The student loan interest rate in the UK is a critical aspect of higher education financing, directly impacting the repayment terms for millions of graduates. As of recent updates, the interest rate is calculated based on the Retail Price Index (RPI) plus a margin, which varies depending on the borrower's income level and the plan type (e.g., Plan 1, Plan 2, or Plan 4). For instance, high earners may face rates significantly above RPI, while lower earners benefit from rates closer to or below it. Understanding these rates is essential for borrowers to manage their debt effectively, as they influence the total amount repaid over time. Regular reviews and adjustments by the government ensure the system remains responsive to economic conditions, though it often sparks debates about fairness and affordability for graduates.

Explore related products

What You'll Learn

![]()

Current UK Student Loan Interest Rates

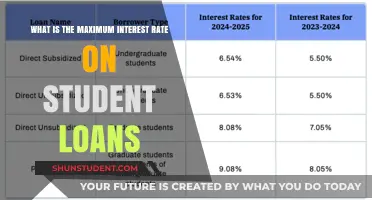

The current UK student loan interest rates are a critical aspect for borrowers to understand, as they directly impact the total amount to be repaid. As of the latest updates, the interest rates for student loans in the UK vary depending on the type of loan and the repayment plan. For Plan 1 loans, which are typically held by students who started their undergraduate courses before September 2012 in England or Wales, or those from Scotland and Northern Ireland, the interest rate is tied to the Retail Price Index (RPI) plus 1%. The RPI is a measure of inflation, and as of the most recent data, the interest rate for Plan 1 loans is RPI + 1%, which translates to a current rate of 4.5% (based on the March 2023 RPI figure of 3.5%).

For Plan 2 loans, which apply to most undergraduate students who started their courses on or after September 2012 in England or Wales, the interest rate is more complex. It is based on the RPI plus up to 3%, depending on the borrower’s income. While studying, the interest rate is RPI + 3%, and after graduation, it varies between RPI and RPI + 3%, depending on income. As of the latest figures, this means the interest rate for Plan 2 loans can range from 3.5% to 6.5%. This tiered system ensures that higher earners pay a higher interest rate, while lower earners benefit from a reduced rate.

Postgraduate loans in England and Wales also follow a similar structure to Plan 2 loans. The interest rate for these loans is RPI + 3%, which currently stands at 6.5%. This rate applies from the first day of the course until the loan is fully repaid. It’s important for postgraduate borrowers to factor this into their long-term financial planning, as the higher interest rate can significantly increase the total repayment amount over time.

For borrowers in Scotland, the interest rates differ slightly. Plan 4 loans, which apply to Scottish students studying in Scotland, have an interest rate of RPI + 0% while studying and RPI + 2.5% after graduation, depending on income. This means the current rate ranges from 3.5% to 6%. Similarly, Plan 5 loans in Northern Ireland have an interest rate of RPI + 0% while studying and RPI + 2.5% after graduation, mirroring the Scottish rates.

Understanding these rates is essential for effective financial management. Borrowers should regularly check for updates, as interest rates are reviewed annually in line with inflation figures. Additionally, it’s worth noting that interest is compounded monthly, meaning it is added to the loan balance each month. While student loan repayments are income-contingent and unpaid balances are written off after a certain period (typically 25–30 years), the interest accrual can still impact the overall debt burden. Staying informed about the current UK student loan interest rates is therefore a key step in managing student loan repayments efficiently.

Understanding the Refundable Student Loan Interest Amount: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Undergraduate vs. Postgraduate Loan Rates

In the UK, student loan interest rates vary depending on the type of loan, the repayment plan, and when the loan was taken out. When comparing Undergraduate vs. Postgraduate Loan Rates, it’s essential to understand the differences in how these loans are structured and the interest rates applied. Undergraduate loans, typically taken out for bachelor’s degrees, have different terms compared to postgraduate loans, which are often used for master’s or doctoral studies. As of the latest information, undergraduate loans generally have lower interest rates than postgraduate loans, but the specifics depend on the repayment plan and the year the loan was issued.

For Undergraduate Loans, the interest rate is tied to the Retail Price Index (RPI) plus up to 3%. For example, if the RPI is 3%, the interest rate could be as high as 6%. However, the actual rate applied depends on the borrower’s income. While studying, the interest rate is RPI plus 3%, but once the borrower starts repaying, the rate adjusts based on their income. If they earn below a certain threshold (e.g., £27,295 per year for Plan 2 loans), the interest rate is capped at RPI only. This means undergraduate loans are designed to be more affordable for lower-income earners, with interest rates that fluctuate but remain relatively manageable.

In contrast, Postgraduate Loans typically have higher interest rates. For Postgraduate Master’s Loans and Doctoral Loans, the interest rate is also linked to RPI but with an additional fixed percentage. As of recent data, the rate is RPI plus 3% while studying and RPI plus up to 3% after graduation, depending on income. However, postgraduate loans often accrue interest at a higher rate than undergraduate loans, especially for higher-income earners. This means borrowers with postgraduate loans may face steeper interest charges over time, particularly if they progress to higher-paying careers quickly.

