Navigating the complexities of student loan interest rates can be overwhelming, and many borrowers turn to platforms like Reddit to seek advice, share experiences, and gain clarity. The question What is your student loan interest rate? frequently surfaces on Reddit threads, reflecting the widespread concern among borrowers about how much their loans are costing them over time. Discussions often delve into comparisons between federal and private loan rates, strategies for refinancing, and the impact of interest rates on long-term repayment plans. Reddit users exchange tips on how to lower interest rates, such as through consolidation or income-driven repayment plans, and share personal stories of managing high-interest debt. These conversations highlight the importance of understanding interest rates to make informed financial decisions and minimize the burden of student loans.

Explore related products

What You'll Learn

![]()

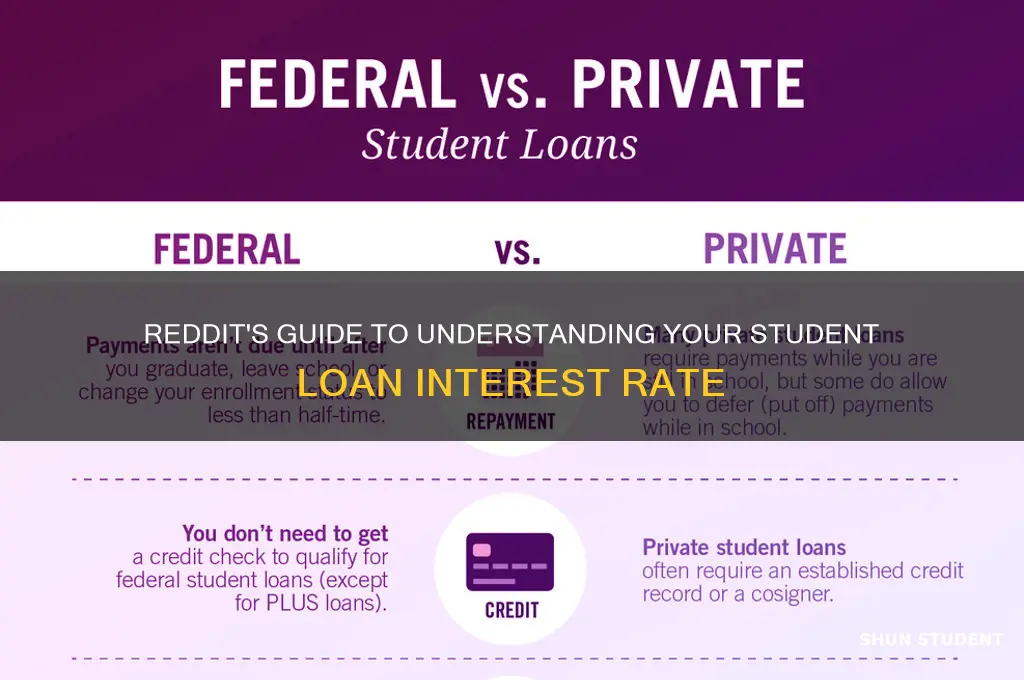

Federal vs. Private Rates

When comparing federal vs. private student loan interest rates, it’s essential to understand the fundamental differences in how these rates are determined and structured. Federal student loan interest rates are set by Congress and are standardized across all borrowers for a given academic year. These rates are fixed, meaning they remain the same for the life of the loan. For example, as of the most recent updates, undergraduate federal loans have a fixed interest rate, typically lower than private loan rates. Federal rates are also subsidized or unsubsidized, with subsidized loans offering the benefit of the government paying the interest while the borrower is in school or during deferment periods. This makes federal loans a more predictable and often more affordable option for many students.

On the other hand, private student loan interest rates are determined by lenders based on market conditions and the borrower’s creditworthiness. Unlike federal loans, private loan rates can be either fixed or variable. Variable rates may start lower but can fluctuate over time, potentially increasing the cost of the loan. Private lenders assess factors like credit score, income, and debt-to-income ratio to determine eligibility and rates. Borrowers with excellent credit may secure competitive rates, but those with poor or limited credit history often face higher rates or may need a cosigner. This variability makes private loans riskier and less predictable compared to federal options.

One of the most significant advantages of federal student loans is their borrower protections and repayment options. Federal loans offer income-driven repayment plans, which cap monthly payments based on income and family size, and loan forgiveness programs like Public Service Loan Forgiveness (PSLF). These benefits are not available with private loans, which typically have stricter repayment terms and fewer options for financial hardship. Additionally, federal loans provide deferment and forbearance options, allowing borrowers to pause payments temporarily without accruing interest on subsidized loans. Private loans rarely offer such flexibility, making them less forgiving in times of financial strain.

Reddit discussions often highlight the long-term cost implications of choosing between federal and private loans. Federal loans, with their fixed rates and borrower protections, are generally considered a safer choice, especially for borrowers unsure of their future financial stability. Private loans, while potentially offering lower rates for well-qualified borrowers, come with higher risks due to variable rates and limited repayment options. Many Redditors advise exhausting federal loan options before considering private loans, as federal rates are often more favorable and come with added security.

