The prevailing student loan interest rate is a critical factor for millions of borrowers, as it directly impacts the cost of financing higher education. As of recent updates, federal student loan interest rates for the 2023-2024 academic year range from 5.5% for undergraduate Direct Subsidized and Unsubsidized Loans to 8.05% for graduate PLUS Loans, reflecting adjustments tied to the 10-year Treasury note. Private student loan rates, however, vary widely based on creditworthiness, lender policies, and market conditions, often ranging from 4% to 13% or higher. Understanding these rates is essential for borrowers to make informed decisions about repayment strategies, loan consolidation, or refinancing options, especially as interest accrual significantly influences the total amount repaid over time.

Explore related products

What You'll Learn

![]()

Federal vs. Private Loan Rates

As of the most recent data, the prevailing student loan interest rates vary significantly between federal and private loans, each with its own set of advantages and drawbacks. Federal student loans, which are issued by the U.S. Department of Education, offer fixed interest rates that are set by Congress annually. For the 2023-2024 academic year, undergraduate students can expect to pay 5.5% on Direct Subsidized and Unsubsidized Loans, while graduate students face a rate of 7.05% on Direct Unsubsidized Loans. PLUS Loans, available to graduate students and parents, carry a higher rate of 8.05%. These federal rates are generally lower than private loan rates and come with borrower protections such as income-driven repayment plans, deferment, and forbearance options.

In contrast, private student loan interest rates are determined by lenders and are often variable, meaning they can fluctuate over the life of the loan based on market conditions. As of recent trends, private loan rates typically range from about 4% to 13%, depending on the borrower’s creditworthiness and the lender’s terms. While some private loans may offer lower rates than federal PLUS Loans, they rarely beat the rates for federal undergraduate loans. Private loans also lack the flexible repayment options and protections provided by federal loans, making them a riskier choice for borrowers with uncertain financial futures.

One key difference between federal and private loan rates is how they are assigned. Federal loan rates are standardized and do not depend on the borrower’s credit history, ensuring equal access for all eligible students. Private lenders, however, assess the borrower’s credit score, income, and debt-to-income ratio to determine the interest rate. Borrowers with excellent credit may secure lower rates, but those with poor or limited credit history often face higher rates or may need a cosigner to qualify. This credit-based pricing model can make private loans less accessible or more expensive for many students.

Another important factor to consider is the long-term cost implications of federal versus private loan rates. Federal loans offer fixed rates, providing predictability in monthly payments and total repayment amounts. Private loans with variable rates, on the other hand, can lead to unexpected increases in monthly payments if interest rates rise. Additionally, federal loans come with the option to consolidate or refinance through government programs, whereas private loans may have stricter refinancing requirements and fewer options for managing repayment.

For borrowers deciding between federal and private loans, it’s crucial to weigh the interest rates alongside other factors such as repayment flexibility, borrower protections, and eligibility requirements. Federal loans are generally recommended as the first choice due to their lower fixed rates and comprehensive benefits. Private loans should be considered only after exhausting federal options and only if the borrower or cosigner has strong credit to secure a competitive rate. Understanding the prevailing rates and terms of both federal and private loans is essential for making an informed decision that aligns with long-term financial goals.

Understanding New Zealand's Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Current Fixed vs. Variable Rates

As of the most recent data, the prevailing student loan interest rates vary depending on the type of loan—federal or private—and whether the rate is fixed or variable. For federal student loans, which are the most common, the interest rates are set by Congress and remain fixed for the life of the loan. For the 2023-2024 academic year, undergraduate students borrowing through the Direct Loan program face a fixed interest rate of 5.5%. Graduate students are offered a fixed rate of 7.05%, while PLUS loans, available to graduate students and parents, carry a fixed rate of 8.05%. These federal rates are determined annually and apply to new loans disbursed between July 1, 2023, and June 30, 2024.

In contrast, private student loans offer both fixed and variable interest rates, which can fluctuate based on market conditions. As of late 2023, fixed rates for private student loans typically range from 4.5% to 14%, depending on the borrower’s creditworthiness and the lender’s terms. Variable rates, on the other hand, generally start lower, ranging from 3.5% to 12%, but are tied to an index such as the Prime Rate or LIBOR, meaning they can increase over time if market interest rates rise. This makes variable rates riskier, as borrowers may face higher monthly payments in the future.