Another key difference is the repayment threshold. For Undergraduate Loans, repayments typically begin once the borrower earns above a certain threshold, which varies by repayment plan (e.g., Plan 2 or Plan 1). For Postgraduate Loans, the repayment threshold is often lower, meaning borrowers may start repaying sooner, even if they are earning less. This, combined with higher interest rates, can make postgraduate loans more expensive in the long run compared to undergraduate loans.

In summary, when comparing Undergraduate vs. Postgraduate Loan Rates, undergraduate loans generally offer more favorable terms with lower interest rates and higher repayment thresholds. Postgraduate loans, while essential for advanced studies, come with higher interest rates and lower repayment thresholds, making them potentially more costly. Borrowers should carefully consider these differences when planning their finances for higher education, as the long-term impact of interest rates can significantly affect repayment amounts.

Understanding New Zealand's Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Interest Rate Calculation Methods

The UK student loan interest rate is a critical aspect of managing student debt, and understanding how it is calculated is essential for borrowers. As of the latest information, the interest rate for student loans in the UK is variable and depends on the type of loan and the borrower's circumstances. For example, Plan 2 loans (for students who started their course after 2012) have an interest rate based on the Retail Price Index (RPI) plus up to 3%, capped at a maximum rate. This means the interest rate can fluctuate annually, reflecting changes in the RPI.

Simple Interest Calculation is one method used to determine the interest accrued on student loans, though it is less common for long-term loans like student debt. Simple interest is calculated by multiplying the principal amount (the original loan) by the interest rate and the time period (usually in years). The formula is: *Simple Interest = P × r × t*, where *P* is the principal, *r* is the annual interest rate (as a decimal), and *t* is the time in years. For instance, if a student has a £10,000 loan at a 5% interest rate for one year, the simple interest would be £500.

Compound Interest Calculation is more commonly applied to UK student loans, particularly for Plan 2 loans. Compound interest calculates interest on the principal amount and any accumulated interest from previous periods. The formula for compound interest is: *A = P(1 + r/n)^(nt)*, where *A* is the amount after time *t*, *P* is the principal, *r* is the annual interest rate, *n* is the number of times interest is compounded per year, and *t* is the time in years. For student loans, interest is typically compounded monthly, meaning *n* would be 12. This method results in higher overall interest compared to simple interest, as the interest itself earns interest over time.

The RPI-Linked Calculation is specific to UK student loans and is a key feature of Plan 2 loans. Here, the interest rate is set as RPI (a measure of inflation) plus an additional percentage, usually up to 3%, depending on the borrower's income. For example, if RPI is 3% and the additional rate is 2%, the total interest rate would be 5%. This method ensures that the loan's value keeps pace with inflation, and the additional percentage is designed to reflect the borrower's ability to repay based on their income.

Another important aspect is the Income-Contingent Interest Rate Adjustment. For Plan 2 loans, the interest rate can vary based on the borrower's income. If the borrower's income is below a certain threshold (e.g., £27,295 as of 2023), the interest rate is capped at RPI only. Once income exceeds this threshold, the additional percentage is added, up to the maximum rate. This ensures that lower-earning graduates are not burdened with high-interest rates, making repayments more manageable.

Understanding these calculation methods is crucial for UK students and graduates to manage their loan repayments effectively. By knowing how interest accrues, borrowers can make informed decisions about their finances, such as considering overpayments when possible to reduce the overall interest paid over the life of the loan. Each method has its implications, and staying informed about annual rate changes and income thresholds is essential for long-term financial planning.

Understanding the Student Loan Interest Phaseout: What You Need to Know

You may want to see also

Explore related products

![]()

Historical Changes in UK Loan Rates

The UK student loan interest rate has undergone significant changes over the years, reflecting broader economic conditions and shifts in government policy. In the early 2000s, the interest rate for student loans was pegged to the Retail Price Index (RPI), a measure of inflation. This meant that the rate fluctuated annually based on changes in the RPI, typically ranging between 1% and 4%. For instance, in 2006, the interest rate was set at 2.4%, aligning with the RPI at the time. This period was characterized by relatively low and stable interest rates, which helped keep borrowing costs manageable for students.

A major shift occurred in 2012 when the UK government introduced a new system for student loans under Plan 2, applicable to students starting university in England and Wales from that year. Under this plan, the interest rate was no longer solely linked to RPI. Instead, it was set at RPI plus up to 3%, depending on the borrower’s income. This change meant that higher-earning graduates faced higher interest rates, while those earning less paid a lower rate. For example, in 2016, the interest rate for Plan 2 loans peaked at 6.3%, reflecting a high RPI and the additional 3% for higher earners. This marked a significant increase from the previous decade and sparked debates about the affordability of student debt.

In 2020, the UK government temporarily reduced the interest rate for Plan 2 loans to align with the RPI, capping it at 2.6% in response to the economic impact of the COVID-19 pandemic. However, this change was short-lived. By 2022, the interest rate had risen sharply again, reaching 7.3% in September 2022 due to soaring inflation. This increase was particularly controversial, as it significantly raised the cost of borrowing for millions of graduates. The government later announced a cap on the interest rate at 6.5% from March 2023, but this still left many borrowers facing higher costs than in previous years.

