Navigating the complexities of student loan interest and its tax implications can be daunting for borrowers. One of the most common questions is, Where do you find student loan interest for tax purposes? Typically, student loan lenders are required to send borrowers a Form 1098-E, which details the amount of interest paid during the tax year. This form is crucial for claiming the Student Loan Interest Deduction, a potential tax benefit that allows eligible borrowers to deduct up to $2,500 of interest paid on qualified student loans. If you haven’t received a Form 1098-E, you can often access this information through your loan servicer’s online portal or by contacting them directly. Understanding where and how to locate this information is essential for maximizing tax savings and ensuring compliance with IRS regulations.

Explore related products

What You'll Learn

- Federal Tax Deductions: Eligibility criteria and limits for claiming student loan interest on federal taxes

- State Tax Benefits: Variations in state-level deductions for student loan interest payments

- IRS Form 1098-E: Purpose and how to use this form for reporting student loan interest

- Income Phase-Outs: Income thresholds affecting eligibility for student loan interest tax deductions

- Qualified Loans: Types of student loans eligible for interest tax deductions

![]()

Federal Tax Deductions: Eligibility criteria and limits for claiming student loan interest on federal taxes

When it comes to federal tax deductions for student loan interest, understanding the eligibility criteria and limits is essential for maximizing your tax benefits. The Internal Revenue Service (IRS) allows taxpayers to deduct a portion of the interest paid on qualified student loans, which can help reduce taxable income. To claim this deduction, you must meet specific requirements set by the IRS. First and foremost, the student loan must be taken out for qualified higher education expenses, such as tuition, fees, room and board, books, and supplies. The loan must also be used for the taxpayer, their spouse, or a dependent enrolled in an eligible institution at least half-time.

Eligibility for the student loan interest deduction is further restricted by income limits. As of the latest IRS guidelines, the deduction begins to phase out for taxpayers with modified adjusted gross income (MAGI) above certain thresholds. For single filers, the phase-out starts at $70,000 and is completely phased out at $85,000. For married couples filing jointly, the phase-out begins at $140,000 and ends at $170,000. If your MAGI exceeds these limits, you may not be eligible for the deduction or may only qualify for a reduced amount. It’s crucial to calculate your MAGI accurately to determine your eligibility.

The maximum amount you can deduct for student loan interest is $2,500 per year, provided you meet all eligibility criteria. This deduction is claimed as an adjustment to income on your federal tax return, meaning you don’t need to itemize deductions to take advantage of it. However, the actual amount you can deduct may be less than $2,500 if your interest payments were lower or if you fall within the phase-out range. Additionally, the loan must be in your name, and you must be legally obligated to pay the interest to qualify for the deduction.

Another important consideration is that the student loan interest deduction cannot be claimed if someone else claims you as a dependent on their tax return. Similarly, if you are married but file separately, you are not eligible for this deduction. It’s also worth noting that the interest paid on loans from related parties, such as family members, or qualified employer plans does not qualify for this deduction. Ensuring your loan meets all IRS criteria is key to successfully claiming this tax benefit.

To claim the student loan interest deduction, you’ll need to receive Form 1098-E from your loan servicer, which reports the amount of interest paid during the tax year. If you paid less than $600 in interest, you may not receive this form, but you can still claim the deduction if you have documentation of the interest paid. When filing your federal tax return, use the Student Loan Interest Deduction worksheet in the instructions for Form 1040 to calculate your eligible deduction. Proper documentation and adherence to IRS guidelines will ensure you accurately claim this valuable tax benefit.

Understanding US Banks' Interest Rates for Student Loans: A Comprehensive Guide

You may want to see also

Explore related products

$12.98 $17.99

![]()

State Tax Benefits: Variations in state-level deductions for student loan interest payments

When it comes to student loan interest taxes, understanding state-level deductions is crucial, as these benefits can vary significantly from one state to another. While the federal government allows taxpayers to deduct up to $2,500 in student loan interest (subject to income limits), states have their own rules and regulations that can either complement or diverge from federal guidelines. State tax benefits for student loan interest payments are an essential area to explore, as they can provide additional savings for borrowers. Some states, like Iowa and North Dakota, directly follow the federal deduction rules, allowing residents to claim the same amount on their state taxes. This alignment simplifies the filing process for taxpayers in these states, as they can mirror their federal deductions on their state returns.

However, other states offer unique deductions or credits that differ from federal provisions. For example, New York allows taxpayers to deduct student loan interest payments even if they claim the standard deduction on their federal return, providing an additional layer of benefit. Similarly, Maryland offers a tax credit for student loan interest payments, which can be more valuable than a deduction since it directly reduces the tax owed rather than just lowering taxable income. These state-specific benefits highlight the importance of researching local tax laws to maximize potential savings. Borrowers should consult their state’s tax agency or a tax professional to understand the exact rules and eligibility criteria.

