Federal student loan interest rates are not fixed indefinitely; they are subject to change annually, typically based on the 10-year Treasury note auction held each May. These rates apply to new loans disbursed between July 1 of the current year and June 30 of the following year. The U.S. Department of Education sets the interest rates for federal student loans by adding a fixed margin to the 10-year Treasury note yield, with the specific margin varying depending on the type of loan (e.g., Direct Subsidized, Unsubsidized, or PLUS loans). Borrowers should stay informed about these annual adjustments, as they can impact the total cost of their loans over time. Existing loans, however, are not affected by these changes, as their interest rates remain fixed for the life of the loan.

| Characteristics | Values |

|---|---|

| Frequency of Change | Annually |

| Effective Date | July 1st of each year |

| Determining Factor | High yield of the 10-year Treasury note at the last auction in May |

| Calculation Method | Treasury rate + fixed markup based on loan type |

| Loan Types Affected | Direct Subsidized, Direct Unsubsidized, Direct PLUS Loans |

| Fixed vs. Variable Rates | Fixed for the life of the loan (based on disbursement date) |

| Next Rate Change Announcement | Typically by June 1st each year |

| Current Rates (2023-2024) | Undergraduate: 5.5%, Graduate: 7.05%, PLUS Loans: 8.05% |

| Legal Basis | Higher Education Act of 1965, as amended |

| Impact on Existing Loans | Applies only to new loans disbursed after July 1st |

Explore related products

What You'll Learn

- Annual Interest Rate Updates: Rates adjust yearly based on 10-year Treasury note auction results

- Loan Type Variations: Rates differ for undergraduate, graduate, and parent PLUS loans

- Fixed vs. Variable Rates: New loans have fixed rates; older loans may have variable rates

- Rate Change Timing: New rates apply to loans disbursed after July 1 each year

- Historical Rate Trends: Rates fluctuate based on economic conditions and federal policies

![]()

Annual Interest Rate Updates: Rates adjust yearly based on 10-year Treasury note auction results

Federal student loan interest rates are not static; they undergo annual adjustments, a process directly tied to the performance of the 10-year Treasury note during a specific auction. This mechanism ensures that student loan rates reflect current economic conditions, particularly the government’s borrowing costs. The annual interest rate updates are a critical aspect of federal student loans, impacting borrowers’ repayment amounts and long-term financial planning. Understanding this process is essential for anyone managing federal student loan debt.

The adjustment process begins with the 10-year Treasury note auction, typically held in May each year. The yield, or return, on this Treasury note serves as the benchmark for determining federal student loan interest rates. Specifically, the rate is calculated by adding a fixed percentage (determined by Congress) to the 10-year Treasury note yield. For example, for undergraduate Direct Subsidized and Unsubsidized Loans, the fixed percentage is 2.05%, while for graduate Unsubsidized Loans, it is 3.60%. This formula ensures that student loan rates remain aligned with broader economic trends.

Once the 10-year Treasury note auction concludes, the U.S. Department of the Treasury announces the yield, and the U.S. Department of Education uses this figure to calculate the new interest rates. These updated rates apply to new federal student loans disbursed on or after July 1 of the same year and remain fixed for the life of the loan. It’s important to note that existing loans are not affected by these changes; their interest rates remain unchanged unless the borrower consolidates or refinances their loans.

The timing of these updates is consistent and predictable, allowing borrowers to anticipate changes. The new rates are finalized by the end of May and take effect on July 1, coinciding with the start of the federal government’s fiscal year. This schedule provides transparency and helps borrowers plan their finances accordingly. For instance, students and parents can estimate the cost of borrowing for the upcoming academic year based on the updated rates.

Borrowers should stay informed about these annual adjustments, as even small changes in interest rates can significantly impact the total cost of repayment over time. Resources such as the Federal Student Aid website provide up-to-date information on current and upcoming rates. Additionally, understanding the link between student loan rates and the 10-year Treasury note can help borrowers contextualize these changes within the broader economic landscape. By staying informed, borrowers can make more strategic decisions about their student loan management.

In summary, federal student loan interest rates are updated annually based on the results of the May 10-year Treasury note auction. This process ensures that rates reflect current economic conditions and government borrowing costs. The new rates take effect on July 1 and apply to loans disbursed after that date, while existing loans retain their original rates. Borrowers should monitor these updates to better plan their repayment strategies and understand the financial implications of their student loans.

Tracing the History of Student Loan Interest Caps: When Did They Begin?

