Student loan interest rates are typically set annually and are influenced by federal legislation and economic conditions. For federal student loans, rates are determined by Congress and are often tied to the yield on the 10-year Treasury note, with an additional fixed margin added to cover administrative costs. These rates are usually announced each spring and apply to new loans disbursed from July 1 of that year through June 30 of the following year. Private student loan interest rates, on the other hand, are set by individual lenders and are based on factors such as the borrower’s creditworthiness, market conditions, and the lender’s policies. Understanding when and how these rates are set is crucial for borrowers to make informed decisions about their student loan financing.

| Characteristics | Values |

|---|---|

| Frequency of Rate Setting | Annually |

| Timing | Rates are set each year by Congress, typically before July 1 |

| Effective Date | New rates apply to loans first disbursed on or after July 1 of that year |

| Basis for Rates | Tied to the 10-year Treasury note yield from the last auction in May |

| Rate Calculation | Treasury note yield + fixed markup based on loan type (e.g., Direct Subsidized, Unsubsidized, PLUS) |

| Fixed or Variable | Fixed for the life of the loan (rates do not change once set) |

| Loan Types Affected | Federal Direct Loans (Subsidized, Unsubsidized, PLUS, Consolidation) |

| Legislative Authority | Higher Education Act of 1965, as amended |

| Recent Rate Setting Year | 2023-2024 academic year rates were set in 2023 |

| Current Rate Range (2023-2024) | 5.5% (Direct Subsidized/Unsubsidized for Undergraduates) to 8.05% (PLUS Loans) |

Explore related products

What You'll Learn

![]()

Federal vs. Private Loan Rates

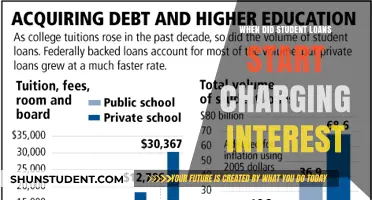

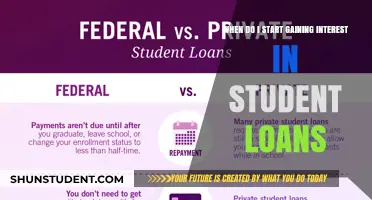

When comparing Federal vs. Private Loan Rates, it’s essential to understand how and when these rates are set, as they differ significantly in structure, timing, and borrower implications. Federal student loan interest rates are established by Congress and tied to the 10-year Treasury note, which is auctioned in May each year. These rates are fixed for the life of the loan and apply to all borrowers, regardless of credit history. For example, if the 10-year Treasury note yield is 3% in May, Congress adds a predetermined margin (e.g., 2.05% for undergraduate Direct Loans) to set the final rate. This process ensures transparency and consistency, with new rates taking effect for loans disbursed on or after July 1 of that year.

In contrast, private student loan rates are determined by individual lenders and are highly personalized, based on factors like credit score, income, and debt-to-income ratio. Unlike federal rates, private loan rates are not tied to a standardized benchmark and can vary widely across lenders. Additionally, private loans often offer both fixed and variable interest rates. Variable rates may fluctuate monthly or quarterly based on market indices like the Prime Rate or LIBOR, making them less predictable than federal rates. Borrowers with excellent credit may secure lower rates than federal options, but those with poor credit could face significantly higher costs.

The timing of rate-setting also differs between federal and private loans. Federal rates are updated annually, based on the May Treasury note auction, and remain fixed for loans disbursed within the subsequent academic year. Private lenders, however, can adjust their rates at any time in response to market conditions or changes in a borrower’s financial profile. This means borrowers shopping for private loans should compare offers carefully and consider how variable rates might impact their long-term repayment obligations.

Another critical distinction is the repayment terms associated with Federal vs. Private Loan Rates. Federal loans offer income-driven repayment plans, deferment, and forbearance options, which can provide flexibility during financial hardship. These benefits are not tied to the interest rate but are part of the federal loan program’s borrower protections. Private loans, on the other hand, rarely offer such accommodations, and repayment terms are strictly defined by the lender. While private loans might have lower rates for well-qualified borrowers, federal loans provide stability and safety nets that can outweigh higher rates for many students.

In summary, Federal vs. Private Loan Rates differ in how they are set, when they are determined, and the flexibility they offer. Federal rates are standardized, fixed, and tied to the 10-year Treasury note, with annual updates based on the May auction. Private rates are personalized, variable or fixed, and subject to lender discretion and market conditions. Borrowers should carefully weigh these differences, considering not only the rate itself but also the long-term implications of repayment terms and borrower protections.

Understanding Student Loan Interest: What Counts and Why It Matters

You may want to see also

Explore related products

![]()

Annual Interest Rate Adjustments

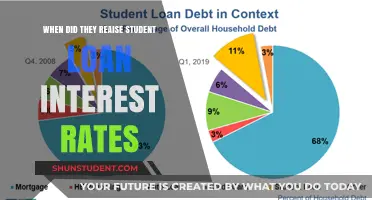

Student loan interest rates are not static; they are subject to annual adjustments, which can significantly impact borrowers' repayment plans. These adjustments are typically tied to the broader economic environment, specifically the performance of certain financial indices. Understanding when and how these rates are set is crucial for borrowers to anticipate changes in their loan costs. The process of setting these rates is standardized and follows a specific timeline, ensuring transparency and fairness for all parties involved.