In contrast, some states do not offer any deductions or credits for student loan interest payments. States like California and Texas, for instance, do not provide such benefits, meaning residents cannot claim these expenses on their state tax returns. This variation underscores the need for borrowers to be aware of their state’s stance on student loan interest deductions, as it directly impacts their overall tax liability. Additionally, states may impose income limits or caps on the amount of interest that can be deducted, further complicating the landscape. For example, Massachusetts allows a deduction for student loan interest but limits it to $1,500 for single filers and $3,000 for married couples filing jointly.

Another important consideration is how states treat refinanced student loans. Some states, like New Jersey, allow deductions for interest paid on both original and refinanced student loans, while others may restrict deductions to only the original loans. This distinction can significantly affect borrowers who have refinanced their loans to secure better interest rates. Furthermore, states may have different rules regarding the eligibility of loans based on the type of institution attended or the purpose of the loan. For instance, some states may only allow deductions for loans used for undergraduate education, excluding graduate or professional degrees.

Lastly, it’s worth noting that state tax benefits for student loan interest payments can change from year to year due to legislative updates. Borrowers should stay informed about any new laws or amendments that could impact their eligibility or the amount they can claim. Resources such as state tax agency websites, tax software tools, and financial advisors can provide up-to-date information. By understanding and leveraging these state-level deductions, student loan borrowers can optimize their tax returns and reduce their overall financial burden. Always verify the latest rules to ensure compliance and maximize potential savings.

When Do Student Plus Loan Interest Rates Begin Accruing?

You may want to see also

Explore related products

![]()

IRS Form 1098-E: Purpose and how to use this form for reporting student loan interest

IRS Form 1098-E, officially titled "Student Loan Interest Statement," serves a specific purpose in the realm of tax reporting for student loan borrowers. Its primary function is to report the amount of interest paid on qualified student loans during the tax year. This form is crucial because the interest paid on student loans may be eligible for a tax deduction, which can reduce your taxable income. Lenders, including banks, credit unions, and other financial institutions, are required to issue Form 1098-E to borrowers who have paid at least $600 in student loan interest during the year. If you’re eligible for the deduction, this form is your key to claiming it on your tax return.

To use IRS Form 1098-E for reporting student loan interest, start by ensuring you receive the form from your lender by January 31 of the following year. If you haven’t received it by early February, contact your lender to request a copy. The form includes essential information, such as the lender’s name, address, and federal identification number, as well as your name, address, and the total interest paid during the tax year. Box 1 of the form specifically lists the amount of interest you paid, which is the figure you’ll need for your tax return.

Once you have Form 1098-E, you can use the interest amount reported in Box 1 to claim the student loan interest deduction on your federal tax return. This deduction is claimed on Schedule 1 of Form 1040, which is then transferred to your main tax form. It’s important to note that the student loan interest deduction is an "above-the-line" deduction, meaning you can claim it even if you don’t itemize your deductions. However, there are income limits and eligibility criteria, so ensure you meet the requirements before claiming the deduction.

When filling out your taxes, carefully enter the interest amount from Form 1098-E into the appropriate line on Schedule 1. Double-check the accuracy of the amount to avoid errors that could delay your tax refund or trigger an IRS inquiry. If you paid student loan interest to multiple lenders, you should receive a separate Form 1098-E from each one. Add up the interest amounts from all forms to ensure you’re claiming the total eligible deduction.

Finally, keep Form 1098-E and any related documentation with your tax records for at least three years in case the IRS requests verification. Understanding how to use this form correctly can help you maximize your tax benefits and ensure compliance with IRS regulations. If you’re unsure about any aspect of the process, consider consulting a tax professional or using tax preparation software that guides you through the steps. By leveraging Form 1098-E, you can take full advantage of the student loan interest deduction and potentially reduce your tax liability.

Reviving Student Interest: When Does Engagement Spark Again?

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Income Phase-Outs: Income thresholds affecting eligibility for student loan interest tax deductions

When navigating the complexities of student loan interest tax deductions, understanding income phase-outs is crucial. Income phase-outs refer to the specific income thresholds that determine eligibility for claiming the student loan interest deduction. These thresholds vary depending on your filing status, such as single, married filing jointly, or head of household. For instance, as of the most recent tax guidelines, single filers with a modified adjusted gross income (MAGI) above $70,000 and married couples filing jointly with a MAGI above $145,000 begin to phase out of eligibility for this deduction. It’s important to note that these figures are subject to change, so consulting the latest IRS guidelines or a tax professional is essential.

The phase-out range is another critical aspect to consider. For single filers, the deduction begins to phase out between $70,000 and $85,000 in MAGI, while for married couples filing jointly, it phases out between $145,000 and $175,000. Once your income exceeds the upper limit of these ranges, you are no longer eligible to claim the student loan interest deduction. This means that if you earn above $85,000 as a single filer or above $175,000 as a married couple filing jointly, you cannot deduct any student loan interest on your tax return. Understanding these ranges helps you plan your finances and manage expectations regarding potential tax benefits.

