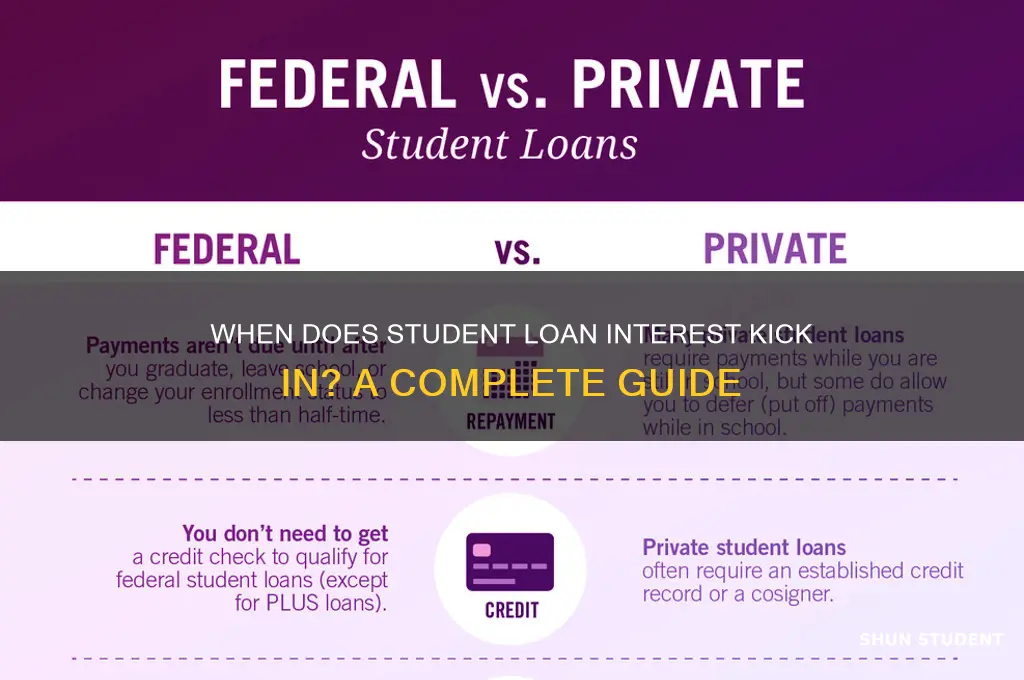

Understanding when interest kicks in on a student loan is crucial for borrowers to manage their finances effectively. Typically, interest begins to accrue on most student loans as soon as the funds are disbursed, though the timing of when borrowers are required to start making payments varies. For federal unsubsidized loans, interest accrues immediately, while subsidized loans may offer a grace period during which the government covers the interest while the borrower is in school. Private loans often have their own terms, with some requiring immediate payments and others deferring interest until after graduation. Knowing these details helps borrowers plan for repayment and explore options like interest capitalization or early payments to minimize long-term costs.

| Characteristics | Values |

|---|---|

| Interest Accrual Start Date | Immediately after disbursement for unsubsidized loans; after grace period for subsidized loans. |

| Grace Period | Typically 6 months after graduation, leaving school, or dropping below half-time enrollment. |

| Loan Types | Unsubsidized Loans: Interest accrues immediately. Subsidized Loans: No interest during school, grace period, or deferment. |

| Deferment Period | Interest may accrue depending on loan type (e.g., unsubsidized loans accrue interest during deferment). |

| Forbearance Period | Interest accrues on all loan types during forbearance. |

| Repayment Start Date | After the grace period ends (usually 6 months post-graduation or leaving school). |

| Capitalization of Interest | Unpaid interest may capitalize (added to the principal balance) when entering repayment or after deferment/forbearance periods. |

| Private Student Loans | Terms vary by lender; interest often accrues immediately after disbursement, with no grace period. |

| Income-Driven Repayment Plans | Interest may still accrue, and unpaid interest can capitalize over time. |

| Latest Data Source | Federal Student Aid (FSA) guidelines as of 2023. |

Explore related products

What You'll Learn

- Grace Period Length: Time after graduation before interest accrual begins on student loans

- In-School Interest: How interest accumulates while the student is still enrolled

- Deferment Rules: Conditions under which interest may or may not accrue during deferment

- Capitalization Impact: When unpaid interest is added to the loan principal balance

- Loan Type Differences: Variations in interest accrual between subsidized and unsubsidized loans

![]()

Grace Period Length: Time after graduation before interest accrual begins on student loans

Understanding the grace period for student loans is crucial for borrowers to manage their finances effectively after graduation. The grace period refers to the time frame after a student leaves school during which they are not required to make payments on their loans, and, in some cases, interest does not accrue. This period is designed to provide graduates with a buffer to find employment and stabilize their financial situation before the burden of loan repayment begins. Typically, the grace period length varies depending on the type of student loan—federal or private—and the specific terms of the loan agreement.

