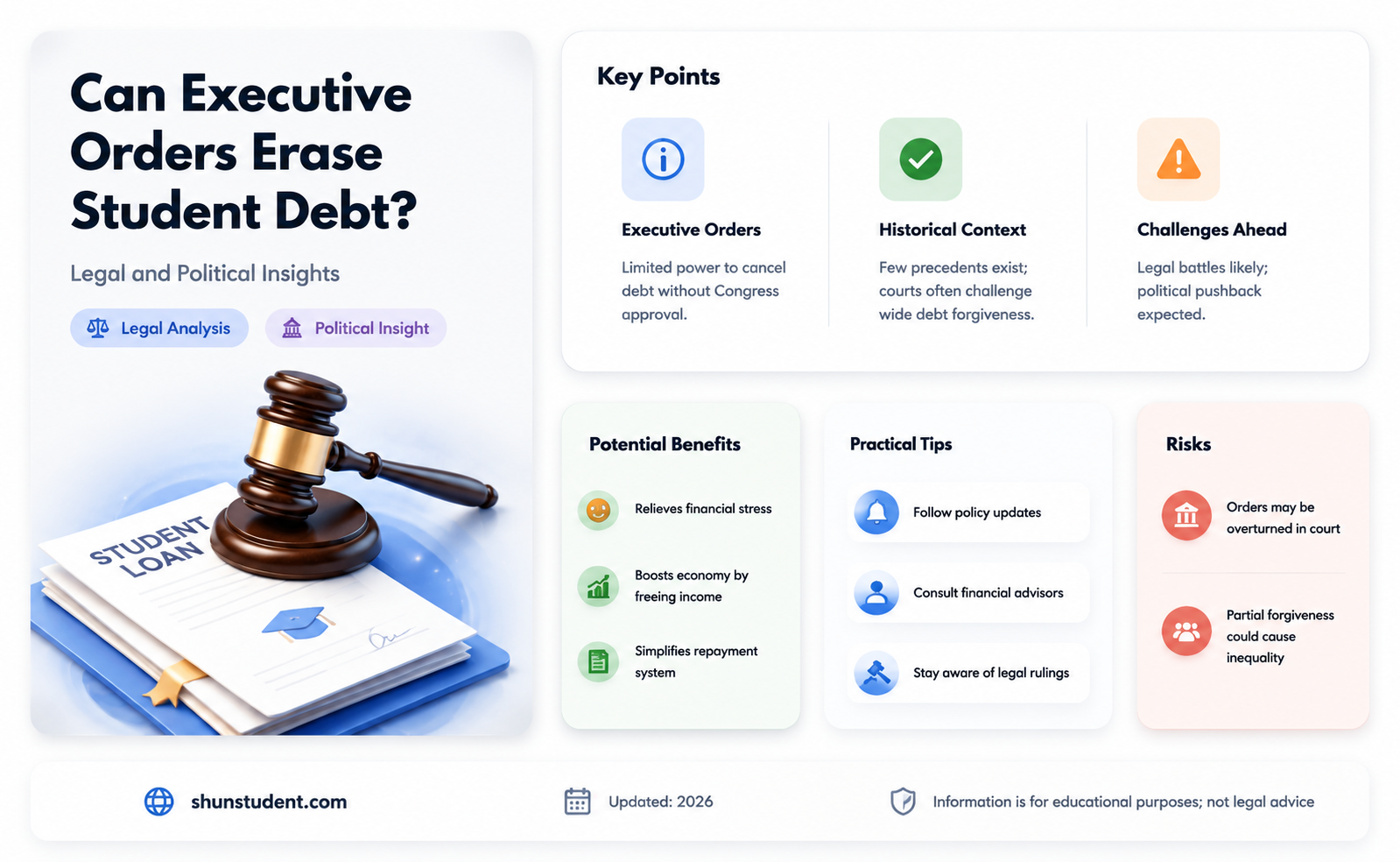

The question of whether an executive order can forgive student loans has become a central issue in the ongoing debate over higher education affordability and economic relief in the United States. As millions of Americans grapple with mounting student debt, policymakers and advocates have explored various avenues to address this crisis, including the potential use of executive authority. Proponents argue that an executive order could provide immediate relief to borrowers, bypassing the often gridlocked legislative process, while critics raise concerns about the legality, scope, and long-term implications of such an action. This contentious topic intersects with constitutional law, economic policy, and political strategy, making it a complex and highly debated issue in both legal and public spheres.