The timeline for these adjustments is critical. The new interest rates are determined each spring and take effect for loans disbursed on or after July 1 of that year. For instance, the rates set in May 2023 would apply to loans disbursed between July 1, 2023, and June 30, 2024. This annual cycle allows borrowers to plan ahead, as they can anticipate the interest rates for the upcoming academic year. It also provides an opportunity for students and their families to make informed decisions about borrowing and financial planning.

Private student loans, on the other hand, may follow a different mechanism for interest rate adjustments. These rates are often tied to indices like the Prime Rate or LIBOR (London Interbank Offered Rate), and adjustments can occur more frequently, sometimes quarterly or even monthly. Private lenders typically disclose their rate adjustment policies in the loan agreement, and borrowers should carefully review these terms. Unlike federal loans, private loan rates are heavily influenced by the borrower's creditworthiness, which can lead to significant variations in interest rates among individuals.

Borrowers should stay informed about these annual adjustments to manage their student loan debt effectively. For federal loan borrowers, keeping an eye on the May Treasury note auction and subsequent announcements from the Department of Education is essential. Private loan borrowers should monitor the relevant financial indices and maintain a good credit score to secure the best possible rates. Understanding these processes empowers borrowers to navigate the complexities of student loan interest rates and make strategic financial decisions.

In summary, annual interest rate adjustments for student loans are a critical aspect of the borrowing process, influenced by economic indicators and specific timelines. Federal student loan rates are set based on the May 10-year Treasury note auction, ensuring a market-aligned approach, while private loans may follow different indices and adjustment frequencies. Borrowers must stay informed about these changes to effectively manage their loan repayments and overall financial health. This knowledge is particularly valuable for long-term financial planning and can help mitigate the impact of rising interest rates on student loan debt.

Understanding Typical Interest Rates for Private Student Loans

You may want to see also

Explore related products

![]()

Fixed vs. Variable Rate Loans

When considering student loans, one of the most critical decisions borrowers face is choosing between fixed-rate and variable-rate loans. This decision is closely tied to the timing of when student loan interest rates are set, as it determines how those rates will behave over the life of the loan. In the United States, federal student loan interest rates are set annually by Congress, based on the 10-year Treasury note yield, and take effect for loans disbursed between July 1 of one year and June 30 of the next. These rates are fixed for the life of the loan, meaning they remain unchanged regardless of market fluctuations. Private student loans, however, offer both fixed and variable rate options, and understanding the differences is essential for making an informed choice.

Fixed-rate loans provide stability and predictability. Once the interest rate is set at the time of loan disbursement, it remains the same throughout the repayment period. This makes budgeting easier, as monthly payments are consistent. For federal loans, the fixed rate is determined by the government and is not influenced by the borrower's creditworthiness. Private fixed-rate loans, on the other hand, may vary based on the borrower's credit history and other factors. The primary advantage of a fixed-rate loan is protection against rising interest rates. If market rates increase, the borrower's rate stays the same, potentially saving money over time. However, if market rates decrease, the borrower does not benefit from lower rates unless they refinance.

Variable-rate loans, in contrast, fluctuate over time based on an underlying index, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. These loans typically start with a lower interest rate than fixed-rate loans, making them initially more appealing. However, as market conditions change, the interest rate and monthly payments can increase or decrease. This introduces uncertainty into the repayment process, as borrowers may face higher costs if rates rise. Variable-rate loans are often chosen when interest rates are expected to remain stable or decline, but they carry the risk of becoming more expensive in a rising-rate environment. Private lenders usually offer variable-rate loans, and the initial rate may be tied to the borrower's credit profile.

The timing of when student loan interest rates are set plays a significant role in the fixed vs. variable rate decision. For federal loans, since rates are fixed annually and remain unchanged, borrowers have clarity about their long-term costs. For private loans, the decision depends on market conditions at the time of borrowing. If rates are historically low, a variable-rate loan might seem attractive, but borrowers must consider the potential for future increases. Conversely, in a low-rate environment, locking in a fixed rate can provide peace of mind, even if it means missing out on potential savings if rates fall further.

Ultimately, the choice between fixed and variable rate loans depends on the borrower's risk tolerance, financial situation, and outlook on interest rate trends. Fixed-rate loans are ideal for those who prioritize predictability and want to avoid the risk of rising rates. Variable-rate loans may suit borrowers who are comfortable with uncertainty and believe rates will remain stable or decline. When student loan interest rates are set—whether annually for federal loans or at the time of application for private loans—borrowers should carefully evaluate their options and consider consulting financial advisors to make the best decision for their circumstances.

Understanding Typical Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Congressional Role in Rate Setting

The role of Congress in setting student loan interest rates is a critical aspect of the broader policy framework governing federal student loans. Unlike private loans, where interest rates are determined by market forces and individual creditworthiness, federal student loan rates are established through legislative action. This process ensures that student loan interest rates align with national educational goals, economic conditions, and fiscal priorities. Congress typically sets these rates through the Higher Education Act (HEA), which is periodically reauthorized and amended to reflect changing needs and circumstances.