For federal student loans, the grace period is generally six months after the borrower graduates, leaves school, or drops below half-time enrollment. During this six-month grace period, interest does not accrue on subsidized federal loans, meaning the government covers the interest costs. However, for unsubsidized federal loans, interest begins accruing immediately after graduation, even during the grace period. This distinction is critical because it affects the total amount the borrower will eventually repay. Borrowers should be aware of the type of federal loans they have to plan accordingly and consider making interest payments during the grace period to avoid capitalization, where unpaid interest is added to the principal balance.

Private student loans, on the other hand, often have varying grace period terms that are determined by the lender. Some private loans may offer a six-month grace period similar to federal loans, while others may provide a shorter or longer period, or even no grace period at all. Additionally, interest on private loans typically begins accruing immediately after graduation, regardless of the grace period. Borrowers with private loans should carefully review their loan agreements to understand when interest starts and whether they have any grace period. This knowledge is essential for budgeting and deciding whether to make early payments to reduce overall interest costs.

It is important for borrowers to note that while the grace period can provide temporary relief, it is not a long-term solution for managing student loan debt. Ignoring accruing interest, especially on unsubsidized and private loans, can lead to higher overall repayment amounts. Borrowers should consider using the grace period to explore repayment options, such as income-driven plans or loan consolidation, and to create a financial strategy for managing their debt. Proactive steps during this time can significantly impact long-term financial health.

Lastly, some borrowers may choose to waive their grace period, particularly if they are in a position to start making payments immediately. For unsubsidized federal loans and private loans, waiving the grace period and beginning payments early can save money by reducing the total interest paid over the life of the loan. However, this decision should be made based on individual financial circumstances and employment prospects. Understanding the grace period and its implications empowers borrowers to make informed decisions about their student loans and take control of their financial future.

Interest-Free Student Loans: A Guide to Debt-Free Education Financing

You may want to see also

Explore related products

![]()

In-School Interest: How interest accumulates while the student is still enrolled

When it comes to student loans, understanding how interest accrues is crucial, especially while you're still in school. In-school interest refers to the interest that accumulates on your student loan balance during the period you are enrolled in classes. This aspect of student loans can significantly impact the total amount you'll owe by the time you graduate. For most student loans, interest begins to accrue as soon as the loan is disbursed, even if you're not yet making payments. This means that from the day the loan funds are applied to your tuition or disbursed to you, interest starts to build up.

The way in-school interest works largely depends on the type of student loan you have. For subsidized federal student loans, the government pays the interest on your behalf while you are enrolled at least half-time, during the grace period after graduation, and during any approved deferment periods. This is a significant benefit, as it prevents the loan balance from growing while you are in school and during certain other periods. However, not all students qualify for subsidized loans, and many borrowers rely on unsubsidized federal loans or private student loans, which do not offer this interest subsidy.

For unsubsidized federal student loans and private student loans, interest accrues continuously from the time the loan is disbursed. If you do not pay the interest as it accrues, it will be capitalized, meaning it is added to the principal balance of your loan. This results in compound interest, where you are charged interest on a larger principal amount, causing your loan balance to grow faster over time. For example, if you borrow $10,000 with a 5% interest rate and do not pay the accruing interest while in school, the interest will be added to the principal, and you will graduate owing more than $10,000.

To minimize the impact of in-school interest, borrowers have a few options. One strategy is to make interest payments while still in school, even if they are not required. By paying the interest as it accrues, you can prevent capitalization and keep your loan balance from growing. Another option is to make small principal payments, which can reduce the overall amount of interest that accrues. Some students also consider taking on part-time work or applying for scholarships and grants to reduce their reliance on loans.

