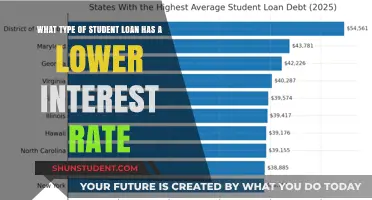

Understanding the average student loan interest rate is crucial for borrowers, especially when considering refinancing options like those offered by SoFi. As of recent data, federal student loan interest rates typically range from 4.99% to 7.54%, depending on the type of loan and the borrower’s program. Private student loan rates, however, can vary widely, often falling between 3.99% and 14.99%, depending on creditworthiness and market conditions. SoFi, a leading student loan refinancing platform, often offers competitive rates starting as low as 4.44% for fixed APR and 4.99% for variable APR, making it an attractive option for those looking to lower their monthly payments or pay off debt faster. Before refinancing, borrowers should compare SoFi’s rates with their current terms to ensure it aligns with their financial goals.

Explore related products

What You'll Learn

![]()

Federal vs. Private Loan Rates

When considering student loans, understanding the difference between federal and private loan rates is crucial. Federal student loans, which are issued by the U.S. Department of Education, typically offer fixed interest rates that are set by Congress. As of the most recent data, federal undergraduate loans have an interest rate of around 4.99%, while graduate loans are slightly higher at approximately 6.54%. These rates are generally lower than private loan rates and come with additional benefits such as income-driven repayment plans, loan forgiveness options, and deferment or forbearance in times of financial hardship. For borrowers seeking predictable monthly payments and flexible repayment terms, federal loans often provide a more secure option.

Private student loans, on the other hand, are offered by banks, credit unions, and online lenders like SoFi. Interest rates for private loans can vary widely based on the borrower’s credit history, income, and other financial factors. As of recent trends, private student loan interest rates typically range from 3.99% to 14.99% or higher, depending on whether the loan is fixed or variable. While some borrowers with excellent credit may secure rates lower than federal loan rates, others with limited credit history or lower credit scores may face significantly higher rates. Private loans also lack the borrower protections and repayment options available with federal loans, making them a riskier choice for many students.

One key advantage of private loans, particularly from lenders like SoFi, is the potential for lower rates for well-qualified borrowers. SoFi, for example, often advertises competitive rates starting as low as 3.99% for those with strong credit profiles. Additionally, private lenders may offer perks such as autopay discounts, career coaching, and flexible repayment terms. However, these benefits come with the caveat that private loans are not eligible for federal loan consolidation, forgiveness programs, or income-driven repayment plans, which can be essential for borrowers facing financial difficulties.

When comparing federal vs. private loan rates, it’s important to consider long-term financial implications. Federal loans provide stability and flexibility, making them a safer choice for most borrowers, especially those unsure about their future income potential. Private loans, while potentially offering lower rates for some, carry higher risks due to their dependence on creditworthiness and lack of federal protections. Borrowers should exhaust federal loan options before turning to private loans, as federal rates are generally more predictable and come with valuable safeguards.

In summary, the choice between federal and private loan rates depends on individual financial circumstances and priorities. Federal loans offer fixed, lower rates and borrower protections, making them a reliable option for most students. Private loans, such as those from SoFi, may provide lower rates for creditworthy borrowers but come with higher risks and fewer repayment options. Before making a decision, students should carefully evaluate their eligibility for federal aid, compare interest rates, and consider their long-term financial goals.

Understanding the Latest Interest Rate Changes for Student Loans

You may want to see also

Explore related products

![]()

Fixed vs. Variable Interest Rates

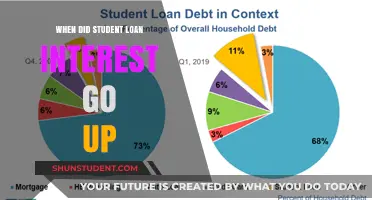

When considering student loan options with SoFi, one of the most critical decisions borrowers face is choosing between fixed and variable interest rates. As of recent data, SoFi offers competitive rates, but understanding the difference between these two types of rates is essential for making an informed decision. A fixed interest rate remains the same throughout the life of the loan, providing predictability and stability in monthly payments. This is particularly beneficial in a rising interest rate environment, as borrowers are shielded from potential increases. For example, if you lock in a fixed rate of 5%, it will stay at 5% regardless of market fluctuations.

On the other hand, variable interest rates can fluctuate over time based on market conditions, typically tied to an index like the London Interbank Offered Rate (LIBOR) or the Secured Overnight Financing Rate (SOFR). Initially, variable rates may be lower than fixed rates, making them an attractive option for borrowers who plan to pay off their loans quickly or expect interest rates to remain stable or decline. However, this option carries risk, as rising interest rates can lead to higher monthly payments and increased overall loan costs. For instance, a variable rate starting at 3% could increase to 6% or more if market rates rise significantly.

