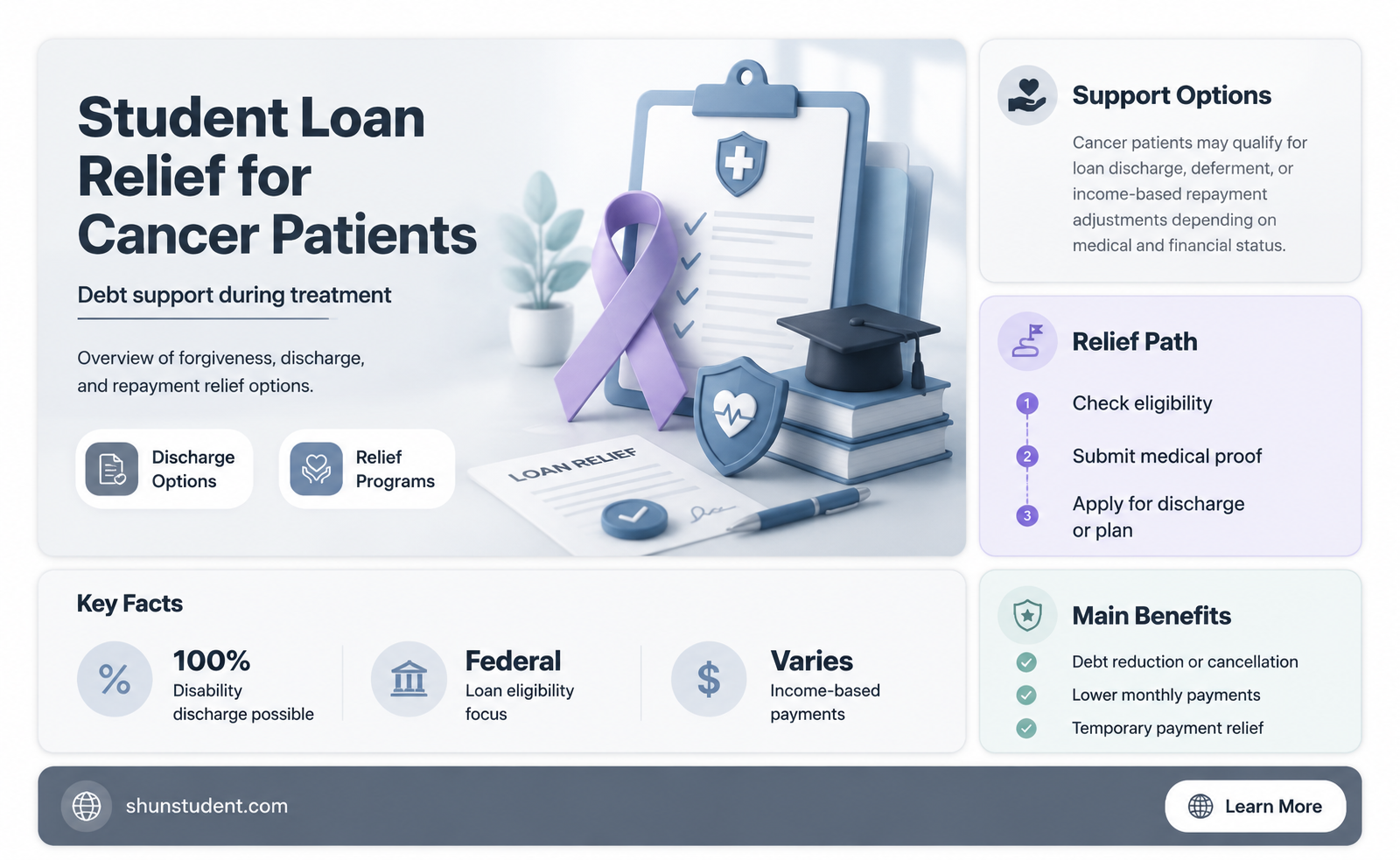

Cancer patients facing financial strain due to their diagnosis may wonder if their student loans can be forgiven. While there is no automatic forgiveness specifically for cancer patients, several options exist to alleviate the burden. These include Total and Permanent Disability (TPD) discharge, which forgives federal student loans for individuals unable to work due to a qualifying disability, including advanced cancer. Additionally, income-driven repayment plans can lower monthly payments based on income and family size, potentially leading to loan forgiveness after a set period. Cancer patients may also explore loan deferment or forbearance to temporarily pause payments, though interest may still accrue. State-specific programs and private lender policies might offer further assistance. Consulting with a financial advisor or student loan specialist is crucial to navigate these options effectively.