When comparing current fixed vs. variable rates, fixed rates provide stability and predictability, as the interest rate and monthly payments remain unchanged throughout the loan term. This is particularly advantageous in a rising interest rate environment, as borrowers are shielded from potential increases. Fixed rates are ideal for those who prefer budgeting certainty and want to avoid the uncertainty of fluctuating payments. However, fixed rates are often higher initially than variable rates, reflecting the lender’s assumption of interest rate risk.

Variable rates, while starting lower, carry inherent risk due to their potential to increase. Borrowers opting for variable rates should consider their tolerance for risk and the current economic climate. If interest rates are expected to remain stable or decrease, variable rates can save money over the life of the loan. However, in a period of rising rates, variable rates can lead to higher overall costs. It’s crucial for borrowers to assess their financial situation and future projections before choosing a variable rate.

For students and parents deciding between fixed and variable rates, it’s essential to weigh the pros and cons based on individual circumstances. Federal loans, with their fixed rates, offer a safe and predictable option, especially for those with limited credit history. Private loans provide more flexibility but require careful consideration of the borrower’s financial stability and market trends. Ultimately, the choice between fixed and variable rates should align with long-term financial goals and risk tolerance.

Understanding the Student Loan Interest Phaseout: What You Need to Know

You may want to see also

Explore related products

![]()

Undergraduate vs. Graduate Loan Rates

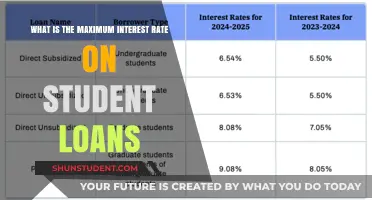

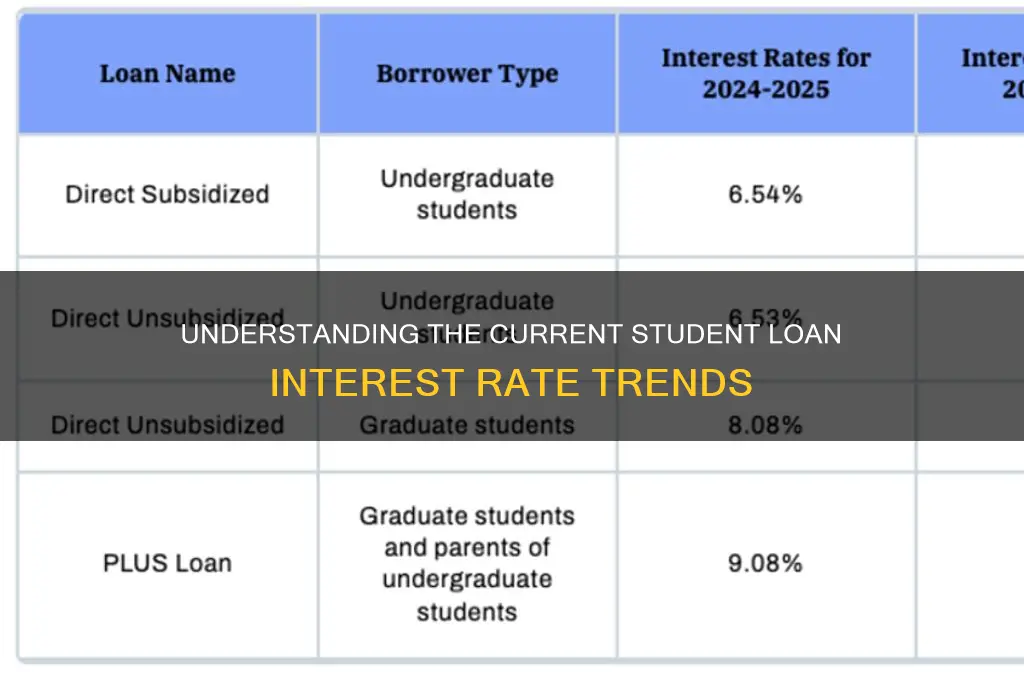

As of the most recent data, the prevailing student loan interest rates in the United States for the 2023-2024 academic year are set by the federal government. For federal student loans, the interest rates are fixed and determined annually based on the 10-year Treasury note index. For undergraduate students, the interest rate on Direct Subsidized and Unsubsidized Loans is 5.5% for the 2023-2024 academic year. In contrast, graduate students face a higher interest rate, with Direct Unsubsidized Loans set at 7.05% and Direct PLUS Loans, which are also available to graduate students, at 8.05%. These rates highlight a significant difference in borrowing costs between undergraduate and graduate students.