The choice between fixed and variable rates often depends on your financial situation, risk tolerance, and economic outlook. If you prioritize consistency and budgeting, a fixed rate is generally the safer choice. It eliminates the uncertainty of fluctuating payments, making it easier to plan your finances long-term. Conversely, if you are comfortable with potential rate changes and believe you can pay off the loan before rates rise substantially, a variable rate might save you money in the short term.

SoFi’s average student loan interest rates for both fixed and variable options are typically lower than federal student loan rates, especially for borrowers with strong credit histories. As of the latest data, fixed rates range from approximately 4% to 7%, while variable rates start around 2% to 5%. However, these ranges can vary based on factors like loan term, creditworthiness, and whether you choose additional benefits like autopay discounts.

Ultimately, the decision between fixed and variable rates should align with your personal financial goals and risk appetite. It’s advisable to evaluate your repayment timeline, current economic trends, and future interest rate projections before committing. SoFi also offers tools and resources to help borrowers compare scenarios, ensuring you choose the option that best fits your needs. By carefully weighing the pros and cons of each, you can make a confident decision about managing your student loan debt effectively.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Refinancing Options with SoFi

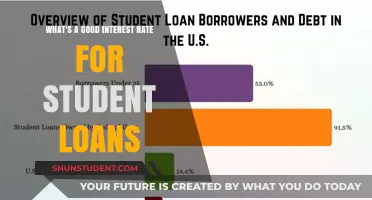

When considering refinancing student loans, understanding the average interest rates is crucial, and SoFi offers competitive options that can help borrowers save money over time. As of recent data, the average student loan interest rate for federal loans ranges from 3.73% to 6.28%, depending on the type of loan and disbursement date. Private loan rates can vary widely, often starting at around 4% and going up to 12% or more, depending on creditworthiness. SoFi, a leading student loan refinancing lender, typically offers variable rates starting as low as 4.99% and fixed rates starting at 5.35%, though these rates can fluctuate based on market conditions and individual financial profiles.

Refinancing with SoFi can be a strategic move for borrowers looking to secure a lower interest rate or adjust their repayment terms. One of the key advantages of SoFi is its flexibility in loan terms, allowing borrowers to choose between 5, 7, 10, 15, and 20-year repayment plans. This customization helps align monthly payments with financial goals, whether the aim is to pay off the loan quickly or reduce monthly obligations. Additionally, SoFi offers both fixed and variable interest rates, giving borrowers the option to lock in a consistent rate or take advantage of potentially lower initial rates with a variable option.

To qualify for refinancing with SoFi, borrowers typically need a strong credit history and a steady income, as these factors significantly influence the interest rate offered. SoFi also considers the borrower’s overall financial health, including debt-to-income ratio and employment status. For those with federal student loans, it’s important to weigh the benefits of refinancing against the loss of federal protections, such as income-driven repayment plans and loan forgiveness programs. SoFi does offer some unique perks, such as unemployment protection, which pauses loan payments temporarily if the borrower loses their job, providing a safety net not available with all lenders.

The application process with SoFi is streamlined and entirely online, making it convenient for borrowers to check their rates without affecting their credit score. Pre-qualification takes just a few minutes and involves providing basic personal and financial information. Once approved, borrowers can select their preferred loan terms and complete the refinancing process. SoFi also stands out for its lack of fees—there are no application fees, origination fees, or prepayment penalties, which can further enhance savings compared to other lenders.

For borrowers with high-interest student loans, refinancing with SoFi can lead to significant long-term savings. For example, refinancing a $30,000 loan from a 7% interest rate to a 5% rate could save thousands of dollars over the life of the loan. SoFi’s competitive rates, combined with its borrower-friendly features, make it a top choice for those looking to optimize their student loan repayment strategy. However, it’s essential to compare offers from multiple lenders and consider individual financial circumstances before making a decision.

Where to Deduct Student Loan Interest on Your Tax Return

You may want to see also

Explore related products

$16.53 $22.99

![]()

Current Average Interest Trends

As of the latest data, the average student loan interest rates offered by SoFi reflect broader market trends and federal benchmarks. SoFi, a leading private student loan lender, typically offers variable and fixed interest rates that are competitive within the industry. Current trends indicate that fixed rates for undergraduate and graduate loans range between 4.5% and 12%, depending on the borrower’s creditworthiness, loan term, and repayment plan. Variable rates, which fluctuate with market conditions, generally start lower but carry the risk of increasing over time, currently ranging from 3.5% to 11%. These rates are influenced by the Federal Reserve’s monetary policy, with recent hikes contributing to a slight upward pressure on borrowing costs.

