International students in the US are subject to special rules with respect to the taxation of their income. While the US tax system is a pay-as-you-go system, with automatic tax withholdings from paychecks, stipends, or financial aid, international students may be eligible for tax reductions or exemptions under tax treaty regulations. To determine income tax withholding, universities require international students to complete tax forms, such as Form W-4 and Form 8233, to establish their residency status, tax treaty eligibility, and applicable state forms. International students are generally exempt from Social Security and Medicare taxes for a specified duration and under specific conditions.

| Characteristics | Values |

|---|---|

| Tax residency status | Determined by the Internal Revenue Code residency rules |

| Tax treaty eligibility | Depends on the student's country of origin |

| Tax withholding forms | W-4, CT-W4, 1040-NR, 1040-NR-EZ, 1042-S, 1099-MISC, W-2, W-7, W8-BEN, 8233, 8843 |

| Tax treaty exemption | Requires Form 8233 and a country-specific statement |

| Social Security Number (SSN) | Required for exemption from withholding |

| Tax withholdings | Automatic deductions from paychecks, stipends, or financial aid |

| Tax filing requirement | Annual tax return due in April for the preceding year |

| Tax software | Sprintax Calculus provided by the International Tax Department |

Explore related products

What You'll Learn

![]()

International students' exemption from FICA taxes

International students on F-1, J-1, M-1, or Q-1/Q-2 nonimmigrant status visas are exempt from paying FICA taxes (Social Security and Medicare taxes) on their wages as long as they are enrolled at least half-time and their on-campus employment is incidental to and for the purpose of pursuing a course of study. This exemption is valid for up to five calendar years while they are considered non-resident aliens for tax purposes. After this period, they may become resident aliens and be liable for Social Security and Medicare taxes, unless they still qualify for the "student FICA exemption".

International students who are non-resident aliens for tax purposes and receive compensation for their work are generally considered employees of the university. Their compensation may take the form of wages or salary, depending on factors such as the permanency of the position, level of employee benefits, and job duties. All such payments are processed through the university's payroll services and are subject to federal and state income tax withholding, unless a tax treaty applies.

To claim exemption or reduction of income tax withholding under a tax treaty, international students must complete the required forms, such as Form 8233 and a country-specific statement, with the university's tax department. These forms must be submitted annually, and the university has the right to reject them if the exemption is not warranted or the forms are inaccurate. Additionally, students must have Social Security Numbers before any exemption from withholding can be granted.

It is important to note that the rules regarding taxation for international students can be complex, and there may be additional considerations or exceptions not covered here. The information provided is intended as a general guide, and students should refer to the Internal Revenue Service (IRS) guidelines and consult with their university's tax department or a qualified tax professional for specific advice regarding their individual circumstances.

Northeastern University: Student Ranking System Explained

You may want to see also

Explore related products

![]()

Tax treaties with the US

The United States has entered into agreements with several nations, known as Totalization Agreements, to avoid double taxation of income with respect to Social Security taxes. Additionally, some countries have tax treaty agreements with the US in which certain types of income may be exempted from federal taxes.

Non-resident alien students who are employed by their university and receive compensation in the form of wages or a salary are generally subject to federal and state income tax withholding. However, if a tax treaty exists, and the treaty exempts the total amount of wages, then the non-resident alien student may claim exemption or reduction of income tax withholding. This exemption includes federal, Virginia, and/or DC tax. Maryland does not recognize tax treaties.

To claim the exemption, the student must complete Form 8233, Exemption from Withholding on Compensation for Independent Personal Services of a Nonresident Alien Individual, as well as a country-specific statement that details the terms of the treaty. These forms must be submitted by the university to the IRS for their review and approval. It is important to note that Form 8233 and the country-specific statement must be completed each year.

In most treaties, the residency article contains a "saving clause" that allows the US to tax its citizens as if the treaty had not come into effect, preventing US citizens or residents from using the tax treaty to reduce their US tax liability. However, most treaties offer an exception to the "savings clause" provision for certain types of individuals, including students, trainees, teachers, and researchers.

To be eligible for the benefits of a tax treaty between the United States and their home country, an individual must first be a "resident" of that country. The definition of "resident" may be provided in the tax treaty, but if it is not, the US will look to the laws of the individual's home country to define "resident".

Concordia University Portland: Student Email Access Explained

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![]()

Tax withholding forms

International students, scholars, teachers, researchers, and exchange visitors in the United States are subject to special rules regarding income tax withholding. Nonresident alien students and scholars who have a taxable scholarship or fellowship grant, income partially or totally exempt from tax under a tax treaty, or any other income taxable under the Internal Revenue Code are required to file taxes.