| Characteristics | Values |

|---|---|

| Legal Authority | The Higher Education Act of 1965 grants the Secretary of Education authority to modify, compromise, waive, or release student loans. However, the extent of this authority is debated, especially for broad-scale forgiveness. |

| Executive Action Precedent | Previous executive orders have provided limited student loan relief, such as pauses on payments and interest accrual during the COVID-19 pandemic, but no large-scale forgiveness has been implemented solely through executive order. |

| Legal Challenges | Broad student loan forgiveness via executive order faces potential legal challenges, as seen in lawsuits against the Biden administration's 2022 forgiveness plan, which was blocked by the Supreme Court. |

| Congressional Role | Congress holds primary authority over student loan policy, and significant forgiveness would likely require legislative action for long-term legitimacy. |

| Political Debate | The issue is highly polarized, with arguments for relief citing economic benefits and moral obligations, while opponents raise concerns about fairness, cost, and legal overreach. |

| Current Status (as of 2023) | No executive order has successfully forgiven student loans on a large scale. Efforts have focused on targeted relief (e.g., Public Service Loan Forgiveness reforms) and administrative fixes. |

| Public Opinion | Polls show divided support, with a majority favoring some form of relief but disagreement on the scope and method of forgiveness. |

| Economic Impact | Large-scale forgiveness could stimulate the economy by increasing disposable income but would also add to the national debt, sparking debate over long-term consequences. |

Explore related products

What You'll Learn

![]()

Legal Authority of Executive Orders

Executive orders derive their authority from Article II of the U.S. Constitution, which vests the President with the power to manage the executive branch. However, this power is not unlimited. The President can issue directives only within the scope of existing laws or constitutional authority. For student loan forgiveness, the question hinges on whether the Higher Education Act of 1965 grants the Secretary of Education—acting under presidential direction—the authority to cancel debt broadly. Section 432(a) of the Act allows the Secretary to "enforce, pay, compromise, waive, or release any right, title, claim, lien, or demand" related to federal student loans, but legal scholars debate whether this provision permits mass forgiveness without congressional action.

Consider the 2022 Biden administration’s attempt to forgive up to $20,000 in student debt per borrower, which cited the HEROES Act of 2003 as justification. This act authorizes the Secretary of Education to waive regulations related to student financial assistance programs during national emergencies. The Supreme Court, in *Biden v. Nebraska* (2023), struck down the plan, ruling that the HEROES Act did not provide clear congressional authorization for such sweeping action. This case underscores the principle that executive orders cannot unilaterally create new law or override existing statutory limits, even during crises.

To assess whether an executive order can forgive student loans, examine the interplay between constitutional powers and statutory constraints. The President’s authority to issue orders is rooted in the Constitution’s executive power clause, but it must align with congressional intent as expressed in legislation. For instance, while the President can direct agencies to implement policies, those policies must fall within the boundaries set by Congress. In the context of student loans, this means any forgiveness initiative must find explicit or implicit authorization in laws like the Higher Education Act or related statutes.

A comparative analysis of past executive actions reveals a pattern: successful orders operate within clear statutory frameworks. For example, President Obama’s use of executive orders to expand the Deferred Action for Childhood Arrivals (DACA) program relied on the Attorney General’s prosecutorial discretion, a well-established legal principle. In contrast, the student loan forgiveness plan lacked a similarly clear statutory basis, leading to its legal demise. This highlights the critical distinction between administrative discretion and legislative authority.

In practice, crafting an executive order for student loan forgiveness requires meticulous legal grounding. Start by identifying specific statutory provisions that could support such action, such as the Higher Education Act’s waiver authority. Next, ensure the order aligns with judicial interpretations of those provisions, as demonstrated in cases like *Biden v. Nebraska*. Finally, anticipate legal challenges by framing the action as a narrow exercise of administrative discretion rather than a broad policy change. While executive orders offer a powerful tool for presidential action, their effectiveness in forgiving student loans ultimately depends on staying within the confines of existing law.

Can Nelnet Student Loans Be Forgiven? Exploring Options for Relief

You may want to see also

Explore related products

![]()

Impact on Federal Budget

Executive action to forgive student loans would immediately reduce federal assets by canceling debt owed to the government, creating a one-time deficit increase. The Congressional Budget Office estimates that forgiving $10,000 per borrower would cost approximately $377 billion, while $50,000 in forgiveness could exceed $1.4 trillion. These figures reflect the direct loss of receivables from the Department of Education’s balance sheet, not accounting for potential economic multipliers or behavioral changes among borrowers. Such a move would require careful reconciliation within the federal budget, potentially necessitating cuts in other areas or increased borrowing to maintain fiscal stability.

From a cash flow perspective, loan forgiveness would reduce annual inflows to the Treasury, as borrowers cease making payments. For context, the federal government collected roughly $80 billion in student loan payments in 2019. While this reduction would free up disposable income for borrowers, it would also diminish a steady revenue stream for the government. Policymakers would need to weigh this trade-off against the potential stimulus effect of increased consumer spending, which could generate tax revenue through economic activity. However, the timing and magnitude of such benefits remain uncertain, making short-term budget adjustments critical.