| Characteristics | Values |

|---|---|

| Eligibility for Loan Forgiveness | Cancer patients may qualify for loan forgiveness under specific programs. |

| Total and Permanent Disability (TPD) Discharge | Available for borrowers with permanent disabilities, including cancer-related disabilities. |

| Income-Driven Repayment (IDR) Forgiveness | After 20-25 years of qualifying payments, remaining balance may be forgiven. |

| Public Service Loan Forgiveness (PSLF) | Forgiveness after 10 years of qualifying payments for those in public service. |

| Cancer-Specific Forgiveness Programs | Limited; no federal programs exclusively for cancer patients. |

| Private Loan Forgiveness | Rare; some private lenders may offer hardship options but not forgiveness. |

| State-Based Assistance | Some states offer financial aid or loan repayment programs for cancer patients. |

| Documentation Required | Medical certification of disability or proof of financial hardship. |

| Tax Implications | Forgiven amounts may be taxable unless under TPD discharge. |

| Application Process | Varies by program; typically involves submitting medical and financial documentation. |

| Impact on Credit Score | Forgiveness under TPD does not negatively impact credit score. |

| Availability for Federal vs. Private Loans | Forgiveness programs primarily apply to federal student loans. |

| Recent Policy Updates | No recent federal policies specifically targeting cancer patients for loan forgiveness. |

Explore related products

What You'll Learn

- Eligibility Criteria: Specific conditions cancer patients must meet to qualify for student loan forgiveness

- Documentation Required: Medical and financial proof needed to support forgiveness applications

- Types of Forgiveness: Overview of programs like Total and Permanent Disability Discharge (TPD)

- Application Process: Steps to apply for loan forgiveness as a cancer patient

- Impact on Credit: How loan forgiveness affects credit scores and financial health

![]()

Eligibility Criteria: Specific conditions cancer patients must meet to qualify for student loan forgiveness

Cancer patients seeking student loan forgiveness must navigate a complex web of eligibility criteria, often tied to specific programs like the Total and Permanent Disability (TPD) discharge. The first condition is a formal certification of total and permanent disability, typically requiring documentation from a physician confirming the inability to engage in substantial gainful activity due to the cancer diagnosis. This certification must align with the U.S. Department of Education’s standards, which often necessitate evidence of ongoing treatment, prognosis, and functional limitations. For instance, patients with advanced-stage cancers or those undergoing aggressive therapies like stem cell transplants may meet these criteria more readily than those in remission or with early-stage diagnoses.

Beyond medical certification, applicants must demonstrate that their disability is expected to last continuously for at least 60 months or result in death. This long-term prognosis is critical, as temporary or short-term disabilities do not qualify. Cancer patients with terminal diagnoses or those whose treatment plans indicate prolonged incapacitation are more likely to meet this threshold. For example, a patient with metastatic cancer and a life expectancy of less than five years would likely qualify, whereas someone with a localized tumor and a high survival rate might not.

Another eligibility factor is the type of student loan held. Only federal student loans, including Direct Loans, Perkins Loans, and Federal Family Education Loans (FFEL), are eligible for TPD discharge. Private student loans are not covered, leaving patients with these loans to explore alternative options like hardship programs offered by individual lenders. This distinction is crucial, as private loans often lack the same forgiveness pathways as federal loans, requiring patients to negotiate directly with lenders for potential relief.

Finally, cancer patients must be aware of the application process and monitoring period. After submitting the TPD discharge application and supporting medical documentation, approved applicants enter a three-year post-approval monitoring period. During this time, they must refrain from earning above the poverty guideline threshold, taking out new federal student loans, or receiving new federal education benefits. Failure to comply can result in loan reinstatement. For instance, a patient who returns to work part-time and exceeds the income limit may lose their forgiveness status. Practical tips include maintaining thorough medical records, consulting with a financial advisor, and staying informed about program updates to ensure compliance throughout the process.

Student Loan Forgiveness for Clinical Medical Assistants: What You Need to Know

You may want to see also

Explore related products

![]()

Documentation Required: Medical and financial proof needed to support forgiveness applications

Cancer patients seeking student loan forgiveness must navigate a complex process that hinges on robust documentation. At its core, the application demands two critical pillars: medical evidence of the diagnosis and financial proof of hardship. Without these, even the most compelling cases can falter. For instance, a pathology report confirming the cancer type, stage, and treatment plan is non-negotiable. Similarly, financial statements—such as tax returns, bank statements, or pay stubs—must illustrate the inability to meet loan obligations due to medical expenses or income loss. This dual requirement underscores the need for meticulous record-keeping from the outset.

