The question of when the $10,000 deduction from student loans will occur has been a pressing concern for many borrowers, especially following recent announcements and policy changes. This deduction, part of broader student loan forgiveness initiatives, aims to alleviate the financial burden on millions of Americans. While specific timelines can vary based on individual circumstances and the implementation process, borrowers are advised to stay informed through official channels, such as the Department of Education or their loan servicers. Understanding the eligibility criteria and application requirements is crucial to ensure timely processing and maximize the benefits of this relief program.

| Characteristics | Values |

|---|---|

| Eligibility Criteria | Borrowers earning less than $125,000 (individual) or $250,000 (married couples) per year. |

| Loan Types Covered | Federal student loans held by the U.S. Department of Education. |

| Amount of Forgiveness | Up to $10,000 in forgiveness. |

| Additional Forgiveness for Pell Grant Recipients | Up to $20,000 in forgiveness. |

| Application Process | Borrowers must apply through a dedicated application (not automatic). |

| Application Deadline | December 31, 2023 (extended from previous deadlines). |

| Implementation Status | On hold due to legal challenges; awaiting Supreme Court decision. |

| Legal Challenges | Multiple lawsuits have paused the program. |

| Expected Timeline (if approved) | Forgiveness could be processed within 4-6 weeks after application approval. |

| Impact on Taxes | Forgiveness is tax-free under the American Rescue Plan Act of 2021. |

| Current Status (as of October 2023) | Program is paused; borrowers are encouraged to apply to be prepared. |

Explore related products

What You'll Learn

- Repayment Plan Thresholds: When income exceeds thresholds, repayments begin, deducting 10,000 from student loans

- Loan Forgiveness Programs: Certain programs forgive 10,000 after meeting eligibility criteria, reducing loan balances

- Administrative Adjustments: Errors or updates in loan accounts may trigger 10,000 deductions

- Lump-Sum Payments: Voluntary or mandatory lump-sum payments can deduct 10,000 from the principal

- Tax Refunds: Offset programs may deduct 10,000 from tax refunds to repay student loans

![]()

Repayment Plan Thresholds: When income exceeds thresholds, repayments begin, deducting 10,000 from student loans

Student loan repayment plans often hinge on income thresholds, a critical detail for borrowers navigating their financial obligations. Once your income surpasses a predetermined threshold, repayments kick in, and the deduction of $10,000 from your student loan balance becomes a tangible reality. This mechanism is designed to balance affordability with the responsibility of repaying borrowed funds. Understanding these thresholds is crucial, as they vary depending on the type of loan and repayment plan you’ve selected. For instance, income-driven repayment plans like Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE) typically set thresholds based on the federal poverty line and family size, adjusting annually.

Consider this scenario: If you’re on an income-driven plan and your annual income rises above 150% of the federal poverty line for your family size, repayments begin. For a single borrower in 2023, this threshold is approximately $20,440. Once you exceed this amount, a portion of your income—usually 10% under plans like REPAYE—is allocated toward loan repayment. The $10,000 deduction, however, is not a standard feature of these plans but may apply under specific loan forgiveness programs or one-time relief initiatives. For example, the 2022 federal student loan forgiveness program offered up to $10,000 in debt cancellation for eligible borrowers, but this was a separate policy from regular repayment thresholds.

Analyzing the interplay between income thresholds and deductions reveals a strategic approach to managing student debt. Borrowers should monitor their income levels closely, especially if they anticipate crossing the threshold. Tools like the Department of Education’s Loan Simulator can help estimate monthly payments based on current income and family size. Additionally, keeping track of policy changes—such as temporary threshold adjustments during economic downturns—can provide opportunities to minimize repayments or qualify for forgiveness programs.

Practical tips for navigating this system include updating your income information annually to ensure accurate repayment calculations and exploring options like consolidating loans to simplify management. If your income fluctuates, consider recertifying your plan mid-year to adjust payments accordingly. For those nearing the threshold, reducing taxable income through contributions to retirement accounts or health savings plans might delay the onset of repayments. However, weigh these strategies against long-term financial goals, as they may impact eligibility for other benefits.

