benefits, maximizes the chances of securing loan forgiveness.

Mastering Student Loan Forgiveness: Avoid Rejection with Proven Strategies

You may want to see also

Explore related products

![]()

Types of Loans Covered

Federal student loans, particularly those under the William D. Ford Federal Direct Loan Program, are the primary candidates for forgiveness programs available to disabled veterans and their spouses. This includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans. If you or your spouse has taken out these loans, understanding their eligibility for forgiveness is crucial. For instance, the Total and Permanent Disability (TPD) discharge program can erase these debts entirely if the veteran meets the disability criteria outlined by the U.S. Department of Veterans Affairs (VA).

Private student loans, on the other hand, are not covered by federal forgiveness programs like TPD discharge. Lenders like Sallie Mae, Navient, or Discover operate independently and are not bound by federal regulations. However, some private lenders may offer disability discharge options, though these are rare and often require extensive documentation. If you’re dealing with private loans, contact the lender directly to inquire about potential relief options. Alternatively, explore refinancing with a lender that offers more flexible terms for disabled veterans or their spouses.

Parent PLUS Loans, often taken out by parents to fund their child’s education, can also be discharged through the TPD program if the parent borrower is disabled. However, if the loan was transferred to the child (the veteran) or their spouse, the eligibility shifts to the new borrower’s disability status. For example, if a disabled veteran’s spouse took over the PLUS Loan, they could seek forgiveness based on the veteran’s VA disability rating. This requires careful documentation linking the veteran’s disability to the loan discharge application.

Perkins Loans, though less common today, are another federal loan type eligible for forgiveness under the TPD program. If you or your spouse has an outstanding Perkins Loan, it can be discharged 100% if the veteran meets the VA’s disability criteria. Additionally, Perkins Loans may qualify for cancellation through the Veterans’ Total and Permanent Disability Discharge, even if the borrower is the spouse. Ensure you submit the VA’s disability documentation to the loan servicer to initiate the process.

Consolidation loans, which combine multiple federal student loans into one, retain their eligibility for TPD discharge if the underlying loans were federal. However, consolidating loans can reset the clock on certain forgiveness programs, so proceed with caution. For disabled veterans’ spouses, consolidating loans might simplify repayment but could delay access to forgiveness benefits. Always consult a financial advisor or loan servicer before consolidating to ensure it aligns with your forgiveness goals.

Understanding which loans qualify for forgiveness is the first step toward financial relief for disabled veterans and their spouses. Federal loans offer the most straightforward path, while private loans require creative solutions. By identifying the loan type and its eligibility, you can navigate the forgiveness process with clarity and confidence.

Forgiven Student Loan Accounting: A Step-by-Step Guide for Taxpayers

You may want to see also

Explore related products

![]()

Application Process Steps

Disabled veterans and their spouses may qualify for student loan forgiveness through programs like the Total and Permanent Disability (TPD) discharge, but the application process requires precision and documentation. The first step involves confirming eligibility, which hinges on the veteran’s disability status. The U.S. Department of Veterans Affairs (VA) must classify the veteran as totally and permanently disabled, or the veteran must have received a 100% disability rating. Spouses are not directly eligible but can benefit if they hold the loans and meet specific criteria, such as being a co-borrower or having consolidated loans under their name.

Once eligibility is confirmed, gather essential documents. These include proof of the veteran’s disability rating, such as a VA disability award letter, and evidence of the loan type (federal loans qualify, private loans do not). If the spouse is applying, they must provide marriage certification and loan ownership proof. For TPD discharge, the application can be submitted via the U.S. Department of Education’s online portal or by mail. Alternatively, if the veteran is unable to apply, the spouse can act as a representative payee with proper authorization.

The third step involves monitoring the application’s progress. After submission, the Department of Education reviews the case, which can take several weeks. During this period, loan payments may be suspended, but interest may accrue. Applicants should keep records of all communications and follow up if there are delays. Approval results in tax-free loan forgiveness, but denied applications can be appealed with additional evidence.

A critical caution: beware of scams targeting veterans and their families. Legitimate applications are free and handled directly through official government channels. Avoid third-party services promising expedited forgiveness for a fee. Additionally, understand that forgiven amounts may have tax implications, though TPD discharges are currently tax-free under the American Rescue Act through 2025.

In conclusion, the application process for disabled veteran spouses seeking student loan forgiveness demands meticulous preparation and adherence to official guidelines. By confirming eligibility, gathering precise documentation, and staying vigilant against fraud, applicants can navigate this complex system effectively. The reward—financial relief—is worth the effort for those who qualify.

