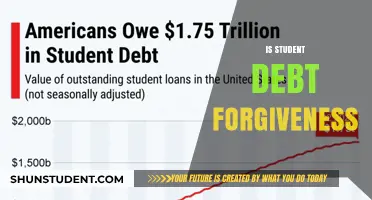

The topic of when Biden’s student loan forgiveness will happen has been a pressing concern for millions of borrowers across the United States. President Joe Biden’s administration has proposed several initiatives aimed at alleviating the burden of student debt, including a plan to forgive up to $20,000 in federal student loans for eligible borrowers. However, the implementation of this forgiveness has faced legal challenges, with multiple lawsuits delaying its rollout. As of now, the timeline remains uncertain, as the Supreme Court’s decision on the matter is pending. Borrowers are advised to stay informed through official channels, such as the Department of Education, for updates on when and how the forgiveness program will proceed.

| Characteristics | Values |

|---|---|

| Program Name | Biden-Harris Administration’s Student Debt Relief Plan |

| Announcement Date | August 24, 2022 |

| Eligibility Criteria | Annual income below $125,000 (individual) or $250,000 (married/family) |

| Debt Forgiveness Amount | Up to $10,000 (non-Pell Grant recipients) / Up to $20,000 (Pell Grant recipients) |

| Loan Types Covered | Federal student loans (Direct Loans, FFELP, Perkins Loans) |

| Current Status | On hold due to legal challenges (as of October 2023) |

| Legal Challenges | Supreme Court ruled against the program in June 2023 |

| Alternative Initiatives | SAVE Plan (income-driven repayment), targeted loan cancellations |

| Application Period | Closed due to legal hold; no new applications accepted |

| Number of Borrowers Affected | Approximately 43 million eligible borrowers |

| Total Debt Relief Estimated | Up to $400 billion |

| Updates as of October 2023 | Administration exploring alternative pathways for debt relief |

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for Biden's student loan forgiveness program based on income and loan type

- Application Process: Steps and timeline for applying for student loan forgiveness under Biden's plan

- Loan Types Covered: Which federal student loans are eligible for forgiveness under the program

- Forgiveness Amounts: Maximum forgiveness amounts for eligible borrowers under Biden's plan

- Implementation Timeline: Expected dates for forgiveness to be processed and applied to accounts

![]()

Eligibility Criteria: Who qualifies for Biden's student loan forgiveness program based on income and loan type

The Biden administration's student loan forgiveness program hinges on two critical factors: your income and the type of loans you hold. Understanding these eligibility criteria is essential for borrowers navigating the complexities of debt relief.

Here's a breakdown to help you determine if you qualify.

Income Thresholds: A Sliding Scale of Relief

The program targets individuals and families with lower to moderate incomes. Single borrowers earning less than $125,000 annually or married couples filing jointly with incomes under $250,000 are eligible for up to $10,000 in forgiveness. Pell Grant recipients, often indicative of greater financial need, can receive up to $20,000 in relief. This tiered approach ensures that those most burdened by student debt receive the most significant assistance.

Loan Type Matters: Federal Loans Take Center Stage

Not all student loans qualify for forgiveness. Only federal student loans held by the Department of Education are eligible. This includes Direct Loans, Federal Family Education Loans (FFEL) held by the government, and Federal Perkins Loans. Private loans, even if used for educational expenses, are excluded from this program. It's crucial to review your loan servicer information to confirm the type of loans you hold.

Navigating the Gray Areas: Part-Time Work and Recent Graduates

Part-time workers and recent graduates often face unique financial situations. The program considers your annual income, regardless of employment status. Even if you work part-time, if your income falls below the threshold, you may still qualify. Recent graduates, even if currently unemployed, are eligible based on their income from the previous year.

Stay Informed and Act Promptly

Eligibility criteria can evolve, so staying informed is crucial. Visit the Federal Student Aid website (https://studentaid.gov/) for the most up-to-date information and application details. Don't delay – taking action promptly ensures you don't miss out on this opportunity for financial relief.

Biden's Student Loan Forgiveness: $10K Relief Plan Explained

You may want to see also

Explore related products

![]()

Application Process: Steps and timeline for applying for student loan forgiveness under Biden's plan

The Biden administration's student loan forgiveness plan has been a beacon of hope for millions of borrowers, but navigating the application process can feel like deciphering a complex map. Understanding the steps and timeline is crucial for maximizing your chances of success.

Here's a breakdown to guide you through the journey.

Phase 1: Preparation (Ongoing)

Think of this as gathering your tools before embarking on a hike. Start by verifying your eligibility. The plan targets borrowers with federal student loans held by the Department of Education, with income thresholds playing a significant role. Gather your loan information, including servicer details and outstanding balances. Create an account on the Federal Student Aid (FSA) website (studentaid.gov) if you haven't already. This will be your central hub for application and updates.

