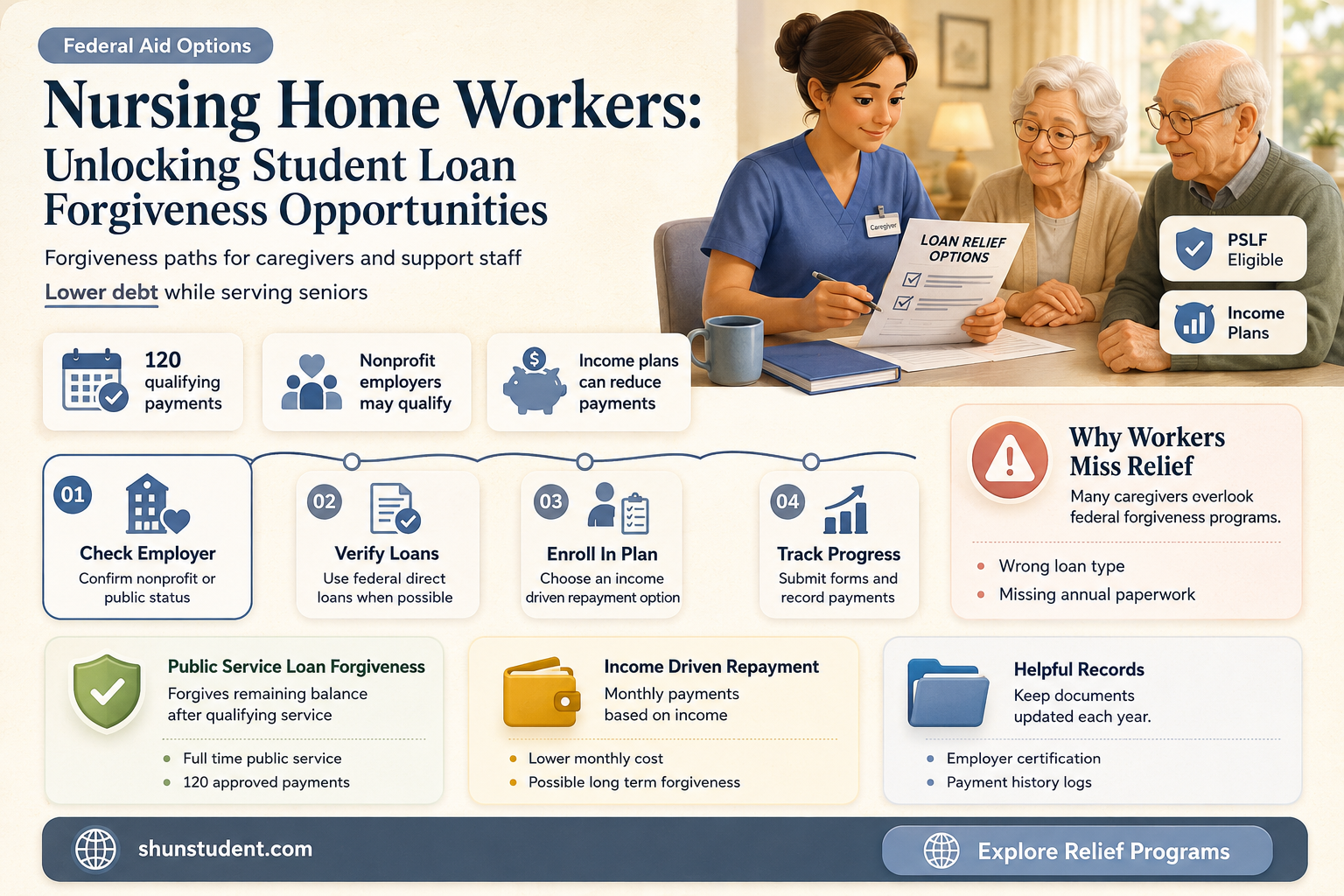

Nursing home employees play a vital role in providing care for vulnerable populations, yet many face significant financial burdens due to student loan debt. The question of whether these dedicated professionals can have their student loans forgiven is a pressing concern, as it could alleviate financial stress and encourage more individuals to pursue careers in this essential field. Various federal and state programs, such as the Public Service Loan Forgiveness (PSLF) program, offer opportunities for loan forgiveness to those working in public service roles, including healthcare. However, navigating the eligibility requirements and application processes can be complex, leaving many nursing home employees unsure of their options. Understanding the available pathways to student loan forgiveness is crucial for both current and prospective nursing home workers seeking financial relief and long-term career stability.

