The topic of when student loan interest started is a critical aspect of understanding the evolution of higher education financing in the United States. Student loan interest rates have a significant impact on borrowers, affecting the total cost of repayment and long-term financial planning. The history of student loan interest dates back to the 1960s, when the federal government first began offering subsidized loans to students. Over the years, interest rates have fluctuated in response to economic conditions, legislative changes, and shifts in federal policy. Key milestones include the introduction of variable interest rates in the 1990s, the switch to fixed rates in 2006, and subsequent adjustments under the Bipartisan Student Loan Certainty Act of 2013. Understanding these changes is essential for borrowers navigating the complexities of student loan repayment and for policymakers seeking to address the growing student debt crisis.

| Characteristics | Values |

|---|---|

| Student Loan Interest Resumption | September 1, 2023 (after a pause since March 2020 due to COVID-19) |

| Interest Accrual Restart | Interest began accruing again on federally held student loans starting September 1, 2023 |

| Payment Resumption | Payments resumed in October 2023 |

| COVID-19 Interest Freeze | March 13, 2020, to August 31, 2023 (0% interest during this period) |

| Current Interest Rates | Varies by loan type; for 2023-2024: Direct Subsidized/Unsubsidized (Undergrad): 5.5%, Direct Unsubsidized (Grad): 7.05%, Direct PLUS: 8.05% |

| Next Interest Rate Adjustment | July 1, 2024 (rates adjusted annually based on 10-year Treasury note) |

| Loan Forgiveness Updates | Ongoing legal challenges to the Biden administration's forgiveness plan; no widespread forgiveness as of October 2023 |

| Income-Driven Repayment Changes | New SAVE Plan (Saving on a Valuable Education) launched in 2023, offering lower payments and faster forgiveness |

Explore related products

What You'll Learn

![]()

Origins of Student Loan Interest Rates

The origins of student loan interest rates in the United States can be traced back to the mid-20th century, when the federal government began implementing programs to make higher education more accessible. The concept of student loans gained momentum with the passage of the National Defense Education Act (NDEA) in 1958, which was enacted in response to the Soviet Union's launch of Sputnik. This act provided low-interest loans to students pursuing degrees in science, mathematics, and foreign languages, setting an early precedent for government-backed student lending. The interest rates under the NDEA were subsidized to encourage students to enter fields deemed critical to national security, marking the first instance of federal involvement in setting student loan interest rates.

The next significant milestone came with the creation of the Federal Family Education Loan (FFEL) Program in 1965 as part of the Higher Education Act. This program expanded access to student loans beyond specific fields of study, allowing a broader range of students to borrow funds for college. Initially, interest rates under FFEL were set at a fixed rate, typically around 7-8%, and were subsidized by the federal government to keep borrowing costs manageable for students. The FFEL program laid the foundation for the modern student loan system, with interest rates serving as a mechanism to ensure repayment while keeping higher education affordable.

In 1993, the Direct Loan Program was introduced, shifting the responsibility for student loans directly to the federal government rather than private lenders. This program introduced variable interest rates tied to the cost of government borrowing, with rates initially set at 8% for subsidized loans and 9% for unsubsidized loans. The move to variable rates was intended to reflect market conditions and reduce costs for taxpayers. However, it also introduced uncertainty for borrowers, as their interest rates could fluctuate over the life of the loan.

A major turning point occurred in 2006 with the passage of the Deficit Reduction Act, which established fixed interest rates for federal student loans. Under this legislation, rates were set at 6.8% for subsidized Stafford loans and 8.5% for unsubsidized loans, effective July 1, 2006. This change aimed to simplify the loan structure and provide borrowers with predictable repayment terms. However, it also sparked debates about the fairness of fixed rates, particularly as market interest rates began to diverge significantly from the statutory rates.

The most recent evolution in student loan interest rates came with the Bipartisan Student Loan Certainty Act of 2013, which tied federal student loan rates to the 10-year Treasury note. Under this system, rates are adjusted annually based on market conditions, with caps to protect borrowers from excessive increases. For example, undergraduate subsidized and unsubsidized loans issued between July 1, 2023, and July 1, 2024, carry a rate of 5.5%, while graduate unsubsidized loans are at 7.05%, and PLUS loans are at 8.05%. This market-based approach reflects a shift toward aligning student loan rates with broader economic trends, though it continues to be a subject of debate regarding affordability and accessibility.

Throughout these developments, the origins of student loan interest rates highlight a balance between making higher education accessible and ensuring the sustainability of federal lending programs. From the fixed rates of the early programs to the market-driven rates of today, the evolution of student loan interest rates reflects changing economic priorities and policy goals. Understanding this history is crucial for addressing the ongoing challenges of student debt and the role of interest rates in shaping the financial futures of millions of borrowers.