You may want to see also

Explore related products

![]()

Loan Type Variations: Rates differ for undergraduate, graduate, and parent PLUS loans

Federal student loan interest rates are not uniform across all loan types; they vary significantly depending on whether the borrower is an undergraduate student, a graduate student, or a parent taking out a PLUS loan. These variations are important to understand, as they directly impact the cost of borrowing and repayment obligations. Undergraduate students typically receive the lowest interest rates among the three categories. For the 2023-2024 academic year, for instance, undergraduate Direct Subsidized and Unsubsidized Loans carried a fixed interest rate of 5.5%. This rate is set annually by Congress based on the 10-year Treasury note yield, plus a fixed markup, and applies to loans first disbursed between July 1 of the current year and June 30 of the following year.

Graduate students, on the other hand, face higher interest rates compared to undergraduates. For the same 2023-2024 period, Direct Unsubsidized Loans for graduate students had a fixed rate of 7.05%. This difference reflects the higher borrowing limits available to graduate students and the assumption that they have a greater ability to repay their loans due to advanced degrees often leading to higher earning potential. It’s crucial for graduate students to factor these higher rates into their financial planning, as they can significantly increase the total cost of their education over time.

Parent PLUS loans carry the highest interest rates among federal student loan options. For the 2023-2024 academic year, the rate for parent PLUS loans was set at 8.05%. These loans are designed for parents who are borrowing on behalf of their dependent undergraduate students. The higher rate is partly due to the fact that PLUS loans do not have borrowing limits tied to the student’s cost of attendance, and they also come with additional fees, such as an origination fee that is deducted from the loan amount before disbursement. Parents should carefully consider the long-term financial implications of these higher rates before taking out PLUS loans.

The timing of interest rate changes for these loan types is consistent across the board: new rates are set each year for loans first disbursed on or after July 1, based on the 10-year Treasury note auction held in May. However, the specific rate assigned to each loan type remains fixed for the life of the loan, meaning the rate at the time of disbursement does not change annually. Borrowers should stay informed about these annual adjustments, especially if they plan to take out multiple loans over several years, as each loan may carry a different interest rate depending on the year it was disbursed.

Understanding these loan type variations is essential for borrowers to make informed decisions about financing their education. Undergraduates benefit from the lowest rates, while graduate students and parents face progressively higher costs. By being aware of these differences and the annual rate-setting process, borrowers can better manage their debt and explore strategies to minimize interest expenses, such as paying off higher-rate loans first or considering refinancing options in the future.

Understanding Low Student Loan Interest Rates: What's Considered Favorable?

You may want to see also

Explore related products

![]()

Fixed vs. Variable Rates: New loans have fixed rates; older loans may have variable rates

Federal student loan interest rates can change based on the type of loan and when it was disbursed. Understanding the difference between fixed and variable rates is crucial for borrowers, especially when considering how these rates impact repayment over time. New federal student loans, such as Direct Loans disbursed after July 1, 2006, come with fixed interest rates. This means the rate remains the same for the life of the loan, providing predictability and stability for borrowers. Fixed rates are determined by federal law and are based on the 10-year Treasury note yield at the time of loan issuance, plus a margin set by Congress. For example, undergraduate Direct Subsidized and Unsubsidized Loans disbursed between July 1, 2023, and July 1, 2024, have a fixed rate of 5.5%.

In contrast, older federal student loans, particularly those from the Federal Family Education Loan (FFEL) Program, may have variable interest rates. These rates can fluctuate annually based on economic conditions, specifically changes in the 91-day Treasury bill rate. Variable rates are capped by federal regulations, but they introduce uncertainty for borrowers, as monthly payments can increase or decrease over time. For instance, FFEL loans disbursed before July 1, 2006, had variable rates that adjusted annually, though these loans are no longer issued. Borrowers with variable-rate loans should monitor interest rate changes to plan their finances effectively.

The shift from variable to fixed rates in federal student loans reflects a policy change aimed at simplifying repayment and reducing borrower risk. Since 2006, all new federal student loans have been issued with fixed rates, ensuring borrowers know exactly what their interest costs will be throughout the loan term. This change was driven by concerns that variable rates exposed borrowers to unpredictable payment increases, especially during periods of rising interest rates. As a result, newer borrowers benefit from greater financial clarity and stability.

