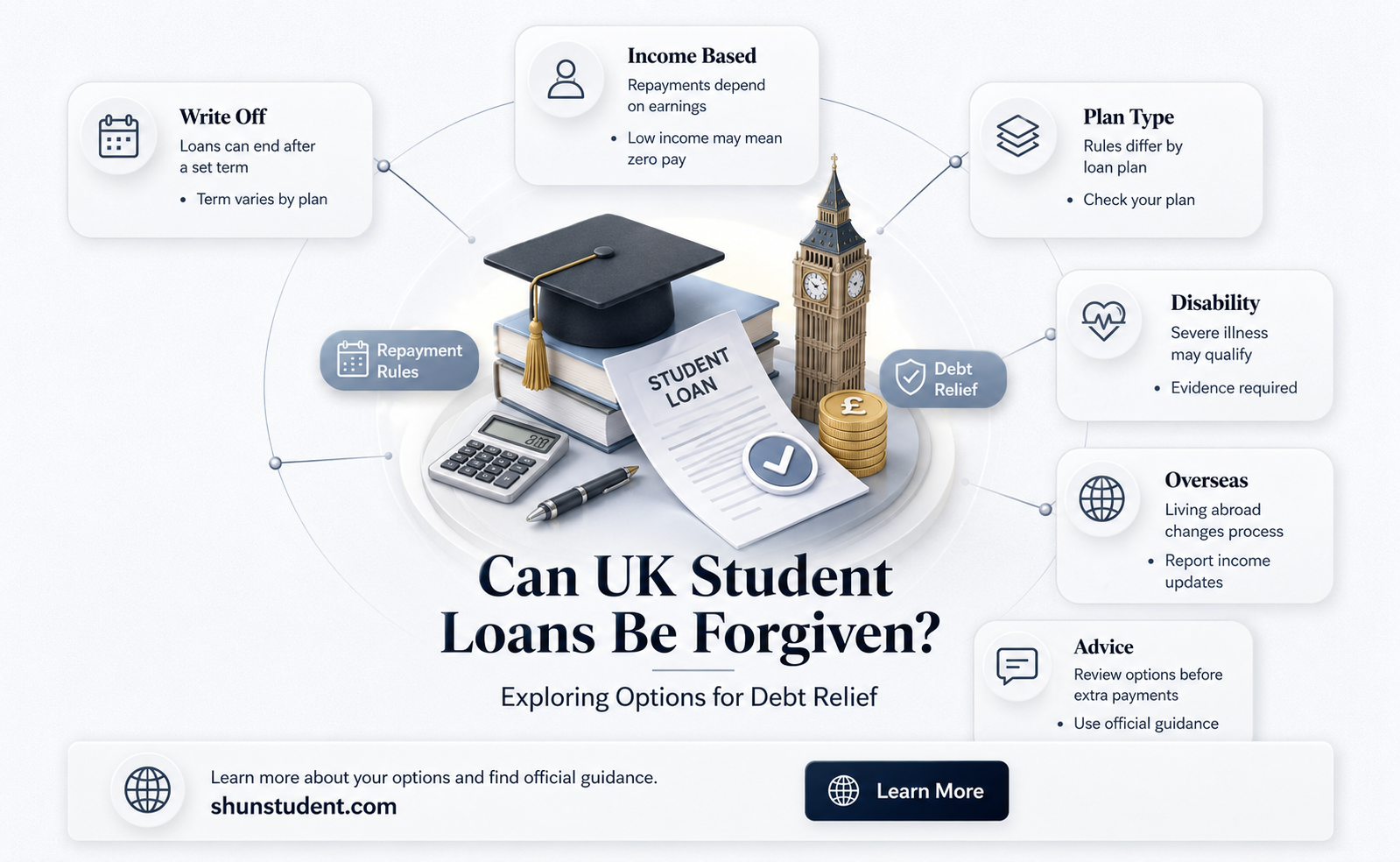

In the United Kingdom, student loan forgiveness is a topic of significant interest for many graduates burdened by debt. While the UK system differs from others, such as the US, it does offer certain mechanisms for loan forgiveness under specific circumstances. Generally, student loans in the UK are income-contingent, meaning repayments are tied to earnings, and any outstanding balance is written off after a set period, typically 30 years in England and Wales, and 35 years in Scotland. Additionally, loans may be forgiven in cases of permanent disability or death. However, there are no widespread programs for loan forgiveness based on profession or public service, unlike in some other countries. Understanding these nuances is crucial for borrowers seeking clarity on their financial obligations and potential pathways to debt relief.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Student loans in the UK are not typically "forgiven" in the traditional sense. Instead, they are written off after a certain period, depending on the repayment plan. |

