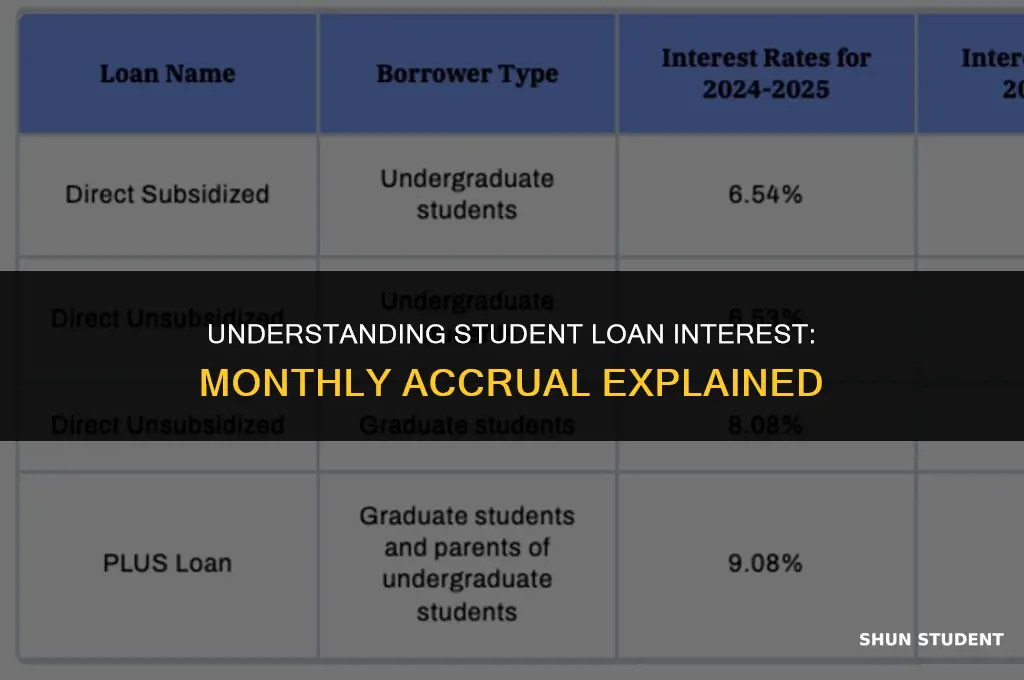

Student loans often come with interest charges that can significantly impact the total amount repaid over time. One common question borrowers have is whether interest is added each month to their loan balance. The answer to this question can vary depending on the specific terms of the loan. For federal student loans, interest typically accrues daily and is capitalized (added to the principal balance) at the end of each billing cycle, which is usually monthly. This means that each month, the interest charged is based on the outstanding principal balance, including any previously accrued interest that has been capitalized. Understanding how interest accrues and is capitalized is crucial for borrowers to manage their student loan debt effectively and make informed decisions about repayment strategies.

| Characteristics | Values |

|---|---|

| Loan Type | Federal or private student loans |

| Interest Accrual Period | Monthly |

| Interest Rate Type | Fixed or variable |

| Fixed Interest Rate Range | Typically between 3% and 7% |

| Variable Interest Rate Index | Often tied to LIBOR or Prime Rate |

| Interest Calculation Method | Compounded monthly |

| Grace Period | Usually 6 months after graduation |

| Repayment Term | 10 to 20 years |

| Interest Subsidy | Available for federal loans during grace period |

| Prepayment Penalty | None for federal loans, may apply for private loans |

| Interest Rate Discounts | Available for automatic payments or good credit |

| Loan Servicer | Varies by loan type and lender |

| Loan Forgiveness Options | Available for certain public service professions |

| Deferment Options | Available for hardship or active military duty |

| Forbearance Options | Available for temporary financial hardship |

| Default Consequences | Damage to credit score, wage garnishment, and legal action |

Explore related products

What You'll Learn

- Interest Accrual Process: How interest is calculated and added to the principal balance monthly

- Types of Interest Rates: Fixed vs. variable rates and their impact on monthly interest charges

- Grace Periods: Timeframes after graduation or loan disbursement when interest may not accrue

- Repayment Strategies: Methods to minimize interest, such as paying more than the minimum monthly payment

- Loan Forgiveness Programs: Options that may forgive accrued interest under certain conditions

![]()

Interest Accrual Process: How interest is calculated and added to the principal balance monthly

The interest accrual process on student loans is a critical aspect that borrowers need to understand. Interest is typically calculated on a daily basis and then added to the principal balance monthly. This means that the interest charged is not just a flat rate but is compounded over time, which can significantly increase the total amount owed.

