Federal student loan forgiveness is a critical topic for millions of borrowers seeking relief from their educational debt. Programs like Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) forgiveness, and Teacher Loan Forgiveness offer pathways to debt elimination under specific conditions. PSLF forgives remaining balances after 120 qualifying payments for those working full-time in public service, while IDR plans forgive loans after 20–25 years of payments based on income. Additionally, recent initiatives, such as the limited PSLF waiver and one-time adjustments, have expanded eligibility for forgiveness. Understanding these programs and their requirements is essential for borrowers to maximize their chances of qualifying for loan forgiveness.

| Characteristics | Values |

|---|---|

| Public Service Loan Forgiveness (PSLF) | Forgiveness after 120 qualifying payments (10 years) while working full-time for a qualifying employer (government, non-profit, etc.). |

| Income-Driven Repayment (IDR) Forgiveness | Forgiveness after 20-25 years of qualifying payments, depending on the plan (e.g., PAYE, REPAYE, IBR, ICR). |

| Teacher Loan Forgiveness | Up to $17,500 in forgiveness for eligible teachers working in low-income schools for 5 consecutive years. |

| Disability Discharge | Full forgiveness for borrowers with a permanent disability, verified by the U.S. Department of Education. |

| Closed School Discharge | Forgiveness if the school closes while enrolled or shortly after withdrawal. |

| Borrower Defense to Repayment | Forgiveness if the school misled the borrower or violated certain laws. |

| Death or Bankruptcy Discharge | Forgiveness upon the borrower's death or in rare cases of bankruptcy. |

| Perkins Loan Cancellation | Up to 100% forgiveness for eligible professions (teachers, nurses, etc.) over 5 years. |

| Temporary Relief (e.g., COVID-19) | Paused payments and 0% interest during specific periods (e.g., COVID-19 pandemic). |

| Military Service Benefits | Forgiveness or repayment assistance for qualifying military service members. |

| Updated IDR Account Adjustment (2024) | One-time adjustment in 2024 to count past payments, including forbearance, toward IDR and PSLF forgiveness. |

Explore related products

What You'll Learn

![]()

Public Service Loan Forgiveness (PSLF) Program

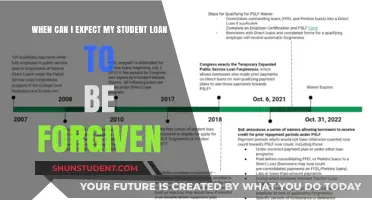

The Public Service Loan Forgiveness (PSLF) Program offers a pathway to debt relief for borrowers committed to a career in public service. Established in 2007, this federal initiative forgives the remaining balance on eligible federal student loans after the borrower has made 120 qualifying monthly payments while working full-time for a qualifying employer. Unlike income-driven repayment plans that forgive loans after 20–25 years, PSLF provides relief in as few as 10 years, making it a compelling option for those in eligible roles.

To qualify, borrowers must have Direct Loans or consolidate other federal loans into a Direct Consolidation Loan. Payments made under specific repayment plans, such as Standard, Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE), count toward the 120-payment requirement. Critically, the borrower must be employed full-time by a U.S. federal, state, local, or tribal government agency, a 501(c)(3) nonprofit organization, or another qualifying nonprofit that provides public services. Private employers do not qualify, even if the borrower’s role is public service-oriented.

One common pitfall is misunderstanding what constitutes a "qualifying payment." Payments must be made on time, in full, and while employed by a qualifying employer. Periods of deferment, forbearance, or economic hardship do not count. Borrowers should submit the Employment Certification Form annually or when changing jobs to ensure their payments are tracking correctly. This proactive approach helps avoid surprises, as the program has historically faced criticism for its complex requirements and low approval rates.

For those considering PSLF, strategic planning is essential. Borrowers should choose an income-driven repayment plan to minimize monthly payments, making it easier to manage debt while working in lower-paying public service roles. Additionally, consolidating loans early can simplify the process, as only Direct Loans qualify. While the program demands long-term commitment, the potential to eliminate tens of thousands of dollars in debt makes it a worthwhile pursuit for eligible individuals.

Finally, recent updates to PSLF, such as the Limited Waiver and Temporary Expanded Public Service Loan Forgiveness (TEPSLF), have broadened eligibility and addressed past administrative errors. These changes allow previously ineligible payments to count toward forgiveness, providing a second chance for borrowers who were mistakenly steered into the wrong loan type or repayment plan. Staying informed about such updates and consulting with a loan servicer can maximize the chances of successful forgiveness.

