The question of whether parent plus student loan interest is tax deductible is an important one for many families navigating the complexities of financing higher education. In the United States, the Tax Cuts and Jobs Act of 2017 made significant changes to the tax deductibility of student loan interest. Prior to this legislation, taxpayers could deduct up to $2,500 of student loan interest per year, regardless of their income level. However, the new law eliminated this deduction for tax years 2018 through 2025. Despite this change, there are still some circumstances under which student loan interest may be deductible, such as if the loan was taken out solely for the purpose of paying for qualified higher education expenses and the taxpayer is legally obligated to repay the loan. Additionally, some states offer their own student loan interest deductions, which may help offset the loss of the federal deduction. It's important for taxpayers to consult with a tax professional to understand how these changes impact their specific situation and to explore any available state-level deductions.

Explore related products

What You'll Learn

- Eligibility Criteria: Understand the requirements to qualify for the Parent PLUS loan interest deduction

- Deduction Limits: Explore the maximum amount of interest that can be deducted annually

- Tax Filing Requirements: Learn about the necessary forms and documentation needed to claim the deduction

- Impact on Tax Refund: Discover how the deduction affects your overall tax refund amount

- Common Mistakes: Avoid frequent errors that could lead to the deduction being denied or delayed

![]()

Eligibility Criteria: Understand the requirements to qualify for the Parent PLUS loan interest deduction

To qualify for the Parent PLUS loan interest deduction, there are specific eligibility criteria that must be met. First and foremost, the borrower must have taken out a Parent PLUS loan to cover the educational expenses of their dependent child. This loan must have been used solely for tuition, fees, room and board, and other qualified higher education expenses. Additionally, the borrower must have paid interest on the loan during the tax year for which they are claiming the deduction.

The income of the borrower also plays a crucial role in determining eligibility. There are income limits set by the IRS, and borrowers must fall below these limits to qualify for the deduction. For the 2023 tax year, the income limit is $85,000 for single filers and $170,000 for joint filers. It's important to note that these limits are subject to change, so borrowers should always check the latest IRS guidelines.

Another key requirement is that the borrower must be legally obligated to repay the loan. This means that the loan cannot be in default, and the borrower must be making regular payments. If the loan is in default, the borrower will not be able to claim the interest deduction.

Furthermore, the deduction is only available for interest paid on loans taken out for the borrower's dependent child. This means that if the borrower has taken out a Parent PLUS loan for multiple children, they will need to keep track of the interest paid on each loan separately. The deduction can only be claimed for the interest paid on the loan for the child who is the dependent of the borrower.

Lastly, it's important to keep accurate records of all loan payments and interest paid. This will be necessary when filing taxes to claim the deduction. Borrowers should also be aware that the deduction is subject to phase-out based on income, so even if they meet the eligibility criteria, the amount of the deduction may be reduced if their income is close to the phase-out threshold.

In summary, to qualify for the Parent PLUS loan interest deduction, borrowers must have taken out a Parent PLUS loan for their dependent child, paid interest on the loan during the tax year, fall below the income limits set by the IRS, be legally obligated to repay the loan, and keep accurate records of all loan payments and interest paid. By understanding these eligibility criteria, borrowers can better navigate the tax implications of their Parent PLUS loan and potentially benefit from the interest deduction.

