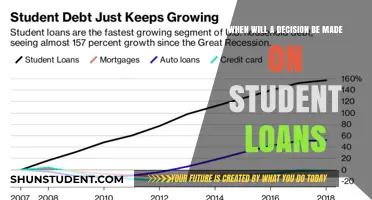

The topic of student loan cancellation has been a pressing issue for millions of Americans, with many eagerly awaiting news on when President Biden will announce a decision. Since his campaign, Biden has expressed support for some form of student debt relief, and recent reports suggest his administration is actively considering options, including targeted cancellation or broader forgiveness. While no official announcement has been made, speculation is mounting that a decision could come in the near future, potentially before the midterm elections. Borrowers and advocacy groups are closely monitoring developments, as the outcome could significantly impact the financial well-being of millions and shape the political landscape.

| Characteristics | Values |

|---|---|

| Current Status | No official announcement yet (as of October 2023). |

| Recent Developments | Supreme Court struck down Biden's original student loan forgiveness plan in June 2023. |

| Alternative Efforts | Biden administration has been pursuing targeted loan cancellation through existing programs (e.g., Public Service Loan Forgiveness, income-driven repayment plans). |

| Potential Timeline | Unclear; administration has not provided a specific date or timeframe. |

| Key Factors Influencing Announcement | Legal challenges, political considerations, and economic conditions. |

| Public Expectations | Mixed; some borrowers anticipate partial relief, while others remain skeptical. |

| Recent Statements | Biden has emphasized commitment to providing relief but has not confirmed a new plan. |

| Legislative Efforts | No new legislation proposed specifically for broad student loan cancellation. |

| Targeted Relief Focus | Focus on low-income borrowers, public service workers, and those with predatory loans. |

| Estimated Impact | Any new plan is likely to be more limited in scope compared to the original proposal. |

Explore related products

$14.99 $14.99

What You'll Learn

- Potential Announcement Timeline: Speculation on when Biden might announce student loan cancellation

- Eligibility Criteria: Details on who may qualify for loan forgiveness

- Amount of Forgiveness: Possible loan cancellation amounts being considered

- Legal Challenges: Potential lawsuits and obstacles to implementation

- Political Impact: How the decision could affect Biden’s approval ratings and elections

![]()

Potential Announcement Timeline: Speculation on when Biden might announce student loan cancellation

The timing of Biden’s potential announcement on student loan cancellation hinges on a delicate balance of political strategy, legal considerations, and economic signals. Observers note that major policy announcements often align with key moments in the election cycle, such as the State of the Union address or the Democratic National Convention. For instance, the 2024 election season could provide a strategic window, as debt relief could energize younger voters—a critical demographic for Biden’s reelection campaign. However, the administration must also navigate ongoing legal challenges to previous loan forgiveness attempts, which may delay an announcement until court rulings provide clearer guidance.

Analyzing historical patterns, Biden’s previous actions on student loans offer clues. The extension of the student loan payment pause in 2022 and 2023 suggests a willingness to act incrementally, but also highlights the administration’s caution. A potential timeline could see an announcement in late 2023 or early 2024, timed to maximize political impact without overshadowing other legislative priorities. For borrowers, this means monitoring economic indicators like inflation rates and unemployment, as the administration may wait for signs of stabilization before moving forward.

Instructively, borrowers should prepare for multiple scenarios. If an announcement comes in early 2024, it could coincide with tax season, creating a logistical challenge for both the government and borrowers. To stay informed, individuals should follow updates from the Department of Education and trusted news sources. Practical steps include keeping loan documents organized and understanding current repayment terms, as any cancellation would likely apply to specific categories of debt, such as federal loans under certain income thresholds.

Comparatively, Biden’s approach differs from Trump’s, who favored executive orders with immediate effect but limited scope. Biden’s strategy appears more methodical, prioritizing long-term legal viability over quick wins. This suggests that an announcement might be paired with a detailed implementation plan, including eligibility criteria and a phased rollout. For example, cancellation could start with borrowers in lower income brackets or those with loans over 20 years old, gradually expanding to broader groups.