In conclusion, repayment plan thresholds serve as a dynamic tool for aligning student loan obligations with borrowers’ financial capabilities. While the $10,000 deduction is not directly tied to these thresholds, understanding how income triggers repayments is essential for effective debt management. By staying informed and proactive, borrowers can optimize their repayment strategies and potentially benefit from forgiveness opportunities when they arise.

Will Presidential Candidates Forgive Student Debt? A Voter's Guide

You may want to see also

Explore related products

![]()

Loan Forgiveness Programs: Certain programs forgive 10,000 after meeting eligibility criteria, reducing loan balances

Student loan borrowers often seek ways to reduce their debt burden, and one promising avenue is through loan forgiveness programs that deduct $10,000 from their balances. These programs are designed to provide financial relief to eligible individuals who meet specific criteria, such as working in public service, teaching in low-income schools, or making consistent income-driven payments. Understanding the eligibility requirements and application processes is crucial for borrowers aiming to benefit from these opportunities.

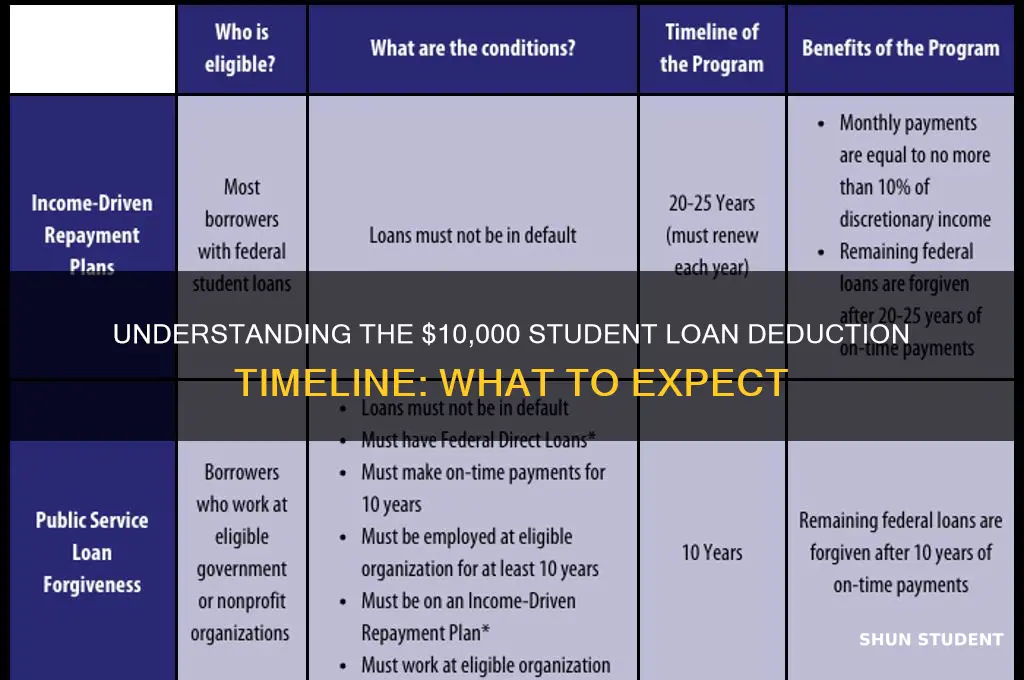

One prominent example is the Public Service Loan Forgiveness (PSLF) program, which forgives the remaining balance on federal Direct Loans after 120 qualifying payments. While PSLF doesn’t specifically deduct $10,000, it’s worth noting because it can eliminate significantly larger amounts. However, programs like the Limited PSLF Waiver or one-time adjustments introduced by the Department of Education have occasionally allowed borrowers to receive credits toward forgiveness, effectively reducing balances by $10,000 or more for those who meet specific conditions. These opportunities are often time-sensitive, requiring borrowers to act quickly to qualify.