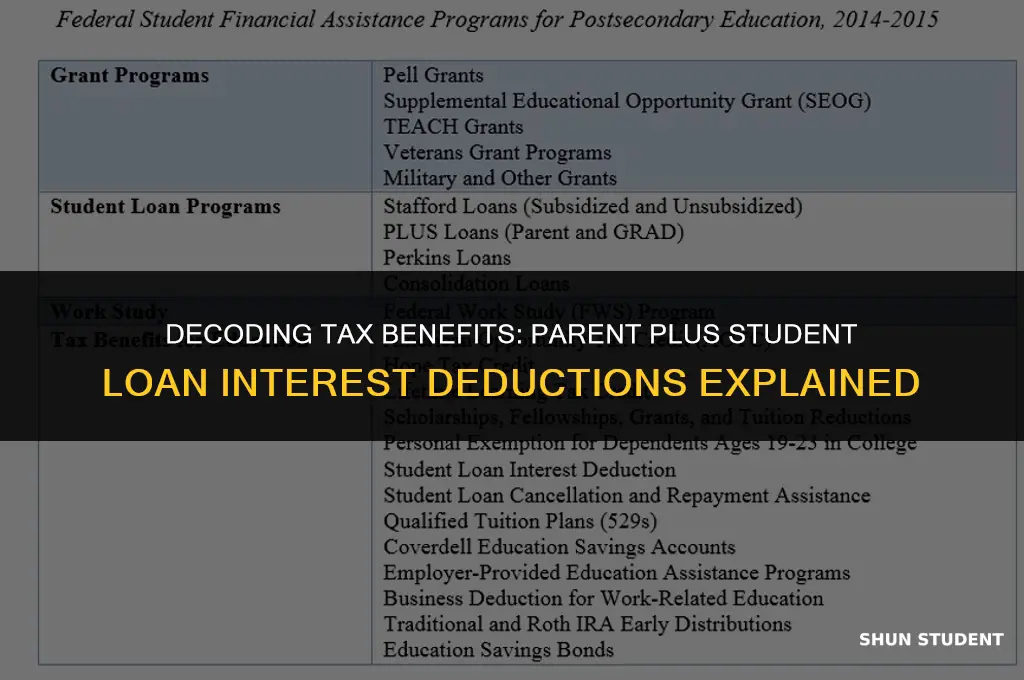

Decoding Student Loan Interest Deductions: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Deduction Limits: Explore the maximum amount of interest that can be deducted annually

The deduction limits for student loan interest can significantly impact the amount of tax relief a borrower or their parent can claim annually. As of the latest tax regulations, the maximum amount of interest that can be deducted is $2,500 per year. This limit applies to both parent and student borrowers, and it's important to note that this is a per-taxpayer limit, not per loan.

To maximize this deduction, borrowers should ensure they are keeping accurate records of their interest payments throughout the year. This can be particularly important for those who have multiple loans or who are unsure about the total amount of interest they are paying. Many loan servicers provide annual statements detailing the interest paid, which can be a valuable resource come tax time.

It's also crucial to understand that the deduction is only available for interest paid on qualified student loans. These are loans taken out solely for the purpose of paying for higher education expenses, and they must meet certain criteria set forth by the IRS. For example, the loan must be for the borrower's own education or for a dependent's education, and it cannot be used for other purposes such as room and board or other living expenses.

Additionally, the deduction is subject to income limits. As of the current tax year, the deduction begins to phase out for taxpayers with modified adjusted gross incomes above $70,000 ($140,000 for joint filers). This means that higher-income borrowers may not be able to claim the full $2,500 deduction, or they may not be able to claim it at all.

To navigate these limits effectively, borrowers should consult with a tax professional or use tax preparation software that can help them determine their eligibility for the deduction and calculate the maximum amount they can claim. It's also important to stay informed about any changes to the tax code that may affect the deduction limits, as these can change from year to year.

In summary, understanding the deduction limits for student loan interest is essential for borrowers looking to maximize their tax relief. By keeping accurate records, ensuring they have qualified loans, and staying within the income limits, borrowers can take full advantage of this valuable tax benefit.

1996 Student Loan Interest Rates: A Look Back at Borrowing Costs

You may want to see also

Explore related products

![]()

Tax Filing Requirements: Learn about the necessary forms and documentation needed to claim the deduction

To claim the deduction for parent plus student loan interest, you must meet specific tax filing requirements. The first step is to ensure you have the necessary forms and documentation. The primary form you'll need is Form 1098-E, which is the Student Loan Interest Statement. This form is provided by the lender and details the amount of interest paid on the student loan during the tax year. It's crucial to obtain this form as it serves as proof of the interest paid and is required by the IRS to claim the deduction.

In addition to Form 1098-E, you may need to provide documentation to prove that you are the borrower and that the loan is for higher education expenses. This could include a copy of the loan agreement, tuition bills, or enrollment records. The IRS may also require additional documentation to verify your income and tax filing status, such as W-2 forms or previous tax returns.

When filing your taxes, you'll need to itemize your deductions on Schedule A of Form 1040. The student loan interest deduction is listed as an itemized deduction, and you'll need to provide the necessary documentation to support your claim. It's important to note that you cannot claim the deduction if you file Form 1040A or Form 1040EZ, as these forms do not allow for itemized deductions.

To ensure you meet all the tax filing requirements, it's recommended to consult with a tax professional or use tax preparation software. These resources can help you navigate the complex tax laws and ensure you have all the necessary documentation to claim the deduction. Remember, the burden of proof is on you, the taxpayer, so it's essential to keep accurate records and provide all the required documentation to support your claim.

In summary, claiming the deduction for parent plus student loan interest requires careful attention to tax filing requirements. By obtaining the necessary forms and documentation, itemizing your deductions, and consulting with a tax professional if needed, you can ensure you meet all the criteria to claim this valuable tax break.