It's important to carefully review the terms of your student loan to understand how in-school interest works for your specific situation. Federal student loans offer more flexibility and benefits compared to private loans, so it's generally advisable to exhaust federal loan options before considering private lenders. Additionally, staying informed about your loan status and making proactive decisions about interest payments can help you manage your debt more effectively and avoid unnecessary financial burden after graduation.

In summary, in-school interest is a critical component of student loans that can significantly affect the total cost of your education. While subsidized federal loans offer a reprieve from accruing interest, unsubsidized federal loans and private loans require careful management to prevent the loan balance from growing. By understanding how interest accumulates and exploring strategies to mitigate its impact, students can take control of their financial future and minimize the long-term costs of their education.

Monthly Interest Charges: How Student Loan Companies Calculate Your Debt

You may want to see also

Explore related products

![]()

Deferment Rules: Conditions under which interest may or may not accrue during deferment

When it comes to student loans, understanding deferment rules is crucial, especially regarding whether interest accrues during this period. Deferment allows borrowers to temporarily pause their loan payments under specific conditions, but the rules around interest vary depending on the type of loan. For federal student loans, the government often covers the interest on subsidized loans during deferment, meaning no additional interest accrues. However, for unsubsidized federal loans, interest continues to accrue during deferment, which can increase the total amount owed over time. This distinction is vital for borrowers to manage their loan balances effectively.

For private student loans, deferment rules are typically less favorable than those for federal loans. Most private lenders do not offer interest-free deferment periods, meaning interest will almost always accrue during deferment. Borrowers with private loans should carefully review their loan agreements to understand the specific terms and conditions. If interest accrues during deferment, it may capitalize (be added to the principal balance), further increasing the cost of the loan. Proactive communication with private lenders can sometimes lead to alternative arrangements, but these are not guaranteed.

The conditions under which deferment is granted also play a role in interest accrual. Common eligibility criteria for deferment include enrollment in school at least half-time, economic hardship, unemployment, or active military duty. For federal loans, meeting these conditions may qualify borrowers for interest-free deferment on subsidized loans, while unsubsidized loans will still accrue interest. It is essential to apply for deferment through the loan servicer and provide necessary documentation to ensure the correct terms are applied.

Borrowers should also be aware of the differences between deferment and forbearance. While both allow for paused payments, forbearance is generally granted due to financial hardship and almost always results in interest accrual, regardless of the loan type. Deferment, on the other hand, may offer interest-free benefits for subsidized loans but not for unsubsidized or private loans. Understanding these nuances helps borrowers make informed decisions about managing their student loan debt.

Lastly, proactive management of student loans during deferment can mitigate long-term costs. For loans accruing interest during deferment, borrowers may consider making interest-only payments to prevent capitalization. This approach keeps the principal balance from growing and reduces the overall cost of the loan. Regularly reviewing loan terms, staying in contact with loan servicers, and exploring repayment plans or forgiveness programs can also help borrowers navigate deferment rules effectively and minimize financial burden.

Understanding Average Student Loan Interest Rates with SoFi: A Guide

You may want to see also

Explore related products

$6.99

![]()

Capitalization Impact: When unpaid interest is added to the loan principal balance

Interest capitalization on a student loan occurs when unpaid interest is added to the principal balance of the loan, increasing the total amount you owe. This process is a critical aspect of understanding when and how interest "kicks in" on student loans, particularly for federal loans. Capitalization typically happens under specific circumstances, such as at the end of a grace period, deferment, or forbearance, when the borrower transitions from a non-payment period to repayment. For example, if you have an unsubsidized federal student loan, interest accrues while you are in school, during the grace period, and in deferment. If this interest is not paid as it accrues, it will capitalize and be added to the principal balance when repayment begins.

The capitalization impact is significant because it directly increases the total cost of the loan. When interest capitalizes, the principal balance grows, and future interest is calculated on this new, higher amount. This means you end up paying interest on the interest that was previously unpaid, leading to higher monthly payments and a longer repayment term. For instance, if you have a $20,000 loan with $1,000 in accrued interest that capitalizes, your new principal balance becomes $21,000. As a result, the total interest you pay over the life of the loan increases, making it more expensive to repay the debt.