Another pathway is through income-driven repayment (IDR) plans, which cap monthly payments based on income and family size. After 20–25 years of qualifying payments, the remaining balance is forgiven. While not a direct $10,000 deduction, these plans can lead to substantial forgiveness, particularly for borrowers with lower incomes. For instance, the IDR Account Adjustment launched in 2023 retroactively credited borrowers for months spent in forbearance or certain repayment plans, accelerating progress toward forgiveness and potentially reducing balances by $10,000 or more for eligible individuals.

To maximize the benefits of these programs, borrowers should take proactive steps. First, consolidate loans into a Direct Consolidation Loan if necessary, as only Direct Loans qualify for most forgiveness programs. Second, certify employment annually for PSLF to ensure payments count toward forgiveness. Third, monitor updates from the Department of Education, as new initiatives or waivers may provide additional opportunities for balance reductions. Finally, keep detailed records of payments and correspondence to resolve any discrepancies during the application process.

In conclusion, while not all forgiveness programs explicitly deduct $10,000, strategic use of PSLF, IDR plans, and temporary adjustments can lead to significant balance reductions. By staying informed and meeting eligibility criteria, borrowers can leverage these programs to alleviate their student loan burden effectively.

Will Discover Student Loans Be Forgiven? Exploring Potential Debt Relief Options

You may want to see also

Explore related products

![]()

Administrative Adjustments: Errors or updates in loan accounts may trigger 10,000 deductions

Administrative adjustments in student loan accounts can silently shift the balance by $10,000 or more, often catching borrowers off guard. These adjustments arise from errors, updates, or corrections in loan servicing systems, such as miscalculated interest, misapplied payments, or changes in loan status. For instance, a borrower might discover a sudden deduction after a servicer corrects a years-old coding error that incorrectly categorized their loan type. Such adjustments are not tied to forgiveness programs but stem from internal audits or borrower disputes, making them unpredictable yet impactful.

To navigate these adjustments, borrowers should proactively monitor their loan accounts monthly. Tools like the National Student Loan Data System (NSLDS) provide real-time updates on loan balances and servicer actions. If an unexpected $10,000 deduction appears, immediately contact the loan servicer to request a detailed explanation. Documentation is key—retain all correspondence and account statements to dispute inaccuracies. For example, if a payment was misapplied, providing proof of correct allocation can reverse the adjustment.

While administrative adjustments are often corrective, they can also work in the borrower’s favor. Suppose a servicer discovers an overcharge due to a system glitch; the $10,000 deduction could reduce the principal balance, lowering future interest accrual. However, the opposite is equally possible—an underpayment correction could increase the balance. Borrowers should treat these adjustments as opportunities to audit their accounts thoroughly, ensuring every dollar is accounted for.

Preventing unexpected deductions requires vigilance and advocacy. Enroll in auto-pay to minimize payment errors, and annually review your loan terms to ensure they align with your original agreement. If you suspect systemic issues, file a complaint with the Consumer Financial Protection Bureau (CFPB) or Federal Student Aid Ombudsman. These steps not only protect your financial interests but also pressure servicers to maintain accuracy, reducing the likelihood of future administrative adjustments.

Understanding the Timeline for Consolidating Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Lump-Sum Payments: Voluntary or mandatory lump-sum payments can deduct 10,000 from the principal

Lump-sum payments offer a strategic way to reduce student loan debt by directly targeting the principal balance. Whether voluntary or mandated, these payments can deduct $10,000 or more, depending on the loan terms and borrower’s financial capacity. For instance, a borrower with a $30,000 loan balance could allocate a $10,000 tax refund or bonus toward their principal, immediately lowering the amount subject to interest accrual. This approach not only shortens the loan term but also saves on long-term interest costs, making it a financially savvy move for those with disposable income.

Analyzing the mechanics, lump-sum payments differ from regular monthly installments, which often prioritize interest and fees. When a borrower specifies that a payment should be applied to the principal, the $10,000 deduction directly reduces the loan’s base amount. For example, a borrower with a 6% interest rate on a $50,000 loan could save over $3,000 in interest by applying a $10,000 lump sum. However, borrowers must ensure their loan servicer applies the payment correctly, as some may allocate it to future payments instead of the principal unless instructed otherwise.