| Repayment Plan Types | - Plan 1: Loans taken out before 2012 (England and Wales). Written off after 25 years. - Plan 2: Loans taken out after 2012 (England and Wales). Written off after 30 years. - Plan 4: Loans for Scottish students. Written off after 30 years. - Plan 5: Loans for Northern Irish students. Written off after 25 years. |

| Repayment Threshold | Repayments begin once income exceeds a threshold: - Plan 1: £20,195 per year (from April 2023). - Plan 2: £27,295 per year (from April 2023). - Plan 4: £25,000 per year (from April 2023). - Plan 5: £20,195 per year (from April 2023). |

| Interest Rates | Interest accrues based on income and inflation rates, but unpaid balances are written off after the specified period, regardless of the amount repaid. |

| Disability Discharge | Loans may be written off if the borrower becomes permanently unfit for work due to a disability. |

| Death of Borrower | Outstanding student loan balance is written off upon the borrower's death. |

| Overseas Repayments | Borrowers living abroad must continue repayments based on their income, but the loan is still written off after the same period as in the UK. |

| Early Repayment | Borrowers can repay the loan early, but there is no financial benefit to doing so, as the loan will be written off after the specified period anyway. |

| Impact on Credit Score | Student loans do not appear on credit reports in the UK and do not affect credit scores. |

| Tax Deduction | Repayments are deducted directly from income through the tax system (Pay As You Earn - PAYE) or self-assessment. |

| Loan Transferability | Student loans cannot be transferred to another person. |

| Updates to Terms | Terms and conditions of student loans can change based on government policy updates. |

Explore related products

What You'll Learn

![]()

Eligibility criteria for student loan forgiveness in the UK

In the UK, student loan forgiveness isn’t a universal program but rather a set of specific circumstances where repayment obligations are waived. The primary pathway to forgiveness is through the income-contingent repayment system, which automatically cancels any remaining debt after 30 years (25 years for pre-2006 loans) from the April after graduation. This isn’t an application-based forgiveness but a built-in feature of the loan structure, designed to protect borrowers from indefinite debt. For example, if a borrower’s income never reaches the repayment threshold (£22,012 annually for Plan 2 loans as of 2023), they may never repay the full amount, and the remainder is written off after the term.

Another eligibility criterion for loan forgiveness is total permanent disability. Borrowers who are deemed permanently unfit for work due to physical or mental health conditions can apply for cancellation through the Total and Permanent Disability Discharge (TPDD) scheme. This requires medical evidence and approval from the Department for Work and Pensions. For instance, a borrower diagnosed with a severe chronic illness that prevents employment could have their entire loan balance forgiven, regardless of how much they’ve repaid. This provision ensures that individuals facing long-term health challenges aren’t burdened by student debt.

For those in specific professions, additional forgiveness programs exist. Teachers, for example, may qualify for partial loan cancellation through the Teachers Student Loan Reimbursement scheme if they work in low-income schools or shortage subjects like math or science. Similarly, NHS professionals, including nurses, midwives, and healthcare workers, can access the NHS Learning Support Fund, which offers grants and loan forgiveness for tuition fees after several years of service. These targeted programs incentivize careers in high-demand sectors while alleviating financial strain.

It’s crucial to note that bankruptcy does not automatically discharge student loans in the UK, unlike in some other countries. However, if a borrower declares bankruptcy and can demonstrate that repaying the loan would cause undue hardship, the court may discharge the debt. This is rare and requires extensive evidence of financial incapacity. Additionally, borrowers who move abroad and cease to be UK residents may still be subject to repayment obligations, depending on their income and the terms of their loan plan. Understanding these nuances is essential for anyone seeking clarity on eligibility for student loan forgiveness.

Parent PLUS Loans and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Income-based repayment plans and loan cancellation

In the UK, income-based repayment plans are a cornerstone of the student loan system, designed to ensure that graduates repay their loans in a way that aligns with their financial circumstances. Under the current Plan 2 (for English and Welsh students who started university after 2012) and Plan 4 (for Scottish and Northern Irish students), repayments are calculated as 9% of any income above a threshold. As of April 2023, this threshold is £27,295 per year, £2,274 per month, or £524 per week. If your income falls below this threshold, you pay nothing, and the loan is effectively paused until your earnings rise. This system inherently provides a safety net, ensuring that repayment remains manageable regardless of your career trajectory.

One of the most significant features of income-based repayment plans is the automatic loan cancellation mechanism. For Plan 2 and Plan 4 loans, any outstanding balance is written off after 30 years from the April following graduation. This means that if you’ve been making repayments for three decades and still have a remaining balance, it’s forgiven. For example, if you graduate at 22 and earn just above the threshold for the next 30 years, you’ll likely repay only a fraction of the loan, with the rest cancelled. This contrasts with Plan 1 loans (for those who started university before 2012), where the cancellation period is 25 years, but the repayment threshold is lower at £20,195 annually.

