The question of whether Bernie Sanders can forgive student loans has been a central issue in his political platform, particularly during his presidential campaigns. As a staunch advocate for economic equality and education reform, Sanders has proposed ambitious plans to cancel all or a significant portion of outstanding student debt, arguing that it burdens millions of Americans and stifles economic mobility. While he has championed legislation like the College for All Act, which aims to eliminate tuition at public colleges and universities, the authority to forgive student loans ultimately lies with Congress and the executive branch. Despite his influence, Sanders’ ability to implement such policies depends on broader political support and legislative action, making the feasibility of widespread student loan forgiveness a complex and ongoing debate.

Explore related products

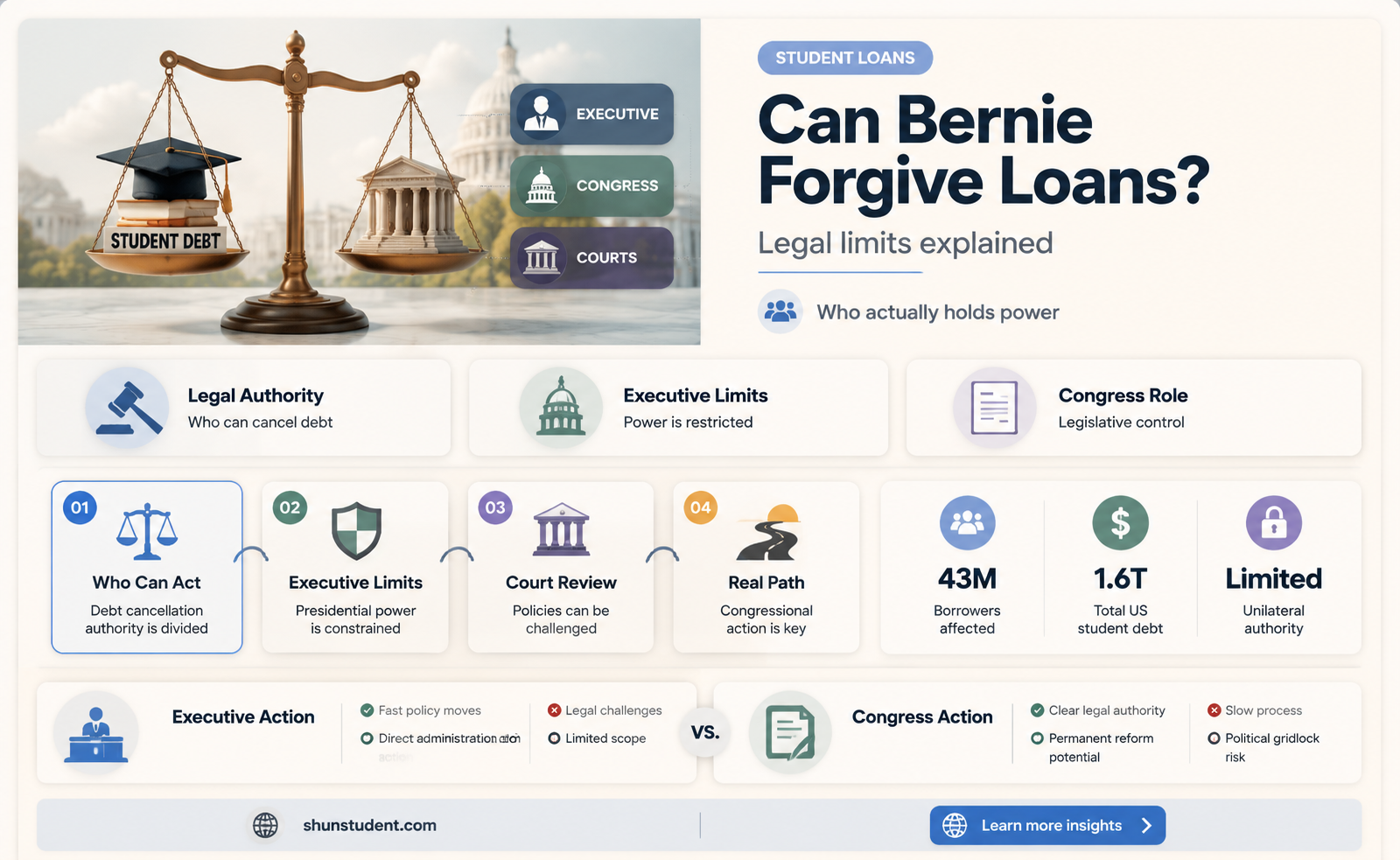

What You'll Learn

- Legal Authority: Does the President have the power to cancel student debt without Congress

- Economic Impact: How would loan forgiveness affect the economy and inflation

- Equity Concerns: Would forgiveness benefit all borrowers equally, or favor certain groups

- Political Feasibility: Can Bernie Sanders rally enough support to make forgiveness happen

- Alternatives to Forgiveness: What other solutions, like income-driven repayment, could be explored

![]()

Legal Authority: Does the President have the power to cancel student debt without Congress?