Undergraduate Loan Rates are generally lower to support students who are often borrowing for the first time and may have limited financial resources. The 5.5% interest rate for undergraduate Direct Subsidized and Unsubsidized Loans is designed to make higher education more accessible. Subsidized loans, in particular, offer additional benefits, as the government pays the interest while the borrower is in school at least half-time, during the grace period after leaving school, and during deferment periods. This feature is not available for graduate students, making undergraduate loans more advantageous in terms of interest accrual.

Graduate Loan Rates, on the other hand, are notably higher, reflecting the increased borrowing limits and extended repayment periods often associated with advanced degrees. The 7.05% rate for Direct Unsubsidized Loans and the 8.05% rate for Direct PLUS Loans mean that graduate students will accrue more interest over time, leading to higher overall repayment amounts. Graduate students also do not have access to subsidized loans, meaning interest begins accruing on unsubsidized loans as soon as the funds are disbursed. This difference underscores the importance of careful financial planning for graduate students.

The disparity in Undergraduate vs. Graduate Loan Rates can significantly impact long-term financial outcomes. For instance, a graduate student borrowing $50,000 at 7.05% will pay substantially more in interest over the life of the loan compared to an undergraduate student borrowing the same amount at 5.5%. Additionally, graduate students often borrow larger amounts due to higher tuition costs and living expenses, exacerbating the financial burden. As a result, graduate students may need to explore alternative financing options, such as scholarships, grants, or employer tuition assistance, to mitigate the higher costs associated with their loans.

Understanding the differences in Undergraduate vs. Graduate Loan Rates is crucial for borrowers to make informed decisions about their education financing. While federal student loans offer consistent terms and protections, such as income-driven repayment plans and loan forgiveness programs, the higher interest rates for graduate loans can make repayment more challenging. Prospective students should carefully consider their borrowing needs, explore all available financial aid options, and weigh the long-term implications of their loan choices. By doing so, they can minimize their debt burden and achieve their educational and career goals more sustainably.

Understanding the Maximum Interest Rates on Student Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Subsidized vs. Unsubsidized Loan Rates

As of the most recent data, the prevailing student loan interest rates in the United States for the 2023-2024 academic year are as follows: undergraduate federal Direct Subsidized and Unsubsidized Loans carry a fixed interest rate of 5.5%, while graduate Unsubsidized Loans are set at 7.05%. Direct PLUS Loans, available to graduate students and parents, have a higher rate of 8.05%. These rates are determined annually by the federal government and are based on the 10-year Treasury note yield, plus a fixed margin. Understanding the difference between Subsidized vs. Unsubsidized Loan Rates is crucial for borrowers, as it directly impacts the total cost of borrowing and repayment strategies.

Subsidized Loans are available only to undergraduate students with demonstrated financial need. The key advantage of these loans is that the federal government pays the interest while the borrower is in school at least half-time, during the grace period after leaving school (typically six months), and during any approved deferment periods. This means the loan balance does not increase during these times, making subsidized loans a more cost-effective option. The interest rate for subsidized loans is the same as unsubsidized loans for undergraduates (5.5% for 2023-2024), but the government’s interest coverage makes them significantly more favorable for eligible borrowers.

Unsubsidized Loans, on the other hand, are available to both undergraduate and graduate students, regardless of financial need. Unlike subsidized loans, the borrower is responsible for all interest that accrues on unsubsidized loans from the time the loan is disbursed. If the borrower chooses not to pay the interest while in school, during the grace period, or during deferment, the unpaid interest is capitalized, meaning it is added to the principal balance of the loan. This increases the total amount to be repaid over time. For undergraduates, the unsubsidized loan rate is 5.5%, while for graduate students, it jumps to 7.05%, reflecting the higher borrowing limits and longer repayment terms for advanced degrees.

The choice between subsidized and unsubsidized loans depends largely on the borrower’s financial situation and eligibility. Subsidized loans are ideal for undergraduate students with financial need, as they minimize long-term costs by avoiding interest capitalization. However, not all students qualify for subsidized loans due to federal eligibility requirements. Unsubsidized loans, while more widely available, require careful consideration of the long-term financial impact of accruing and capitalized interest. Borrowers should exhaust subsidized loan options before turning to unsubsidized loans to keep overall debt levels manageable.