While the 30-year cancellation rule provides long-term relief, it’s crucial to understand its implications. For high earners, the loan may be fully repaid before the cancellation period ends, but for those with fluctuating or modest incomes, it acts as a financial safeguard. However, interest accrues on the loan, which can increase the total amount owed. For Plan 2 loans, the interest rate is tied to the Retail Price Index (RPI) plus up to 3%, depending on income. This means that even if your loan is eventually cancelled, the interest could significantly inflate the balance over time.

To maximise the benefits of income-based repayment plans, consider practical strategies. First, ensure your employer is deducting repayments correctly through PAYE, as errors can lead to over or underpayment. Second, if you’re self-employed, report your income accurately to HMRC to avoid miscalculations. Third, keep track of your loan balance and repayments via the Student Loans Company (SLC) portal. Finally, if you’re nearing the 30-year mark, avoid making voluntary overpayments unless you’re certain the loan will be fully repaid before cancellation—otherwise, you might be paying more than necessary.

In summary, income-based repayment plans in the UK offer a flexible and forgiving approach to student loan repayment, with automatic cancellation after 30 years providing a long-term safety net. While the system is designed to be fair, understanding its nuances—such as interest accrual and repayment thresholds—can help borrowers navigate it more effectively. By staying informed and proactive, you can ensure that your student loan remains a manageable part of your financial journey.

Does Reserve Service Qualify for Student Loan Forgiveness? Key Insights

You may want to see also

Explore related products

![]()

Disability-related student loan discharge options

In the UK, students with disabilities face unique financial challenges, and the government has established specific provisions to alleviate the burden of student loan debt for this demographic. The Disability-Related Student Loan Discharge is a lesser-known but crucial option that can provide significant relief. This discharge is available to individuals who have a permanent disability that prevents them from working, thereby affecting their ability to repay their student loans. The process is designed to be supportive, but it requires thorough documentation and adherence to specific criteria.

To qualify for disability-related student loan discharge, applicants must provide evidence of their disability from a qualified professional, such as a doctor or specialist. This evidence must demonstrate that the disability is long-term or permanent and severely impacts the individual’s ability to engage in substantial gainful activity. The Student Loans Company (SLC) assesses each case individually, ensuring that the decision is fair and based on robust medical evidence. It’s essential to gather all necessary documentation, including medical reports and statements from healthcare providers, to streamline the application process.

One practical tip for applicants is to consult with a disability advisor or support worker who can guide them through the application process. These professionals can help ensure that all required documentation is complete and accurately reflects the applicant’s situation. Additionally, applicants should be aware that the discharge applies to both tuition fee loans and maintenance loans, offering comprehensive relief from student debt. However, it’s important to note that the discharge does not cover any additional debts, such as those owed to private lenders or credit card companies.

Comparatively, the UK’s approach to disability-related student loan discharge is more inclusive than some other countries, where similar provisions may come with stricter eligibility criteria or limited coverage. For instance, while the U.S. offers Total and Permanent Disability (TPD) discharge, it requires a more complex application process and periodic reviews. In contrast, the UK system focuses on permanent disabilities without the need for recurring assessments, providing long-term peace of mind for eligible individuals.

In conclusion, disability-related student loan discharge is a vital lifeline for UK students with permanent disabilities. By understanding the eligibility criteria, gathering the necessary documentation, and seeking professional guidance, applicants can navigate the process effectively. This option not only eases financial stress but also acknowledges the unique challenges faced by individuals with disabilities, fostering a more inclusive approach to student debt relief.

Devry Student Loan Forgiveness: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

Loan forgiveness for public sector workers

Public sector workers in the UK, particularly those in roles like nursing, teaching, and social work, often face significant financial pressures, including student loan repayments. Recognising their contributions, the UK government has introduced specific loan forgiveness schemes to alleviate this burden. For instance, the NHS Learning Support Fund offers grants and bursaries to nursing, midwifery, and allied health students, with the potential for partial loan forgiveness after qualifying and working in the NHS. Similarly, teachers in shortage subjects or areas can benefit from the Teachers’ Student Loan Reimbursement Scheme, which reimburses up to £2,000 annually for up to ten years. These targeted initiatives aim to retain talent in critical public services while easing financial strain.

While these schemes are a step in the right direction, they are not without limitations. Eligibility criteria can be stringent, often requiring workers to commit to specific roles or regions for extended periods. For example, teachers must work in designated schools in England or Wales, and nurses must remain in the NHS to qualify for loan forgiveness. Additionally, the reimbursement amounts may not fully offset the total student debt, leaving recipients still responsible for a substantial portion. Prospective applicants should carefully review the terms and conditions, ensuring their career plans align with the scheme’s requirements to maximise benefits.