COVID-19 Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness Eligibility and Requirements

Teachers dedicated to serving in low-income schools can access a powerful tool for reducing their federal student loan burden: the Teacher Loan Forgiveness program. This initiative offers up to $17,500 in forgiveness for eligible Direct or FFEL Program loans after completing five consecutive, full-time academic years in a qualifying school.

Trump's Student Loan Forgiveness Plan: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

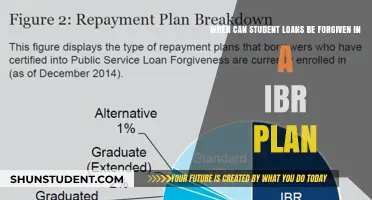

Income-Driven Repayment (IDR) Plan Forgiveness

Federal student loan borrowers often seek pathways to forgiveness, and one of the most accessible routes is through Income-Driven Repayment (IDR) plans. These plans tie monthly payments to income and family size, offering a lifeline to those with limited earnings. After 20 or 25 years of consistent payments, depending on the plan, the remaining balance is forgiven. This structure ensures that borrowers aren’t trapped in lifelong debt, especially if their careers don’t yield high salaries. For example, someone earning $40,000 annually with $60,000 in loans might pay as little as $150 per month under an IDR plan, with forgiveness kicking in after 25 years.

To qualify for IDR forgiveness, borrowers must choose from one of four plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), or Income-Contingent Repayment (ICR). Each plan has unique eligibility criteria and payment calculations. For instance, REPAYE caps payments at 10% of discretionary income and is available to all borrowers, while PAYE requires proof of partial financial hardship and limits payments to 10% of income. Borrowers should use the Federal Student Aid Loan Simulator to estimate payments and forgiveness timelines under each plan. Pro tip: Recertify income and family size annually to avoid payment spikes or disqualification.

A critical but often overlooked aspect of IDR forgiveness is tax implications. The forgiven amount is typically treated as taxable income, which could result in a hefty bill. For example, if $50,000 is forgiven, it might push a borrower into a higher tax bracket for that year. However, the American Rescue Act of 2021 temporarily exempts forgiven student loans from taxation through 2025, providing a window of relief. Borrowers should consult a tax professional to plan for potential liabilities post-2025. Additionally, tracking payment counts is essential, as servicer errors can delay forgiveness. Request an annual statement to verify progress.

IDR plans aren’t a one-size-fits-all solution. They’re ideal for borrowers with low-to-moderate incomes who anticipate long-term financial constraints. However, those with high earning potential might pay more over time due to interest capitalization. For instance, a borrower with $100,000 in loans and a starting salary of $50,000 could see their balance grow under ICR before forgiveness. Conversely, public service workers can combine IDR with Public Service Loan Forgiveness (PSLF) for faster relief after 10 years. The key is aligning the plan with career trajectory and financial goals.

Finally, persistence is paramount. IDR forgiveness requires two decades of commitment, during which life circumstances can change. Borrowers must stay informed about policy updates, such as the 2023 IDR Account Adjustment, which retroactively credited months toward forgiveness for certain borrowers. Automating payments and setting calendar reminders for recertification deadlines can prevent setbacks. While the journey is lengthy, IDR forgiveness offers a structured path to financial freedom for those who navigate it wisely.

Student Loan Forgiveness: Will It Impact Your Credit Score?

You may want to see also

Explore related products

![]()

Total and Permanent Disability (TPD) Discharge

Federal student loan borrowers facing total and permanent disability (TPD) may qualify for loan discharge, a provision designed to alleviate financial burden during severe hardship. This process, while compassionate, requires specific documentation and adherence to guidelines set by the U.S. Department of Education. To initiate a TPD discharge, borrowers must provide proof of their disability from one of three sources: the Social Security Administration (SSA), the U.S. Department of Veterans Affairs (VA), or a physician certified by the Department of Education. Each pathway has distinct requirements, ensuring that only those with verifiable, long-term disabilities receive relief.

For SSA beneficiaries, the process is relatively straightforward. If you’ve received a notice of award for Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) based on a finding that you are disabled, you can submit this documentation to apply for TPD discharge. The SSA must confirm that your disability is expected to last for at least 60 months or result in death. Borrowers can apply directly through the TPD discharge website, where they’ll grant permission for the Department of Education to access their SSA records. This automated process often leads to faster approval, typically within 3-4 months.