In summary, while the interest rates for subsidized and unsubsidized loans may appear similar for undergraduates, the treatment of interest during periods of non-payment sets them apart. Subsidized loans offer a significant advantage by preventing interest from accruing while the borrower is in school or in deferment, whereas unsubsidized loans can lead to higher total repayment amounts due to capitalization. Graduate students, who are only eligible for unsubsidized loans, face even higher rates, underscoring the importance of strategic borrowing and exploring other financial aid options to minimize reliance on loans. Understanding these differences is essential for making informed decisions about student loan borrowing and repayment.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Explore related products

$16.53 $22.99

![]()

Historical Rate Trends and Changes

As of the most recent data available, the prevailing student loan interest rates in the United States for federal loans are as follows: undergraduate Direct Subsidized and Unsubsidized Loans have a fixed rate of 5.5% for the 2022-2023 academic year, while graduate/professional Direct Unsubsidized Loans are at 7.05%, and Direct PLUS Loans for parents and graduate students are at 8.05%. These rates are determined annually by the federal government, based on the 10-year Treasury note index, and remain fixed for the life of the loan. Private student loan interest rates, on the other hand, vary by lender and borrower creditworthiness, typically ranging from 3% to 12% or more, with both fixed and variable rate options available.

The historical trends in student loan interest rates reveal a pattern of fluctuations influenced by broader economic conditions and legislative actions. In the early 1990s, federal student loan rates were set by Congress and remained fixed at relatively high levels, with rates peaking at 8.25% for undergraduate loans in the 1994-1995 academic year. This era was characterized by a focus on deficit reduction, which led to higher borrowing costs for students. However, starting in the late 1990s and early 2000s, there was a shift toward variable interest rates tied to market conditions, with rates dropping significantly during periods of economic downturn, such as the early 2000s recession.

A major turning point came in 2006 with the passage of the College Cost Reduction and Access Act, which gradually lowered interest rates on subsidized loans for undergraduate students. By the 2011-2012 academic year, these rates had been reduced to 3.4%, though this lower rate was initially temporary and required periodic congressional extensions. In 2013, Congress allowed the rate to double to 6.8% before ultimately setting it at 4.29% for the 2014-2015 year as part of a broader overhaul. This legislation also transitioned all federal student loans to a fixed-rate model, eliminating variable rates and tying annual adjustments to the 10-year Treasury note.

The most recent decade has seen a steady but moderate increase in federal student loan interest rates, reflecting rising Treasury yields. For instance, undergraduate rates climbed from 3.76% in the 2016-2017 academic year to 5.5% in 2022-2023, while graduate and PLUS loan rates saw similar upward trends. These increases have sparked debates about the affordability of higher education, particularly as outstanding student loan debt surpassed $1.7 trillion. Meanwhile, private student loan rates have remained competitive, with variable rates often starting lower than federal rates but carrying the risk of future increases.

Legislative proposals and economic forecasts suggest that student loan interest rates may continue to evolve. For example, discussions around capping rates or implementing income-driven repayment plans could reshape the landscape. Additionally, the Federal Reserve’s monetary policy decisions, particularly regarding interest rates, will likely influence both federal and private loan rates. Borrowers are advised to monitor these trends closely, as historical patterns indicate that rates can shift significantly in response to economic and political developments. Understanding these changes is crucial for making informed decisions about financing education and managing loan repayment strategies.

Understanding the Latest Interest Rate Changes for Student Loans

You may want to see also

Frequently asked questions

The prevailing interest rates for federal student loans vary annually and are set by Congress based on the 10-year Treasury note. For the 2023-2024 academic year, rates range from 5.5% for undergraduate Direct Subsidized and Unsubsidized Loans to 8.05% for Grad PLUS and Parent PLUS Loans.

Private student loan interest rates are determined by lenders and are based on factors such as the borrower’s credit score, income, and repayment term. Rates can be fixed or variable, typically ranging from 3% to 14% or higher.

Yes, federal student loan interest rates are updated annually based on the yield of the 10-year Treasury note auctioned in May, plus a fixed margin set by Congress. New rates apply to loans disbursed from July 1 to June 30 of the following year.

Yes, options include refinancing with a private lender (if you qualify for a lower rate), enrolling in income-driven repayment plans (which may reduce monthly payments but not the interest rate), or taking advantage of lender discounts, such as autopay reductions.

Federal student loans have fixed interest rates set by the government, while private loans have rates determined by lenders and can be fixed or variable. Subsidized federal loans do not accrue interest while the borrower is in school, whereas unsubsidized and private loans typically do.