Nonresident alien students must follow a different set of instructions when completing the Form W-4, Employee's Withholding Allowance Certificate. Even if a tax treaty allows an exemption from withholding, a Form W-4 should still be completed as treaty exemptions are not claimed on this form, and provisions may have dollar limitations. Non-resident alien students who do not receive payments that are completely exempt from income tax withholding under a tax treaty will receive a Form W-2, Wage and Tax Statement, from Payroll Services.

If a nonresident alien student is eligible for a tax withholding exception under a treaty provision, they must complete Form 8233, Exemption from Withholding on Compensation for Independent Personal Services of a Nonresident Alien Individual, as well as a country-specific statement that details the terms of the treaty. These forms must be completed annually and submitted by the university to the IRS for review and approval.

International students can apply for an ITIN (Individual Taxpayer Identification Number) by submitting Form W-7 with their annual tax return.

Tax Treaties

Tax treaties vary depending on the state. For example, tax treaties are recognized in Virginia and Washington, D.C., but not in Maryland.

Social Security and Medicare Taxes

Nonresident alien students are generally exempt from Social Security and Medicare Taxes on wages paid to them for services performed within the United States. However, once an individual becomes a Resident Alien, they become liable for self-employment taxes. An exception to this is the FICA exemption, which applies to all students regardless of their tax residency status, as long as they are employed by a school, college, or university where they are enrolled at least half-time.

Syracuse University: International Students' Hub

You may want to see also

Explore related products

$13.65 $25

![]()

Tax residency status

The US tax system is a pay-as-you-go system, with automatic tax withholdings from paychecks, stipends, or financial aid. The amount is estimated based on information provided in tax forms, as well as an individual's tax filing status and residency.

International students and scholars have a federal tax filing requirement, even without US-source income. However, the tax residency status of an international student impacts their tax obligations and requirements.

Non-resident aliens

International students on F-1, J-1, or M-1 visas for less than five calendar years are generally considered non-resident aliens. These students are exempt from Social Security and Medicare taxes on wages for services performed in the US. Non-resident aliens are also exempt from self-employment taxes, as nonimmigrants are generally not permitted to earn self-employment income in the US.

Non-resident alien students who receive payments that are not completely exempt from income tax withholding under a tax treaty will receive a Form W-2, Wage and Tax Statement, from Payroll Services. They must also file Form 8843. If they have earned income in a given year, they will also need to file Form 1040NR or 1040NR-EZ and the corresponding state forms.

Resident aliens

F-1 students who have been in the US for longer than five years are generally considered resident aliens. Resident aliens are liable for self-employment taxes under the same conditions as US citizens. They are also subject to the same federal and state income tax withholding requirements as US citizens.

Tax treaties

Some countries have tax treaties with the US that can reduce or eliminate federal income taxes. Tax treaties vary by country, and students must complete a country-specific statement detailing the terms of the treaty. To claim an exemption under a tax treaty, students must fill out Form 8233, Exemption from Withholding on Compensation for Independent Personal Services of a Nonresident Alien Individual.

Social Security and Medicare taxes

International students are exempt from FICA (Social Security and Medicare) taxes for the first five years on an F-1 visa. F-1 students who have been in the US for more than five years may still be exempt if registered for at least half-time during a semester.

Freiburg University: Applications and Competition

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)

![]()

Tax on scholarships

International students in the United States on F-1, J-1, or M-1 visas are generally considered nonresident aliens and are exempt from paying Social Security and Medicare taxes on wages earned within the United States. However, they may be subject to federal and state income tax withholding on their earnings.

Scholarships, fellowships, and grants paid to nonresident aliens are generally subject to withholding. Tax treaties between the United States and the student's country of residence may reduce the withholding tax rate from 30% to 14% or the treaty rate. To claim this reduced rate, students must complete Form 8233 ("Exemption from Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual") and a country-specific statement detailing the treaty's terms. These forms must be submitted annually and reviewed by the university and the IRS.

If a student's income consists solely of a taxable scholarship, fellowship, or grant, they are required to file a tax return. They must report their exempt and taxable payments and remit any tax due using Forms 1040NR or 1040NR-EZ and corresponding state forms.

It is important to note that universities withhold federal and state income taxes throughout the year based on the Form W-4 ("Employee's Withholding Allowance Certificate") completed by the student. Even if a tax treaty allows an exemption from withholding, students should still complete Form W-4, as treaty exemptions are not claimed on this form, and there may be dollar limitations to the treaty provisions.

