As the pause on federal student loan interest rates implemented during the COVID-19 pandemic comes to an end, borrowers are eagerly awaiting clarity on when normal student loan interest rates will resume. This pause, which has provided significant financial relief to millions of borrowers, is set to expire, leaving many to wonder about the timing and potential impact of the return to standard interest rates. Understanding when these rates will resume is crucial for borrowers to plan their finances effectively, as it will directly affect monthly payments and long-term repayment strategies. The federal government’s guidance on this transition will play a pivotal role in helping borrowers navigate the post-pause landscape.

| Characteristics | Values |

|---|---|

| Resume Date | September 1, 2023 (for new loans disbursed on/after July 1, 2023) |

| Current Status | Interest rates are temporarily paused due to COVID-19 relief measures |

| Interest Rate for Undergraduate Loans | 5.5% (for loans first disbursed July 1, 2023 - June 30, 2024) |

| Interest Rate for Graduate Loans | 7.05% (for loans first disbursed July 1, 2023 - June 30, 2024) |

| Interest Rate for PLUS Loans | 8.05% (for loans first disbursed July 1, 2023 - June 30, 2024) |

| Payment Resumption | October 1, 2023 (for existing loans, after COVID-19 forbearance ends) |

| COVID-19 Forbearance End Date | September 30, 2023 (interest resumes October 1, 2023) |

| Applicable Loans | Federal student loans (Direct Subsidized, Unsubsidized, PLUS, Consolidation) |

| Private Loans | Not affected by federal interest rate changes; check lender terms |

| Source of Information | U.S. Department of Education, Federal Student Aid |

Explore related products

What You'll Learn

![]()

Federal Student Loan Interest Rates

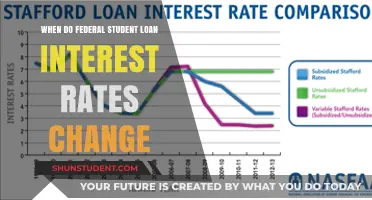

For federal student loans, interest rates are fixed for the life of the loan and are set annually by Congress based on the 10-year Treasury note index. The rates for loans first disbursed between July 1, 2023, and June 30, 2024, are as follows: Direct Subsidized and Unsubsidized Loans for undergraduate students have a rate of 5.5%, while Direct Unsubsidized Loans for graduate or professional students are at 7.05%. Direct PLUS Loans, available to graduate students and parents of dependent undergraduates, carry a rate of 8.05%. These rates reflect a slight increase from the previous year, emphasizing the importance of understanding the financial implications of borrowing.

The resumption of interest accrual means that borrowers will need to factor these rates into their repayment strategies. For example, a borrower with a standard 10-year repayment plan on a $30,000 Direct Unsubsidized Loan for undergraduates at 5.5% interest will face monthly payments of approximately $326. Understanding these rates is crucial for managing loan repayment effectively and exploring options like income-driven repayment plans or loan consolidation to potentially lower monthly payments.

It’s also important to note that interest rates for federal student loans are not retroactive; they apply only to new loans disbursed during the specified period. Existing loans retain their original interest rates, which were determined at the time of disbursement. Borrowers should review their loan agreements or log into their accounts on the Federal Student Aid website to confirm their specific rates and terms. Staying informed about these details can help borrowers make educated decisions and avoid surprises when payments resume.

Lastly, borrowers should be proactive in preparing for the resumption of payments and interest accrual. This includes updating contact information with loan servicers, exploring repayment plans, and considering options like automatic payments, which may qualify for a small interest rate reduction. Additionally, those facing financial hardship should investigate deferment, forbearance, or income-driven repayment plans to manage their obligations. As federal student loan interest rates resume, being informed and prepared will be key to navigating this transition successfully.

Key Factors That Disqualify You from Student Loan Interest Deduction

You may want to see also

Explore related products

![]()

End of COVID-19 Payment Pause

The COVID-19 pandemic brought about unprecedented financial relief measures, including a pause on federal student loan payments and a halt to interest accrual. This payment pause, initially implemented in March 2020, has been extended multiple times, providing borrowers with much-needed financial breathing room. However, as the pandemic situation evolves, the question on many borrowers’ minds is: when will normal student loan interest rates resume? The answer is closely tied to the end of the COVID-19 payment pause, which has been officially set to expire on August 31, 2022, with payments resuming in September 2022. This marks a significant shift for millions of borrowers who have not made payments or accrued interest for over two years.