For taxpayers filing as head of household, the income phase-out thresholds differ slightly. The phase-out begins at $70,000 and ends at $85,000, mirroring the single filer range. This consistency simplifies the process for head of household filers but underscores the importance of knowing your filing status and its associated thresholds. If you’re unsure about your filing status or how it impacts your eligibility, tools like the IRS’s Interactive Tax Assistant or tax preparation software can provide clarity.

It’s also worth noting that the student loan interest deduction is capped at $2,500 per year, regardless of how much interest you’ve paid. However, the phase-out rules can reduce this amount or eliminate it entirely based on your income. For example, if you’re a single filer with a MAGI of $80,000, you may only be eligible for a partial deduction. Calculating your exact deduction requires understanding both your income level and the phase-out formula, which reduces the deduction by a specific percentage for each dollar earned above the phase-out threshold.

Lastly, keep in mind that the student loan interest deduction is an above-the-line deduction, meaning you can claim it even if you don’t itemize your deductions. However, income phase-outs can still limit or negate this benefit. To find specific information about these thresholds, refer to IRS Publication 970, *Tax Benefits for Education*, or visit the IRS website. Staying informed about these rules ensures you maximize your tax benefits while remaining compliant with federal regulations.

Understanding the Phase-Out of Student Loan Interest Deduction: What You Need to Know

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

Qualified Loans: Types of student loans eligible for interest tax deductions

When it comes to finding student loan interest taxes, understanding which loans qualify for deductions is crucial. The IRS allows taxpayers to deduct up to $2,500 in student loan interest annually, provided the loans meet specific criteria. Qualified loans are those taken out solely to pay for higher education expenses, including tuition, fees, room and board, books, supplies, and other necessary costs. These loans must be used for the taxpayer, their spouse, or dependents and must be taken out during an academic period when the student is enrolled at least half-time in a degree, certificate, or other program leading to a recognized credential.

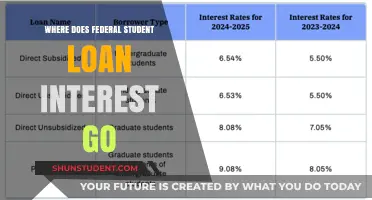

The most common types of qualified loans eligible for interest tax deductions are federal student loans, such as Direct Subsidized Loans, Direct Unsubsidized Loans, PLUS Loans, and consolidated federal loans. These loans are funded by the U.S. Department of Education and are specifically designed to help students and their families cover educational expenses. Federal student loans are often the first choice for borrowers due to their fixed interest rates, flexible repayment plans, and eligibility for loan forgiveness programs. If you’ve paid interest on any of these federal loans, you can claim the deduction as long as you meet the income limits set by the IRS.

In addition to federal loans, certain private student loans also qualify for the interest tax deduction, provided they meet the IRS criteria. Private loans must be used exclusively for qualified higher education expenses and must be taken out by the taxpayer, their spouse, or dependent. It’s important to note that private loans are not automatically eligible—the lender must certify that the loan was used for qualified expenses. Borrowers should request a Form 1098-E from their lender, which reports the amount of interest paid during the tax year and confirms the loan’s eligibility for the deduction.

Another category of qualified loans includes loans taken out through employer-sponsored programs or state-based loan initiatives, as long as they adhere to IRS guidelines. For example, if an employer offers a student loan assistance program and the funds are used for qualified education expenses, the interest on these loans may be deductible. Similarly, state-based loans that meet federal criteria can also qualify. However, loans from family members or other informal arrangements do not meet the IRS definition of a qualified loan, even if they are used for education expenses.

To ensure eligibility for the student loan interest tax deduction, borrowers should carefully review the terms of their loans and maintain detailed records of how funds were used. The IRS scrutinizes whether the loan was used exclusively for qualified education expenses, so documentation is key. If you’re unsure whether your loan qualifies, consult the IRS Publication 970 or speak with a tax professional. Understanding which qualified loans are eligible for the deduction can help you maximize your tax savings and reduce the financial burden of student loan repayment.

Understanding the Latest Interest Rate Changes for Student Loans

You may want to see also

Frequently asked questions

You can find information about student loan interest taxes on your Form 1098-E, which is provided by your loan servicer. This form reports the interest paid during the tax year and is used to claim the Student Loan Interest Deduction on your federal tax return.

You report student loan interest on Schedule 1 (Form 1040), line 20, as part of the Student Loan Interest Deduction. This amount is then transferred to line 16 of your Form 1040.

The rules for claiming student loan interest taxes can be found in IRS Publication 970, *Tax Benefits for Education*. It outlines eligibility requirements, deduction limits, and how to report the interest on your tax return.

If you didn’t receive a Form 1098-E, contact your loan servicer to request a copy. If you paid less than $600 in interest, the servicer is not required to send the form, but you can still claim the deduction by verifying the interest paid through your loan account statements.

You can determine your eligibility for the student loan interest tax deduction by reviewing the criteria in IRS Publication 970. Key factors include your income level, filing status, and whether the loan was used for qualified education expenses.

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)