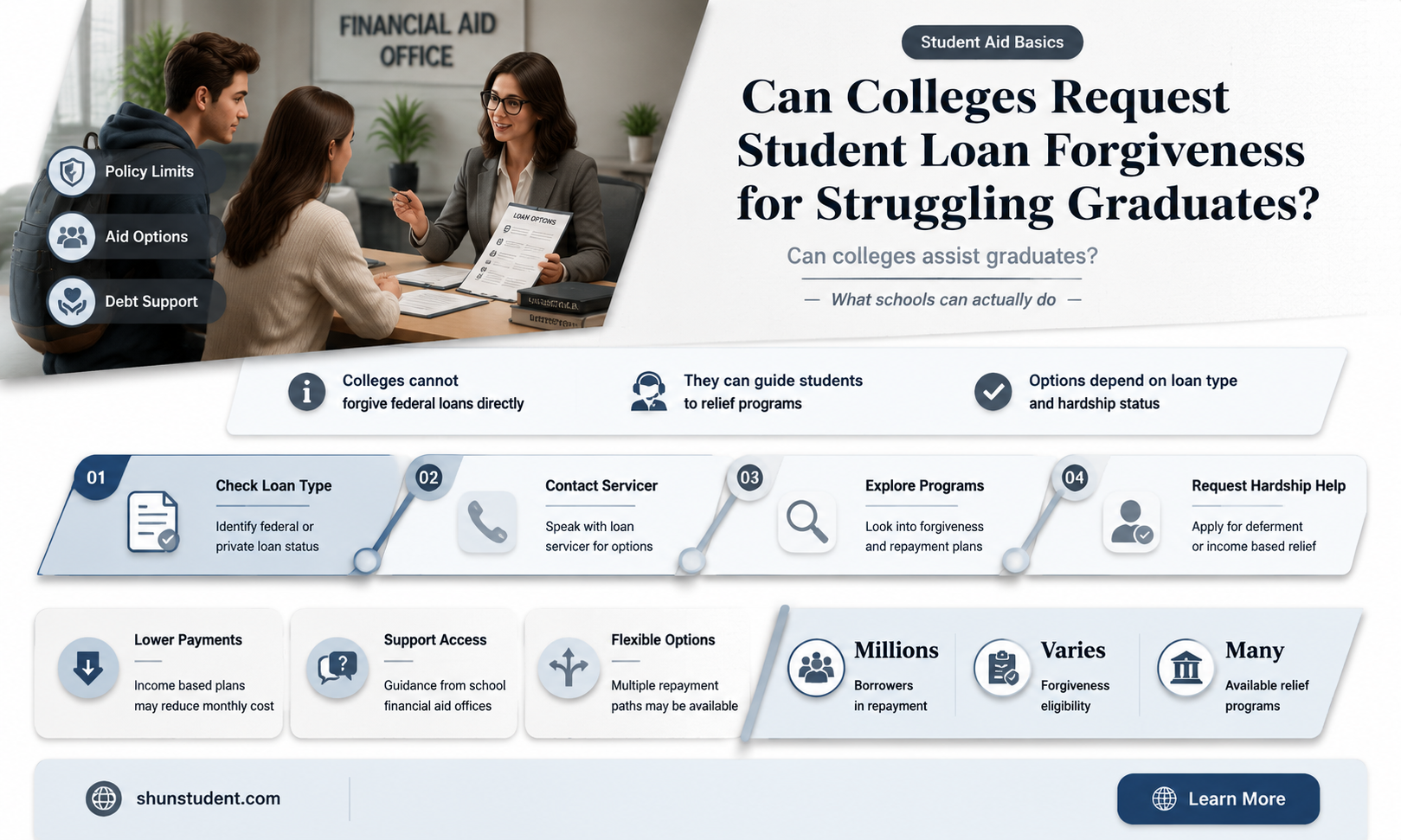

The question of whether a college can request to have a student's loan forgiven is a complex and nuanced issue that intersects with federal regulations, institutional policies, and individual circumstances. While colleges themselves do not have the authority to directly forgive student loans, they can play a role in advocating for or facilitating loan forgiveness programs, particularly in cases where students were defrauded or misled by the institution. For instance, under the Borrower Defense to Repayment program, students who can prove their college engaged in misconduct or violated certain laws may qualify for loan forgiveness, and the college’s involvement in such cases can be pivotal. Additionally, colleges may offer resources or guidance to help students navigate forgiveness options, such as Public Service Loan Forgiveness or income-driven repayment plans. However, the ultimate decision rests with federal loan servicers and the Department of Education, making it essential for students to understand their rights and available pathways to relief.

| Characteristics | Values |

|---|---|

| Can a college request loan forgiveness? | No, colleges cannot directly request student loan forgiveness on behalf of students. |

| Role of colleges in loan forgiveness | Colleges may provide documentation or verification for certain forgiveness programs (e.g., Public Service Loan Forgiveness or Closed School Discharge). |

| Programs requiring college involvement | Closed School Discharge, Borrower Defense to Repayment, Teacher Loan Forgiveness (verification of employment). |

| Primary responsibility for forgiveness | Students must apply for loan forgiveness through their loan servicer or the Department of Education. |

| College liability for student loans | Colleges are not liable for student loans unless they engage in fraud or misconduct (e.g., Borrower Defense to Repayment). |

| Exceptions | In rare cases, colleges may offer institutional loan forgiveness or repayment assistance programs for specific graduates. |

| Federal vs. private loans | Forgiveness programs are primarily for federal loans; private loans are not eligible for college-initiated forgiveness. |

| Documentation required | Colleges may need to provide transcripts, enrollment records, or proof of school closure for specific forgiveness programs. |