Medical Hardship and Student Loans: Exploring Forgiveness Options for Borrowers

You may want to see also

Explore related products

![]()

Required Documentation List

To secure student loan forgiveness as a disabled veteran’s spouse, meticulous documentation is non-negotiable. Lenders and forgiveness programs demand proof of eligibility, leaving no room for ambiguity. Start with the veteran’s VA Disability Award Letter, which verifies their disability rating and status. This document is the cornerstone of your application, as it directly links the veteran’s condition to your eligibility for programs like Total and Permanent Disability (TPD) discharge. Without it, your request lacks credibility.

Next, gather marriage and identity verification documents. A certified copy of your marriage certificate establishes your legal relationship to the veteran, while government-issued IDs for both parties confirm identities. For widowed spouses, a death certificate is essential. These documents bridge the gap between the veteran’s disability and your claim, ensuring you’re not just a distant relative but a direct beneficiary.

Financial records play a surprising role in this process. While not always required, tax returns and loan statements can demonstrate your inability to repay the debt, especially if the veteran’s disability impacts household income. Some programs, like Public Service Loan Forgiveness (PSLF), may also require proof of employment in qualifying sectors. Keep these documents organized and up-to-date to streamline your application.

Finally, don’t overlook medical evidence if the veteran’s disability is under review or contested. While the VA Disability Award Letter typically suffices, additional medical records or physician statements can bolster your case. This is particularly crucial for disabilities that worsen over time or require frequent reassessment. Proactive documentation not only strengthens your application but also prepares you for potential audits or follow-up inquiries.

In summary, the required documentation list is a checklist of trust. Each piece of paper tells a story—one of eligibility, relationship, and need. Approach this process with precision, ensuring every document is current, certified, and relevant. The goal isn’t just to apply but to eliminate any reason for denial. With the right paperwork, you transform a request into an undeniable claim.

Student Loan Forgiveness and Taxes: What You Need to Report

You may want to see also

Explore related products

![]()

Impact on Credit Score

Pursuing student loan forgiveness as a disabled veteran’s spouse can indirectly affect your credit score, depending on how the process is managed. During the application period, your loans may enter a temporary status such as "pending" or "in review," which itself does not harm your credit. However, if payments are paused or delayed while awaiting approval, the loan servicer may report the account as "deferred" or "in forbearance" to credit bureaus. While these statuses do not lower your score, they can signal financial stress to lenders, potentially affecting future credit applications.

The direct impact on your credit score hinges on whether the forgiveness program requires you to consolidate loans or enroll in a specific repayment plan. Loan consolidation often involves a hard credit inquiry, which can temporarily reduce your score by a few points. Additionally, if consolidation results in closing older accounts, it may shorten your average credit history, another factor that influences your score. However, these effects are usually minor and short-lived, especially compared to the long-term benefits of forgiveness.

A critical consideration is how forgiveness programs handle reporting to credit bureaus post-approval. Total and Permanent Disability (TPD) discharge, for instance, removes the debt entirely, and the account is typically reported as "paid in full" or "settled," which is neutral or positive for your credit. However, partial forgiveness programs may leave a remaining balance, and how this is reported—whether as a new loan or adjusted account—can vary. Monitoring your credit report during this transition is essential to ensure accuracy and address any discrepancies promptly.

To minimize credit score impact, maintain timely payments on other credit accounts while pursuing forgiveness. If your loans are in limbo, consider setting up payment reminders or automatic payments for credit cards and other debts to demonstrate financial responsibility. Additionally, avoid opening new credit accounts during this period, as multiple inquiries or new debt can compound any temporary score reductions. Proactive management ensures that the pursuit of student loan forgiveness remains a financial relief, not a credit setback.

Understanding Income Calculation for Student Loan Forgiveness Programs

You may want to see also

Frequently asked questions

Yes, a disabled veteran's spouse may be eligible for student loan forgiveness through programs like the Total and Permanent Disability (TPD) Discharge if the spouse is the borrower and meets the disability criteria, or through Public Service Loan Forgiveness (PSLF) if they work in qualifying public service roles.

No, the disabled veteran's status does not automatically qualify their spouse for student loan forgiveness. The spouse must meet specific eligibility criteria for programs like TPD Discharge (based on their own disability) or PSLF (based on their employment).

The VA does not directly offer student loan forgiveness for spouses of disabled veterans. However, the spouse may explore federal programs like TPD Discharge or PSLF, or state-specific assistance programs.

For TPD Discharge, the spouse must provide proof of their own total and permanent disability, such as a physician's certification or SSA disability determination. For PSLF, they need to submit employment certification forms and proof of qualifying payments.

Yes, spouses of disabled veterans can enroll in income-driven repayment (IDR) plans, which cap monthly payments based on income and family size. After 20–25 years of qualifying payments, any remaining balance may be forgiven, though it may be taxable.