Critics argue that large-scale loan forgiveness could exacerbate inflationary pressures by injecting liquidity into the economy without addressing underlying productivity. If borrowers redirect freed-up funds toward consumption rather than savings or investment, demand could outpace supply in key sectors, driving prices higher. Proponents counter that targeted forgiveness, such as for low-income borrowers, could mitigate this risk by focusing relief on those most likely to spend the funds immediately. Regardless, the Federal Reserve might need to adjust monetary policy in response, complicating efforts to manage inflation and interest rates.

Long-term budgetary implications depend on whether forgiveness is paired with reforms to the student loan system. Without changes to college funding models or loan terms, future borrowing could continue to rise, leading to a cycle of debt accumulation and forgiveness. Incorporating reforms, such as income-driven repayment caps or increased institutional accountability, could reduce the likelihood of recurring crises. However, such measures would require legislative action, highlighting the limitations of executive orders in addressing systemic issues. Balancing immediate relief with sustainable policy changes remains a central challenge for any forgiveness initiative.

Navient Student Loan Forgiveness: Strategies to Erase Your Debt

You may want to see also

Explore related products

![]()

Congressional Role in Loan Forgiveness

The power to forgive student loans is not solely within the executive branch's purview. While executive orders can provide temporary relief or modify existing loan programs, Congress holds the constitutional authority to appropriate funds and enact legislation that directly addresses loan forgiveness. This distinction is critical, as it shapes the scope, permanence, and legality of any forgiveness initiatives. For instance, the Higher Education Act of 1965, which Congress passed, established the framework for federal student loans and subsequent forgiveness programs like Public Service Loan Forgiveness (PSLF). Without congressional action, executive orders risk legal challenges and lack the funding mechanisms to implement large-scale forgiveness.

Consider the practical steps Congress must take to enable loan forgiveness. First, legislation must explicitly authorize the Department of Education to discharge loans, specifying eligibility criteria, such as income thresholds or public service requirements. Second, Congress must appropriate funds to cover the forgiven amounts, as the federal government is legally obligated to repay lenders for discharged loans. For example, the American Rescue Plan Act of 2021 included a provision making student loan forgiveness tax-free through 2025, a critical step to ensure borrowers are not burdened with unexpected tax liabilities. Without these legislative actions, executive orders remain limited in their ability to provide meaningful, long-term relief.

A comparative analysis highlights the limitations of executive action versus congressional legislation. Executive orders, like those issued under the HEROES Act, can pause loan payments or interest accrual during emergencies, but they cannot unilaterally cancel debt without clear statutory authority. In contrast, Congress can pass comprehensive bills, such as the proposed Student Debt Cancellation Act, which directly targets loan forgiveness. While executive actions offer quick, temporary fixes, congressional legislation ensures permanence, accountability, and broader public support. This duality underscores why advocates for widespread loan forgiveness must focus on legislative solutions rather than relying solely on executive power.

Persuasively, Congress’s role in loan forgiveness is not just procedural but deeply tied to democratic principles. By requiring legislative action, the process ensures public debate, stakeholder input, and checks on executive overreach. This transparency builds trust and legitimacy, which are essential for policies affecting millions of borrowers. For instance, congressional hearings on student debt have brought to light systemic issues in loan servicing and repayment plans, informing more targeted reforms. While slower than executive orders, this deliberative approach fosters sustainable solutions that address the root causes of the student debt crisis.

Finally, a descriptive overview of recent congressional efforts illustrates its pivotal role. In 2022, the House passed the Student Loan Forgiveness for Frontline Heroes Act, targeting forgiveness for essential workers during the pandemic. Similarly, the Fresh Start Through Repayment Act aimed to simplify repayment plans and reduce defaults. These bills, though not yet law, demonstrate Congress’s capacity to craft tailored solutions. Borrowers and advocates must therefore engage with their representatives, pushing for legislation that aligns with their needs. Without congressional action, executive orders remain a temporary bandage on a systemic wound.

Adjunct Professors and Student Loan Forgiveness: Eligibility Explained

You may want to see also

Explore related products

$14.95 $14.95

![]()

Potential Legal Challenges

The authority to forgive student loans via executive order hinges on a delicate interpretation of the Higher Education Act, specifically the Secretary of Education’s powers under Section 432(a) and 455(h). While these provisions grant flexibility in loan administration, they were designed for adjustments like deferments or income-driven repayment plans, not wholesale forgiveness. Stretching this authority to erase trillions in debt invites scrutiny: does "modify" encompass cancellation, or does it violate the non-delegation doctrine by exceeding congressional intent? Courts may demand a clear, unambiguous grant of power for such a transformative action, setting a high bar for executive justification.