| Impact on college reputation | High loan default rates or fraud allegations can affect a college's eligibility to participate in federal aid programs. |

Explore related products

What You'll Learn

- Eligibility Criteria: Specific conditions required for a college to request student loan forgiveness

- Documentation Needed: Essential paperwork colleges must provide to support forgiveness claims

- Types of Forgiveness: Programs like PSLF, institutional forgiveness, or school closure options

- College Responsibility: Role of the institution in initiating or supporting forgiveness requests

- Student Involvement: Steps students must take to collaborate with colleges for forgiveness

![]()

Eligibility Criteria: Specific conditions required for a college to request student loan forgiveness

Colleges rarely have the authority to directly request student loan forgiveness on behalf of their students. However, specific conditions exist where institutions can play a role in facilitating loan forgiveness or discharge. Understanding these eligibility criteria is crucial for both colleges and students navigating the complexities of student debt relief.

Institutional Misconduct or Closure: One of the most direct pathways involves cases where the college itself has engaged in misconduct or has closed abruptly. Under the *Borrower Defense to Repayment* program, students may seek loan forgiveness if their school misled them or violated state laws. For instance, if a college falsely advertised job placement rates or accreditation status, affected students can file claims. In such cases, the college’s actions—not its request—trigger the process, but the institution’s cooperation in providing documentation can expedite outcomes. Similarly, if a college closes while a student is enrolled or shortly after, the *Closed School Discharge* may apply, though this is typically initiated by the student, not the college.

Public Service Loan Forgiveness (PSLF) Employment Certification: While colleges cannot directly request PSLF forgiveness, they can support eligible employees in meeting program requirements. For instance, higher education institutions often qualify as nonprofit organizations, making their employees eligible for PSLF after 10 years of qualifying payments. Colleges can assist by providing timely employment certification forms, ensuring accurate job descriptions, and educating staff about the program. This indirect role is critical, as errors in certification can delay or disqualify forgiveness applications.