Descriptively, the atmosphere surrounding a potential announcement is charged with anticipation and skepticism. Advocacy groups push for swift action, while opponents argue it could exacerbate inflation. The administration’s challenge is to strike a tone that reassures both borrowers and critics. A likely scenario involves framing the announcement as part of a broader economic recovery plan, emphasizing job creation and wage growth alongside debt relief. For borrowers, this means the timing could align with other economic initiatives, such as infrastructure investments or workforce development programs.

Ultimately, the timeline for Biden’s student loan cancellation announcement remains speculative but is likely tied to political and legal milestones. Borrowers should stay proactive, monitoring key dates like court rulings, legislative sessions, and campaign events. While uncertainty persists, one takeaway is clear: the announcement, when it comes, will be a carefully calculated move with far-reaching implications for millions of Americans.

Understanding Grading Criteria: What Students Will Be Evaluated On

You may want to see also

Explore related products

![]()

Eligibility Criteria: Details on who may qualify for loan forgiveness

As of the latest updates, President Biden's student loan cancellation plan has been a subject of intense speculation and debate. While the exact announcement date remains uncertain, understanding the potential eligibility criteria is crucial for borrowers. The eligibility criteria for loan forgiveness under Biden's plan are expected to be multifaceted, targeting specific groups of borrowers based on income, loan type, and other factors. Here’s a detailed breakdown to help you assess your potential qualification.

Income-Driven Eligibility: A Key Determinant

One of the most discussed eligibility factors is income-driven repayment (IDR) plan enrollment. Borrowers earning below a certain threshold, likely aligned with federal poverty guidelines, may qualify for partial or full forgiveness. For instance, individuals earning less than 250% of the federal poverty level (approximately $34,000 for a single-person household) could be prioritized. This approach mirrors Biden’s campaign promise to provide relief to low- and middle-income borrowers, ensuring that forgiveness benefits those most in need. If you’re currently on an IDR plan, review your income documentation to gauge your standing.

Loan Type and Servicer: Not All Loans Are Created Equal

Eligibility will likely hinge on the type of federal student loan held. Direct Loans, including subsidized and unsubsidized Stafford Loans, are expected to qualify, while Federal Family Education Loans (FFEL) and Perkins Loans held by private lenders may not unless consolidated into a Direct Loan. This distinction is critical, as consolidating ineligible loans could be a strategic step for some borrowers. Additionally, loans serviced by entities like Navient or FedLoan may require specific actions, such as ensuring accounts are in good standing, to qualify for forgiveness.

Public Service Loan Forgiveness (PSLF): A Special Consideration

Borrowers in public service roles may receive enhanced benefits. Under the PSLF program, those who have made 120 qualifying payments while working full-time for a government or nonprofit organization could see their remaining balance forgiven. Biden’s plan might expand this by waiving certain PSLF requirements retroactively, benefiting those with previously disqualified payments. If you’re in public service, audit your employment certification forms and payment history to maximize eligibility.

Practical Steps to Prepare for Eligibility

To position yourself for potential forgiveness, take proactive steps now. First, update your contact information with your loan servicer to ensure you receive notifications. Second, consolidate ineligible loans into a Direct Consolidation Loan if necessary. Third, apply for IDR plans if your income qualifies, as this could reduce your monthly payments and increase forgiveness potential. Finally, monitor official announcements from the Department of Education and avoid scams promising immediate relief.

By understanding these eligibility criteria and taking targeted actions, borrowers can better navigate the uncertainty surrounding Biden’s student loan cancellation announcement. While the timeline remains unclear, preparedness is key to maximizing potential benefits.

Will Student Debt Forgiveness Be Automatic? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Amount of Forgiveness: Possible loan cancellation amounts being considered

The Biden administration's potential student loan cancellation has sparked intense speculation, with one of the most pressing questions being the amount of forgiveness borrowers can expect. While no official figures have been confirmed, several proposals and leaks suggest a range of possibilities, each with distinct implications for borrowers and the economy.

