In the UK, the timing of when student loans start accruing interest depends on the type of loan and the repayment plan. For most undergraduate students, interest begins to accrue from the day the first payment is made, typically at a rate linked to the Retail Price Index (RPI) plus up to 3%. However, for students on income-contingent repayment plans, such as Plan 2 (England and Wales) or Plan 4 (Northern Ireland), interest is calculated daily but only becomes repayable once the borrower’s income exceeds a certain threshold. Postgraduate loans, on the other hand, accrue interest from the first day of the course, usually at RPI plus 3%. Understanding these nuances is crucial for borrowers to manage their loan repayments effectively and plan their finances accordingly.

| Characteristics | Values |

|---|---|

| Interest Accrual Start Date | Interest accrues from the date the first payment is made to the student or on behalf of the student (e.g., tuition fees, maintenance loan). |

| Interest Rate (Plan 2 & Plan 3) | Linked to the Retail Price Index (RPI) plus up to 3%, depending on income. As of April 2023, rates range from 2.6% (for incomes up to £27,295) to 6.1% (for incomes above £49,130). |

| Interest Rate (Plan 1) | Fixed at RPI + 1%, currently 6.1% (from September 2023). |

| Interest During Study | Interest accrues while studying. |

| Repayment Threshold (Plan 2 & Plan 3) | Repayments begin when income exceeds £27,295 per year (from April 2023). |

| Repayment Threshold (Plan 1) | Repayments begin when income exceeds £20,195 per year (from April 2023). |

| Interest Capitalization | Interest is added to the loan balance monthly but is not compounded. |

| Loan Written Off | After 30 years (Plan 2 & Plan 3) or 25 years (Plan 1) from the April after graduation, any remaining balance is written off. |

| Inflation Adjustment | Repayment thresholds and interest rates are adjusted annually based on inflation (RPI). |

| Overseas Interest Rates | Different rates apply if the borrower moves overseas; rates vary based on the country of residence. |

| Postgraduate Loans | Interest accrues at RPI + 3% from the date the loan is taken out. |

| Repayment Method | Repayments are deducted automatically via PAYE or self-assessment tax returns. |

Explore related products

What You'll Learn

- Interest Start Dates: When does interest begin on UK student loans after graduation

- Repayment Thresholds: At what income level do repayments and interest apply

- Study Period Interest: Does interest accrue while still studying in the UK

- Loan Types Comparison: Differences in interest accrual between Plan 1 and Plan 2 loans

- Post-Graduation Grace Period: Is there a delay before interest starts after leaving university

![]()

Interest Start Dates: When does interest begin on UK student loans after graduation?

In the UK, the interest on student loans typically begins accruing immediately after the first payment is made, but the specific details can vary depending on the type of loan and the repayment plan. For most students, the interest start date is closely tied to their graduation or the end of their course. Understanding when interest begins to accrue is crucial for managing loan repayments effectively.

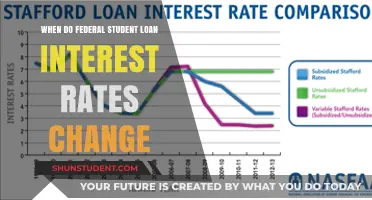

For Plan 1 loans, which are available to students from England and Wales who started their undergraduate courses before 1 September 2012, interest starts accruing from the day the first loan payment is made. However, the repayment of the loan itself only begins once the borrower’s income exceeds the repayment threshold, which is currently set at £19,895 per year. The interest rate for Plan 1 loans is linked to the Retail Price Index (RPI) and can fluctuate annually, but it is capped at a maximum rate.

Plan 2 loans, applicable to English and Welsh students who began their undergraduate courses on or after 1 September 2012, also start accruing interest from the first payment date. Repayments begin when the borrower’s income surpasses the threshold, which is currently £27,295 per year. The interest rate for Plan 2 loans is based on the RPI plus up to 3%, depending on income. This means that higher earners may face higher interest rates, though the rate is capped to prevent excessive charges.

For students from Scotland, the interest on student loans begins accruing from the April after graduation or leaving the course. Repayments typically start in the April following graduation, provided the borrower’s income exceeds the threshold, which is currently £25,000 per year. The interest rate is tied to the RPI, ensuring it remains in line with inflation.

In Northern Ireland, the rules are similar to Plan 1 loans in England and Wales. Interest begins accruing from the first payment date, and repayments start once the borrower’s income exceeds the threshold, which is currently £19,895 per year. The interest rate is linked to the RPI, with a cap to protect borrowers from excessively high rates.

It’s important for graduates to be aware of these interest start dates, as they directly impact the total amount repayable over the life of the loan. Early repayment strategies, such as making voluntary payments when financially feasible, can help reduce the overall interest accrued. Additionally, staying informed about annual changes to interest rates and repayment thresholds is essential for effective loan management.