Teacher Loan Forgiveness Programs: Colleges of education or institutions with teacher preparation programs can guide graduates toward forgiveness opportunities. For example, the *Teacher Loan Forgiveness* program offers up to $17,500 in forgiveness for teachers working in low-income schools for five consecutive years. While the application is student-driven, colleges can ensure program eligibility by maintaining proper accreditation and providing verification of students’ teaching placements. Additionally, institutions can advocate for students by documenting the school’s eligibility as a low-income institution, a key criterion for forgiveness.

Income-Driven Repayment (IDR) Forgiveness: Though not a direct request mechanism, colleges can counsel students on enrolling in IDR plans, which offer forgiveness after 20–25 years of qualifying payments. By integrating financial literacy programs into student services, institutions can help borrowers understand how to minimize long-term debt. For example, advising students to recertify income annually and choose the most advantageous IDR plan can reduce the time until forgiveness eligibility.

In summary, while colleges cannot unilaterally request student loan forgiveness, they can significantly influence outcomes by addressing institutional misconduct, supporting employees and graduates in qualifying programs, and providing proactive financial guidance. Students and institutions alike must understand these specific conditions to maximize the potential for debt relief.

California Student Loan Forgiveness: Tax Implications and What You Need to Know

You may want to see also

Explore related products

![]()

Documentation Needed: Essential paperwork colleges must provide to support forgiveness claims

Colleges play a pivotal role in substantiating student loan forgiveness claims, but their involvement hinges on providing precise, verifiable documentation. At the core of this process lies the enrollment verification, a record confirming the student’s attendance dates, program details, and status (full-time or part-time). This document is critical for programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, which require proof of qualifying employment during enrollment. Without it, forgiveness claims risk rejection due to unverifiable timelines.

Equally essential is the school closure documentation, which colleges must furnish if they cease operations before a student completes their program. This paperwork includes official closure dates, accreditation status, and any transfer credit agreements. For instance, students affected by the 2019 closure of ITT Tech relied on such records to qualify for borrower defense to repayment. Incomplete or missing details in this documentation can delay or derail forgiveness applications, underscoring the need for colleges to maintain meticulous records.

Another critical piece is the program accreditation status, particularly for career-focused programs. If a program loses accreditation during a student’s enrollment, the college must provide proof of this change, as it directly impacts loan eligibility. For example, students enrolled in unaccredited nursing programs have successfully claimed forgiveness by submitting accreditation revocation notices. Colleges should proactively issue these documents to affected students, ensuring they meet the "misrepresentation" criteria under borrower defense claims.

Lastly, tuition and fee breakdowns are indispensable for claims involving overcharging or unauthorized fees. Colleges must provide itemized statements detailing tuition, fees, and any financial aid applied. This transparency is vital for students alleging they were misled about costs or program outcomes. For instance, students at Corinthian Colleges used such documentation to prove they were charged exorbitant fees for subpar education, leading to widespread loan discharges. Colleges should retain these records for at least six years post-enrollment to support potential claims.

In summary, colleges must prioritize maintaining and providing enrollment verifications, closure records, accreditation statuses, and tuition breakdowns to support loan forgiveness claims. These documents are not merely administrative formalities but lifelines for students seeking relief from burdensome debt. By ensuring accuracy and accessibility, colleges can fulfill their ethical and legal obligations while empowering students to navigate the complex forgiveness process.

Student Loan Forgiveness: What Happens After 120 Payments?

You may want to see also

Explore related products

![]()

Types of Forgiveness: Programs like PSLF, institutional forgiveness, or school closure options

Colleges themselves cannot directly request forgiveness of a student's federal loans, but they can play a role in certain forgiveness programs. Understanding these programs is crucial for both institutions and students navigating the complexities of loan repayment.