Stay informed through official channels like the FSA website and emails from your loan servicer. Beware of scams – legitimate information will always come directly from the Department of Education.

Phase 2: Application Launch (Expected Late 2023/Early 2024)

Once the application portal opens, act promptly. The exact date remains unconfirmed, but the Department of Education has indicated a late 2023 or early 2024 launch. The application process is expected to be online through the FSA website. Be prepared to provide personal information, loan details, and potentially income verification documents. Double-check your application for accuracy before submitting. Errors can delay processing.

Keep a record of your submission confirmation for future reference.

Phase 3: Review and Processing (Timeline Uncertain)

After submission, your application enters a review period. The Department of Education hasn't disclosed a specific processing timeline, but expect it to take several weeks or even months due to the anticipated high volume of applications. Be patient and avoid submitting multiple applications, as this can cause delays.

Phase 4: Decision and Notification (Timeline Uncertain)

Once your application is processed, you'll receive notification of the decision. If approved, your loan balance will be adjusted accordingly. If denied, you'll be provided with reasons and potential avenues for appeal.

Crucial Considerations:

- Income-Driven Repayment Plans: Even if you're eligible for forgiveness, consider enrolling in an income-driven repayment plan. These plans can lower your monthly payments and potentially lead to additional forgiveness after a certain period.

- Public Service Loan Forgiveness (PSLF): If you work in public service, explore PSLF, which offers forgiveness after 10 years of qualifying payments.

- Stay Informed: The student loan landscape is constantly evolving. Regularly check the FSA website and subscribe to their email updates for the latest information.

Remember, the Biden student loan forgiveness plan is a complex process. By understanding the steps, preparing thoroughly, and staying informed, you can navigate the application process with greater confidence and increase your chances of achieving much-needed relief.

Will Ontario Forgive Student Loans? Exploring Debt Relief Options for Borrowers

You may want to see also

Explore related products

![]()

Loan Types Covered: Which federal student loans are eligible for forgiveness under the program

The Biden administration's student loan forgiveness program has been a topic of much discussion, but understanding which federal student loans qualify is crucial for borrowers seeking relief. Not all federal loans are created equal, and eligibility hinges on specific types and conditions. Here's a breakdown to help you navigate the complexities.

Direct Loans: These are the primary beneficiaries of the forgiveness program. Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans (for both graduate students and parents), and Direct Consolidation Loans are all eligible. If you've been making payments on these loans, you might be closer to forgiveness than you think. For instance, borrowers with Direct Loans who have made 10 years of qualifying payments under an income-driven repayment plan could see their remaining balance forgiven.

Federal Family Education Loan (FFEL) Program Loans and Perkins Loans: Here’s where it gets tricky. FFEL and Perkins Loans are not automatically eligible for forgiveness. However, there’s a workaround. If you consolidate these loans into a Direct Consolidation Loan, they become eligible for forgiveness. This strategy requires careful consideration, as consolidation can reset the clock on certain benefits, such as progress toward Public Service Loan Forgiveness (PSLF). Borrowers should weigh the pros and cons before taking this step.

Income-Driven Repayment (IDR) Forgiveness: For those enrolled in IDR plans, the forgiveness timeline varies. Typically, after 20-25 years of qualifying payments, the remaining balance is forgiven. The Biden administration has proposed adjustments to IDR plans, potentially reducing the repayment period and increasing the amount of income shielded from repayment calculations. These changes could significantly impact eligibility and the speed at which borrowers achieve forgiveness.

Public Service Loan Forgiveness (PSLF): This program offers a faster route to forgiveness for borrowers working in qualifying public service jobs. After 10 years of qualifying payments, the remaining balance is forgiven. The Biden administration has expanded eligibility for PSLF, allowing more borrowers to benefit. For example, payments made under any repayment plan now count toward PSLF, provided the borrower was employed full-time by a qualifying employer.

Practical Tips: To maximize your chances of forgiveness, ensure your loans are in the right category. If you have FFEL or Perkins Loans, consider consolidating them into a Direct Consolidation Loan. Keep detailed records of your payments and employment, especially if you’re aiming for PSLF. Stay updated on policy changes, as the Biden administration continues to refine the program. Finally, consult with a financial advisor or student loan specialist to tailor a strategy that aligns with your unique circumstances.

Understanding which loans qualify for forgiveness is the first step toward financial relief. By focusing on eligible loan types and leveraging available programs, borrowers can navigate the complexities of the Biden student loan forgiveness initiative with greater confidence.

Biden's Student Loan Forgiveness Checks: Fact or Fiction?

You may want to see also

Explore related products

$9.99 $12.99

$14.95 $14.95

![]()

Forgiveness Amounts: Maximum forgiveness amounts for eligible borrowers under Biden's plan

Biden's student loan forgiveness plan has been a beacon of hope for millions of borrowers, but understanding the maximum forgiveness amounts is crucial for managing expectations. The plan offers up to $20,000 in forgiveness for borrowers who received Pell Grants, and $10,000 for those who did not, provided their annual income falls below specified thresholds: $125,000 for individuals or $250,000 for married couples filing jointly. These caps are not arbitrary; they reflect a targeted approach to alleviate the burden on lower- and middle-income borrowers who often struggle the most with repayment.