Understanding Student Loan Interest Rates: A Comprehensive Guide for Borrowers

You may want to see also

Explore related products

![]()

Repayment Thresholds: At what income level do repayments and interest apply?

In the UK, the repayment thresholds for student loans are a crucial aspect of understanding when and how interest accrues. For most students who took out loans after 2012, the repayment threshold is set at an annual income of £27,295 (as of April 2023). This means that if you earn below this threshold, you are not required to make any repayments, but interest will still accrue on your loan balance. The interest rate is typically linked to the Retail Price Index (RPI) and can vary depending on your income level and the type of loan you have.

Once your income exceeds the repayment threshold, you are obligated to start making repayments. These repayments are calculated as a percentage of your income above the threshold, currently set at 9%. For example, if you earn £30,000 annually, your repayment amount would be 9% of the difference between £30,000 and £27,295, which is £2,705. This means you would repay £243.45 per year, or approximately £20.29 per month. It’s important to note that repayments are automatically deducted through the tax system, so you don’t need to actively manage them.

Interest on student loans begins accruing from the day you receive your first payment. For loans taken out after 2012, the interest rate is RPI plus up to 3%, depending on your income. If you earn below the repayment threshold, the interest rate is RPI only. Once you earn above the threshold, the interest rate increases progressively, reaching RPI + 3% for incomes above £49,130. This tiered interest system means that higher earners pay a higher rate of interest, which can significantly impact the overall cost of the loan over time.

For students who took out loans before 2012, the repayment threshold and interest rates differ. The threshold for Plan 1 loans (taken out before 2012) is currently £20,195, with repayments calculated at 9% of income above this level. The interest rate for Plan 1 loans is fixed at RPI or the Bank of England base rate plus 1%, whichever is lower. Understanding which plan your loan falls under is essential, as it directly affects when and how much interest accrues and when repayments begin.

It’s also worth noting that unpaid student loan balances are written off after a certain period, typically 30 years after the first repayment was due. This means that if you never earn above the repayment threshold, you may not repay the full loan amount, and the remaining balance will be forgiven. However, interest continues to accrue until the loan is fully repaid or written off, making it important to monitor your income and understand how it impacts your loan obligations. Always check the latest figures and rules from official sources, as thresholds and interest rates can change annually.

When Did Student Loans Switch to Compounding Interest?

You may want to see also

Explore related products

![]()

Study Period Interest: Does interest accrue while still studying in the UK?

In the UK, student loans do begin to accrue interest from the day the first payment is made to the student or their university, even while the borrower is still studying. This means that interest starts accumulating during the study period, which is an important consideration for students planning their finances. The interest rate applied to student loans in the UK is not fixed and can vary depending on the type of loan and the borrower's circumstances. For most students, the interest rate is based on the Retail Price Index (RPI) and is updated annually in line with inflation.

During the study period, the interest accrual process is relatively straightforward. For loans taken out after 2012, the interest rate is set at RPI plus 3% while the student is studying. This rate applies to both the tuition fee loan and the maintenance loan. For example, if the RPI is 2%, the interest rate on the student loan would be 5% during the study period. It's worth noting that the interest is added to the total loan balance, increasing the overall amount to be repaid after graduation.

The fact that interest accrues during the study period can significantly impact the total cost of the loan. As the interest is compounded, it can lead to a substantial increase in the loan balance over time. For instance, a student borrowing £9,000 per year for a three-year degree could accumulate several thousand pounds in interest by the time they graduate, depending on the interest rate and the duration of their course. This highlights the importance of understanding the interest accrual process and considering strategies to minimize the overall cost of the loan.

Students should be aware that the interest accrual process differs for loans taken out before 2012. For these loans, the interest rate is typically lower and may be fixed for the duration of the study period. However, the exact terms and conditions can vary depending on the specific loan agreement. It's essential for students to review their loan contracts carefully to understand the interest rates, repayment terms, and any other conditions that may apply to their particular loan.

To manage the impact of interest accrual during the study period, students can consider making voluntary repayments if they have the means to do so. While it's not compulsory to make repayments until after graduation, reducing the loan balance can help minimize the overall interest costs. Additionally, students can explore other financial support options, such as grants or scholarships, which do not require repayment and can help reduce reliance on loans. By being proactive and informed about the interest accrual process, students can make more strategic decisions about their finances and reduce the long-term burden of student loan debt.

Understanding Wells Fargo Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Loan Types Comparison: Differences in interest accrual between Plan 1 and Plan 2 loans

In the UK, student loans are primarily categorized under two repayment plans: Plan 1 and Plan 2. These plans differ significantly in terms of when and how interest accrues, which directly impacts the total amount borrowers repay over time. Understanding these differences is crucial for borrowers to manage their finances effectively. Plan 1 loans, typically held by students who started their courses before September 2012 (in England and Wales) or after September 2006 (in Northern Ireland), have a fixed interest rate tied to the Retail Price Index (RPI) or the Bank of England base rate, whichever is lower. Interest begins accruing from the date the first payment is made, but the rate remains relatively stable, making it easier for borrowers to predict their repayment amounts.