Analytical Perspective:

Proposed amounts for student loan cancellation have varied widely, from $10,000 to $50,000 per borrower. A $10,000 forgiveness plan, often cited as a baseline, would eliminate debt entirely for approximately one-third of borrowers, primarily those with smaller balances. However, this amount would provide limited relief for graduate students or those with higher debt loads. On the other end, a $50,000 cancellation would significantly benefit higher-debt borrowers but could cost the government upwards of $1 trillion, raising concerns about fiscal responsibility and equity. Striking a balance between affordability and impact is critical, as the chosen amount will determine who benefits most and how the policy is perceived.

Instructive Approach:

To understand the potential amounts, consider the following steps: First, review the Biden campaign’s initial promise of $10,000 in forgiveness, which has been a recurring figure in discussions. Second, examine the push from progressive lawmakers for $50,000, which targets broader relief but faces political and financial hurdles. Third, analyze the compromise options, such as $20,000 or $30,000, which could address more borrowers’ needs without exceeding budgetary constraints. Finally, factor in income caps or eligibility criteria, as these could limit the scope of forgiveness and reduce overall costs.

Persuasive Argument:

A $50,000 cancellation is not just a policy choice but a moral imperative. Millions of borrowers, particularly those from low-income backgrounds or with advanced degrees, are burdened by debts that stifle their financial futures. While a $10,000 forgiveness would help some, it falls short of addressing systemic issues in higher education financing. By canceling $50,000, the administration could stimulate economic growth, reduce racial wealth gaps, and restore faith in the promise of education. Critics argue the cost is prohibitive, but the long-term benefits—increased consumer spending, homeownership, and entrepreneurship—far outweigh the initial investment.

Comparative Analysis:

Comparing the $10,000 and $50,000 proposals reveals stark differences in impact. A $10,000 cancellation would cost approximately $377 billion and primarily benefit borrowers with lower balances, such as community college graduates or those with partial degrees. In contrast, a $50,000 plan would cost over $1 trillion but would disproportionately aid graduate students and those in high-debt fields like medicine or law. While both options have merit, the choice hinges on whether the goal is to provide widespread relief or target those most burdened by debt.

Descriptive Insight:

Imagine a borrower with $30,000 in student loans, a common scenario for many undergraduates. Under a $10,000 cancellation, they would still owe $20,000, likely continuing their struggle with monthly payments. However, with a $50,000 forgiveness, their debt would vanish entirely, freeing up funds for savings, investments, or other expenses. This example illustrates how the amount of forgiveness directly correlates to the transformative potential of the policy, shaping not just individual lives but the broader economic landscape.

In conclusion, the amount of student loan forgiveness is a pivotal aspect of the Biden administration’s potential announcement. Whether $10,000, $50,000, or a figure in between, the decision will have far-reaching consequences for borrowers and the nation. As discussions continue, understanding these possibilities is essential for setting realistic expectations and advocating for meaningful change.

Elizabeth Warren's Executive Order: Student Loan Forgiveness Possibility Explored

You may want to see also

Explore related products

![]()

Legal Challenges: Potential lawsuits and obstacles to implementation

The path to student loan cancellation is fraught with legal landmines, even if President Biden announces a plan. Opponents will likely challenge the administration’s authority to act unilaterally, arguing it exceeds executive power and violates the separation of powers. Such lawsuits could delay implementation for years, leaving borrowers in limbo.

Consider the 2021 eviction moratorium, struck down by the Supreme Court for overstepping federal authority. Similarly, challengers could argue that canceling student debt requires congressional approval, citing the Constitution’s appropriations clause. Without explicit legislative backing, the administration’s legal footing becomes precarious, inviting injunctions and protracted court battles.

Another obstacle lies in standing—who has the right to sue? Taxpayer groups, lenders, or even states with financial ties to loan servicing could claim injury, though courts have historically been skeptical of such broad standing arguments. However, if a plaintiff with direct harm emerges—say, a loan servicer losing revenue—the case gains traction. Borrowers themselves, ironically, might also sue if partial cancellation creates inequities, such as excluding private loan holders or setting arbitrary eligibility thresholds.