NY State Schedule: Student Loan Interest Deduction Explained

You may want to see also

Explore related products

![Ka-ching!: How your family can cut thousands off your student loan debt without spending a cent [seriously].](https://m.media-amazon.com/images/I/81mX7TbTYsL._AC_UY218_.jpg)

![]()

Impact on Tax Refund: Discover how the deduction affects your overall tax refund amount

The deduction for parent plus student loan interest can have a significant impact on your overall tax refund amount. When you claim this deduction, you reduce your taxable income, which in turn lowers the amount of tax you owe. This can result in a larger refund check or a reduction in the amount you need to pay when filing your taxes.

To understand the full impact of this deduction, it's important to consider your individual tax situation. Factors such as your income level, filing status, and the amount of interest you've paid on the student loan will all influence how much the deduction affects your refund. For example, if you're in a higher tax bracket, the deduction will have a greater impact on your refund amount compared to someone in a lower tax bracket.

One way to estimate the impact of the parent plus student loan interest deduction on your refund is to use a tax calculator or consult with a tax professional. They can help you run the numbers and determine how much the deduction will reduce your taxable income and, subsequently, your tax liability. This can give you a better idea of what to expect when filing your taxes and claiming the deduction.

It's also worth noting that the deduction can only be claimed for interest paid on loans used for higher education expenses. This means that if you've taken out a parent plus loan for other purposes, such as refinancing existing debt or covering living expenses, the interest on those loans may not be eligible for the deduction. Therefore, it's important to keep accurate records of how the loan funds are used to ensure you're only claiming the deduction for eligible expenses.

In summary, the parent plus student loan interest deduction can have a substantial impact on your tax refund amount by reducing your taxable income and lowering your tax liability. However, the exact impact will depend on your individual tax situation and the specific details of your loan. By understanding these factors and consulting with a tax professional if needed, you can make the most of this deduction and potentially increase your tax refund.

Lower Interest Rates: Which Student Loan Type Fits Your Needs?

You may want to see also

Explore related products

$14.87 $15.95

![]()

Common Mistakes: Avoid frequent errors that could lead to the deduction being denied or delayed

One common mistake that can lead to the deduction being denied or delayed is failing to meet the income requirements. To qualify for the student loan interest deduction, your income must be below certain thresholds. For the 2023 tax year, the deduction begins to phase out for single filers with adjusted gross income (AGI) above $70,000 and joint filers with AGI above $145,000. If your income exceeds these limits, you may not be eligible for the full deduction or any deduction at all.

Another frequent error is not maintaining proper documentation. To claim the student loan interest deduction, you must have a Form 1098-E from your lender, which shows the amount of interest you paid during the year. If you don't receive this form or lose it, you may need to request a copy from your lender or use other documentation to substantiate your claim. This can delay the processing of your return and potentially lead to the deduction being denied.

Additionally, some taxpayers mistakenly claim the deduction for interest paid on loans that don't qualify. For example, you can't claim the deduction for interest paid on a loan from a family member or a loan that was used for purposes other than education. Make sure you understand the eligibility requirements for the loan and the interest before claiming the deduction.

Lastly, failing to file your tax return on time can also lead to the deduction being delayed or denied. If you owe taxes, the IRS may apply any refund you're due, including the student loan interest deduction, to your outstanding balance. To avoid this, make sure you file your return by the deadline and pay any taxes you owe promptly.

To avoid these common mistakes, it's essential to carefully review the eligibility requirements for the student loan interest deduction and maintain proper documentation. If you're unsure about any aspect of the deduction, consider consulting with a tax professional to ensure you're claiming it correctly.

Strategic Timing: When to Repay Student Loan Interest Rates Wisely

You may want to see also

Frequently asked questions

Yes, the interest on a Parent PLUS student loan is tax deductible. This deduction can help reduce your taxable income, resulting in a lower tax bill.

To deduct Parent PLUS student loan interest, you must meet certain eligibility requirements. These include having paid the interest on a qualified student loan during the tax year, being the borrower (parent), and having a modified adjusted gross income (MAGI) below a certain threshold. Additionally, the student must be your dependent and enrolled at least half-time in a degree program.

The amount you can deduct for Parent PLUS student loan interest depends on your MAGI and the total interest paid during the tax year. For the 2023 tax year, you can deduct up to $2,500 of student loan interest. However, this deduction phases out as your MAGI increases, and you cannot claim the deduction if your MAGI exceeds certain limits.