In contrast, Plan 2 loans, applicable to students who began their courses on or after September 2012 in England and Wales, or September 2016 in Northern Ireland, have a more complex interest structure. Interest accrues from the day the first payment is made, but the rate varies depending on the borrower’s income. While studying, the interest rate is RPI plus 3%, but once the borrower enters repayment, it ranges from RPI (for incomes up to £27,295) to RPI plus 3% (for incomes above £49,130). This tiered system means that higher earners pay more interest, potentially increasing the overall loan balance faster than under Plan 1.

Another key difference lies in the repayment thresholds and durations. Plan 1 loans require borrowers to start repaying once their income exceeds £19,895 annually, with the loan written off after 25 years. Plan 2 loans, however, have a higher repayment threshold of £27,295, and the loan is written off after 30 years. The longer repayment period and higher threshold of Plan 2 can result in more interest accruing over time, especially for borrowers with fluctuating incomes that frequently push them into higher interest brackets.

For borrowers, the choice between Plan 1 and Plan 2 is not optional but depends on when and where they studied. However, understanding the interest accrual mechanisms is essential for financial planning. Plan 1 borrowers benefit from a simpler, more predictable interest structure, while Plan 2 borrowers must be mindful of how their income affects the interest rate and, consequently, the total amount repaid. Both plans start accruing interest immediately after the first payment, but the long-term financial implications vary widely based on these structural differences.

Lastly, it’s important to note that interest accrual directly influences the loan balance, even if repayments are not yet required. For Plan 1 borrowers, the fixed interest rate ensures steady growth, whereas Plan 2 borrowers may see their balance increase more rapidly, particularly if they earn above the higher interest threshold. Borrowers should regularly review their loan statements and consider overpayments if possible, as reducing the principal balance can significantly decrease the total interest paid over the life of the loan. In summary, while both plans begin accruing interest immediately, the dynamic interest rates and repayment terms of Plan 2 make it a more complex and potentially costlier option compared to the straightforward structure of Plan 1.

Understanding Medical Student Loan Interest Rates: What’s Typical in 2023?

You may want to see also

![]()

Post-Graduation Grace Period: Is there a delay before interest starts after leaving university?

In the UK, understanding when student loans start accruing interest is crucial for graduates planning their finances. One common question is whether there is a post-graduation grace period before interest begins to accumulate. The answer depends on the type of student loan you have, as the UK operates different loan systems for students from England, Wales, Scotland, and Northern Ireland. For most graduates, interest does start accruing immediately after leaving university, but there are nuances to consider.

For students from England and Wales who took out loans under the current Plan 2 or Plan 3 repayment schemes, interest begins to accrue from the day you leave your course. There is no grace period, meaning interest starts accumulating straight away. However, the interest rate is tied to the Retail Price Index (RPI) and can vary depending on your income. While this might sound daunting, repayments are only required once you earn above a certain threshold, and any outstanding balance is written off after 30 years.

In contrast, students from Scotland under the Student Awards Agency Scotland (SAAS) system do benefit from a post-graduation grace period. Interest does not begin to accrue until April after you graduate or leave your course. This provides a short window of time before interest starts, though repayments are still only required once you earn above the threshold. Similarly, students from Northern Ireland under the Student Loans Company (SLC) system also face interest accrual from the day they leave their course, with no grace period.

It’s important to note that while interest accrues immediately for most graduates, the repayment terms are designed to be manageable. Repayments are calculated as a percentage of your income above the threshold, and if you’re not earning enough, you won’t make any repayments. This system aims to balance the need for loan recovery with the financial realities of new graduates. However, understanding when interest starts can help you plan and potentially explore strategies to minimize the overall cost of your loan.

For those considering early repayment or overpayments, knowing that interest accrues immediately post-graduation can influence your decisions. While overpaying can reduce the total interest paid over time, it’s essential to weigh this against other financial priorities, such as saving for emergencies or paying off higher-interest debt. In summary, while there is generally no post-graduation grace period for interest accrual in the UK, the repayment structure is designed to be income-contingent, providing some financial flexibility for graduates.

Where to Deduct Student Loan Interest on Your Tax Return

You may want to see also

Frequently asked questions

In the UK, student loans typically start accruing interest from the day the first payment is made to the student, not from the date the loan is taken out.

Yes, the interest rate on UK student loans is variable and is based on the Retail Price Index (RPI) or the Bank of England base rate, depending on the type of loan and when it was taken out.

No, interest accrues from the day the loan is issued, not after graduation. However, repayment terms and interest rates may vary depending on the loan plan and repayment threshold.

Some loans, like the Postgraduate Loan, accrue interest from the day the first payment is made. However, for undergraduate loans, interest is applied from the start of the course, but repayments are not required until after graduation and earning above the threshold.