From a persuasive standpoint, lump-sum payments are particularly beneficial for borrowers with high-interest loans or those seeking to accelerate debt repayment. For instance, a borrower in their 30s with a stable income might prioritize paying down student loans to free up cash flow for other financial goals, like saving for a home. By deducting $10,000 from the principal, they could reduce their loan term by several years, achieving financial freedom sooner. This strategy aligns with the principle of paying off high-interest debt first, a cornerstone of effective financial planning.

Comparatively, lump-sum payments stand out against other debt reduction methods, such as income-driven repayment plans or loan forgiveness programs. While these options offer relief through lower monthly payments or eventual forgiveness, they often extend the loan term and increase total interest paid. In contrast, a $10,000 lump-sum payment provides immediate and tangible progress toward debt elimination. For example, a borrower on an income-driven plan might still owe a significant balance after 20 years, whereas a lump-sum payment can shrink the debt faster, offering a clearer path to financial independence.

Practically, implementing this strategy requires careful planning. Borrowers should first confirm their loan terms allow for principal-only payments without penalties. Next, they should assess their budget to identify available funds, such as bonuses, tax returns, or savings. For instance, a borrower earning $60,000 annually might allocate 20% of their $3,000 tax refund toward a lump-sum payment. Finally, they must communicate clearly with their loan servicer to ensure the payment is applied correctly. By taking these steps, borrowers can maximize the impact of a $10,000 deduction and move closer to becoming debt-free.

Forgiving Student Loans: Strategies to Erase Your Debt Burden

You may want to see also

Explore related products

$12.95 $22.99

![]()

Tax Refunds: Offset programs may deduct 10,000 from tax refunds to repay student loans

For those burdened by student loans, the prospect of a tax refund can feel like a lifeline. But a looming question casts a shadow: will the government intercept a portion, specifically $10,000, to chip away at your debt? The answer lies in the complex world of tax refund offsets, a program designed to recoup unpaid debts owed to federal agencies.

Here's the crux: if you're in default on your federal student loans, the Treasury Offset Program (TOP) can garnish your tax refund to satisfy the outstanding balance. This means that instead of receiving your full refund, a significant chunk, potentially up to $10,000, could be diverted directly to your loan servicer.

Understanding the mechanics is crucial. The process begins when your loan servicer reports your default to the Department of Education. This triggers a review by the TOP, which then determines if you owe any debts eligible for offset. If so, they'll notify you in writing before taking any action. It's important to note that the $10,000 figure isn't a fixed amount; the actual deduction depends on the total outstanding balance of your defaulted loans.

This system, while aimed at recouping taxpayer funds, can be a harsh reality for borrowers already struggling financially. The sudden loss of a tax refund, often relied upon for essential expenses, can exacerbate existing hardships. Proactive measures are key. If you're at risk of default, explore repayment options like income-driven plans or loan consolidation. Contact your loan servicer immediately to discuss potential solutions and avoid the consequences of default, including tax refund offsets.

Student Loan Forgiveness: How Many Borrowers Have Benefited So Far?

You may want to see also

Frequently asked questions

The $10,000 student loan forgiveness is part of a federal program announced in 2022. Once your application is approved and processed, the deduction will be applied directly to your loan balance. Timing varies, but eligible borrowers should expect to see the deduction within several weeks to months after approval.

Eligibility for the $10,000 deduction depends on your income and the type of federal student loans you hold. Generally, individuals earning less than $125,000 (or $250,000 for married couples) annually are eligible. Loans must be federally held, including Direct Loans and FFELP loans owned by the Department of Education.

The process varies. Some borrowers may receive automatic forgiveness if their income information is already on file with the Department of Education. However, many borrowers will need to submit an application to confirm eligibility and ensure the deduction is applied. Check the Federal Student Aid website for updates and application details.