One notable trend is the narrowing gap between federal and private student loan interest rates. Federal student loan rates for the 2023-2024 academic year are fixed at 5.5% for undergraduate loans and 7.05% for graduate loans, making SoFi’s rates particularly competitive for borrowers with strong credit profiles. However, private loans like those from SoFi often require a credit check and may necessitate a cosigner for better terms, which can impact the final interest rate offered. Borrowers with excellent credit may secure rates at the lower end of the spectrum, while those with fair or poor credit may face higher costs.

Another trend is the increasing popularity of refinancing options, which SoFi prominently offers. Refinancing allows borrowers to replace their existing student loans with a new loan at a potentially lower interest rate. Current refinancing rates at SoFi start as low as 4.99% for fixed rates and 3.95% for variable rates, depending on market conditions and individual qualifications. This trend is driven by borrowers seeking to reduce monthly payments or shorten loan terms in response to rising inflation and economic uncertainty.

Market analysts also highlight the impact of economic indicators on student loan interest rates. Inflation, unemployment rates, and the overall health of the economy play significant roles in determining borrowing costs. As of now, inflation remains elevated, prompting lenders like SoFi to adjust rates to mitigate risk. Borrowers are advised to monitor these trends closely and consider locking in fixed rates if they anticipate further increases in the near future.

Lastly, SoFi’s interest rates are often accompanied by borrower-friendly features such as autopay discounts, career coaching, and unemployment protection, which can add value despite slightly higher rates compared to some competitors. Prospective borrowers should weigh these benefits against the current average interest trends when deciding on a lender. Staying informed about rate fluctuations and understanding how they align with personal financial goals is crucial for making an educated decision in the current lending environment.

Understanding Ideal Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Impact of Credit Score on Rates

When considering the average student loan interest rates offered by SoFi, it's crucial to understand how credit scores play a pivotal role in determining the rates borrowers receive. SoFi, like many lenders, uses credit scores as a key factor in assessing the risk associated with lending to an individual. A higher credit score generally indicates a lower risk to the lender, which can translate to more favorable interest rates for the borrower. Conversely, a lower credit score may result in higher interest rates, as the lender perceives a greater risk of default. This relationship underscores the importance of maintaining a strong credit profile when seeking student loan refinancing or private student loans through SoFi.

The impact of credit scores on interest rates is particularly significant because even a slight difference in rates can lead to substantial savings or additional costs over the life of the loan. For instance, a borrower with an excellent credit score (typically 720 or above) might qualify for SoFi’s lowest advertised rates, which are often competitive with other top lenders. On the other hand, a borrower with a fair or poor credit score (below 670) may face higher rates, potentially increasing the total repayment amount by thousands of dollars. This disparity highlights why borrowers should aim to improve their credit scores before applying for student loan refinancing or private loans.

SoFi typically requires a minimum credit score of 650 for refinancing, though meeting this threshold does not guarantee the lowest rates. Borrowers with scores in the mid-700s or higher are more likely to secure the most favorable terms. Additionally, SoFi considers other factors alongside credit scores, such as income, employment history, and debt-to-income ratio. However, the credit score remains a dominant factor in rate determination. Prospective borrowers can check their credit reports for inaccuracies and take steps to improve their scores, such as paying down debt and ensuring timely payments, to increase their chances of qualifying for lower rates.

For those with limited credit history, such as recent graduates, SoFi offers the option to apply with a cosigner. A cosigner with a strong credit profile can help secure a lower interest rate, as their creditworthiness is considered in the application. This can be a strategic move for borrowers who are still building their credit but need immediate access to competitive rates. Over time, as the primary borrower establishes their own credit history, they may choose to release the cosigner from the loan through a cosigner release process, which SoFi provides after a certain period of consistent on-time payments.

In summary, the impact of credit scores on SoFi’s student loan interest rates cannot be overstated. Borrowers with higher credit scores are more likely to receive lower rates, while those with lower scores may face higher costs. Understanding this relationship and taking proactive steps to improve creditworthiness can significantly influence the terms of a student loan. Whether refinancing existing loans or taking out new private loans, focusing on credit health is essential for maximizing savings and achieving financial goals with SoFi.

Federal Student Loan Interest Rates in 2002: A Historical Overview

You may want to see also

Frequently asked questions

The average student loan interest rate offered by SoFi typically ranges from 4.99% to 11.99% for fixed rates and 5.74% to 11.99% for variable rates, depending on creditworthiness and loan terms.

SoFi determines interest rates based on factors such as credit history, income, loan term, and whether the borrower chooses a fixed or variable rate. Stronger financial profiles generally qualify for lower rates.

SoFi’s interest rates can be competitive with or lower than federal student loan rates, especially for borrowers with excellent credit. However, federal loans often come with additional benefits like income-driven repayment plans and forgiveness options, which SoFi does not offer.