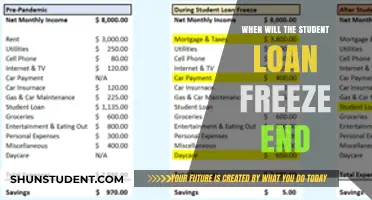

The Student Loan Debt Relief Act has been a highly anticipated piece of legislation aimed at alleviating the financial burden on millions of borrowers. As of now, the exact start date for the implementation of this act remains uncertain, as it is contingent upon several factors, including congressional approval, presidential signing, and administrative setup. Borrowers are eagerly awaiting updates, as the act promises to provide significant relief through measures such as debt forgiveness, reduced interest rates, and expanded repayment options. While the timeline is still unclear, advocates and policymakers continue to push for swift action to address the growing student loan crisis.

Explore related products

What You'll Learn

- Eligibility Criteria: Details on who qualifies for student loan debt relief under the act

- Application Process: Steps borrowers must take to apply for debt relief

- Relief Amounts: Maximum debt forgiveness amounts and income limits specified

- Implementation Timeline: Expected start and end dates for relief distribution

- Legal Challenges: Potential delays due to ongoing lawsuits or legislative hurdles

![]()

Eligibility Criteria: Details on who qualifies for student loan debt relief under the act

The eligibility criteria for student loan debt relief under the act are designed to target specific groups of borrowers, ensuring that the relief reaches those most in need. To qualify, borrowers must meet certain income thresholds, which are based on federal poverty guidelines. For instance, individuals earning up to 200% of the federal poverty level—approximately $27,180 for a single-person household in 2023—are typically eligible for the maximum relief amount. Families with higher household sizes have adjusted income limits, ensuring fairness across different living situations.

Another critical factor is the type of loan held by the borrower. Only federal student loans, such as Direct Loans, Perkins Loans, and Federal Family Education Loans (FFEL) held by the Department of Education, qualify for relief. Private loans, unfortunately, are excluded from this program. Borrowers must also be in good standing with their loans, meaning they should not be in default unless they have made satisfactory arrangements to rehabilitate their loans. This ensures that the relief benefits those who have actively managed their debt responsibly.

The act also considers the borrower’s enrollment status during specific periods. For example, borrowers who were enrolled in college during the COVID-19 pandemic may receive additional consideration, as they faced unique financial challenges during that time. Similarly, those who received Pell Grants, a marker of significant financial need, are often prioritized for higher relief amounts. This tiered approach aims to provide more substantial support to those with the greatest financial burdens.

Practical steps for borrowers include verifying their loan types through the Federal Student Aid website and ensuring their income documentation is up to date. Borrowers should also monitor official government announcements, as eligibility criteria may evolve based on legislative changes or court rulings. Proactively updating contact information with loan servicers can prevent missing critical updates about the application process. By staying informed and prepared, eligible borrowers can maximize their chances of receiving the relief they qualify for.

Is Student Loan Forgiveness Dead? Analyzing the Current Landscape

You may want to see also

Explore related products

![]()

Application Process: Steps borrowers must take to apply for debt relief

The application process for student loan debt relief under the Student Loan Debt Relief Act is designed to be straightforward, but borrowers must navigate it carefully to ensure eligibility and timely approval. Here’s a step-by-step breakdown to guide you through the process.

Step 1: Verify Eligibility

Before applying, confirm that you meet the criteria for debt relief. Typically, eligibility depends on factors like income level, loan type (federal or private), and repayment status. For instance, borrowers earning below a specified threshold (e.g., $125,000 for individuals or $250,000 for married couples) often qualify for partial or full relief. Use the official government portal to check your eligibility status, as this will save time and prevent unnecessary applications.

Step 2: Gather Required Documentation

Once eligibility is confirmed, compile all necessary documents. This may include tax returns, proof of income, loan statements, and identification. Keep digital copies handy, as most applications are submitted online. If you’re missing any documents, contact your loan servicer or the IRS promptly to avoid delays. Pro tip: Organize files in a single folder for easy access during the application process.