In summary, when evaluating federal vs. private student loan interest rates, borrowers should prioritize federal loans for their fixed rates, borrower protections, and repayment flexibility. Private loans may seem appealing for those with strong credit, but their variable rates and lack of safeguards make them a riskier choice. As Reddit users frequently emphasize, understanding these differences is crucial for making an informed decision that aligns with long-term financial goals. Always compare rates, terms, and benefits before committing to any student loan.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Fixed vs. Variable Rates

When considering student loan interest rates, one of the most critical decisions borrowers face is choosing between fixed and variable rates. This choice can significantly impact the total cost of your loan over time. Fixed rates remain the same throughout the life of the loan, providing predictability and stability. Variable rates, on the other hand, fluctuate based on market conditions, which means your monthly payments can increase or decrease over time. Understanding the pros and cons of each can help you make an informed decision tailored to your financial situation.

Fixed rates are often preferred by borrowers who value consistency and long-term planning. With a fixed rate, you know exactly how much interest you’ll pay each month, making it easier to budget. This is particularly beneficial in a rising interest rate environment, as your rate won’t increase even if market rates climb. However, fixed rates are typically higher than the initial rates offered for variable loans. If you prioritize peace of mind and want to avoid surprises, a fixed rate might be the better choice, especially if you plan to take several years to repay your loans.

Variable rates can be appealing because they often start lower than fixed rates, potentially saving you money in the short term. However, this comes with the risk of rate increases over time. Variable rates are tied to a benchmark index, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate, and adjust periodically based on changes in these indices. If interest rates rise, your monthly payments could increase, making it harder to manage your budget. Variable rates are best suited for borrowers who expect to pay off their loans quickly or who are confident that interest rates will remain stable or decline.

Reddit discussions often highlight the importance of considering your financial outlook when choosing between fixed and variable rates. For example, if you’re in a high-paying field and plan to aggressively pay down your loans, a variable rate might offer initial savings. However, if you’re in a field with uncertain income or prefer a set repayment plan, a fixed rate provides security. Many Redditors also advise monitoring economic trends and refinancing options, as you can switch from a variable to a fixed rate (or vice versa) if your circumstances change.

Ultimately, the decision between fixed and variable rates depends on your risk tolerance, financial stability, and repayment timeline. Fixed rates offer certainty and protection against rising interest rates, while variable rates can provide initial savings but come with the risk of increased costs. By carefully evaluating your situation and staying informed about market conditions, you can choose the option that best aligns with your goals and minimizes the long-term cost of your student loans.

Understanding the Latest Interest Rate Changes for Student Loans

You may want to see also

Explore related products

![]()

Refinancing Options

Refinancing your student loans can be a strategic move to secure a lower interest rate, reduce monthly payments, or simplify your finances by consolidating multiple loans into one. When considering refinancing options, it’s essential to evaluate your current interest rate against what lenders are offering. Many Reddit users share their experiences with refinancing, highlighting the importance of comparing rates from multiple lenders to ensure you’re getting the best deal. Platforms like SoFi, Earnest, Laurel Road, and CommonBond are frequently mentioned as popular choices for refinancing, each offering competitive rates based on creditworthiness and financial stability. Before applying, check your credit score, as a higher score can qualify you for lower interest rates.

One key aspect of refinancing is deciding between fixed and variable interest rates. Fixed rates remain the same over the life of the loan, providing predictability in monthly payments, while variable rates may start lower but can fluctuate with market conditions. Reddit discussions often caution against variable rates unless you plan to pay off the loan quickly, as rising interest rates could increase your overall cost. Additionally, consider the loan term—shorter terms typically come with lower interest rates but higher monthly payments, while longer terms reduce monthly payments but increase the total interest paid over time.

Another factor to weigh is whether to refinance federal student loans into a private loan. While refinancing can offer lower rates, federal loans come with benefits like income-driven repayment plans, loan forgiveness programs, and deferment or forbearance options. Reddit users often advise against giving up these protections unless you’re confident in your financial stability and don’t foresee needing federal loan benefits. If you decide to proceed, ensure the private lender’s terms align with your long-term financial goals.

Many lenders offer additional perks to attract borrowers, such as autopay discounts, career coaching, or referral bonuses. These incentives can slightly reduce your interest rate or provide added value. Reddit threads frequently emphasize the importance of reading the fine print to understand any fees, prepayment penalties, or hidden costs associated with refinancing. Some users also recommend using prequalification tools to estimate rates without impacting your credit score, allowing you to compare offers without commitment.

Lastly, timing is crucial when refinancing. Monitor interest rate trends and consider refinancing when rates are low. Reddit users often share success stories of locking in significantly lower rates during favorable market conditions. However, be mindful of application timelines, as refinancing can take several weeks to process. By carefully researching and comparing refinancing options, you can potentially save thousands of dollars over the life of your student loans and achieve greater financial flexibility.