The medical documentation required goes beyond a simple doctor’s note. Applicants must provide detailed records, including biopsy results, treatment schedules, and prognoses. For example, a patient with Stage III breast cancer undergoing chemotherapy might submit oncology reports, treatment logs, and a letter from their oncologist detailing the physical and financial toll of the disease. These documents should explicitly link the diagnosis to the inability to work or manage loan payments. Incomplete or vague medical records can delay or derail the forgiveness process, making it essential to collaborate closely with healthcare providers to ensure all necessary details are included.

Financial proof is equally critical and must paint a clear picture of economic distress. This includes not only income documentation but also evidence of cancer-related expenses, such as insurance copays, medication costs, and travel to treatment centers. For instance, a patient spending $500 monthly on targeted therapy medications should provide pharmacy receipts and insurance explanations of benefits (EOBs). Additionally, if the patient has reduced their work hours or lost their job due to treatment, employment records or a letter from their employer can strengthen the case. The goal is to demonstrate that the financial burden of cancer has rendered loan repayment unmanageable.

A practical tip for applicants is to organize documents chronologically and categorize them by type (medical, financial, employment). This not only streamlines the application process but also ensures nothing is overlooked. For example, create separate folders for lab results, treatment invoices, and income statements. Additionally, keep a log of all expenses related to cancer care, no matter how small, as these cumulative costs can significantly bolster the financial hardship argument. Finally, consult with a financial advisor or student loan specialist to review the documentation before submission, as their expertise can identify gaps or areas for improvement.

In conclusion, the documentation required for student loan forgiveness as a cancer patient is both extensive and specific. Medical records must unequivocally prove the diagnosis and its impact, while financial documents must vividly illustrate the resulting hardship. By approaching this process with organization, thoroughness, and attention to detail, applicants can maximize their chances of a successful outcome. Remember, the goal is not just to inform but to persuade—every piece of paper should tell a story of resilience and need.

Veterans Guide: Applying for Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Types of Forgiveness: Overview of programs like Total and Permanent Disability Discharge (TPD)

Cancer patients facing the burden of student loans may find relief through specific forgiveness programs, particularly the Total and Permanent Disability Discharge (TPD). This federal initiative offers a lifeline by canceling federal student loans for individuals who can no longer work due to a permanent disability. To qualify, applicants must provide documentation proving their disability, which can include a physician’s certification, Social Security Administration notice, or Veterans Affairs determination. For cancer patients, this often means submitting medical evidence that their condition prevents substantial gainful activity, a key criterion for TPD approval.

The application process for TPD discharge is straightforward but requires attention to detail. Borrowers must complete an application through the U.S. Department of Education’s TPD Servicer, Nelnet. Once approved, loans are discharged, and borrowers are no longer obligated to make payments. However, a critical aspect to note is the three-year monitoring period. During this time, borrowers must not earn above the poverty line, take out new federal loans, or have their loans reinstated. For cancer patients, this period can be challenging, as financial stability and medical expenses often intertwine, making it essential to plan carefully.

Comparing TPD to other forgiveness programs highlights its unique benefits for cancer patients. Unlike Public Service Loan Forgiveness (PSLF), which requires 120 qualifying payments and employment in a specific sector, TPD offers immediate relief without such prerequisites. Similarly, income-driven repayment plans may reduce monthly payments but do not eliminate the debt entirely. TPD stands out as a comprehensive solution for those whose health conditions permanently alter their ability to work. However, it’s important to recognize that private student loans are not eligible for TPD discharge, leaving borrowers with limited options for those debts.

Practical tips for cancer patients pursuing TPD include gathering all necessary medical documentation in advance and consulting with a healthcare provider to ensure the application accurately reflects their condition. Additionally, borrowers should monitor their income during the post-discharge monitoring period to avoid reinstatement of loans. For those with private loans, exploring lender-specific hardship programs or refinancing options may provide partial relief. Ultimately, TPD discharge serves as a vital resource, offering financial freedom to cancer patients during a time when focus should be on health, not debt.

Can Student Loan Be Forgiven? Exploring Debt Relief Options for Borrowers

You may want to see also

Explore related products

![]()

Application Process: Steps to apply for loan forgiveness as a cancer patient

Cancer patients seeking student loan forgiveness face a complex but navigable process. The first critical step is understanding eligibility. While there’s no direct "cancer patient forgiveness" program, options like Total and Permanent Disability (TPD) discharge apply if cancer renders you unable to work. Gather medical evidence—a physician’s certification of your condition’s severity and permanence is mandatory. This isn’t a quick fix; it requires proof beyond a diagnosis, such as treatment records or prognosis statements.