| Characteristics | Values |

|---|---|

| Eligibility for Loan Forgiveness | Nursing home employees may qualify for student loan forgiveness through programs like Public Service Loan Forgiveness (PSLF) or employer-specific forgiveness programs. |

| Public Service Loan Forgiveness (PSLF) | Requires 120 qualifying payments while working full-time for a qualifying employer (e.g., nonprofit or government-owned nursing homes). Forgives remaining balance after 10 years. |

| Employer-Sponsored Forgiveness | Some nursing homes offer loan repayment assistance or forgiveness as part of their benefits package, depending on the employer and role. |

| Federal Perkins Loan Cancellation | Up to 100% cancellation for nurses working full-time in eligible positions, including long-term care facilities, over 5 years. Program ended in 2017, but existing borrowers may still qualify. |

| Nurse Corps Loan Repayment Program | Offers up to 85% loan repayment for nurses working in Critical Shortage Facilities, including some nursing homes, for 3 years. |

| State-Specific Programs | Some states offer loan forgiveness or repayment programs for healthcare workers, including nursing home employees, depending on location and role. |

| Income-Driven Repayment (IDR) Forgiveness | After 20-25 years of qualifying payments under IDR plans, remaining balance may be forgiven, though this is not specific to nursing home employees. |

| Tax Implications | PSLF and Perkins cancellation are tax-free, but other programs may require borrowers to pay taxes on forgiven amounts. |

| Loan Type Requirements | Forgiveness typically applies to federal student loans (e.g., Direct Loans). Private loans are generally not eligible unless refinanced into a federal loan. |

| Employment Requirements | Must work full-time (30+ hours/week) in a qualifying role and facility. Part-time work may be considered if combined to meet full-time equivalency. |

| Documentation Needed | Employment Certification Form (ECF) for PSLF, proof of employment, and loan repayment history are required for most programs. |

| Program Availability | Availability depends on federal, state, or employer funding and may change over time. |

| Impact on Credit Score | Loan forgiveness does not negatively impact credit score; forgiven amounts are removed from the loan balance. |

| Application Process | Requires submitting applications and documentation to the loan servicer or program administrator. |

| Recent Updates | Temporary PSLF waivers (ended Oct. 31, 2022) allowed past payments to count, even if not under PSLF. Future changes may expand eligibility. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Loan Forgiveness

Nursing home employees seeking student loan forgiveness must navigate a complex web of eligibility criteria tied to specific programs. The Public Service Loan Forgiveness (PSLF) program stands out as a primary option, requiring 120 qualifying payments while working full-time for a nonprofit or government employer. Nursing homes often qualify if they are nonprofit or government-owned, but employees must verify their employer’s status using the PSLF Help Tool. Additionally, loans must be federal Direct Loans, and payments must be made under an income-driven repayment plan. Partial employment, such as part-time work, may disqualify applicants unless they meet the program’s full-time equivalency standards, typically 30 hours per week.

Another pathway is the Federal Perkins Loan Cancellation program, though it is no longer accepting new loans. Eligible nursing home employees with existing Perkins Loans can have up to 100% of their loans forgiven after five years of full-time service in a qualifying role. This program requires annual cancellation applications, and forgiveness is granted incrementally: 20% after the first and second years, 30% after the third and fourth years, and 10% after the fifth year. While less accessible now, those with Perkins Loans should explore this option if applicable.

State-based loan forgiveness programs offer additional opportunities, often tailored to address local healthcare workforce shortages. For instance, the New York State Clinical Faculty Loan Forgiveness Program provides up to $20,000 annually for eligible nursing professionals who teach in clinical settings, including nursing homes. Similarly, the Maryland Nurse Support Program II offers up to $10,000 annually for licensed nurses working in long-term care facilities. These programs typically require a service commitment, ranging from two to four years, and may have specific licensure or employment duration requirements.

A critical yet often overlooked criterion is documentation. Applicants must maintain meticulous records of employment, payments, and certifications. For PSLF, submitting the Employer Certification Form annually or when changing jobs ensures a clear record of qualifying employment. For state programs, proof of licensure, employment contracts, and service hours are frequently required. Failure to provide adequate documentation can result in denial, even if all other criteria are met.

Finally, nursing home employees should consider their long-term career trajectory when pursuing loan forgiveness. Programs like PSLF require a decade of commitment, during which job changes or repayment plan adjustments could disrupt eligibility. Balancing immediate financial relief with future career goals is essential. For example, transitioning to a higher-paying role mid-career might disqualify an applicant from income-driven repayment plans, halting progress toward forgiveness. Strategic planning, coupled with regular reviews of program guidelines, ensures sustained eligibility and maximizes the likelihood of successful loan forgiveness.

