The new interest rate on student loans is a critical topic for borrowers, as it directly impacts the cost of repaying educational debt. Each year, federal student loan interest rates are adjusted based on the 10-year Treasury note auction, with rates for the upcoming academic year typically announced in May. For the 2023-2024 academic year, undergraduate borrowers face a rate of 5.5%, while graduate students and parents with PLUS loans see rates of 7.05% and 8.05%, respectively. These increases reflect broader economic trends, including rising inflation and higher borrowing costs, making it essential for students and families to understand how these changes affect their long-term financial planning and repayment strategies. Private student loan rates, which vary by lender and creditworthiness, are also influenced by these economic factors, further complicating the borrowing landscape.

Explore related products

What You'll Learn

![]()

Federal vs. Private Loan Rates

As of the latest updates, the interest rates on student loans have seen some changes, particularly in the federal loan sector. For the 2023-2024 academic year, federal student loan interest rates have been set at 5.5% for undergraduate Direct Subsidized Loans and Direct Unsubsidized Loans for undergraduate students. Graduate and professional students will face a rate of 7.05% for Direct Unsubsidized Loans, while parents and graduate students borrowing through the Direct PLUS Loan program will see a rate of 8.05%. These rates are fixed for the life of the loan, providing borrowers with predictability in their repayment plans.

When comparing Federal vs. Private Loan Rates, one of the most significant differences is the variability and structure of interest rates. Federal student loans offer fixed interest rates, which means the rate remains the same throughout the loan term. This stability can be particularly beneficial in a fluctuating economic environment. In contrast, private student loans often come with variable interest rates, which can change periodically based on market conditions. While private loans might offer lower initial rates for borrowers with excellent credit, these rates can increase over time, potentially leading to higher overall costs.

Another critical aspect of Federal vs. Private Loan Rates is the eligibility criteria and borrower protections. Federal student loans are need-based and do not require a credit check (except for PLUS Loans), making them accessible to a broader range of students. They also come with flexible repayment options, including income-driven repayment plans, deferment, and forbearance, which can provide relief during financial hardships. Private loans, on the other hand, typically require a good credit history or a cosigner, and they offer fewer repayment options and protections. This lack of flexibility can make private loans riskier, especially for borrowers who may face economic uncertainty after graduation.

The Federal vs. Private Loan Rates comparison also highlights differences in loan limits and fees. Federal loans have annual and aggregate borrowing limits, which are designed to prevent students from taking on excessive debt. Additionally, federal loans have relatively low origination fees, which are deducted from the loan amount. Private loans often have higher borrowing limits, which can be advantageous for students attending expensive institutions, but they also come with higher origination fees and may include additional charges. These factors can significantly impact the total cost of borrowing.

Lastly, it’s important to consider the long-term implications of choosing between federal and private loans. Federal loans offer loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), which can eliminate remaining debt after a certain number of qualifying payments. Private loans rarely offer such forgiveness options, making them a less attractive choice for borrowers pursuing careers in public service or nonprofit sectors. When evaluating Federal vs. Private Loan Rates, borrowers should weigh not only the immediate interest rates but also the long-term benefits and protections provided by federal loans. Making an informed decision based on individual financial circumstances and career goals is crucial for managing student loan debt effectively.

Understanding the Maximum Interest Rates on Student Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Current Interest Rate Trends

As of the latest updates, the interest rates on federal student loans for the 2023-2024 academic year have been set, reflecting broader economic trends and federal monetary policies. For undergraduate students, the interest rate on Direct Subsidized and Unsubsidized Loans is 5.5%, up from 4.99% in the previous year. Graduate students face a higher rate of 7.05% on Direct Unsubsidized Loans, while PLUS Loans for parents and graduate students are set at 8.05%. These increases are tied to the rising yield on 10-year Treasury notes, which is a key benchmark for federal student loan rates. Borrowers should note that these rates are fixed for the life of the loan, meaning they will not change over time unless the borrower refinances.