Public Service Loan Forgiveness (PSLF) stands out as a beacon for borrowers committed to public service careers. This program forgives the remaining balance on Direct Loans after 120 qualifying payments while working full-time for a qualifying employer, such as government organizations, non-profits, or certain public service entities. Colleges can indirectly support students by providing career counseling that highlights public service opportunities and by offering resources to help graduates navigate the PSLF application process. For instance, many institutions host workshops on loan management, emphasizing the importance of consolidating loans into the Direct Loan program and submitting employment certification forms regularly.

Institutional loan forgiveness programs, though less common, offer another pathway for relief. Some colleges, particularly private institutions, provide loan forgiveness or repayment assistance programs (LRAPs) to graduates who pursue careers in low-paying fields, such as education, social work, or public interest law. These programs often require recipients to meet specific income thresholds and maintain good standing with their loan servicers. For example, a law school might offer LRAP benefits to alumni working in non-profit legal services, forgiving a portion of their loans annually. While colleges initiate these programs, students must actively apply and meet eligibility criteria, making awareness and timely application key to success.

School closure discharges provide a safety net for students whose institutions abruptly cease operations. If a college closes while a student is enrolled or shortly after withdrawal, they may qualify for a discharge of their federal loans under the Closed School Discharge program. This option is not initiated by the college but by the student, who must submit an application to their loan servicer. However, colleges facing financial instability have a responsibility to inform students of their rights and provide guidance on the discharge process. For instance, ITT Tech and Corinthian Colleges’ closures led to thousands of students seeking relief through this program, underscoring the importance of transparency and proactive communication from institutions in distress.

Comparing these forgiveness options reveals distinct eligibility requirements and application processes. PSLF demands a long-term commitment to public service, institutional programs often target specific career paths, and school closure discharges are reactive measures tied to institutional failure. Borrowers must carefully assess their circumstances and choose the program that aligns with their situation. For example, a teacher working in a low-income school might prioritize PSLF, while a social worker with private loans could benefit from an institutional LRAP. Colleges can enhance student outcomes by integrating loan forgiveness education into financial literacy programs, ensuring graduates are equipped to make informed decisions about their debt.

Practical tips for maximizing forgiveness opportunities include maintaining meticulous records, staying informed about program updates, and seeking professional advice when needed. For PSLF, borrowers should submit employment certification forms annually to track qualifying payments. Those pursuing institutional forgiveness should review program guidelines and deadlines regularly. Students affected by school closures should act swiftly to gather necessary documentation and apply for discharge. By combining institutional support with individual diligence, borrowers can navigate the forgiveness landscape more effectively, turning overwhelming debt into manageable—or even forgivable—obligations.

Can Lawyers Qualify for Student Loan Forgiveness? Exploring Options

You may want to see also

Explore related products

![]()

College Responsibility: Role of the institution in initiating or supporting forgiveness requests

Colleges often position themselves as gateways to opportunity, yet their role in the student debt crisis extends beyond enrollment numbers and graduation rates. While federal loan forgiveness programs primarily involve borrowers and loan servicers, institutions of higher education possess unique leverage to initiate or support forgiveness requests. For instance, colleges can identify systemic issues within their programs that lead to disproportionate debt burdens, such as low completion rates in certain majors or inadequate career services. By acknowledging these shortcomings and taking corrective action, colleges can provide evidence to support borrower defense claims, a pathway for loan forgiveness when schools mislead students or violate specific laws.

Consider the case of Corinthian Colleges, a for-profit institution whose closure led to widespread loan forgiveness for defrauded students. While the Department of Education spearheaded the effort, it relied heavily on documentation from the institution itself—enrollment records, marketing materials, and internal communications—to substantiate claims of misconduct. This example underscores the critical role colleges play in maintaining transparent records and cooperating with investigations. Institutions that proactively audit their practices and disclose irregularities not only protect their students but also streamline the forgiveness process for those eligible.