Implementation hurdles compound these challenges. Even if legal authority is established, the Department of Education’s infrastructure may struggle to process millions of adjustments swiftly. Errors in eligibility determinations or payment recalculations could spawn individual lawsuits, further clogging the system. For instance, the Public Service Loan Forgiveness program faced years of delays due to administrative complexities, a cautionary tale for large-scale debt relief.

To mitigate risks, the administration could adopt a phased approach, targeting specific groups (e.g., low-income borrowers) first to test legal waters. Pairing cancellation with legislative action, even symbolic, could strengthen its case. Borrowers should prepare for uncertainty by documenting their loan histories and staying informed, as court rulings could retroactively alter eligibility. While cancellation remains a political promise, its realization hinges on navigating this legal gauntlet.

When Student Loan Forgiveness Escapes Taxes: Key Scenarios Explained

You may want to see also

Explore related products

![]()

Political Impact: How the decision could affect Biden’s approval ratings and elections

The timing of Biden's student loan cancellation announcement could significantly sway his approval ratings, particularly among younger voters aged 18–34, who hold a disproportionate share of student debt. A swift decision before the 2024 election might energize this demographic, historically less likely to vote, by framing the move as a direct financial relief measure. Conversely, delaying the announcement risks disillusionment, as seen in the 7-point drop in approval among 18–29-year-olds after the Supreme Court struck down his initial forgiveness plan in June 2023. Polling from Morning Consult indicates that 60% of this age group considers student debt a "very important" issue, making the announcement a high-stakes political calculus.

However, the political impact isn’t confined to young voters. Biden’s decision could alienate older, debt-free demographics who view broad cancellation as fiscally irresponsible or unfair. A September 2023 Pew Research survey found that 56% of Republicans and Republican-leaning independents strongly oppose cancellation, compared to 74% of Democrats who support it. This partisan divide suggests that while the move could solidify Biden’s base, it may also harden opposition, particularly in swing states like Pennsylvania and Wisconsin, where independent voters often prioritize economic stability over progressive policies.

Strategically, announcing cancellation during a campaign season could serve as a rallying cry, akin to Obama’s 2012 focus on student loan reform, which helped mobilize youth turnout. Yet, the execution matters: a phased rollout, such as forgiving $10,000 per borrower initially, might mitigate backlash while still delivering tangible benefits. Pairing the announcement with a broader economic message—such as job creation or inflation reduction—could blunt criticism of "handouts" and reframe the policy as part of a comprehensive recovery plan.

Caution is warranted, though. If the announcement is perceived as politically motivated or poorly timed (e.g., amid rising inflation), it could backfire. For instance, a Gallup poll revealed that 44% of Americans believe cancellation would worsen inflation, a concern Biden’s team must address head-on. Additionally, legal challenges, as seen with the Supreme Court’s rejection of his initial plan, could delay implementation, undermining its electoral impact.

In conclusion, the political ramifications of Biden’s student loan cancellation decision hinge on timing, messaging, and execution. Done right, it could bolster his standing with young voters and reinforce his commitment to economic fairness. Mishandled, it risks alienating key demographics and reinforcing narratives of government overreach. The announcement isn’t just a policy move—it’s a high-wire act with the potential to define Biden’s electoral legacy.

Student Loan Forgiveness and Taxes: Will You Receive a 1099-C?

You may want to see also

Frequently asked questions

As of the latest updates, there is no specific date announced for President Biden to declare student loan cancellation. The administration continues to review options and legal pathways for potential relief.

President Biden has expressed interest in providing student loan relief, including potential cancellation of up to $10,000 per borrower, but no official confirmation or details have been finalized.

Delays are attributed to legal challenges, political opposition, and ongoing discussions about the scope and eligibility criteria for any potential cancellation program.

It is unlikely that all borrowers will qualify. Any cancellation program is expected to have income limits or other eligibility criteria to target relief to those most in need.