The question of whether the President can unilaterally cancel student debt hinges on the interpretation of existing legal authority, particularly the Higher Education Act of 1965. Section 432(a) of this act grants the Secretary of Education the power to "enforce, pay, compromise, waive, or release any right, title, claim, lien, or demand, however acquired, including any equity or any right of redemption." Proponents argue this language provides a broad mandate to modify or cancel student loans without congressional approval. However, critics counter that such actions would exceed the intended scope of the law, which primarily focuses on administrative management rather than large-scale debt forgiveness.

Analyzing the legal landscape reveals a complex interplay between executive authority and legislative intent. While the President, through the Secretary of Education, possesses certain administrative powers, these are typically limited to case-by-case adjustments rather than sweeping policy changes. For instance, the Obama administration used this authority to implement income-driven repayment plans and loan forgiveness for defrauded students, but these actions were narrowly tailored and grounded in specific legal provisions. A blanket cancellation of student debt, as some advocates propose, would likely face significant legal challenges, particularly regarding the separation of powers and the non-delegation doctrine.

From a practical standpoint, the logistical challenges of unilateral debt cancellation cannot be overlooked. The Department of Education would need to determine eligibility criteria, manage the financial implications, and ensure compliance with existing laws. Without congressional involvement, these tasks would be fraught with uncertainty and risk. For example, forgiving federal student loans held by private servicers could trigger contractual disputes, while state-level taxation of forgiven debt could create unintended financial burdens for borrowers. These complexities underscore the need for a comprehensive legislative framework rather than an executive order.

Persuasively, the argument for congressional involvement rests on the principle of democratic accountability. Student debt cancellation is a policy decision with far-reaching economic and social implications, affecting not only borrowers but also taxpayers and the broader financial system. By requiring legislative action, Congress can engage in public debate, weigh competing interests, and craft a solution that balances fairness and fiscal responsibility. While the President may have limited authority to address specific cases of hardship, a systemic approach to debt forgiveness demands the legitimacy and stability that only Congress can provide.

In conclusion, while the President possesses certain administrative powers under the Higher Education Act, the authority to cancel student debt on a large scale remains legally ambiguous and practically challenging. Advocates for unilateral action must confront the risks of overstepping constitutional boundaries and the logistical hurdles of implementation. Ultimately, a collaborative approach involving both the executive and legislative branches offers the most viable path forward, ensuring that any solution is both legally sound and politically sustainable.

Jill Stein's Plan to Cancel Student Debt: A Comprehensive Solution

You may want to see also

Explore related products

![]()

Economic Impact: How would loan forgiveness affect the economy and inflation?

Student loan forgiveness, a cornerstone of Bernie Sanders’ policy agenda, would inject approximately $1.6 trillion into the economy by eliminating debt for 45 million Americans. This immediate reduction in household liabilities could stimulate consumer spending, as borrowers redirect monthly payments toward goods, services, and savings. However, the economic ripple effects are complex, intertwining short-term gains with long-term risks, particularly regarding inflationary pressures.

Consider the mechanics of inflation: increased demand without proportional supply growth drives prices upward. Loan forgiveness would boost disposable income, potentially spurring demand for housing, education, and consumer goods. For instance, freed from debt, a 28-year-old teacher earning $50,000 annually could allocate $300–$500 monthly (typical loan payments) to rent, travel, or investments. Multiply this by millions, and aggregate demand rises. If supply chains remain constrained—as seen post-pandemic—this surge could exacerbate inflation, particularly in sectors like housing, where demand already outstrips supply.

Critics argue that broad forgiveness is regressive, benefiting higher-earning graduates disproportionately. A 35-year-old engineer earning $90,000 annually might save $1,000 monthly, while a 25-year-old barista earning $30,000 might save $200. To mitigate this, targeted forgiveness (e.g., capping eligibility at $125,000 income) could reduce inflationary risks by limiting demand spikes. Pairing forgiveness with investments in affordable housing or education supply could further stabilize prices by addressing root causes of inflation in these sectors.