The end of the COVID-19 payment pause means that federal student loan interest rates will revert to their pre-pandemic levels, and borrowers will once again be responsible for making monthly payments. It’s crucial for borrowers to prepare for this transition by reviewing their loan details, updating their contact information with their loan servicers, and exploring repayment options that align with their financial situation. The U.S. Department of Education has emphasized the importance of proactive planning to avoid delinquency or default once payments resume. Borrowers who were in income-driven repayment plans or pursuing Public Service Loan Forgiveness (PSLF) should ensure their certification and payment counts are up to date.

For those struggling to resume payments, it’s essential to explore available options, such as enrolling in an income-driven repayment plan, which caps monthly payments based on income and family size, or applying for deferment or forbearance if eligible. The Biden administration has also hinted at potential additional relief measures, but as of now, borrowers should assume payments will restart in September. Loan servicers are expected to communicate directly with borrowers about their repayment options and next steps, so staying informed and responsive to these communications is critical.

Another key aspect of the end of the payment pause is the resumption of interest accrual. Since March 2020, federal student loans have had a 0% interest rate, but this will change once the pause ends. Borrowers should factor this into their budgeting, as interest will begin to accrue again, potentially increasing the overall cost of their loans over time. Understanding the terms of your loans, including the interest rate and repayment timeline, will help you manage your finances effectively during this transition.

Finally, the end of the COVID-19 payment pause serves as a reminder for borrowers to reassess their financial goals and priorities. With payments resuming, now is the time to create a sustainable budget, explore opportunities to refinance or consolidate loans (if applicable), and take advantage of resources provided by the Department of Education. While the pause provided temporary relief, the return to normal repayment terms underscores the importance of long-term financial planning. By taking proactive steps now, borrowers can navigate this transition smoothly and work toward achieving financial stability.

When Did the Student Loan Interest Freeze Begin?

You may want to see also

Explore related products

![]()

Private Loan Interest Resumption

As of the latest updates, the resumption of normal student loan interest rates, particularly for private loans, is a critical concern for borrowers. Unlike federal student loans, which have seen interest rate pauses and policy changes due to government interventions, private student loans operate under different terms. Private loan interest resumption typically follows the terms outlined in the loan agreement, which means borrowers need to carefully review their contracts to understand when and how interest will resume.

Private student loans are not subject to federal pauses or waivers, meaning interest accrual generally continues uninterrupted unless specified by the lender. For instance, some private lenders offered temporary forbearance or reduced interest rates during the COVID-19 pandemic, but these measures were voluntary and not mandated. Borrowers who took advantage of such programs should verify with their lender when normal interest rates will resume, as these dates vary widely. It’s essential to check for any communication from the lender regarding the end of any temporary relief measures.

To prepare for private loan interest resumption, borrowers should first confirm the exact date when their regular interest rates will restart. This information can usually be found in the loan agreement or by contacting the lender directly. Once the date is confirmed, borrowers should assess their financial situation to ensure they can manage the increased monthly payments. Creating a budget that accounts for the resumed interest accrual can help avoid delinquency or default. Additionally, exploring options like refinancing or consolidating private loans at a lower interest rate could be a strategic move to reduce long-term costs.

Another important step is to understand the terms of interest capitalization, if applicable. Some private loans capitalize unpaid interest, adding it to the principal balance, which can significantly increase the total cost of the loan. Borrowers should inquire whether their lender plans to capitalize interest upon resumption and take steps to pay off any accrued interest before it is added to the principal. Staying proactive and maintaining open communication with the lender can provide clarity and potentially open doors to alternative repayment plans.

Finally, borrowers should stay informed about any changes in private loan policies or market trends that could impact their interest rates. Economic factors, such as fluctuations in the prime rate, can influence variable-rate private loans. Monitoring these changes and planning accordingly can help borrowers navigate the resumption of normal interest rates more effectively. Being prepared and informed is key to managing private student loan debt responsibly as interest rates return to their standard terms.

Understanding Interest Rates on $10,000 Student Loan Debt

You may want to see also

Explore related products

![]()

New Loan Disbursement Rates

As of the latest updates, normal student loan interest rates are set to resume on new loan disbursements starting September 1, 2024. This resumption follows a period of paused or reduced interest rates due to temporary measures implemented during the COVID-19 pandemic. For borrowers taking out new federal student loans after this date, understanding the new loan disbursement rates is crucial for financial planning. The interest rates for the 2024-2025 academic year are based on the 10-year Treasury note auction held in May 2024, plus a fixed markup determined by the type of loan and borrower status.

For undergraduate students, new Direct Subsidized and Unsubsidized Loans will carry a fixed interest rate of 5.5% for the upcoming academic year. This rate applies to loans first disbursed between July 1, 2024, and June 30, 2025. Graduate and professional students will face a higher rate of 7.05% for new Direct Unsubsidized Loans during the same period. These rates reflect an increase from the previous year, emphasizing the importance of borrowers factoring these costs into their long-term repayment strategies.