Historically, Plan 1 loans, which apply to students who began university before 2012, have had a more stable interest rate structure. These loans remain linked to the lower of RPI or the Bank of England base rate plus 1%. As a result, Plan 1 borrowers have generally faced lower interest rates compared to their Plan 2 counterparts. For example, in 2023, the Plan 1 interest rate was set at 3.4%, significantly lower than the 6.5% cap for Plan 2 loans. This disparity highlights the differing financial burdens faced by graduates depending on when they took out their loans.

Overall, the historical changes in UK student loan interest rates reflect a complex interplay between economic conditions, inflation, and government policy. From the RPI-linked rates of the early 2000s to the income-contingent system introduced in 2012, and the recent spikes due to high inflation, the landscape has evolved significantly. These changes have had profound implications for borrowers, influencing the total cost of repayment and the long-term financial health of graduates. Understanding these historical shifts is crucial for students and policymakers alike as they navigate the challenges of student debt in the UK.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Explore related products

$16.53 $22.99

![]()

Repayment Thresholds and Interest Impact

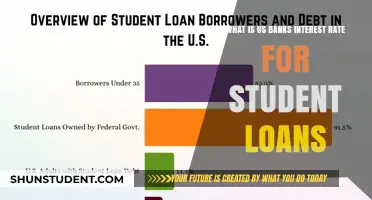

In the UK, student loan repayment thresholds play a crucial role in determining when and how much graduates need to repay, while interest rates influence the overall debt burden. As of recent updates, the repayment threshold for Plan 2 student loans (applicable to English and Welsh students who started university after 2012) is set at £27,295 per year, or £2,274 per month. For Plan 1 loans (older loans for students in the UK), the threshold is lower at £20,195 per year. Graduates only begin repaying their loans once their income exceeds these thresholds, with repayments calculated at 9% of the amount earned above the limit. Understanding these thresholds is essential, as they directly affect when repayments start and how much is deducted from your income.

The interest on UK student loans is tiered based on income and is designed to reflect the Retail Price Index (RPI) plus up to 3%, depending on earnings. For Plan 2 loans, while studying and until April after leaving the course, the interest rate is RPI + 3%. Once graduates start earning, the rate varies: it is RPI only for incomes up to £27,295, RPI + up to 3% for incomes between £27,295 and £49,130, and RPI + 3% for incomes above £49,130. This means that higher earners accrue interest at a faster rate, increasing the overall debt. However, it’s important to note that the interest is added to the loan balance rather than being charged upfront, and repayments are still based solely on income, not the total debt size.

The impact of interest on student loans can be significant, particularly for higher earners or those with larger loan balances. For example, a graduate earning £35,000 per year would accrue interest at RPI + up to 3%, depending on the exact RPI rate at the time. While repayments are fixed at 9% of income above the threshold, the growing interest means the total debt may increase over time, even as repayments are being made. This is a key consideration for borrowers, as it affects the long-term affordability of the loan and the likelihood of fully repaying it before the loan term ends (typically 30 years after the first repayment is due).

Repayment thresholds also have a direct impact on how quickly borrowers can clear their debt. For those earning just above the threshold, repayments will be minimal, and the interest accrued may outpace the repayment amount, causing the debt to grow. Conversely, higher earners will repay more each month but may still face increasing debt due to higher interest rates. Borrowers should regularly review their income and repayment amounts to understand how interest affects their loan balance. Tools like the Student Loan Repayment Calculator provided by the UK government can help estimate repayments and interest accrual based on current earnings.

Finally, it’s worth noting that not all borrowers will repay their student loans in full before the debt is written off after 30 years. For many, the combination of repayment thresholds and interest rates means the loan functions more like a graduate tax than a traditional loan. Lower earners may repay very little over their lifetime, while higher earners contribute more but may still not clear the debt entirely. Understanding these dynamics is crucial for financial planning, as it helps graduates make informed decisions about careers, savings, and other financial commitments in the context of their student loan obligations.

Understanding the Student Loan Interest Deduction on Your 1040 Form

You may want to see also

Frequently asked questions

The interest rate for undergraduate student loans in the UK is linked to the Retail Price Index (RPI) and varies depending on the plan type (e.g., Plan 1, Plan 2, Plan 4). As of 2023, the rate is typically RPI + up to 3%, but it is capped and reviewed annually.

The UK student loan interest rate is updated annually in September, based on the RPI from the previous March. This ensures the rate reflects current inflation trends.

Yes, postgraduate student loans in the UK have a different interest rate structure. As of 2023, the rate is typically RPI + 3%, but it may vary depending on the borrower's circumstances and repayment plan.

The interest begins accruing from the first day of your course, but repayment is only required once you earn above the repayment threshold (e.g., £27,295 for Plan 2 in 2023/24). The rate applies throughout the loan term, including during study and repayment periods.