To qualify for the higher forgiveness amount, borrowers must demonstrate they received a Pell Grant, a need-based award typically given to undergraduates with significant financial need. This distinction underscores the plan’s focus on equity, as Pell Grant recipients often come from disadvantaged backgrounds and carry higher debt loads. For example, a single borrower earning $100,000 annually with a Pell Grant history could see $20,000 wiped from their balance, while a non-Pell Grant recipient in the same income bracket would receive $10,000.

However, the forgiveness amounts are not one-size-fits-all. Borrowers must carefully review their eligibility, particularly their income levels during the COVID-19 pandemic (2020 or 2021 tax years). Those earning above the thresholds are ineligible, regardless of their Pell Grant status. Additionally, the forgiveness applies only to federal student loans held by the Department of Education, excluding private loans and certain types of federal loans not managed by the department.

Practical steps to maximize forgiveness include verifying Pell Grant status through the Federal Student Aid website and ensuring income documentation is accurate. Borrowers should also monitor updates from the Department of Education, as legal challenges and policy changes could impact the timeline and availability of forgiveness. While the plan offers significant relief, understanding these specifics ensures borrowers can navigate the process effectively and set realistic expectations for their financial future.

Rethinking Student Debt Forgiveness: My Shift in Perspective and Why

You may want to see also

Explore related products

![]()

Implementation Timeline: Expected dates for forgiveness to be processed and applied to accounts

The Biden administration's student loan forgiveness program has been a topic of significant interest, with many borrowers eagerly awaiting updates on when they can expect relief. As of the latest information, the implementation timeline for processing and applying forgiveness to accounts is a multi-phase process, influenced by legal challenges and administrative procedures. Here’s a breakdown of what borrowers can anticipate.

Phase 1: Application Submission and Review

Borrowers eligible for forgiveness under the Biden plan must first complete an application, which is expected to be available in the coming months. The Department of Education has indicated that the application process will be streamlined, with an online portal designed to handle high volumes of submissions. Once applications are submitted, a review period will follow, during which eligibility criteria such as income thresholds and loan types will be verified. This phase is projected to take 4–6 weeks from the time of submission, though delays could occur if there is an overwhelming response.

Phase 2: Forgiveness Processing

After eligibility is confirmed, the actual processing of forgiveness will begin. This stage involves adjusting loan balances and notifying loan servicers of the changes. The Department of Education estimates that this step will take an additional 6–8 weeks, depending on the complexity of individual cases. Borrowers should monitor their accounts during this period, as updates may not be immediate. For those with multiple loans, forgiveness may be applied incrementally, starting with the oldest loans first.

Phase 3: Account Updates and Notifications

Once forgiveness is processed, borrowers will receive official notifications confirming the changes to their accounts. Loan servicers will update balances accordingly, and borrowers should see the forgiven amounts reflected within 2–3 weeks of receiving their confirmation. It’s crucial to verify these updates independently, as discrepancies may arise. Borrowers should also be aware that forgiven amounts may have tax implications, though the Biden plan currently excludes forgiven student loans from taxable income through 2025.

Key Considerations and Practical Tips

To ensure a smooth process, borrowers should keep their contact information updated with their loan servicers and the Department of Education. Regularly checking the official Federal Student Aid website for updates is also advisable, as timelines may shift due to legal or administrative developments. Additionally, borrowers should avoid making payments during the processing period unless necessary, as overpayments may not be refundable. For those with private loans or who are unsure of their eligibility, consulting a financial advisor or student loan specialist can provide clarity.

While the exact dates for each phase remain subject to change, the Biden administration has outlined a clear framework for implementing student loan forgiveness. By understanding the timeline and staying proactive, borrowers can navigate the process with greater confidence and minimize potential delays. Patience and vigilance will be key as this historic relief program unfolds.

Forgiving Student Loans for Disability: Understanding the Process Timeline

You may want to see also

Frequently asked questions

The Biden student loan forgiveness program began implementation in late 2022, with eligible borrowers receiving relief starting in October 2022. However, legal challenges have delayed the process, and the timeline remains uncertain pending court decisions.

Borrowers earning less than $125,000 (individuals) or $250,000 (married couples) annually qualify for up to $10,000 in forgiveness, with an additional $10,000 for Pell Grant recipients, provided they meet income criteria.

Student loan payments resumed in October 2023 after a lengthy pause due to the COVID-19 pandemic. Interest also began accruing again at that time.

If the Supreme Court rules against the plan, the forgiveness program will likely be halted, and borrowers will remain responsible for their full loan balances. Payments would continue as scheduled unless further action is taken.