Historically, stimulus measures like the 2021 American Rescue Plan temporarily lifted inflation but also fueled economic growth. Loan forgiveness differs by being a one-time transfer, not recurring spending. Its impact on inflation would hinge on the Federal Reserve’s response: if rates rise to counter inflation, borrowing costs for businesses and homebuyers could offset the stimulus. Conversely, if managed with fiscal discipline—such as funding forgiveness through progressive taxation—the inflationary impact could be muted while still boosting long-term productivity by enabling investment in entrepreneurship or skill development.

In conclusion, while student loan forgiveness could stimulate the economy by freeing up consumer spending, its inflationary consequences depend on implementation details and broader economic conditions. Targeted forgiveness, supply-side investments, and monetary policy coordination could maximize benefits while minimizing risks, turning a politically charged proposal into a tool for balanced economic growth.

Credit Union Employees: Student Loan Forgiveness Eligibility Explained

You may want to see also

Explore related products

![]()

Equity Concerns: Would forgiveness benefit all borrowers equally, or favor certain groups?

Student loan forgiveness, as proposed by figures like Bernie Sanders, raises critical equity concerns. While the policy aims to alleviate financial burdens, its impact would not be uniform across all borrowers. For instance, those with higher loan balances, often stemming from advanced degrees, would benefit more in absolute terms than those with smaller debts. This disparity highlights a key question: does forgiveness disproportionately favor certain groups, such as higher-earning professionals, over others?

Consider the demographic and socioeconomic factors at play. Borrowers from low-income backgrounds, who often rely on federal loans to access higher education, might see significant relief. However, they are also more likely to default or struggle with repayment, making forgiveness a lifeline. In contrast, wealthier borrowers, who may have taken out larger loans for prestigious institutions, could reap substantial financial gains without the same level of need. This imbalance underscores the challenge of designing a policy that equitably serves diverse borrower profiles.

A comparative analysis reveals further inequities. For example, Black and Latino borrowers, who disproportionately carry higher student debt due to systemic barriers, would stand to gain more from forgiveness. Yet, without targeted provisions, the policy could still perpetuate existing inequalities. For instance, if forgiveness is applied universally, it might overlook the unique challenges faced by these groups, such as lower post-graduation earnings and higher default rates. Thus, equity demands a nuanced approach that accounts for intersecting identities and systemic disparities.

To address these concerns, policymakers could consider tiered forgiveness models or income-based caps. For instance, capping forgiveness at a certain income threshold would ensure benefits are directed toward those most in need. Additionally, pairing forgiveness with investments in affordable education and debt counseling could create long-term equity. Practical steps like these would not only mitigate disparities but also align forgiveness with broader goals of social and economic justice. Ultimately, the equity of student loan forgiveness hinges on its ability to address, not exacerbate, the inequalities it seeks to remedy.

Does Nelnet Forgive Student Loans? Understanding Loan Forgiveness Options

You may want to see also

Explore related products

$14.95 $14.95

![]()

Political Feasibility: Can Bernie Sanders rally enough support to make forgiveness happen?

Bernie Sanders has long championed student loan forgiveness as a cornerstone of his progressive agenda, but the political landscape presents formidable challenges to turning this vision into reality. The first hurdle lies in the Senate, where the filibuster requires 60 votes to pass most legislation. With the current partisan divide, securing Republican support for a sweeping forgiveness plan seems unlikely. Sanders could propose a budget reconciliation process, which allows certain fiscal measures to pass with a simple majority, but this strategy is constrained by strict rules and may not accommodate the broad scope of his forgiveness proposal. Without a clear pathway to bypass the filibuster, the feasibility of his plan hinges on building a coalition that transcends partisan lines or fundamentally altering Senate rules, both of which are politically daunting.

To rally sufficient support, Sanders must navigate a complex web of stakeholder interests. Progressives within his own party are largely aligned, but moderate Democrats, particularly those from swing states, may balk at the cost and scope of forgiveness. These lawmakers are sensitive to accusations of fiscal irresponsibility or perceived unfairness to those who have already paid off their loans. Sanders could mitigate these concerns by framing forgiveness as an economic stimulus, citing studies that suggest debt relief could boost consumer spending and reduce defaults. However, this messaging must be paired with a robust strategy to address critics who argue that forgiveness disproportionately benefits higher-income earners, such as doctors and lawyers, rather than those most in need.