Step 3: Complete the Application

Access the official application portal, which is typically hosted on the Department of Education’s website. Fill out the form accurately, double-checking details like Social Security numbers and loan account information. Incomplete or incorrect applications can result in rejection or delays. If you encounter technical issues, use the provided helpline or support email for assistance.

Step 4: Submit and Follow Up

After submitting your application, you’ll receive a confirmation number or email. Keep this for your records. Monitor your application status through the portal, as processing times can vary. If weeks pass without an update, reach out to the support team to ensure your application is being reviewed. Patience is key, as high application volumes may slow down the process.

Cautions and Tips

Beware of scams targeting borrowers seeking debt relief. Always use official government websites and avoid sharing personal information with unverified sources. Additionally, stay informed about deadlines and updates to the program, as policies may change. For example, some relief programs require annual recertification of income, so mark your calendar to avoid missing critical dates.

The application process for student loan debt relief is manageable with careful preparation and attention to detail. By verifying eligibility, gathering documents, completing the application accurately, and staying proactive, borrowers can maximize their chances of approval. Remember, this relief is a lifeline for many, so take the time to navigate the process correctly.

Supreme Court Ruling: Student Loan Forgiveness Decision Explained

You may want to see also

Explore related products

![]()

Relief Amounts: Maximum debt forgiveness amounts and income limits specified

The Student Loan Debt Relief Act, as proposed, outlines specific relief amounts and income limits to determine eligibility for debt forgiveness. Understanding these parameters is crucial for borrowers seeking financial relief. The act specifies a maximum debt forgiveness amount of $10,000 for eligible borrowers, with an additional $10,000 available for those who received Pell Grants during their undergraduate studies. This means that a borrower who meets the criteria and received a Pell Grant could potentially have up to $20,000 in student loan debt forgiven.

To qualify for this relief, borrowers must meet certain income limits. As of the latest proposals, individuals earning less than $125,000 per year and married couples filing jointly with incomes below $250,000 are eligible. These income thresholds are based on adjusted gross income (AGI) from either the 2020 or 2021 tax year, providing flexibility for borrowers whose financial situations may have changed. It’s essential to gather your tax documents from these years to verify your eligibility before applying for relief.

A key aspect of the relief amounts is their targeted approach. The higher forgiveness amount for Pell Grant recipients acknowledges the disproportionate burden of student debt on lower-income borrowers. For example, a single borrower earning $100,000 annually with $15,000 in student loans and a history of receiving Pell Grants would have $20,000 forgiven, effectively eliminating their debt. In contrast, a borrower without Pell Grant history would receive $10,000 in relief, reducing their debt to $5,000. This tiered system aims to address economic disparities in student debt.

Practical steps to maximize your relief include ensuring your income documentation is accurate and up-to-date. If your income fluctuated between 2020 and 2021, choose the year that best supports your eligibility. Additionally, verify your Pell Grant status through your Federal Student Aid account, as this directly impacts the relief amount you qualify for. Borrowers should also monitor updates from the Department of Education, as implementation details may evolve.

In summary, the relief amounts and income limits specified in the Student Loan Debt Relief Act are designed to provide targeted financial assistance. By understanding these parameters—$10,000 in general relief, $20,000 for Pell Grant recipients, and income limits of $125,000 for individuals and $250,000 for couples—borrowers can better navigate the application process. Staying informed and prepared will ensure you take full advantage of this opportunity to alleviate student loan debt.

Will IRS Tax Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Implementation Timeline: Expected start and end dates for relief distribution

The Student Loan Debt Relief Act's implementation timeline is a critical aspect for borrowers eagerly awaiting financial respite. While the exact dates remain subject to legislative and administrative processes, a phased approach is anticipated. Initial projections suggest that the relief distribution could commence as early as the first quarter of 2024, provided there are no legal challenges or procedural delays. This timeline aligns with the government’s goal to provide swift assistance to eligible borrowers, many of whom have been burdened by debt for years.

Once the program begins, the distribution process is expected to unfold in stages, prioritizing borrowers based on factors such as loan type, income level, and outstanding balance. For instance, individuals with federal Direct Loans and those earning below a specified income threshold may receive relief first. This staggered approach aims to ensure fairness and manage the logistical complexities of processing millions of applications. Borrowers should monitor official announcements for their specific eligibility window, as missing it could delay their relief.

