The topic of whether interest is currently accruing on student loans is a pressing concern for many borrowers. With the economic challenges posed by recent global events, the status of student loan interest has been a subject of much debate and policy change. Understanding the current landscape of student loan interest accrual is crucial for borrowers to manage their finances effectively and make informed decisions about their repayment strategies.

Explore related products

What You'll Learn

![]()

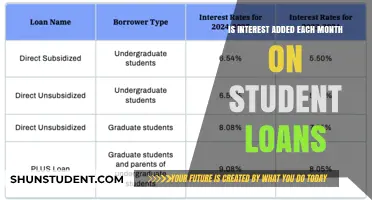

Current interest rates on student loans

As of June 2024, the interest rates on federal student loans in the United States are set by the government and vary depending on the type of loan and the borrower's circumstances. For undergraduate students, the current interest rate for subsidized and unsubsidized loans is 5.5%. Graduate students face higher rates, with unsubsidized loans carrying a 7% interest rate and Graduate PLUS loans at 8.5%. These rates are fixed for the life of the loan, meaning they do not change over time, regardless of market fluctuations.

It's important to note that interest accrues on student loans even while the borrower is in school, although payments are typically deferred until after graduation. This means that students should be aware of the interest rates and how they will impact their overall debt burden. For those with variable-rate private student loans, the interest rate can fluctuate based on market conditions, potentially leading to higher or lower monthly payments over time.

To manage student loan debt effectively, borrowers should consider strategies such as making interest-only payments while in school, if possible, and exploring options for loan forgiveness or income-driven repayment plans after graduation. Additionally, refinancing student loans with a private lender could potentially secure a lower interest rate, although this would depend on the borrower's creditworthiness and other factors.

In conclusion, understanding the current interest rates on student loans is crucial for borrowers to make informed decisions about their education financing. By being aware of the rates and how they impact loan accrual, students can take steps to minimize their debt burden and navigate the complexities of student loan repayment.

Decoding Student Loans: The Interest-First Payment Dilemma Explained

You may want to see also

Explore related products

![]()

Impact of interest accrual on loan balance

Interest accrual on student loans can significantly impact the overall loan balance over time. When interest accrues, it is added to the principal balance of the loan, which means that the borrower will end up paying more in total. This can be particularly concerning for borrowers who are already struggling to make their monthly payments.

One of the key factors that determines the impact of interest accrual on a loan balance is the interest rate. Higher interest rates will result in more interest accruing over time, which will increase the total amount that the borrower owes. Additionally, the frequency with which interest is compounded can also affect the loan balance. Interest that is compounded more frequently will result in a higher total amount owed.

Another important factor to consider is the length of time that the loan is in repayment. The longer the loan is in repayment, the more time interest has to accrue and increase the loan balance. This can be particularly problematic for borrowers who have long repayment terms or who are unable to make large payments towards their loans.

There are a few strategies that borrowers can use to minimize the impact of interest accrual on their loan balance. One strategy is to make extra payments towards the principal balance of the loan. This can help to reduce the amount of interest that accrues over time. Additionally, borrowers can consider refinancing their loans to a lower interest rate, which can also help to reduce the impact of interest accrual.

In conclusion, interest accrual can have a significant impact on the overall loan balance for student loan borrowers. By understanding the factors that contribute to interest accrual and implementing strategies to minimize its impact, borrowers can better manage their student loan debt and avoid paying more than necessary.

COVID Student Loan Interest Rate Expiration: What Borrowers Need to Know

You may want to see also

Explore related products

$15.99 $20

![]()

How interest accrual affects monthly payments

Interest accrual on student loans can significantly impact the total amount paid over the life of the loan. When interest accrues, it is added to the principal balance, which means that the borrower is charged interest on the interest that has already accrued. This can lead to a snowball effect, where the amount owed grows exponentially over time.

For example, let's say a borrower takes out a $10,000 student loan with a 6% interest rate. If the borrower makes no payments for one year, the interest that accrues will be $600. The following year, the borrower will be charged interest on the new balance of $10,600, which will result in an interest charge of $636. As you can see, the amount of interest charged each year is increasing, which will continue to happen until the borrower starts making payments.

The impact of interest accrual on monthly payments can be significant. Using the same example above, if the borrower starts making payments after one year, their monthly payment would be $116.67. However, if the borrower had made payments from the beginning, their monthly payment would have been $100. As a result, the borrower will pay a total of $1,999.92 more in interest over the life of the loan due to the accrual of interest during the first year.