Discovering New Horizons: The Most Fascinating Aspect of Student Life

You may want to see also

Explore related products

![]()

Interest Capitalization Explained

Interest capitalization is a critical concept to understand when managing student loans, as it directly impacts the total amount you’ll repay over the life of the loan. Simply put, interest capitalization occurs when unpaid interest is added to the principal balance of your loan. This means you’ll start accruing interest on a higher total amount, increasing the overall cost of your loan. For example, if your loan has a $10,000 principal and $500 in unpaid interest capitalizes, your new principal becomes $10,500, and future interest calculations will be based on this higher amount.

One common scenario where interest capitalization happens is during periods when interest is not being paid, such as during deferment, forbearance, or the grace period after graduation for certain types of loans (e.g., unsubsidized federal loans). During these times, interest continues to accrue but is not required to be paid. When the repayment period resumes, the unpaid interest is capitalized, increasing your loan balance. This is why it’s often recommended to pay at least the accruing interest during these periods if possible, as it can save you significant money in the long run.

Another instance where interest capitalization occurs is when you switch repayment plans or exit certain repayment statuses. For example, if you’ve been on an income-driven repayment plan and your payments haven’t covered the full interest accrual, the unpaid interest may capitalize when you switch plans or recertify your income. Similarly, if you’ve been in a deferment or forbearance and transition back to repayment, any unpaid interest will likely capitalize unless you pay it off beforehand.

To minimize the impact of interest capitalization, it’s essential to understand your loan terms and interest rate, as discussed in Reddit threads about student loan interest rates. Federal student loans typically have fixed interest rates, while private loans may have variable rates, which can fluctuate over time. Knowing your rate helps you calculate how much interest accrues daily and how quickly it can capitalize. For instance, a loan with a 6% interest rate will accrue interest faster than one with a 4% rate, making it even more critical to manage capitalization.

Finally, proactive strategies can help you avoid or reduce interest capitalization. Paying at least the monthly interest accrual during periods like deferment or forbearance prevents capitalization when repayment resumes. Additionally, making extra payments toward the principal balance reduces the amount of interest that can capitalize. If you’re unsure about your loan’s capitalization rules, contact your loan servicer for clarification. Understanding and managing interest capitalization is key to keeping your student loan debt under control and saving money over time.

Understanding Unpaid Interest on Student Loans: What Borrowers Need to Know

You may want to see also

Explore related products

$16.53 $22.99

$6.99

![]()

Reducing Interest Payments

Once you’ve identified your interest rates, refinancing is a popular strategy discussed on Reddit to reduce interest payments. Refinancing involves taking out a new loan with a lower interest rate to pay off your existing loans. This is particularly beneficial for private loans or if you have a high credit score and stable income. However, be cautious with federal loans, as refinancing them into private loans means losing access to federal protections like income-driven repayment plans and loan forgiveness programs. Reddit users often recommend comparing offers from multiple lenders to ensure you get the best rate.

Another effective method to reduce interest payments is making extra payments toward the principal balance. Even small additional payments can make a big difference over time. Focus on paying extra toward your highest-interest loans first, a strategy known as the avalanche method. This approach minimizes the total interest you’ll pay and shortens the life of your loans. Many Reddit users share success stories of paying off their loans years ahead of schedule by consistently making extra payments, even if they’re as little as $50 a month.

If refinancing isn’t an option, consolidating federal loans can sometimes lead to a lower interest rate. Direct Consolidation Loans for federal student loans calculate the weighted average of your current rates, rounded to the nearest one-eighth of a percent. While this may not drastically reduce your rate, it simplifies your payments by combining multiple loans into one. Reddit users often suggest consolidation for borrowers with multiple federal loans who want a single, manageable payment. However, avoid consolidating federal loans with private ones, as this could result in losing federal benefits.

Lastly, taking advantage of interest rate discounts offered by lenders can help reduce payments. Many loan servicers offer a 0.25% interest rate reduction for enrolling in autopay, which is a simple way to save money. Additionally, some lenders provide loyalty discounts or rate reductions after a certain number of on-time payments. Reddit users frequently highlight these discounts as easy wins that require minimal effort but yield long-term savings. Always review your loan terms to see if you qualify for any available discounts.

By combining these strategies—understanding your rates, refinancing, making extra payments, consolidating, and leveraging discounts—you can effectively reduce your student loan interest payments. Reddit communities often stress the importance of staying proactive and informed, as small changes can lead to substantial savings over the life of your loans.

Maximizing Tax Savings: Standard Deduction for Single Student Loan Interest

You may want to see also

Frequently asked questions

Reddit users report varying rates, but federal student loans typically range from 3.73% to 6.28% (as of recent years), while private loans can range from 3% to 14% or higher, depending on creditworthiness.

Reddit users suggest checking your loan servicer’s website, reviewing your loan agreement, or logging into your Federal Student Aid account (for federal loans) to find your exact interest rate.

Reddit users recommend refinancing with a private lender for a lower rate, enrolling in autopay for a small discount, or consolidating federal loans to simplify payments, though consolidation may not always lower rates.

Many Reddit users express frustration with private loan rates, lack of transparency, and the difficulty of refinancing due to credit requirements. Federal loan rates are also criticized for not adjusting to market changes.