The upward trend in student loan interest rates mirrors the Federal Reserve’s efforts to combat inflation through higher interest rates. As the Fed raises its benchmark rate, borrowing costs across the economy, including student loans, tend to increase. This shift has significant implications for current and future borrowers, as higher rates translate to larger monthly payments and increased total repayment amounts over the life of the loan. For example, a borrower with a $30,000 loan at 5.5% will pay approximately $3,000 more in interest over a 10-year repayment period compared to a rate of 4.99%.

Private student loan interest rates have also been on the rise, though they vary widely depending on the lender, the borrower’s creditworthiness, and market conditions. Unlike federal loans, private loan rates can be fixed or variable, with variable rates often tied to indices like the Prime Rate or LIBOR. As of recent data, private loan rates range from around 4% to 13% or more, with variable rates generally starting lower but carrying the risk of increasing over time. Borrowers considering private loans should carefully compare offers and consider the long-term impact of rising rates on their financial health.

For existing borrowers with federal student loans, the current interest rate environment underscores the importance of exploring repayment strategies to manage debt effectively. Options such as income-driven repayment plans, loan consolidation, or refinancing (for private loans) can help mitigate the impact of higher rates. Additionally, borrowers should stay informed about potential policy changes, such as interest rate caps or loan forgiveness programs, which could provide relief in the future.

In summary, the current interest rate trends for student loans reflect a broader economic shift toward higher borrowing costs. Federal student loan rates have increased for the 2023-2024 academic year, while private loan rates remain variable and dependent on market conditions. Borrowers must carefully consider these trends when planning for repayment and explore strategies to minimize the financial burden of higher interest rates. Staying informed and proactive is key to navigating this evolving landscape.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![]()

Impact on Monthly Payments

The recent changes in student loan interest rates are set to have a tangible impact on borrowers' monthly payments, influencing both short-term budgets and long-term financial planning. For those with federal student loans, the new interest rates, which typically adjust annually based on the 10-year Treasury note, will directly affect the cost of borrowing. If the interest rate has increased, borrowers can expect higher monthly payments, assuming all other factors remain constant. This is particularly significant for loans with a standard repayment plan, where the monthly amount is calculated to ensure the loan is paid off within a fixed period, usually 10 years. Even a small uptick in interest rates can lead to a noticeable rise in monthly obligations, requiring borrowers to adjust their financial strategies accordingly.

For borrowers on income-driven repayment plans, the impact of the new interest rate may be slightly different but no less important. These plans cap monthly payments at a percentage of the borrower’s discretionary income, but the accruing interest can still affect the overall loan balance. If the interest rate has risen, borrowers may find that their payments cover less of the principal balance, leading to more interest capitalization over time. This could result in higher total repayment amounts, even if the monthly payments remain relatively stable. Understanding this dynamic is crucial for borrowers to assess whether switching to a different repayment plan might be more beneficial in the long run.

Graduate students and parents with PLUS loans are also likely to feel the effects of the new interest rates, as these loans often carry higher rates than undergraduate loans. An increase in interest rates will disproportionately impact these borrowers, as their monthly payments will rise more significantly compared to those with lower-rate loans. For example, a parent with a PLUS loan may see their monthly payment increase by $50 or more, depending on the loan amount and the size of the rate hike. This underscores the need for these borrowers to review their budgets and explore options like refinancing or consolidating loans to mitigate the impact.

Private student loan borrowers may experience a different kind of impact, as their interest rates are typically fixed or variable based on market conditions and creditworthiness. If the federal rate increase signals a broader trend in rising interest rates, private loan borrowers with variable rates could see their monthly payments climb as well. Even those with fixed rates might consider refinancing to lock in a lower rate before further increases occur. However, this strategy depends on individual credit profiles and market conditions, making it essential for borrowers to monitor their loans closely and act proactively.

Finally, the psychological and behavioral impact of higher monthly payments cannot be overlooked. For many borrowers, even a modest increase in monthly obligations can strain already tight budgets, potentially leading to financial stress or difficulty meeting other financial goals. Borrowers should take this opportunity to reassess their overall financial health, explore opportunities for additional income, and consider reaching out to loan servicers for assistance. Programs like loan deferment, forbearance, or switching to an income-driven plan can provide temporary relief, though they may not be suitable for everyone. By staying informed and taking decisive action, borrowers can navigate the impact of the new interest rates on their monthly payments more effectively.