It's important to note that the impact of interest accrual on monthly payments will vary depending on the specific terms of the loan, including the interest rate, the principal balance, and the repayment term. Borrowers should carefully review their loan terms and consider making payments as soon as possible to minimize the impact of interest accrual on their monthly payments.

In conclusion, interest accrual can have a significant impact on the total amount paid over the life of a student loan, and borrowers should be aware of this when considering their repayment options. By making payments as soon as possible and understanding the terms of their loan, borrowers can minimize the impact of interest accrual on their monthly payments and save money in the long run.

When Did Pandemic Student Loan Interest Hold End?

You may want to see also

Explore related products

![]()

Options for managing interest on student loans

If you're grappling with the burden of student loan interest, there are several strategies you can employ to manage it effectively. One option is to consider refinancing your student loans. This involves taking out a new loan with a lower interest rate to pay off your existing loans. By doing so, you can reduce the amount of interest that accrues over time. However, it's important to note that refinancing federal student loans may result in the loss of certain benefits, such as income-driven repayment plans and loan forgiveness programs.

Another approach is to focus on making extra payments towards the principal balance of your loans. By doing this, you can reduce the overall amount of interest that accrues, as interest is calculated based on the outstanding principal balance. Even small extra payments can make a significant difference over time. For example, if you have a $30,000 loan with a 6% interest rate and you make an extra payment of $50 per month, you could save over $4,000 in interest over the life of the loan.

Income-driven repayment plans are another option for managing student loan interest. These plans adjust your monthly payment amount based on your income and family size, which can help make your payments more manageable. Additionally, some income-driven repayment plans offer loan forgiveness after a certain number of years of on-time payments. However, it's important to note that these plans may result in a higher overall interest cost over the life of the loan, as the lower monthly payments may not cover the accruing interest.

If you're struggling to make your student loan payments, it may be worth considering a loan deferment or forbearance. A deferment allows you to temporarily postpone your loan payments, while a forbearance allows you to temporarily reduce or suspend your payments. However, it's important to note that interest may continue to accrue during these periods, so it's essential to understand the terms and conditions of any deferment or forbearance agreement before entering into it.

Finally, it's crucial to stay informed about any changes to student loan policies and interest rates. By staying up-to-date, you can make informed decisions about your repayment strategy and take advantage of any new options or benefits that become available. For example, in response to the COVID-19 pandemic, the federal government implemented a temporary pause on interest accrual and loan payments for certain federal student loans. By staying informed, you can ensure that you're taking advantage of any similar opportunities that may arise in the future.

Navigating Student Loan Interest Tax Deductions: Where to Look

You may want to see also

Explore related products

$10.45 $22.95

![]()

Potential changes to student loan interest policies

Recent discussions around student loan interest policies have sparked debates on the fairness and sustainability of the current system. One potential change being considered is the implementation of a variable interest rate structure, which would tie loan rates to market conditions. This could lead to lower rates for borrowers during economic downturns but might also result in higher rates during periods of economic growth.

Another proposed change is the introduction of income-driven repayment plans, which would cap monthly payments at a percentage of the borrower's income. This could provide relief to those struggling with high payments but might also extend the repayment period and increase the total interest paid over the life of the loan.

Some policymakers are advocating for a complete overhaul of the student loan system, including the elimination of interest altogether. This radical approach would shift the burden of funding higher education from individual borrowers to the government, potentially reducing the financial strain on students and recent graduates.

Critics argue that such changes could lead to unintended consequences, such as increased borrowing and decreased incentives for responsible repayment. They also raise concerns about the potential impact on taxpayers and the overall economy.

As these discussions continue, it is clear that any changes to student loan interest policies will have far-reaching implications for borrowers, lenders, and the broader financial system. Careful consideration and analysis will be necessary to ensure that any reforms are effective, equitable, and sustainable in the long term.

Student Loans That Defer Interest: Types and Eligibility Explained

You may want to see also

Frequently asked questions

As of my last update in June 2024, interest is not accruing on federal student loans. The U.S. Department of Education has implemented a temporary pause on interest accrual and payments for federal student loans due to the COVID-19 pandemic. This pause has been extended several times and is currently in effect.

To check if your student loans are eligible for the interest pause, you should contact your loan servicer or visit the U.S. Department of Education's website for more information. They can provide details on which loans are covered under the pause and any specific requirements or conditions that apply.

If you're unsure about the status of your student loans, it's best to reach out to your loan servicer directly. They can provide you with the most up-to-date information regarding your loan balance, interest accrual status, and any payment obligations you may have during this time. Additionally, staying informed through official government communications and educational resources can help you understand your rights and options as a borrower.