Mastering the Art of Writing a Student Loan Forgiveness Letter

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) Requirements

Nursing home employees burdened by student loan debt may find relief through the Public Service Loan Forgiveness (PSLF) program. This federal initiative offers a pathway to debt forgiveness after 120 qualifying payments, but understanding its requirements is crucial to avoid pitfalls.

First, eligibility hinges on employment. You must work full-time for a qualifying employer, which includes government organizations at any level (federal, state, local) and certain non-profit organizations. Many nursing homes, particularly those operated by government entities or non-profits, fall under this umbrella. However, private, for-profit nursing homes typically don't qualify.

Secondly, not all loan types are eligible. Only Direct Loans qualify for PSLF. If you have Federal Family Education Loans (FFEL) or Perkins Loans, you'll need to consolidate them into a Direct Consolidation Loan to participate. This step is often overlooked, leading to years of ineligible payments.

Additionally, repayment plan selection matters. You must be enrolled in an income-driven repayment (IDR) plan. These plans cap your monthly payments based on your income and family size, making them more manageable while working towards forgiveness. Popular IDR plans include Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE).

Finally, the 120 qualifying payments must be made on time and in full. Partial payments or payments made during periods of deferment or forbearance don't count. Keeping meticulous records of your payments and employment is essential. The PSLF program requires certification of your employment annually or whenever you switch jobs. This proactive approach ensures you're on track and allows for course correction if needed.

USPS Employment and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Employer Certification Process

Nursing home employees seeking student loan forgiveness often encounter the Public Service Loan Forgiveness (PSLF) program, which requires a meticulous employer certification process. This step is pivotal, as it verifies that the borrower’s employment qualifies for forgiveness. Without proper certification, even years of eligible service may be disqualified. The process begins with the borrower submitting an Employment Certification Form (ECF) to their employer, who must confirm the organization’s eligibility as a tax-exempt nonprofit or government entity. Nursing homes, often operated by such organizations, typically meet this criterion, but verification is essential.

The employer’s role extends beyond a simple signature. They must provide detailed information, including the borrower’s job title, employment dates, and the organization’s tax status. Accuracy is critical, as errors can delay or invalidate the certification. For instance, misclassifying the employer’s tax status or omitting employment dates can lead to rejection. Borrowers should proactively review the form with their employer to ensure all fields are completed correctly. Additionally, submitting the ECF periodically—not just at the end of employment—can help track qualifying payments and identify issues early.

One common pitfall is assuming all nursing homes qualify automatically. While many are affiliated with nonprofit or government entities, some operate as for-profit businesses, rendering their employees ineligible for PSLF. Borrowers must verify their employer’s status using the IRS Tax Exempt Organization Search tool or consult HR for documentation. Another challenge arises when nursing homes are part of larger healthcare networks. In such cases, the borrower must confirm that their specific facility or department falls under the qualifying umbrella.

To streamline the process, borrowers should maintain open communication with their employer’s HR or payroll department. Providing clear instructions and deadlines can expedite certification. For example, explaining the purpose of the ECF and its role in loan forgiveness can motivate employers to prioritize the task. Borrowers should also keep copies of all submitted forms and follow up if they haven’t received confirmation within 30 days. This proactive approach minimizes the risk of lost or overlooked certifications.

In conclusion, the employer certification process is a critical yet often overlooked step in securing student loan forgiveness for nursing home employees. By understanding the requirements, verifying employer eligibility, and maintaining meticulous records, borrowers can navigate this process effectively. While it demands attention to detail and persistence, successful certification brings borrowers one step closer to financial relief. For nursing home employees, this effort not only alleviates personal debt but also reinforces their commitment to a vital yet undervalued profession.

Are Student Loan Forgiveness Texts Real or Scams?

You may want to see also

Explore related products

$12.95 $22.99

![]()

Income-Driven Repayment Plans

Nursing home employees burdened by student loan debt often overlook Income-Driven Repayment (IDR) plans as a viable solution. These plans, offered by the federal government, adjust monthly payments based on income and family size, potentially lowering them to as little as $0. For instance, a certified nursing assistant earning $35,000 annually with $50,000 in loans could see payments drop from $500 to $150 under the Revised Pay As You Earn (REPAYE) plan. This reduction not only eases financial strain but also sets the stage for loan forgiveness after 20–25 years of qualifying payments.

To enroll in an IDR plan, nursing home employees must first consolidate any Federal Family Education Loans (FFEL) into a Direct Consolidation Loan, as only Direct Loans qualify. Next, they complete the IDR application, providing income documentation such as tax returns or pay stubs. The process is free, but borrowers should beware of third-party companies charging fees for assistance. Once enrolled, annual recertification is mandatory to ensure payments remain aligned with current income. Failure to recertify can result in a return to the standard repayment plan, often with a higher monthly payment.