Discovering New Horizons: The Most Fascinating Aspect of Student Life

You may want to see also

Explore related products

![]()

Fixed vs. Variable Rates

As of the latest updates, the interest rates on student loans have been a topic of significant discussion, especially with the recent changes in federal and private loan rates. When considering student loans, one of the most critical decisions borrowers face is choosing between fixed and variable interest rates. This decision can have long-term financial implications, so understanding the differences is essential.

Fixed interest rates remain constant throughout the life of the loan. This means that the rate you agree to when you take out the loan will not change, regardless of market fluctuations. For federal student loans, the government sets fixed rates annually, and these rates apply to all borrowers who take out loans during that period. For example, as of the 2023-2024 academic year, undergraduate federal Direct Loans have a fixed rate of 5.5%, while graduate Direct Loans are at 7.05%, and PLUS Loans are at 8.05%. Fixed rates offer predictability, as your monthly payments will remain stable, making it easier to budget and plan for repayment. This stability is particularly beneficial in a rising interest rate environment, as borrowers are shielded from potential increases.

On the other hand, variable interest rates fluctuate over time based on an underlying index, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. Private student loans often offer variable rates, which may start lower than fixed rates but can increase over time. For instance, a variable rate might begin at 3% but could rise to 7% or higher if market conditions change. While variable rates can be advantageous in a falling interest rate environment, they carry the risk of higher costs if rates rise. Borrowers with variable rates must be prepared for the possibility of increased monthly payments, which can complicate financial planning.

Choosing between fixed and variable rates depends on your risk tolerance and financial outlook. If you prefer stability and want to lock in a consistent payment, a fixed rate is generally the better option. It’s particularly appealing for long-term loans, as it protects you from potential rate hikes. Conversely, if you’re comfortable with some uncertainty and believe interest rates may decrease or remain low, a variable rate could save you money in the short term. However, it’s crucial to consider the worst-case scenario and ensure you can afford higher payments if rates rise.

Another factor to consider is the current economic climate. In periods of low interest rates, variable rates may seem more attractive, but they can quickly become less favorable if rates begin to climb. Fixed rates, while often higher initially, provide peace of mind and are typically recommended for borrowers who prioritize long-term financial security. Additionally, some private lenders offer the option to refinance loans later, which can allow borrowers to switch from a variable to a fixed rate if their financial situation or market conditions change.

In summary, the choice between fixed and variable rates hinges on your personal financial goals and risk tolerance. Fixed rates offer stability and predictability, making them ideal for borrowers who want consistent payments. Variable rates, while potentially lower initially, come with the risk of increasing costs and are better suited for those willing to accept uncertainty. When evaluating the new interest rates on student loans, carefully weigh these factors to make an informed decision that aligns with your long-term financial strategy.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

$16.53 $22.99

![]()

Loan Refinancing Options

As of the latest updates, the interest rates on federal student loans for the 2023-2024 academic year have been set, with undergraduate loans at 5.5%, graduate loans at 7.05%, and PLUS loans at 8.05%. These rates are fixed for the life of the loan, but they do not apply to private student loans, which can have variable rates and terms. Given these new rates, many borrowers are exploring loan refinancing options to manage their debt more effectively. Refinancing involves taking out a new loan with a private lender to pay off existing student loans, often with the goal of securing a lower interest rate or better repayment terms.

One of the primary benefits of loan refinancing options is the potential to reduce your interest rate, especially if you have a high credit score or a stable income. Private lenders often offer competitive rates that can be lower than federal loan rates, particularly for borrowers with excellent financial profiles. For example, if you originally borrowed when interest rates were higher, refinancing now could save you thousands of dollars over the life of the loan. However, it’s crucial to compare offers from multiple lenders to ensure you’re getting the best deal. Many lenders also offer pre-qualification tools that allow you to check potential rates without affecting your credit score.