For borrowers with older, variable-rate loans, consolidation can be a strategy to switch to a fixed rate. By consolidating FFEL loans into a Direct Consolidation Loan, borrowers can lock in a fixed interest rate based on the weighted average of their existing rates, rounded up to the nearest one-eighth of a percent. This can provide long-term savings and simplify repayment, especially if interest rates are expected to rise. However, consolidation may reset the clock on certain benefits, such as payment counts toward loan forgiveness programs, so borrowers should weigh the pros and cons carefully.

In summary, fixed rates apply to all new federal student loans, offering stability and predictability, while variable rates are a feature of older loans, particularly those from the FFEL Program. Understanding this distinction is essential for managing student loan debt effectively. Borrowers with variable-rate loans should stay informed about annual rate adjustments and consider consolidation to secure a fixed rate. As federal student loan interest rates change based on economic conditions and policy updates, staying informed about these dynamics can help borrowers make informed decisions about their repayment strategies.

Student Loans Without Interest: What You Need to Know

You may want to see also

Explore related products

![]()

Rate Change Timing: New rates apply to loans disbursed after July 1 each year

Federal student loan interest rates are not static; they are subject to annual adjustments, and understanding the timing of these changes is crucial for borrowers. The key date to remember is July 1, as this marks the threshold for when new interest rates take effect. Specifically, the updated rates apply to loans that are first disbursed on or after July 1 of each year. This means that if you are taking out a federal student loan, the interest rate you receive will depend on the timing of your loan disbursement relative to this date. For example, if your loan is disbursed on June 30, it will carry the previous year’s interest rate, but if it is disbursed on July 1 or later, the new rate will apply.

The annual rate change is tied to the yield on the 10-year Treasury note, which is determined by the federal government each spring through a formula set by Congress. Once the new rates are calculated, they remain fixed for the life of the loan, meaning they do not fluctuate with market conditions after disbursement. This predictability allows borrowers to plan their finances with a clear understanding of their loan costs. However, it also underscores the importance of being aware of the July 1 cutoff, as it directly impacts the interest rate you’ll pay over the long term.

For students and parents borrowing through federal programs like Direct Subsidized, Direct Unsubsidized, or PLUS loans, the July 1 deadline is particularly significant. If you anticipate needing loans for the upcoming academic year, knowing whether your disbursement will occur before or after this date can help you estimate your total borrowing costs. For instance, if rates are expected to increase, you might consider consolidating or taking out loans before July 1 to lock in the lower rate. Conversely, if rates are projected to decrease, waiting until after July 1 could save you money.

It’s also important to note that the July 1 rate change applies only to new loans disbursed after that date. Existing loans are not affected, as their interest rates are already fixed. This distinction is critical for borrowers who may have multiple loans with different disbursement dates. For example, if you have a loan from the previous year and take out an additional loan after July 1, the two loans will have different interest rates, which could influence your repayment strategy.

To stay informed about upcoming rate changes, borrowers should monitor announcements from the U.S. Department of Education, typically made in May or June each year. Additionally, financial aid offices at colleges and universities often provide updates and guidance on how the new rates may impact students. By being proactive and understanding the July 1 cutoff, borrowers can make informed decisions about their federal student loans and manage their debt more effectively.

When Did Student Loan Interest Rates Start Rising?

You may want to see also

Explore related products

$16.53 $22.99

![]()

Historical Rate Trends: Rates fluctuate based on economic conditions and federal policies

Federal student loan interest rates have historically been subject to fluctuations driven by broader economic conditions and shifts in federal policies. Since the introduction of the Federal Direct Loan Program in the 1990s, rates have been tied to the 10-year Treasury note yield, reflecting the government’s borrowing costs. During periods of economic stability or growth, such as the late 1990s and early 2000s, interest rates tended to rise as the Treasury yield increased, mirroring a stronger economy. Conversely, during economic downturns, like the 2008 financial crisis, rates decreased as the Federal Reserve lowered borrowing costs to stimulate economic activity. This linkage between Treasury yields and student loan rates underscores how macroeconomic trends directly influence borrowing costs for students.

Federal policies have also played a pivotal role in shaping interest rate trends. For instance, the Bipartisan Student Loan Certainty Act of 2013 established a new framework for setting rates, capping them based on the 10-year Treasury note plus a fixed margin, depending on the type of loan. This marked a shift from the previously fixed rates set by Congress, which were often criticized for being arbitrary. Additionally, in response to the COVID-19 pandemic, the federal government implemented a temporary 0% interest rate on most federal student loans, coupled with a pause on payments, to provide financial relief to borrowers. Such policy interventions highlight how legislative actions can override market-driven rate changes during crises.