A critical yet underutilized aspect of IDR plans is their synergy with Public Service Loan Forgiveness (PSLFW). Nursing home employees working full-time for a nonprofit or government employer can qualify for tax-free loan forgiveness after 10 years of payments. However, these payments must be made under an IDR plan to count toward PSLF. For example, a registered nurse earning $45,000 annually could pay approximately $200 monthly under an IDR plan, with the remaining balance forgiven after 120 qualifying payments. This dual strategy maximizes debt relief for those committed to long-term care careers.

Despite their benefits, IDR plans are not without drawbacks. Lower monthly payments extend the loan term, increasing the total interest paid over time. Additionally, forgiven amounts after 20–25 years may be taxed as income, though current legislation offers temporary relief through 2025. Nursing home employees should weigh these factors against their financial goals and consult resources like the Federal Student Aid website or a certified loan counselor. With careful planning, IDR plans can transform overwhelming debt into manageable obligations, paving the way for financial stability.

Oregon Student Loan Forgiveness: Exploring State Programs for Borrowers

You may want to see also

Explore related products

$7.99

![]()

State-Specific Forgiveness Programs

Nursing home employees burdened by student loan debt may find relief through state-specific forgiveness programs, which often target healthcare workers in underserved areas or high-demand roles. These programs vary widely in eligibility criteria, award amounts, and application processes, reflecting each state’s unique healthcare needs and budgetary priorities. For instance, New York’s Clinical Faculty Loan Forgiveness Program offers up to $20,000 annually for nurses who teach in accredited nursing programs, while Minnesota’s Nurse Loan Forgiveness Program provides up to $6,000 per year for licensed practical or registered nurses working in long-term care facilities. Understanding these state-specific options requires careful research and alignment with individual career paths.

To navigate these programs effectively, nursing home employees should first identify their state’s offerings by consulting local health departments or higher education agencies. For example, California’s Bachelor of Science Nursing Loan Repayment Program forgives up to $10,000 annually for nurses working in federally qualified health centers or nursing homes in designated shortage areas. In contrast, Texas’ Nursing Faculty Loan Repayment Program targets nurse educators, offering up to $5,000 per year. A critical step is verifying whether nursing home employment qualifies, as some programs prioritize primary care or rural settings over long-term care facilities.

One common thread among state programs is the requirement of a service commitment, typically ranging from two to four years. For instance, Illinois’ Nurse Educator Loan Repayment Program requires a three-year teaching commitment in exchange for up to $5,000 annually. Nursing home employees should weigh the long-term benefits of loan forgiveness against the commitment’s impact on career flexibility. Additionally, applicants must ensure they meet licensing and employment status requirements, as many programs exclude part-time workers or those with disciplinary histories.

A comparative analysis reveals that states with aging populations, such as Florida and Pennsylvania, often have more robust programs for long-term care workers. Florida’s Nursing Student Loan Forgiveness Program offers up to $4,000 annually for nurses working in state-approved facilities, including nursing homes. Pennsylvania’s Primary Care Loan Repayment Program includes long-term care nurses in its eligibility criteria, providing up to $60,000 over four years. These examples highlight the importance of geographic considerations when exploring forgiveness opportunities.

In conclusion, state-specific forgiveness programs offer a viable pathway for nursing home employees to alleviate student loan debt, but success hinges on meticulous planning and eligibility alignment. By targeting programs like Minnesota’s $6,000 annual award or California’s $10,000 repayment option, nurses can strategically reduce their financial burden while contributing to critical healthcare roles. Practical tips include maintaining detailed employment records, staying informed about application deadlines, and leveraging state-specific resources to maximize forgiveness potential.

Military Student Loan Forgiveness: What Servicemembers Need to Know

You may want to see also

Frequently asked questions

Yes, nursing home employees may qualify for student loan forgiveness through programs like Public Service Loan Forgiveness (PSLF) if they work full-time for a qualifying employer and meet other program requirements.

PSLF forgives the remaining balance on federal Direct Loans after 120 qualifying payments while working full-time for a qualifying employer, such as a nonprofit or government-run nursing home.

Not all nursing homes qualify. Only those that are government-run or nonprofit organizations are eligible employers for PSLF. Private, for-profit nursing homes do not qualify.

Yes, nursing home employees may also qualify for loan forgiveness through state-based programs, the Nurse Corps Loan Repayment Program, or income-driven repayment plans, depending on their role and eligibility.

Employees should ensure they have federal Direct Loans, work full-time for a qualifying employer, make payments under an income-driven repayment plan, and submit the Employer Certification Form regularly to track qualifying payments.