Understanding Interest on Unsubsidized Student Loans: Costs and Repayment Strategies

You may want to see also

Explore related products

![]()

Historical Changes in Interest Rates

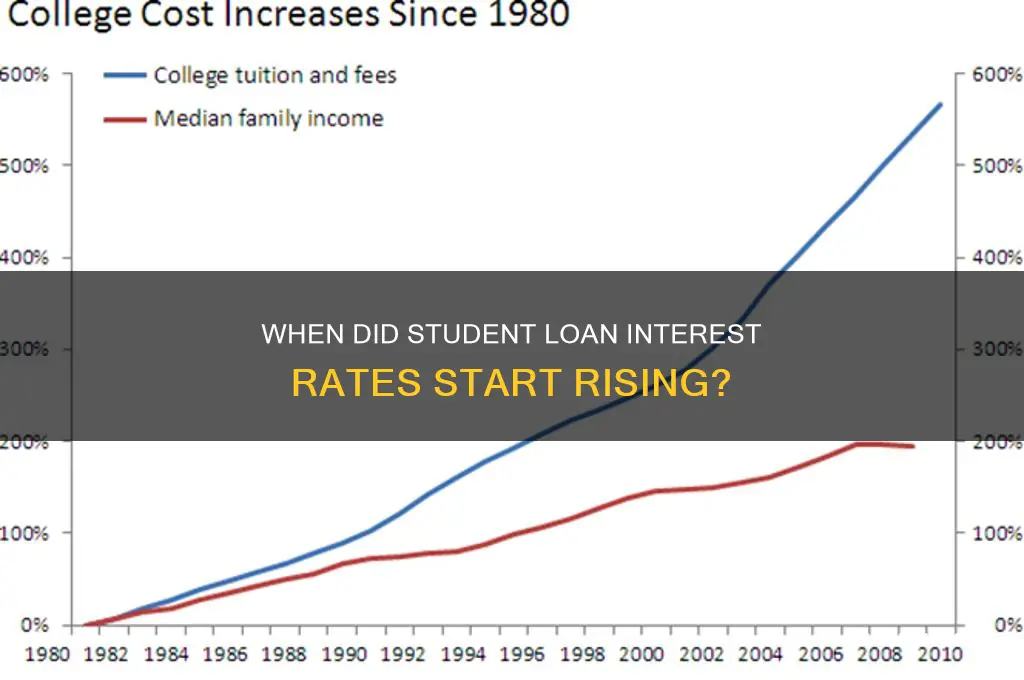

The history of student loan interest rates in the United States is marked by significant changes, influenced by economic conditions, legislative actions, and shifts in federal policy. Prior to the 1990s, student loan interest rates were largely fixed and set by Congress, often reflecting broader economic trends. For instance, in the 1980s, interest rates on federal student loans were relatively high, mirroring the prevailing high-interest-rate environment of that decade. However, these rates were not directly tied to market conditions, leading to occasional disparities between student loan rates and other borrowing costs.

A major shift occurred in the 1990s with the introduction of market-based interest rates for student loans. The Higher Education Amendments of 1992 allowed interest rates on new federal student loans to fluctuate annually, based on the cost of borrowing for the federal government, plus a small markup. This change aimed to make the student loan program more sustainable and responsive to economic conditions. For example, in the mid-1990s, as the economy stabilized and inflation declined, student loan interest rates dropped to around 6-8%, providing some relief to borrowers.

The 2000s saw further adjustments to student loan interest rates, driven by both legislative and economic factors. The College Cost Reduction and Access Act of 2007 gradually reduced interest rates on subsidized Stafford loans for undergraduate students, with rates scheduled to decrease from 6.8% to 3.4% over several years. However, this reduction was temporary, and rates were set to revert to 6.8% in 2012, sparking debates about affordability. Ultimately, the Bipartisan Student Loan Certainty Act of 2013 established a new framework, tying interest rates to the 10-year Treasury note, with additional markups based on the type of loan and borrower status.

Since 2013, student loan interest rates have been set annually based on this market-tied formula, resulting in rates that reflect broader economic conditions. For instance, during periods of low interest rates, such as in the late 2010s, student loan rates remained relatively low, with undergraduate borrowers paying around 3-5%. However, as inflation and Treasury yields rose in the early 2020s, student loan interest rates also increased, reaching levels not seen in over a decade. These changes underscore the ongoing impact of economic fluctuations on the cost of borrowing for education.

Throughout these historical changes, the debate over student loan interest rates has centered on balancing the need for sustainable federal lending programs with the goal of keeping higher education affordable. While market-based rates have introduced flexibility, they have also exposed borrowers to uncertainty, particularly during periods of rising interest rates. Understanding these historical shifts is crucial for policymakers and borrowers alike, as they navigate the complexities of student loan financing in an ever-changing economic landscape.