Public opinion plays a critical role in Sanders’ ability to mobilize support. Polls consistently show that a majority of Americans favor some form of student debt relief, but the specifics matter. Broad forgiveness, such as Sanders’ proposal to cancel all $1.7 trillion in student debt, may face resistance compared to targeted relief for low-income borrowers or those defrauded by predatory institutions. Sanders could leverage grassroots movements, such as the Debt Collective, to amplify the moral and economic case for forgiveness. However, he must also contend with a vocal minority opposed to any form of debt cancellation, who argue that it undermines personal responsibility and shifts the burden to taxpayers.

Finally, Sanders’ success depends on his ability to leverage his position as a Senate leader and grassroots organizer. He could use his influence to attach forgiveness provisions to must-pass legislation, such as spending bills, or pressure the Biden administration to take executive action. However, executive forgiveness faces legal challenges, as demonstrated by ongoing lawsuits against the Biden administration’s limited relief efforts. Sanders must also balance his advocacy for forgiveness with other priorities, such as healthcare and climate change, to avoid diluting his message. By strategically aligning forgiveness with broader themes of economic justice and generational equity, Sanders could build a coalition powerful enough to overcome political obstacles, but the path remains fraught with uncertainty.

Can Current College Students Qualify for Debt Forgiveness Programs?

You may want to see also

Explore related products

![]()

Alternatives to Forgiveness: What other solutions, like income-driven repayment, could be explored?

Income-driven repayment (IDR) plans are not a new concept, but their potential as a widespread solution to the student debt crisis is often overshadowed by the allure of blanket forgiveness. These plans, which cap monthly payments at a percentage of the borrower's discretionary income, offer a lifeline to those struggling under the weight of six-figure debts. For instance, the Revised Pay As You Earn (REPAYE) plan limits payments to 10% of discretionary income and forgives any remaining balance after 20–25 years of consistent payments. While this doesn't eliminate debt overnight, it transforms an insurmountable burden into manageable installments tied to earning potential.

However, IDR plans are not without flaws. Administrative complexities, such as annual recertification and confusing paperwork, deter many eligible borrowers from enrolling. A 2021 Government Accountability Office report found that only 31% of eligible borrowers were enrolled in IDR plans, highlighting a critical gap between policy and practice. Simplifying the application process, automating income verification, and providing clearer guidance could dramatically increase participation. For example, integrating IDR enrollment into the Free Application for Federal Student Aid (FAFSA) process could capture borrowers at the outset, ensuring they’re aware of their options before repayment begins.

Another alternative worth exploring is expanding Public Service Loan Forgiveness (PSLF), which forgives remaining debt after 10 years of qualifying payments for borrowers working in government or nonprofit sectors. While this program has faced criticism for its stringent eligibility criteria and low approval rates, targeted reforms could make it more accessible. Lowering the required number of payments from 120 to 96 months, broadening the definition of qualifying employment, and streamlining the application process could incentivize more borrowers to pursue public service careers while alleviating their debt burden.

Finally, refinancing federal loans at lower interest rates could provide immediate relief without the long-term commitment of IDR or PSLF. While this option is more commonly associated with private loans, federal borrowers could benefit from a government-backed refinancing program tied to current market rates. For example, reducing interest rates from 6% to 3% on a $30,000 loan could save borrowers over $10,000 in interest payments over 10 years. Pairing this with a moratorium on interest capitalization during economic downturns would further protect borrowers from spiraling debt.

In conclusion, while forgiveness captures headlines, income-driven repayment, streamlined PSLF, and refinancing offer practical, scalable solutions to the student debt crisis. Each approach addresses different facets of the problem, from affordability to accessibility, and could be implemented in tandem for maximum impact. The challenge lies not in choosing one solution over another but in designing a comprehensive strategy that meets borrowers where they are, ensuring no one is left behind.

Adjunct Professors and Student Loan Forgiveness: Eligibility Explained

You may want to see also

Frequently asked questions

Bernie Sanders has proposed canceling all student loan debt in the United States, totaling about $1.6 trillion, as part of his policy agenda. However, as of now, he has not been able to implement this plan due to political and legislative challenges.

Bernie Sanders proposed funding his student loan forgiveness plan through a tax on Wall Street speculation, including a 0.5% tax on stock trades, a 0.1% tax on bond trades, and a 0.005% tax on derivative trades.

Bernie Sanders’ plan specifically focuses on forgiving federal student loan debt. Private student loans would not be included in his proposal, as they are not under federal jurisdiction.