Veterans with service-connected disabilities face a slightly different process. The VA must certify that you are unemployable due to a service-connected disability, with a disability rating of 100% permanent and total. Submit your VA documentation, such as a benefits summary letter, to the TPD discharge servicer. This route acknowledges the unique challenges faced by disabled veterans, offering them a streamlined path to loan forgiveness. It’s a critical benefit for those who have sacrificed for their country and now face long-term health issues.

If you’re not receiving SSA or VA benefits, a physician’s certification is your alternative. A licensed doctor must complete a TPD discharge application form, confirming that you are unable to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously for at least 60 months or result in death. This method requires more effort but is essential for borrowers whose disabilities are recognized by medical professionals rather than federal agencies. Ensure your physician provides detailed, accurate information to avoid delays.

Once approved, TPD discharge offers immediate relief, but it comes with a three-year post-discharge monitoring period. During this time, you must meet certain conditions, such as not earning above the poverty guideline for your family size and not receiving a new federal student loan or TEACH Grant. Failure to comply may result in loan reinstatement. Additionally, discharged loans may be considered taxable income, though exceptions exist under the American Rescue Plan Act of 2021 for discharges through 2025. Understanding these nuances ensures you maximize the benefit without unexpected financial consequences.

Unlock Debt Relief: Strategies for Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Closed School Loan Discharge Process

If your school closes while you’re enrolled or shortly after you leave, you may qualify for a closed school discharge, wiping out 100% of your federal student loans tied to that institution. This process isn’t automatic—you must apply and meet specific criteria. First, confirm your eligibility: the school must have closed while you were enrolled, or within 120 days of your withdrawal, and you must not have already transferred credits to another institution. If you’re unsure about your status, contact your loan servicer or check the Federal Student Aid website for updates on closed schools.

The application process begins with submitting a closed school discharge request to your loan servicer. You’ll need to provide proof of enrollment dates, such as a transcript or enrollment verification form. If you’ve already made payments on the loans, keep records handy, as this could affect the outcome. Be proactive—some servicers may not volunteer information about this option, so it’s on you to initiate the process. If your initial request is denied, don’t give up; you can appeal by providing additional documentation or seeking assistance from the Federal Student Aid Ombudsman.

One common pitfall borrowers face is assuming they’re ineligible because they attended the school years before it closed. However, if you took out loans for a program that was cut short due to the closure, you may still qualify. For instance, if you were in a two-year program and the school closed after your first year, your loans for both years could be discharged. Another misconception is that borrowers who transferred credits are automatically disqualified. In reality, if the transferred credits didn’t result in a comparable degree or certification, you might still be eligible.

Comparing the closed school discharge to other forgiveness programs highlights its unique advantages. Unlike Public Service Loan Forgiveness, which requires 10 years of qualifying payments, or income-driven repayment plans, which forgive remaining balances after 20–25 years, the closed school discharge offers immediate relief without a waiting period. However, it’s narrower in scope—only borrowers affected by a school closure qualify. If you’re in this situation, act quickly, as delays could lead to unnecessary collections or credit damage.

Finally, consider the long-term impact of a successful discharge. Not only will your loan balance drop to zero, but any payments you made after the school’s closure may be refunded. Additionally, the discharge removes the debt from your credit report, improving your financial standing. For borrowers overwhelmed by the closure’s aftermath, this process offers a clear path to recovery. Stay informed, gather your documents, and take decisive action—your financial freedom could depend on it.

Seeking Public Forgiveness for Student Plus Loans: Is It Possible?

You may want to see also

Frequently asked questions

Federal student loans are forgiven under the PSLF program after 120 qualifying payments (10 years) while working full-time for a qualifying public service employer, such as government or nonprofit organizations.

Federal student loans are forgiven under IDR plans after 20–25 years of qualifying payments, depending on the specific plan. The remaining balance is forgiven, though it may be taxable as income.

Federal student loans are forgiven through the TPD discharge if the borrower has a permanent disability and provides documentation from the U.S. Department of Veterans Affairs, Social Security Administration, or a physician.

The SAVE Plan, replacing the REPAYE Plan, offers forgiveness after 10 years for balances under $12,000 (if all loans were for undergraduate study) and after 20–25 years for higher balances, depending on the loan type.