To calculate the interest, lenders use the daily simple interest formula: Principal x Interest Rate x Number of Days. The interest rate is usually expressed as an annual percentage rate (APR) and is divided by 365 to get the daily rate. The number of days is the actual number of days in the month.

For example, if a borrower has a $10,000 loan with a 6% APR, the daily interest rate would be 6% / 365 = 0.0164%. If the month has 30 days, the interest accrued for that month would be $10,000 x 0.0164% x 30 = $49.20. This amount is then added to the principal balance, making the new balance $10,049.20.

It's important to note that interest accrues even during periods of deferment or forbearance, although the borrower may not be required to make payments during these times. This can lead to a significant increase in the total amount owed by the end of the loan term.

Understanding the interest accrual process can help borrowers make informed decisions about their student loans. By knowing how interest is calculated and added to the principal balance, borrowers can better manage their finances and potentially save money by making extra payments or refinancing their loans.

The Hidden Income: Understanding Student Loan Interest Taxation

You may want to see also

Explore related products

![]()

Types of Interest Rates: Fixed vs. variable rates and their impact on monthly interest charges

Understanding the difference between fixed and variable interest rates is crucial when managing student loan debt. Fixed interest rates remain constant throughout the life of the loan, providing predictability in monthly payments. Variable interest rates, on the other hand, fluctuate based on market conditions, which can lead to changes in the amount of interest charged each month.

For example, if a student loan has a fixed interest rate of 5%, the borrower will pay the same amount of interest each month, regardless of changes in the economy. However, if the loan has a variable interest rate tied to the prime rate, the interest charged could increase or decrease as the prime rate changes. This variability can make budgeting more challenging for borrowers.

The impact of fixed versus variable rates on monthly interest charges can be significant. With a fixed rate, borrowers can plan their finances more effectively, knowing exactly how much interest they will be charged each month. Variable rates, while potentially offering lower initial interest charges, can increase over time, leading to higher overall interest costs.

When considering the question of whether interest is added each month on student loans, it's important to note that both fixed and variable interest rates can result in interest accruing monthly. The key difference lies in the predictability and potential variability of the interest charges. Borrowers should carefully consider their financial situation and future expectations when choosing between fixed and variable interest rates for their student loans.

Why I'm Passionate About Becoming a Student Ambassador

You may want to see also

Explore related products

![]()

Grace Periods: Timeframes after graduation or loan disbursement when interest may not accrue

After graduating from college or receiving a loan disbursement, borrowers may be eligible for a grace period. During this timeframe, interest may not accrue on the loan, providing a temporary reprieve from the financial burden. The length of the grace period varies depending on the type of loan and the lender's policies. For example, federal student loans typically offer a six-month grace period, while private loans may have shorter or longer periods, or none at all.

It's important to note that not all loans are eligible for a grace period. For instance, Parent PLUS loans and private loans may not offer this benefit. Additionally, if a borrower has previously consolidated their loans, they may not be eligible for another grace period. To determine eligibility, borrowers should review their loan agreements or contact their lenders directly.

During the grace period, borrowers are not required to make payments on their loans. However, it's important to remember that interest may still accrue after the grace period ends. Borrowers should consider making payments during the grace period to reduce the overall cost of the loan. Additionally, making payments during the grace period can help borrowers establish a positive payment history and avoid default.

To make the most of the grace period, borrowers should create a budget and prioritize their expenses. They should also consider enrolling in automatic payment plans or setting up reminders to ensure timely payments once the grace period ends. By being proactive and informed, borrowers can effectively manage their student loans and avoid unnecessary financial stress.