A second vulnerability lies in the separation of powers. The Constitution assigns spending authority to Congress, yet mass loan forgiveness effectively reallocates taxpayer funds without legislative approval. Opponents could argue this usurps Congress’s role, particularly if the action resembles taxation or appropriation. Historical precedent offers caution: in *Clinton v. City of New York* (1998), the Supreme Court struck down a presidential line-item veto as an unconstitutional encroachment on legislative power. Student loan forgiveness, if framed as executive spending, risks a similar fate by sidestepping the budgetary process.

Standing to sue presents a procedural hurdle, but not an insurmountable one. Taxpayer standing is typically limited, yet challengers could include states (claiming harm to their tax bases) or private lenders (alleging financial injury). Alternatively, plaintiffs might argue competitive standing if forgiveness disproportionately benefits certain demographics. For instance, a state with a high concentration of non-borrowers could claim unequal treatment under the Equal Protection Clause. While standing is often a threshold issue, creative litigation strategies could clear this initial barrier, opening the door to substantive challenges.

Finally, the Administrative Procedure Act (APA) requires agencies to follow notice-and-comment rulemaking for significant actions. If forgiveness is implemented through regulatory change, skipping this process could render it "arbitrary and capricious." Courts have invalidated rushed or inadequately justified rules, as seen in *Department of Homeland Security v. Regents of the University of California* (2020). A hasty executive order, lacking public input or detailed cost-benefit analysis, would likely face APA challenges, forcing the administration to defend both the substance and process of its decision.

In sum, while an executive order to forgive student loans may appear expedient, its legality rests on precarious ground. From statutory interpretation to constitutional boundaries, each layer of challenge demands rigorous justification. Policymakers must weigh not only the policy’s merits but also its resilience in court—a miscalculation could leave borrowers in limbo and set a dangerous precedent for executive overreach.

Hospital Student Loan Forgiveness: Unlocking Debt Relief for Healthcare Professionals

You may want to see also

Explore related products

![]()

Economic Effects of Loan Forgiveness

Student loan forgiveness, particularly through executive action, has sparked intense debate over its economic implications. Proponents argue that canceling debt would stimulate consumer spending, as borrowers freed from monthly payments could redirect funds toward goods and services. A 2021 Moody’s Analytics report estimated that forgiving $10,000 per borrower could boost GDP by $86 billion to $108 billion over a decade. However, critics counter that such a policy could inflate demand without addressing supply constraints, potentially exacerbating inflation. This tension highlights the delicate balance between short-term stimulus and long-term economic stability.

Consider the distributional effects of loan forgiveness. While it would benefit millions of borrowers, the policy disproportionately favors higher-income individuals, who hold a larger share of student debt due to advanced degrees. For instance, the top 25% of earners owe nearly half of all student debt, according to the Brookings Institution. This raises questions about equity: Is forgiving loans a progressive policy if it primarily aids those already on stable financial footing? Targeted relief, such as income-driven repayment plans or forgiveness for low-income borrowers, could mitigate this imbalance and ensure resources reach those most in need.

Another critical aspect is the potential impact on federal finances. Forgiving $1 trillion in student loans, as some proposals suggest, would increase the national debt, which already exceeds $34 trillion. While proponents argue that the economic benefits outweigh the costs, skeptics warn of crowding out other government spending priorities, such as infrastructure or healthcare. Moreover, the moral hazard of debt forgiveness could incentivize future borrowing, assuming bailouts are guaranteed. Policymakers must weigh these trade-offs to avoid unintended consequences.

Finally, the labor market could experience both positive and negative effects. On one hand, reduced debt burdens might encourage entrepreneurship and career changes, as individuals feel less tied to high-paying jobs solely for loan repayment. On the other hand, if forgiveness leads to higher taxes or inflation, it could dampen job creation and wage growth. A nuanced approach, such as capping forgiveness amounts or linking it to public service, could maximize benefits while minimizing risks. Ultimately, the economic effects of loan forgiveness depend on its design and implementation, not just its existence.

Kansas Student Loan Forgiveness: 25-Year Rule Explained

You may want to see also

Frequently asked questions

An executive order can potentially forgive some student loans, but it is unlikely to forgive all student loans entirely. The scope and legality of such an action depend on existing laws and the authority granted to the executive branch.

Yes, President Biden used executive orders to implement targeted student loan forgiveness programs, such as those for borrowers in public service or those defrauded by for-profit schools. However, broad, universal forgiveness has not been achieved solely through executive action.

The legality of using executive action for widespread student loan forgiveness is debated. Critics argue it may exceed presidential authority, while supporters point to the Higher Education Act as a potential legal basis. Ultimately, it could face legal challenges in court.

No, an executive order cannot forgive private student loans. Executive actions are limited to federal student loans, as private loans are governed by separate contracts and regulations.