However, initiating or supporting forgiveness requests requires more than reactive compliance. Colleges can adopt a proactive stance by integrating loan forgiveness education into their financial aid counseling. For example, institutions could host workshops on Public Service Loan Forgiveness (PSLF) eligibility, helping students understand how their degree aligns with qualifying employment. Similarly, career services offices could partner with nonprofit organizations to create pipelines for graduates into PSLF-eligible roles. Such efforts not only enhance student outcomes but also position the college as a partner in long-term financial wellness.

Critics may argue that colleges should focus on reducing tuition costs rather than navigating forgiveness programs. While cost containment is essential, the reality is that many students will still rely on loans to fund their education. In this context, institutional support for forgiveness requests becomes a complementary strategy. For instance, colleges could establish emergency funds to cover living expenses for students pursuing PSLF, ensuring they can sustain qualifying employment during the 10-year repayment period. Such measures demonstrate a commitment to student success beyond the classroom.

Ultimately, the responsibility of colleges in loan forgiveness extends to reshaping their relationship with students from transactional to transformative. By acknowledging their role in the debt ecosystem, institutions can move from passive observers to active advocates. Whether through policy reforms, educational initiatives, or financial support, colleges have the tools to mitigate the burden of student loans. In doing so, they not only fulfill their mission of fostering opportunity but also rebuild trust in higher education as a pathway to economic mobility.

Can Dependants Benefit from Student Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Student Involvement: Steps students must take to collaborate with colleges for forgiveness

Students seeking loan forgiveness through college collaboration must first understand their eligibility. Not all institutions or programs qualify, and forgiveness often hinges on specific criteria like attendance at a now-closed school or proven misconduct by the college. Students should start by researching their school’s status on the Federal Student Aid website or through the Department of Education’s Closed School Discharge or Borrower Defense to Repayment programs. Without this foundational knowledge, efforts to collaborate with colleges will lack direction and credibility.

Once eligibility is confirmed, students must gather evidence to support their claim. This includes enrollment records, communication with the college, financial aid documents, and any proof of institutional wrongdoing or closure. For instance, if a student attended a for-profit college that misrepresented job placement rates, emails, brochures, or testimonials from former students could strengthen their case. Organizing this evidence into a clear, concise package demonstrates preparedness and increases the likelihood of college cooperation.

The next step is initiating contact with the college’s administration, specifically the financial aid or legal department. Students should draft a formal, professional letter or email outlining their request, referencing relevant forgiveness programs, and attaching their evidence. Persistence is key; follow-ups every 10–14 days keep the issue on the college’s radar. If the college is unresponsive or resistant, students can escalate by involving external parties, such as state attorneys general or the Department of Education’s oversight teams.

Finally, students must maintain detailed records of all communications and actions taken. This includes saving emails, noting call dates and outcomes, and documenting any advice received from legal or financial advisors. These records not only protect the student’s interests but also provide a timeline of efforts, which can be crucial if disputes arise or if further appeals are necessary. Collaboration with colleges for loan forgiveness is a proactive, evidence-driven process that requires patience, organization, and strategic persistence.

Public Service Loan Forgiveness for Medical Students: A Viable Path?

You may want to see also

Frequently asked questions

No, colleges do not have the authority to request or initiate student loan forgiveness on behalf of students. Loan forgiveness programs are typically managed by the federal government or loan servicers.

Some colleges may offer programs like Public Service Loan Forgiveness (PSLF) employment or loan repayment assistance programs (LRAPs) for graduates working in specific fields, but they cannot directly request forgiveness.

Generally, colleges are not responsible for a student's loan debt unless there is proven fraud, misrepresentation, or violation of specific laws, such as the Borrower Defense to Repayment program.

Attending a specific college does not guarantee loan forgiveness. Eligibility for forgiveness depends on factors like the type of loan, repayment plan, and employment in qualifying fields (e.g., public service or nonprofit work).

A college may issue tuition refunds in certain cases (e.g., dropping a course), but this does not directly impact loan forgiveness. Refunds may reduce the loan amount owed but do not qualify for forgiveness programs.