Understanding the Real Interest Rate on Student Loans: What You Need to Know

You may want to see also

Explore related products

![]()

Repayment Strategies: Methods to minimize interest, such as paying more than the minimum monthly payment

One effective strategy to minimize interest on student loans is to pay more than the minimum monthly payment. This approach can significantly reduce the total interest paid over the life of the loan. For example, if a borrower has a $30,000 loan with a 6% interest rate and a 10-year repayment term, paying an extra $50 per month could save them over $4,000 in interest.

Another strategy is to make bi-weekly payments instead of monthly payments. This method can help borrowers pay off their loans faster and reduce the total interest paid. By making 26 bi-weekly payments of $150, a borrower could pay off a $30,000 loan with a 6% interest rate in just over 8 years, saving them over $5,000 in interest compared to making 10 years of monthly payments.

Borrowers can also consider refinancing their student loans to a lower interest rate. This strategy can help reduce the total interest paid over the life of the loan, but it's important to note that refinancing federal student loans may result in the loss of certain benefits, such as income-driven repayment plans and loan forgiveness options.

Additionally, borrowers can take advantage of interest rate discounts offered by some lenders. For example, some lenders offer a 0.25% interest rate discount for borrowers who set up automatic payments. While this may seem like a small discount, it can add up over the life of the loan.

Finally, borrowers can consider consolidating their student loans into a single loan with a lower interest rate. This strategy can help simplify repayment and reduce the total interest paid, but it's important to carefully compare the terms and conditions of the new loan with those of the existing loans to ensure that consolidation is the best option.

Navigating Student Loan Interest: Smart Choices for the Marketplace

You may want to see also

Explore related products

![]()

Loan Forgiveness Programs: Options that may forgive accrued interest under certain conditions

Loan forgiveness programs offer a potential solution for borrowers struggling with the burden of accrued interest on their student loans. These programs, often tied to specific conditions or requirements, can provide significant relief by forgiving a portion or all of the interest that has accumulated over time. One such program is the Public Service Loan Forgiveness (PSLF) program, which is designed for borrowers who work in public service jobs and make qualifying payments for 10 years. Under PSLF, not only can borrowers have their principal balance forgiven, but also any accrued interest that has not yet been paid off.

Another option is the Teacher Loan Forgiveness program, which is available to teachers who work in low-income schools and have been teaching for at least five consecutive years. This program can forgive up to $17,500 of a borrower's principal balance, along with any accrued interest that has not been paid. Additionally, some states offer their own loan forgiveness programs for teachers, which may also include forgiveness of accrued interest.

For borrowers who are not eligible for these specific programs, there are other options to consider. Income-Driven Repayment (IDR) plans, for example, can help borrowers manage their monthly payments and may also lead to forgiveness of accrued interest after a certain number of years. Borrowers who are struggling to make payments due to financial hardship may also be eligible for deferment or forbearance, which can temporarily suspend or reduce their monthly payments and prevent further interest from accruing.

It's important to note that loan forgiveness programs often have specific eligibility requirements and application processes. Borrowers should carefully review the terms and conditions of each program to determine if they qualify and to understand the potential tax implications of having their loans forgiven. Additionally, borrowers should be aware that loan forgiveness programs may not cover all types of student loans, and that private loans may not be eligible for these programs.

In conclusion, loan forgiveness programs can provide significant relief for borrowers struggling with accrued interest on their student loans. By understanding the different options available and their specific requirements, borrowers can take steps to manage their debt and potentially reduce the amount of interest they owe.

When Does Student Loan Interest Pause: Key Suspension Scenarios Explained

You may want to see also

Frequently asked questions

Yes, interest is typically added each month on student loans. This is known as accruing interest, and it's important to understand how it works to manage your loan effectively.

Monthly interest accrual can significantly increase the total amount you'll pay back on your student loan over time. The interest that accrues each month is added to your principal balance, and you'll pay interest on this new balance the following month. This compounding effect can lead to a higher total repayment amount.

While you can't avoid paying interest entirely, there are strategies to minimize the amount of interest you'll pay. For example, making payments while you're in school or during your grace period can help reduce the principal balance and, consequently, the amount of interest that accrues. Additionally, refinancing your loan or consolidating multiple loans may offer lower interest rates, which can also help save money over time.