Understanding the Refundable Student Loan Interest Amount: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Impact of Economic Crises on Rates

Economic crises have historically had a profound impact on student loan interest rates, often leading to shifts in both federal and private lending policies. During times of economic downturn, governments and financial institutions typically adjust interest rates to stimulate economic activity or manage financial risks. For instance, the 2008 global financial crisis prompted the U.S. government to lower federal student loan interest rates to ease the financial burden on borrowers and encourage continued investment in education. This move was part of a broader strategy to stabilize the economy by ensuring that individuals could still access higher education despite widespread job losses and reduced household incomes.

The COVID-19 pandemic further exemplifies how economic crises influence student loan interest rates. In response to the pandemic-induced recession, the U.S. Department of Education suspended federal student loan interest accrual and payments in March 2020. This unprecedented action was aimed at providing immediate financial relief to borrowers facing unemployment or reduced income. The interest rate was effectively set to 0% for federal loans, a measure that remained in place for over three years. This policy not only alleviated financial stress for millions of borrowers but also highlighted the role of student loan interest rates as a tool for economic stabilization during crises.

Private student loan interest rates, on the other hand, are more directly tied to market conditions and lender risk assessments. During economic crises, private lenders often raise interest rates to compensate for increased default risks. For example, during the 2008 financial crisis, private student loan rates surged as lenders tightened credit standards and reduced loan availability. Borrowers with variable-rate loans were particularly vulnerable, as their interest rates fluctuated with market conditions, leading to higher monthly payments during an already challenging economic period.

Economic crises also influence legislative and policy changes related to student loan interest rates. In the aftermath of the Great Recession, the U.S. Congress passed the Health Care and Education Reconciliation Act of 2010, which eliminated subsidies for private lenders in the federal student loan program and set fixed interest rates based on market conditions. This reform aimed to reduce costs for borrowers and provide more predictable loan terms, reflecting lessons learned from the crisis. Similarly, discussions about widespread student loan forgiveness or interest rate caps gained momentum during the COVID-19 pandemic, underscoring the long-term impact of economic shocks on student loan policies.

In summary, economic crises significantly shape student loan interest rates through both immediate policy responses and long-term structural changes. Federal rates are often lowered or suspended to provide relief during downturns, while private rates may rise due to heightened risk. These adjustments reflect the dual goals of supporting individual borrowers and stabilizing the broader economy. Understanding these dynamics is crucial for borrowers navigating financial challenges and for policymakers designing effective responses to future crises.

2008 Student Loan Interest Rates: A Look Back at Borrowing Costs

You may want to see also

Explore related products

![]()

Government Policies Shaping Interest Rates

The role of government policies in shaping student loan interest rates is a critical aspect of higher education financing. Historically, student loan interest rates have been subject to legislative changes, reflecting broader economic goals and political priorities. One significant milestone occurred in 2013 when the Bipartisan Student Loan Certainty Act was signed into law. This act tied federal student loan interest rates to the 10-year Treasury note, a benchmark for government borrowing costs, plus a fixed markup. The goal was to create a market-based system that would ensure stability and predictability for borrowers while aligning with economic conditions. This policy shift marked a departure from fixed interest rates set by Congress, which had been in place since the inception of the federal student loan program.

Prior to 2013, student loan interest rates were often a point of contention, with rates fluctuating based on congressional decisions rather than market forces. For instance, the Higher Education Act of 1965 established subsidized loans with low fixed interest rates to make higher education more accessible. However, as budget concerns grew, policymakers began to adjust rates to manage federal spending. The College Cost Reduction and Access Act of 2007 gradually reduced interest rates on subsidized Stafford loans, culminating in a 3.4% rate for undergraduate borrowers by 2011. This rate, however, was temporary and required periodic extensions, leading to uncertainty for borrowers. The 2013 reform aimed to address this unpredictability by linking rates to market conditions, though it also eliminated subsidized loans for graduate students and capped the interest rate to prevent excessive increases.

Another key policy influencing student loan interest rates is the treatment of private loans versus federal loans. Federal loans typically offer lower, fixed interest rates and more flexible repayment options, such as income-driven repayment plans, which are designed to provide relief to borrowers facing financial hardship. In contrast, private loans often have variable interest rates tied to creditworthiness, making them riskier for borrowers. Government policies, such as the Federal Family Education Loan (FFEL) program, which ended in 2010, previously allowed private lenders to originate federal loans, blending public and private financing mechanisms. The shift to direct lending under the Department of Education streamlined the process and reduced costs, indirectly influencing the interest rate environment by minimizing the role of private lenders in federal loan programs.