Another advantage of loan refinancing options is the ability to customize your repayment terms. Federal loans typically come with standard repayment plans, but private refinancing allows you to choose a term length that fits your financial goals. For instance, you might opt for a shorter term to pay off the loan faster and save on interest, or a longer term to reduce your monthly payments. Keep in mind, though, that extending the repayment term can increase the total interest paid over time. Refinancing also gives you the flexibility to switch from a variable-rate loan to a fixed-rate loan, providing stability in your monthly payments.

While loan refinancing options can be beneficial, they are not without drawbacks, especially for federal loan borrowers. Refinancing federal loans with a private lender means losing access to federal protections such as income-driven repayment plans, loan forgiveness programs, and deferment or forbearance options. If you’re considering refinancing federal loans, carefully weigh the potential savings against the loss of these benefits. For private loans, however, refinancing is often a straightforward decision if you can secure a lower rate or better terms.

To explore loan refinancing options, start by assessing your current financial situation and creditworthiness. Lenders will evaluate your credit score, income, employment history, and debt-to-income ratio when determining your eligibility and interest rate. It’s also important to read the fine print of any refinancing offer, as some lenders may charge origination fees or have prepayment penalties. By taking a strategic approach and doing thorough research, you can leverage loan refinancing to achieve greater financial flexibility and savings in managing your student debt.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Frequently asked questions

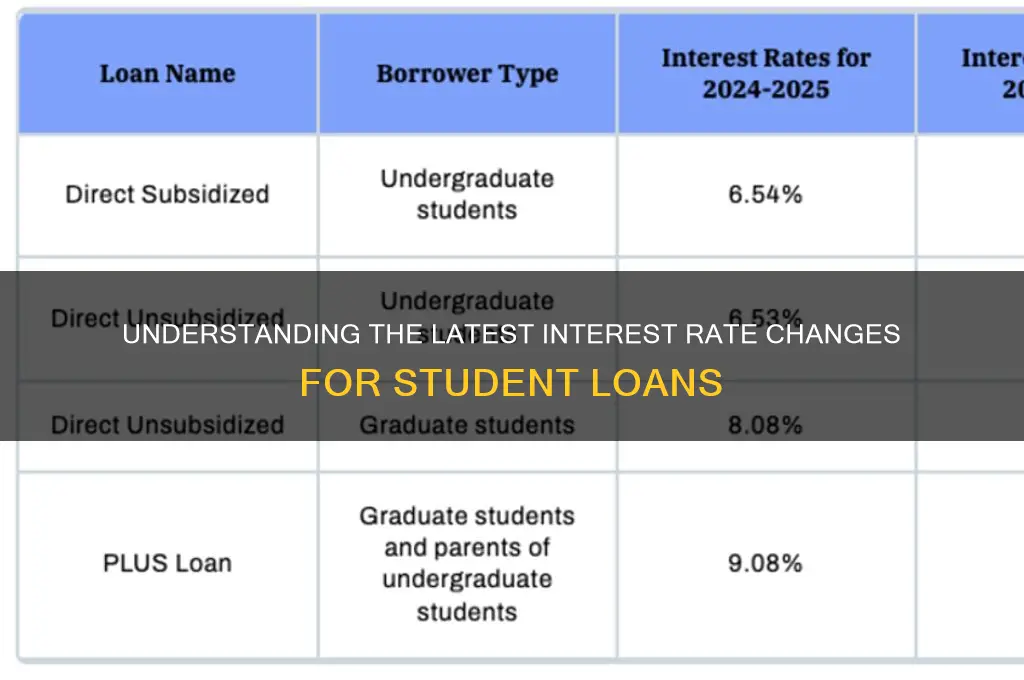

The new interest rates for federal student loans disbursed between July 1, 2023, and June 30, 2024, are as follows: 5.5% for undergraduate Direct Loans, 7.05% for graduate Direct Loans, and 8.05% for Direct PLUS Loans.

The new interest rates for 2023-2024 are higher than the previous year (2022-2023), which were 4.99% for undergraduate loans, 6.54% for graduate loans, and 7.54% for PLUS loans. This increase reflects rising market interest rates.

Private student loan interest rates are not tied to federal rates and vary by lender, creditworthiness, and market conditions. Borrowers should check with their lender for current rates and terms.