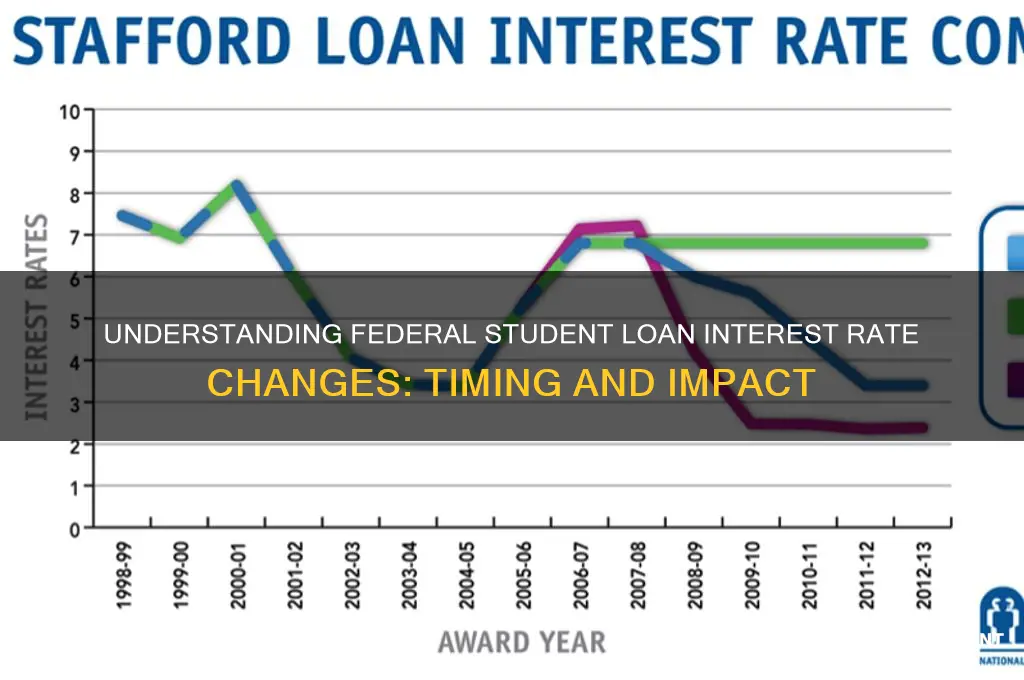

Historical data reveals distinct periods of rate increases and decreases. In the early 2000s, rates for undergraduate Stafford loans dropped to as low as 3.4% due to congressional action, but they later rose to 6.8% before the 2013 reforms. Following the 2013 act, rates became more volatile, reflecting Treasury yield movements. For example, rates for undergraduate loans climbed to 5.05% in 2018 but fell to 2.75% in 2020 amid the pandemic-induced economic slowdown. Graduate and PLUS loans followed similar patterns but at higher margins, illustrating how different loan types respond to the same economic and policy drivers.

Economic indicators, such as inflation and unemployment, have further influenced rate trends. High inflation typically leads to higher interest rates as lenders demand greater returns to compensate for eroding purchasing power. For instance, the inflationary period of the late 1970s and early 1980s saw student loan rates peak at over 9%. Conversely, low inflation and unemployment, as seen in the mid-2010s, contributed to relatively stable and lower rates. These dynamics emphasize the importance of monitoring economic indicators to predict future rate changes.

In summary, historical rate trends for federal student loans are a product of both economic conditions and federal policies. The interplay between Treasury yields, legislative actions, and macroeconomic factors has resulted in periods of both rising and falling rates. Borrowers must remain informed about these trends, as they directly impact the cost of education financing. Understanding this history provides valuable context for anticipating when and why federal student loan interest rates may change in the future.

Understanding When Student Loan Interest Rates Are Determined Annually

You may want to see also

Frequently asked questions

Federal student loan interest rates typically change annually, effective July 1, for new loans disbursed for the upcoming academic year.

Federal student loan interest rates are determined by the 10-year Treasury note auction in May, plus a fixed margin set by Congress based on the type of loan.

No, interest rates on existing federal student loans remain fixed for the life of the loan. Only new loans disbursed after July 1 are subject to the updated rates.

The new federal student loan interest rates are typically announced in May or June, following the 10-year Treasury note auction.

No, federal student loan interest rates do not change mid-academic year. They remain fixed for the entire academic year, with changes only applying to new loans disbursed after July 1.