A comparative analysis reveals that loan forgiveness for public sector workers in the UK is more structured than in some other countries, such as the US, where programs like Public Service Loan Forgiveness (PSLF) offer broader eligibility but come with complex application processes. In the UK, schemes are sector-specific, making them easier to navigate but less accessible to those outside designated professions. For instance, social workers, though vital, currently lack a dedicated loan forgiveness program, highlighting gaps in the system. Policymakers could consider expanding eligibility to include more public sector roles, ensuring a fairer distribution of financial relief.

For public sector workers considering these schemes, practical steps include researching eligibility criteria early in their careers, maintaining accurate records of employment and repayments, and staying informed about policy updates. For example, nurses should apply for the NHS Learning Support Fund during their studies, while teachers should confirm their school’s eligibility for the reimbursement scheme before accepting a position. Additionally, combining loan forgiveness with other financial strategies, such as income-based repayment plans, can further reduce financial pressure. By proactively engaging with these programs, workers can make meaningful progress toward managing their student debt.

In conclusion, loan forgiveness for public sector workers in the UK serves as a vital tool for supporting those in essential roles while addressing the broader issue of student debt. While existing schemes offer tangible benefits, their narrow focus and limited scope leave room for improvement. By expanding eligibility and simplifying processes, the government could enhance the impact of these programs, ensuring more workers reap the rewards of their dedication to public service. For now, those eligible should take full advantage of available opportunities, carefully planning their careers to align with the schemes’ requirements.

FedLoan Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Time-based loan write-off after 25-30 years

In the UK, student loans aren't forgiven in the traditional sense, but they do come with a unique feature: time-based write-off. This means that after 25 to 30 years, depending on the loan plan, any remaining balance is automatically wiped clean. For instance, under Plan 2 (the most common plan for English and Welsh students who started university after 2012), the loan is written off 30 years after the April following graduation. This system is designed to alleviate long-term financial pressure, particularly for borrowers who may never earn enough to repay the loan in full.

Consider the mechanics of this write-off. Repayments are income-contingent, meaning borrowers only repay 9% of their earnings above a certain threshold (£27,295 annually for Plan 2 as of 2023). If, after 30 years, the loan hasn’t been fully repaid, the residual amount is forgiven. This structure contrasts with systems in other countries, like the US, where student debt often persists indefinitely. For UK borrowers, it provides a safety net, ensuring that student debt doesn’t become a lifelong burden. However, it’s crucial to note that the write-off period starts from the first April after graduation, not from the last repayment, so even if repayments begin later, the clock is already ticking.

A common misconception is that this write-off makes student loans "free money." In reality, the system is funded through a combination of repayments and government subsidies. Borrowers with higher incomes will repay a significant portion of their loan before the write-off period ends, while those with lower incomes may repay very little. For example, someone earning £35,000 annually would repay approximately £61.50 per month under Plan 2, but if their income remains relatively low over 30 years, much of the loan could still be written off. This highlights the progressive nature of the system, where the burden is shared based on earning potential.

Practical tips for navigating this system include understanding your loan plan and repayment threshold. For instance, Plan 1 (for pre-2012 borrowers) has a 25-year write-off period and a lower repayment threshold (£20,195 as of 2023). Keep track of your earnings and repayments through the HMRC portal to ensure accuracy. If you’re self-employed or have multiple income sources, repayments can become more complex, so consider seeking advice from a financial advisor. Finally, while the write-off is automatic, it’s wise to monitor your loan balance periodically to avoid surprises.

In conclusion, the time-based loan write-off after 25-30 years is a cornerstone of the UK’s student loan system, offering a balanced approach to higher education financing. It ensures that borrowers are not indefinitely shackled by debt while maintaining a contribution mechanism tied to earning potential. By understanding the specifics of this system, borrowers can make informed decisions and plan their financial futures with greater confidence.

Is New Jersey Taxing Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Frequently asked questions

Yes, student loans in the UK can be forgiven under certain conditions, such as after a specific period (typically 30 years for Plan 2 loans in England and Wales, and 25 years for Plan 1 loans) if the loan has not been fully repaid.

Yes, student loans can be written off early if the borrower becomes permanently unable to work due to disability or dies. Additionally, loans may be forgiven if the borrower moves abroad and reaches the repayment threshold age.

No, the UK does not offer loan forgiveness based on specific professions. However, some employers (e.g., NHS) may offer repayment assistance as part of their benefits package, but this is not direct loan forgiveness.

Student loans are not typically written off in bankruptcy in the UK. They remain separate from other debts and continue to be repayable based on income, even after bankruptcy is discharged.

Moving abroad does not automatically forgive your student loan. Repayments are still required if you earn above the repayment threshold in your new country of residence. However, loans may be written off after a certain period (e.g., 30 years for Plan 2 loans) regardless of location.