The end date for relief distribution is less certain but is tentatively estimated to fall within 12 to 18 months after the program’s launch. This extended timeframe accounts for potential administrative bottlenecks, appeals, and the need to address edge cases. Borrowers are advised to act promptly upon receiving notification of their eligibility to avoid being placed at the end of the queue. Additionally, staying informed through official channels will be crucial, as updates may alter the timeline.

Practical tips for borrowers include gathering necessary documentation, such as income verification and loan statements, in advance. Those with multiple loan servicers should consolidate their accounts where possible to streamline the process. While the wait may be frustrating, understanding the phased timeline and preparing accordingly can help borrowers navigate the system more effectively. Patience and proactive engagement will be key to securing relief during this unprecedented initiative.

Supreme Court's Decision on Student Loan Forgiveness: What Happened?

You may want to see also

Explore related products

![]()

Legal Challenges: Potential delays due to ongoing lawsuits or legislative hurdles

The fate of the Student Loan Debt Relief Act hangs in the balance, not just on political will, but on the intricate dance of legal challenges and legislative maneuvering. While the Act promises significant relief for millions of borrowers, its implementation timeline remains uncertain due to ongoing lawsuits and potential legislative hurdles. These legal battles, often fueled by ideological divides and financial interests, could significantly delay the Act's rollout, leaving borrowers in limbo.

For instance, consider the case of *Biden v. Nebraska*, where several states challenged the Act's constitutionality, arguing it oversteps executive authority. This lawsuit, currently before the Supreme Court, could set a precedent that either clears the path for implementation or halts it indefinitely. Similarly, challenges based on the Administrative Procedure Act (APA) claim the Act bypassed necessary public comment periods, adding another layer of legal complexity. These cases highlight the fragility of the Act's timeline, demonstrating how a single judicial decision can reshape millions of lives.

Navigating these legal challenges requires a strategic approach. Borrowers should stay informed about case developments through reliable sources like the Department of Education's website or legal news outlets. Understanding the specific arguments in each lawsuit can provide insights into potential outcomes. For example, if the Supreme Court rules against the Act's constitutionality, legislative action would be required to revive it, a process that could take months or even years. Conversely, a favorable ruling could expedite implementation, but borrowers should be prepared for either scenario.

Beyond lawsuits, legislative hurdles pose another threat. Even if legal challenges are overcome, Congress could introduce amendments or budget constraints that delay or dilute the Act's impact. Historically, student loan reform has faced bipartisan resistance, with critics arguing it burdens taxpayers or rewards irresponsible borrowing. To mitigate this risk, advocacy groups and borrowers must maintain pressure on lawmakers, emphasizing the economic benefits of debt relief, such as increased consumer spending and reduced default rates.

Practical steps for borrowers include preparing for multiple scenarios. Continue making payments if they are currently due, but also explore alternative repayment plans or forbearance options in case of delays. Keep detailed records of loan balances and correspondence with servicers, as these may become crucial if disputes arise. Finally, engage with advocacy organizations to amplify your voice and stay updated on collective actions that could influence the Act's trajectory.

In conclusion, while the Student Loan Debt Relief Act holds promise, its start date remains contingent on the resolution of legal and legislative battles. By understanding these challenges and taking proactive steps, borrowers can better navigate the uncertainty and position themselves for relief when it becomes available.

Part-Time Work and Student Loan Forgiveness: What Counts?

You may want to see also

Frequently asked questions

The start date for the Student Loan Debt Relief Act depends on the specific legislation passed and its implementation timeline. As of now, there is no single federal act called the "Student Loan Debt Relief Act," but various proposals and programs (like the Biden administration's debt relief plan) have different timelines. Always check official government sources for the most accurate information.

Relief distribution timelines vary by program. For example, the Biden administration's one-time student loan forgiveness program (if reinstated) could begin disbursing relief within weeks to months after approval, but legal challenges or legislative delays may affect the timeline.

Student loan payments resumed in October 2023 after the pandemic-related pause ended. Debt relief efforts, such as forgiveness programs, are separate from payment resumption. Borrowers should monitor updates from the Department of Education for any changes or new relief initiatives.