Parent borrowers utilizing the Direct PLUS Loan program will see a new disbursement rate of 8.05% for the same period. While this rate is higher than those for undergraduate and graduate loans, it remains fixed for the life of the loan. Borrowers should carefully consider the total cost of borrowing, including interest accrual over time, when deciding to take out PLUS Loans. It’s also advisable to explore alternatives, such as payment plans offered by colleges, to minimize reliance on high-interest debt.

It’s important to note that these new loan disbursement rates are locked in for the duration of the loan, meaning they will not fluctuate with market changes. However, borrowers with existing loans taken out before the rate resumption will continue to pay their original fixed rates. New borrowers should review their financial aid offers carefully, comparing loan options and considering the long-term implications of interest accrual. Utilizing resources like the Federal Student Aid website can provide additional guidance on managing student loan debt effectively.

Lastly, borrowers should stay informed about potential legislative changes that could impact student loan interest rates in the future. While the current rates are set for the 2024-2025 academic year, ongoing discussions in Congress may lead to adjustments in subsequent years. Proactively monitoring these developments and exploring repayment plans, such as income-driven options, can help borrowers navigate the financial challenges associated with new loan disbursement rates. Planning ahead and understanding the terms of new loans are essential steps in managing student debt responsibly.

Where to Deduct Student Loan Interest on Your Tax Return

You may want to see also

Explore related products

![]()

Interest Accrual Restart Date

The Interest Accrual Restart Date is a critical milestone for student loan borrowers, as it marks the point when interest begins to accumulate again on federal student loans after a period of suspension. During the COVID-19 pandemic, the U.S. Department of Education paused interest accrual on federally held student loans as part of the payment pause, providing significant financial relief to millions of borrowers. However, this pause is temporary, and understanding when interest accrual resumes is essential for financial planning. As of the latest updates, the Interest Accrual Restart Date is set to coincide with the end of the student loan payment pause, which has been extended multiple times. Borrowers should closely monitor official announcements from the Department of Education or their loan servicers to confirm the exact date.

Once the Interest Accrual Restart Date is reached, interest will begin to compound daily on federal student loans, increasing the overall balance if payments are not made. This is particularly important for borrowers with unsubsidized loans, as these loans accrue interest from the moment they are disbursed, regardless of whether the borrower is in school or in a grace period. Subsidized loans, on the other hand, do not accrue interest while the borrower is in school, during grace periods, or during authorized deferment periods. Knowing the Interest Accrual Restart Date allows borrowers to prepare by exploring repayment options, such as enrolling in income-driven repayment plans or considering refinancing with private lenders if eligible.

To avoid financial strain, borrowers should take proactive steps before the Interest Accrual Restart Date. This includes updating contact information with loan servicers, reviewing loan balances and interest rates, and creating a budget that accommodates monthly payments. Additionally, borrowers may want to make voluntary payments during the pause to reduce the principal balance, as these payments go directly toward the loan’s principal when interest is not accruing. Understanding the Interest Accrual Restart Date also helps borrowers avoid surprises, such as a sudden increase in their loan balance or higher monthly payments due to capitalized interest.

It’s important to note that the Interest Accrual Restart Date may vary depending on the type of loan and the borrower’s situation. For example, borrowers in certain deferment or forbearance programs may have different timelines. Private student loans are not subject to federal pauses and have their own terms for interest accrual, which typically resumes according to the original loan agreement. Borrowers with both federal and private loans should carefully review the terms of each to understand when interest accrual resumes for all their loans. Staying informed about the Interest Accrual Restart Date ensures borrowers can make timely decisions to manage their debt effectively.

Finally, borrowers should leverage available resources to prepare for the Interest Accrual Restart Date. The Department of Education’s Federal Student Aid website offers tools and information to help borrowers understand their loans and explore repayment options. Loan servicers can also provide personalized guidance on managing payments and interest accrual. By staying informed and taking proactive steps, borrowers can minimize the financial impact of interest accrual resuming and work toward long-term financial stability. The Interest Accrual Restart Date is not just a deadline but an opportunity to reassess and take control of student loan obligations.

Understanding the Maximum Interest Rates on Student Loans: A Comprehensive Guide

You may want to see also

Frequently asked questions

Normal student loan interest rates resumed on September 1, 2023, following the end of the COVID-19 payment pause on August 31, 2023.

Interest rates on existing federal student loans will remain the same as they were before the pause. However, new federal student loans issued after July 1, 2023, may have different rates based on market conditions.

Interest began accruing again on September 1, 2023, for most federal student loans, after the COVID-19 payment pause ended on August 31, 2023.