Additionally, students who perform services in exchange for pay are generally considered employees of the university and may receive wage payments. These payments are typically processed through Payroll Services and are subject to federal and state income tax withholding unless a tax treaty applies. If no tax treaty exists or does not exempt the total amount of wages, nonresident alien students' wages are subject to the same graduated/progressive federal and state income tax withholding tables.

Commuting Students: Are There University Funds Available?

You may want to see also

Frequently asked questions

Yes, international students are subject to federal and state income taxes. However, there are certain exemptions and treaties that can reduce or eliminate these taxes.

International students must complete Form W-4, Employee's Withholding Allowance Certificate, and any other relevant state forms. If they are eligible for a tax treaty, they must also complete Form W8-BEN, and possibly Form 8233.

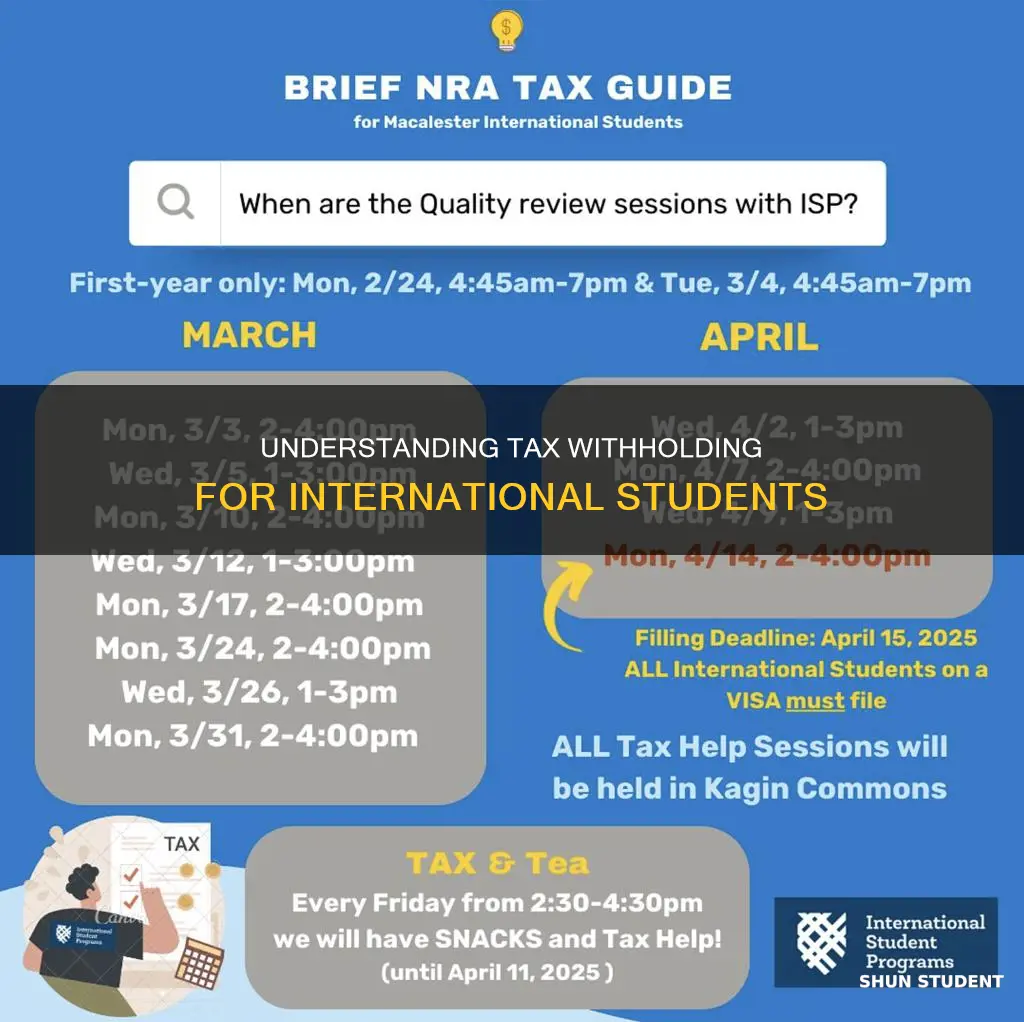

The deadline for filing income tax returns is April 15th of each year.

If you failed to file income tax returns in a previous year, you should file a late income tax return as soon as possible.

International students are generally exempt from Social Security and Medicare taxes for the first 5 years on an F-1 visa. After 5 years, they may still be exempt if they are registered for at least half-time during a semester.