In recent years, government policies have also focused on addressing the student debt crisis through interest rate adjustments and loan forgiveness initiatives. For example, the CARES Act of 2020 suspended federal student loan interest accrual and payments in response to the COVID-19 pandemic, providing immediate financial relief to millions of borrowers. This pause has been extended multiple times, reflecting the ongoing economic challenges faced by borrowers. Additionally, proposals to cap or reduce interest rates on existing loans have gained traction, with some advocating for a zero-interest policy to prevent loan balances from growing over time. These measures highlight the government's ability to use interest rate policies as a tool for both economic stimulus and social welfare.

Internationally, government policies on student loan interest rates vary widely, offering additional context for understanding U.S. approaches. Countries like Germany and Norway offer interest-free loans, while others, such as the UK, tie interest rates to inflation or income levels. These models demonstrate alternative strategies for balancing accessibility and sustainability in higher education financing. In the U.S., ongoing debates about interest rate policies often draw on these international examples, as policymakers seek to reform the system to better serve borrowers. Ultimately, government policies shaping student loan interest rates are deeply intertwined with broader goals of affordability, equity, and economic stability, making them a central issue in education policy discussions.

Understanding Student Loan Consolidation Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Comparison of Public vs. Private Loan Rates

When comparing public vs. private student loan interest rates, it’s essential to understand the historical context and current landscape of student loan interest rates. Public student loans, offered by the federal government, have historically provided lower and more stable interest rates compared to private loans. For instance, federal student loan interest rates are set by Congress and are typically fixed for the life of the loan. In contrast, private student loan rates are determined by lenders and are often variable, fluctuating based on market conditions and the borrower’s creditworthiness. This fundamental difference makes public loans a more predictable and often more affordable option for students.

One key factor in the comparison is the timeline of when student loan interest rates began to diverge between public and private sources. Federal student loan interest rates were standardized under the Federal Family Education Loan (FFEL) Program and later the Direct Loan Program, with rates set annually based on Treasury note yields. For example, in the early 2000s, federal student loan rates were as high as 6.8%, but they have since been adjusted to reflect economic conditions, often remaining below 5% for undergraduate loans. Private student loans, however, have historically carried higher rates, especially for borrowers with limited credit history or lower credit scores. This disparity highlights the advantage of public loans in terms of accessibility and cost.

Another critical aspect is the repayment flexibility associated with public vs. private loan rates. Federal student loans offer income-driven repayment plans, which cap monthly payments based on the borrower’s income and family size, and may even forgive remaining balances after a certain period. These benefits are not typically available with private loans, which often require fixed payments regardless of the borrower’s financial situation. Additionally, federal loans come with options for deferment and forbearance, providing temporary relief during financial hardship, whereas private lenders may offer limited or no such options. This flexibility further underscores the appeal of public loans over private ones.

Interest rate caps and subsidies also play a significant role in the comparison. Federal student loans often have statutory limits on how high interest rates can go, protecting borrowers from excessive costs. For example, undergraduate Direct Subsidized and Unsubsidized Loans have had rates capped at relatively low levels compared to private loans. Private lenders, on the other hand, may charge rates that exceed 10% or more, especially for high-risk borrowers. Furthermore, federal loans may offer subsidies, such as interest-free periods while the borrower is in school or during grace periods, which private loans rarely provide. These features make public loans a more financially prudent choice for many students.

Lastly, the long-term financial impact of choosing between public and private loan rates cannot be overstated. Over the life of a loan, even a small difference in interest rates can result in thousands of dollars in savings. For example, a federal loan with a 4.5% interest rate versus a private loan at 8% on a $30,000 balance could mean a difference of over $10,000 in total repayment. Additionally, the lack of prepayment penalties on federal loans allows borrowers to pay off their debt faster without extra fees, a benefit that may not apply to private loans. When considering "when did student loan interest rates stabilize," it’s clear that public loans have consistently offered more favorable terms, making them the preferred choice for most borrowers.

Unlocking Savings: Finding the Ideal Consolidated Student Loan Interest Rate

You may want to see also

Frequently asked questions

Student loan interest resumed accruing on September 1, 2023, following the end of the COVID-19 payment pause.

Federal student loan interest rates were last updated for loans disbursed between July 1, 2023, and June 30, 2024, based on the 10-year Treasury note auction in May 2023.

Interest capitalization stopped for borrowers in income-driven repayment plans as of July 1, 2023, under new federal regulations.

Federal student loan interest rates peaked in the early 1980s, with rates exceeding 10% for some loans.

Student loan interest became tax-deductible starting in the 1998 tax year, allowing borrowers to deduct up to $2,500 annually under certain conditions.