To minimize the capitalization impact, borrowers should explore strategies to pay accrued interest before it capitalizes. For federal loans, making interest payments while in school, during the grace period, or in deferment can prevent capitalization. Even small payments can make a difference, as they reduce the amount of interest that will be added to the principal. Additionally, borrowers can consider income-driven repayment plans, which may limit capitalization by capping monthly payments based on income and family size, thereby reducing the likelihood of unpaid interest.

Another critical factor is understanding the terms of your specific loan, as capitalization rules can vary. Private student loans, for example, may capitalize interest more frequently or under different conditions than federal loans. Some private lenders capitalize interest monthly if payments are not made, while others may do so at the end of a forbearance period. Reviewing your loan agreement and communicating with your lender can provide clarity on when capitalization occurs and how to avoid it.

Lastly, the capitalization impact underscores the importance of proactive loan management. Borrowers should stay informed about their loan status, track interest accrual, and take advantage of resources like loan simulators to estimate the long-term effects of capitalization. By addressing accrued interest before it capitalizes and choosing repayment strategies that align with financial goals, borrowers can mitigate the increased costs associated with interest capitalization and manage their student loan debt more effectively.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![]()

Loan Type Differences: Variations in interest accrual between subsidized and unsubsidized loans

When it comes to student loans, understanding the differences between subsidized and unsubsidized loans is crucial, as these variations directly impact when and how interest accrues. Subsidized loans, available to undergraduate students with demonstrated financial need, are unique because the government pays the interest on these loans while the borrower is in school at least half-time, during the grace period after leaving school (typically six months), and during any approved deferment periods. This means interest does not kick in until after these periods end, significantly reducing the overall cost of the loan for the borrower. For example, if a student borrows $5,000 in subsidized loans and graduates after four years, they will still owe only $5,000, as no interest has accrued during their time in school or the grace period.

In contrast, unsubsidized loans are available to both undergraduate and graduate students regardless of financial need, but they come with a critical difference in interest accrual. With unsubsidized loans, interest begins to accrue immediately after the loan is disbursed, even while the borrower is still in school. This means that if a student does not pay the interest as it accrues, it will be capitalized—added to the principal balance of the loan—once repayment begins. For instance, if a student borrows $10,000 in unsubsidized loans and does not pay the accruing interest during their four years in school, the capitalized interest could increase the total amount repaid by several hundred dollars, depending on the interest rate.

The timing of interest accrual has long-term financial implications for borrowers. For subsidized loans, the absence of interest during key periods provides a financial cushion, allowing borrowers to focus on repayment without the added burden of compounded interest. However, unsubsidized loans require proactive financial management. Borrowers can choose to pay the interest while in school to prevent capitalization, but many students may not have the means to do so. This difference underscores the importance of carefully considering loan types when borrowing for education.

Another key distinction lies in eligibility and loan limits. Subsidized loans are need-based and have lower annual and aggregate borrowing limits compared to unsubsidized loans. This means students may not qualify for enough subsidized loans to cover their educational expenses, necessitating the use of unsubsidized loans. As a result, understanding the interest accrual differences becomes even more critical, as borrowers may need to manage both types of loans simultaneously. For example, a student might have a subsidized loan for which interest is covered during school but also an unsubsidized loan accruing interest, requiring them to budget for interest payments on the latter.

In summary, the primary difference in interest accrual between subsidized and unsubsidized loans lies in when interest begins to accumulate and who is responsible for paying it. Subsidized loans offer a significant advantage by delaying interest accrual until after school, grace periods, and deferments, while unsubsidized loans start accruing interest immediately. Borrowers should carefully weigh these differences when choosing loan types, as they directly impact the total cost of borrowing and the financial strategies needed to manage student debt effectively.

Which Student Loan Type Carries the Highest Interest Rates?

You may want to see also

Frequently asked questions

Interest typically begins to accrue on a student loan as soon as the loan is disbursed, though this can vary depending on the type of loan. For unsubsidized federal loans, interest starts immediately, while subsidized federal loans may not accrue interest until after the grace period ends.

Yes, many student loans offer a grace period after graduation, leaving school, or dropping below half-time enrollment. For federal student loans, the grace period is usually 6 months, during which interest may or may not accrue depending on the loan type.

No, the timing of when interest kicks in depends on the type of loan. For example, subsidized federal loans may not accrue interest until after the grace period, while unsubsidized federal loans and private loans typically start accruing interest immediately upon disbursement.