Congressional involvement in rate setting is rooted in the need to balance affordability for borrowers with the cost to taxpayers. Federal student loans are subsidized by the government, meaning that interest rates are often lower than those offered by private lenders. When Congress sets these rates, it considers factors such as the cost of government borrowing, inflation, and the financial health of the student loan program. For instance, the Bipartisan Student Loan Certainty Act of 2013 tied federal student loan interest rates to the 10-year Treasury note, plus a fixed margin, to ensure rates remain market-based while providing stability for borrowers.

The timing of rate setting is also a key consideration. Historically, Congress has adjusted student loan interest rates during the reauthorization of the HEA or through standalone legislation. For example, the HEA was last reauthorized in 2008, and subsequent changes to interest rates have been made through acts like the Health Care and Education Reconciliation Act of 2010 and the Bipartisan Student Loan Certainty Act of 2013. These adjustments often coincide with broader debates about higher education funding, affordability, and accessibility, reflecting Congress’s role in shaping education policy.

Another important aspect of Congress’s role is its oversight of the student loan program. Committees such as the House Committee on Education and Labor and the Senate Committee on Health, Education, Labor, and Pensions (HELP) play a pivotal role in reviewing the performance of the program, assessing the impact of current interest rates, and proposing changes. Hearings, reports, and legislative proposals are tools Congress uses to ensure that interest rates remain fair and sustainable for both borrowers and taxpayers.

Finally, Congress’s decisions on student loan interest rates are influenced by political and economic pressures. Advocacy groups, student organizations, and policymakers often push for lower rates to alleviate the burden of student debt, while fiscal conservatives may argue for rates that minimize the cost to the federal budget. This dynamic underscores the complexity of Congress’s role, as it must navigate competing priorities to arrive at a consensus. Ultimately, the congressional process ensures that student loan interest rates are not set arbitrarily but are the result of deliberate, informed policymaking.

Deducting Student Loan Interest: Finding the Right Line on Form 1040

You may want to see also

Explore related products

$16.53 $22.99

![]()

Economic Indicators Impacting Rates

Student loan interest rates are not arbitrarily determined; they are influenced by a variety of economic indicators that reflect the broader financial health and conditions of the economy. These indicators play a crucial role in setting both federal and private student loan interest rates, ensuring that they align with prevailing market conditions. Understanding these economic factors can provide borrowers with insights into why rates fluctuate and what might influence future changes.

One of the most significant economic indicators impacting student loan interest rates is the 10-year Treasury note yield. Federal student loan rates, for instance, are directly tied to the yield of the 10-year Treasury note, which is determined at the annual auction held in May. This yield reflects investor expectations of future inflation, economic growth, and monetary policy. When the Treasury yield rises, student loan interest rates typically follow suit, as lenders adjust to higher borrowing costs in the broader market. Conversely, a decrease in the Treasury yield often leads to lower student loan rates.

Inflation is another critical factor that influences student loan interest rates. As inflation rises, lenders demand higher interest rates to compensate for the eroding purchasing power of future repayments. Central banks, such as the Federal Reserve, often respond to inflationary pressures by raising benchmark interest rates, which in turn affects the cost of borrowing across the economy, including student loans. Borrowers should monitor inflation trends, as persistent inflationary pressures can lead to sustained increases in student loan rates.

Unemployment rates and overall economic growth also play a role in determining student loan interest rates. During periods of high unemployment or economic downturn, lenders may lower interest rates to stimulate borrowing and support economic activity. Conversely, in a strong economy with low unemployment, lenders may raise rates to manage risk and capitalize on favorable conditions. Economic growth indicators, such as GDP growth rates, provide lenders with insights into the financial stability of borrowers and the likelihood of timely repayments.

Lastly, monetary policy decisions by central banks, particularly the Federal Reserve in the United States, have a direct impact on student loan interest rates. When the Fed adjusts the federal funds rate, it influences the cost of credit across the economy. For example, if the Fed raises rates to curb inflation or cool an overheating economy, student loan rates are likely to increase as well. Borrowers should stay informed about Fed announcements and policy shifts, as these decisions can have immediate and long-term effects on borrowing costs.

In summary, student loan interest rates are shaped by a complex interplay of economic indicators, including Treasury yields, inflation, unemployment rates, economic growth, and monetary policy. By keeping an eye on these factors, borrowers can better anticipate changes in student loan rates and make informed decisions about their educational financing. Understanding these dynamics is essential for navigating the student loan landscape and managing debt effectively.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Frequently asked questions

Federal student loan interest rates are set annually on July 1, based on the 10-year Treasury note auction held in May of the same year.

No, private student loan interest rates are set by individual lenders and can vary at any time based on market conditions, creditworthiness, and other factors.

For most federal student loans, the interest rate is fixed for the life of the loan and does not change after it is set at disbursement.

Federal student loan interest rates are generally fixed, but Congress can pass legislation to change rates for future borrowers. Existing loans are not affected unless refinanced.