Next, identify the correct application pathway. For federal loans, submit a TPD discharge application via the U.S. Department of Education’s website. Private loans vary; some lenders offer hardship discharges, but terms are less standardized. Contact your lender directly to inquire about their policies and request a waiver application. Be prepared to negotiate or provide extensive documentation, as private forgiveness is rarer and more discretionary.

Timing matters. Apply for TPD discharge only after stabilizing your treatment plan, as approval halts collections but requires periodic reviews for three years. Premature application risks denial if your condition improves. Conversely, private loan holders may require immediate proof of hardship, so act swiftly if your finances are already strained.

Finally, leverage support systems. Nonprofits like the Cancer Financial Assistance Coalition offer guidance, while loan servicers can clarify application nuances. Keep meticulous records of all submissions and correspondence. While the process demands persistence, successful discharge can alleviate financial burdens, allowing focus on recovery rather than debt.

Virginia's Tax Treatment of Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Impact on Credit: How loan forgiveness affects credit scores and financial health

Loan forgiveness programs, including those potentially available to cancer patients, can significantly impact credit scores and overall financial health. While the immediate relief of reduced debt is a clear benefit, the effects on credit are nuanced. For instance, some forgiveness programs report the forgiven amount as "paid as agreed," which can maintain or even improve a credit score. However, others may mark the account as "settled," which could have a neutral or slightly negative impact, depending on the credit bureau’s interpretation. Understanding these distinctions is crucial for cancer patients navigating financial recovery while managing student loans.

One practical step for cancer patients considering loan forgiveness is to review the specific terms of the program. For example, Public Service Loan Forgiveness (PSLF) or income-driven repayment plans often have clear guidelines on how forgiveness is reported to credit bureaus. Proactively requesting a detailed credit report before and after forgiveness can help identify any discrepancies or unexpected changes. Additionally, maintaining open lines of communication with loan servicers can ensure accurate reporting and minimize adverse effects on credit.

A comparative analysis reveals that loan forgiveness generally has a milder impact on credit than defaults or delinquencies. For cancer patients, who may face income disruptions or medical expenses, avoiding negative marks like late payments is critical. Forgiveness programs can act as a financial safeguard, preventing long-term credit damage. However, it’s essential to weigh the trade-offs, such as potential tax implications from forgiven amounts, which could indirectly affect financial stability if not planned for.

To maximize financial health, cancer patients should pair loan forgiveness with proactive credit management strategies. This includes paying down other debts, keeping credit utilization low, and avoiding new credit inquiries during the forgiveness process. For instance, reducing credit card balances to below 30% of the limit can positively influence credit scores. Additionally, setting up automatic payments for remaining debts ensures consistency, further bolstering creditworthiness.

In conclusion, while loan forgiveness can offer cancer patients much-needed financial relief, its impact on credit scores requires careful navigation. By understanding program specifics, monitoring credit reports, and adopting complementary financial strategies, individuals can mitigate potential drawbacks and strengthen their overall financial health. This approach not only addresses immediate concerns but also lays the groundwork for long-term financial resilience.

Has My Student Loan Been Forgiven? Understanding Loan Forgiveness Updates

You may want to see also

Frequently asked questions

There is no specific federal student loan forgiveness program exclusively for cancer patients. However, cancer patients may qualify for loan forgiveness through existing programs like Public Service Loan Forgiveness (PSLF), Total and Permanent Disability (TPD) discharge, or income-driven repayment plans.

Cancer patients who are deemed totally and permanently disabled may qualify for TPD discharge, which forgives federal student loans. Applicants must provide medical documentation from a physician or receive a disability determination from the Social Security Administration (SSA).

Yes, cancer patients can qualify for PSLF if they work full-time for a qualifying employer (e.g., government or nonprofit) and make 120 eligible payments. Cancer itself does not automatically qualify, but working in public service while managing the disease can make this program accessible.

Some states or private organizations may offer limited loan forgiveness or assistance programs for cancer patients, but these are rare and vary by location. It’s best to research state-specific programs or contact cancer support organizations for potential resources.

![The Cancer-Fighting Kitchen, Second Edition: Nourishing, Big-Flavor Recipes for Cancer Treatment and Recovery [A Cookbook]](https://m.media-amazon.com/images/I/91WnPaVAsCL._AC_UL320_.jpg)