The pause on federal student loan payments, interest, and collections, implemented in response to the COVID-19 pandemic, has been a critical financial relief measure for millions of borrowers. Initially set to expire in September 2020, the pause has been extended multiple times, most recently until August 30, 2023. As this deadline approaches, borrowers are eagerly awaiting clarity on whether the pause will end or be extended further. The uncertainty surrounding the resumption of payments has sparked widespread concern, as many borrowers are still grappling with economic instability and the potential burden of restarting loan obligations. Additionally, the ongoing debate over broader student loan forgiveness initiatives adds another layer of complexity to the situation, leaving borrowers in a state of limbo as they await definitive guidance from policymakers.

| Characteristics | Values |

|---|---|

| Current Status | Student loan payments and interest accrual remain paused. |

| End Date of Pause | October 1, 2023 (as of latest updates). |

| Reason for Pause | COVID-19 pandemic relief measures. |

| Interest Accrual During Pause | No interest accrues during the pause period. |

| Payment Requirement During Pause | No payments required; payments made are applied to principal. |

| One-Time Adjustment | Borrowers in repayment or forbearance for certain periods may receive credit toward forgiveness. |

| IDR Account Adjustment | Past months in repayment, forbearance, or deferment count toward IDR forgiveness. |

| Loan Types Covered | Federal student loans held by the U.S. Department of Education. |

| Private Loans Covered | No, private student loans are not included in the pause. |

| Next Steps for Borrowers | Prepare for payments to resume in October 2023. |

| Updates and Announcements | Check official sources like the U.S. Department of Education for updates. |

Explore related products

![NMLS Study Cards: NMLS MLO Test Prep 2025-2026 for the SAFE Mortgage Loan Originator Exam with Practice Test Questions [Full Color Cards]](https://m.media-amazon.com/images/I/61f1NUOp4iL._AC_UY218_.jpg)

![NMLS Study Guide: SAFE Mortgage Loan Originator Test Prep Secrets Book, Full-Length MLO Practice Exam, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71wuD4SQlSL._AC_UY218_.jpg)

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UY218_.jpg)

What You'll Learn

![]()

Current Pause Expiration Date

The current pause on federal student loan payments, interest accrual, and collections activities is set to expire on August 31, 2023. This date marks a critical juncture for millions of borrowers who have benefited from the payment moratorium since March 2020. Established as part of the CARES Act and extended multiple times under both the Trump and Biden administrations, the pause has provided financial relief during the COVID-19 pandemic. However, its impending end raises urgent questions about borrower preparedness and the potential economic impact of resumed payments.

Analytically, the August 31 expiration date is not arbitrary. It aligns with the Biden administration’s efforts to finalize a broader student loan forgiveness plan, which faced legal challenges in the Supreme Court. While the pause has been a lifeline for many, its termination coincides with rising inflation and economic uncertainty, leaving borrowers with limited time to adjust their budgets. Data from the Federal Reserve suggests that over 40 million borrowers have saved an average of $200 to $300 monthly during the pause, funds that may soon need to be reallocated to loan payments.

Instructively, borrowers should take immediate steps to prepare for the resumption of payments. First, log into your loan servicer’s website to review your balance, interest rate, and monthly payment amount. Second, consider enrolling in income-driven repayment (IDR) plans or exploring refinancing options if your credit score allows. Third, set aside a portion of your current budget to simulate loan payments, easing the transition in September. Ignoring these steps could lead to financial strain or delinquency once payments restart.

Persuasively, the August 31 deadline underscores the need for systemic reform in student loan policy. While the pause has been a temporary solution, it highlights the long-term challenges of rising tuition costs and unsustainable debt burdens. Advocacy groups argue that a one-time forgiveness program, coupled with affordable repayment plans, is essential to prevent future crises. Borrowers should use this window to engage with policymakers, urging them to address the root causes of student debt rather than relying on temporary fixes.

Comparatively, the current pause expiration differs from previous extensions in its finality. Earlier deadlines were often tied to pandemic conditions, but this one is linked to broader policy goals, such as the implementation of loan forgiveness and IDR reforms. Unlike past extensions, which were announced with little notice, the August 31 date has been communicated well in advance, giving borrowers more time to plan. However, this also means there is less likelihood of another extension, making proactive preparation essential.

Descriptively, the end of the pause will ripple through the economy, affecting not just individual borrowers but also sectors like housing and consumer spending. For example, a recent survey by Bankrate found that 58% of borrowers are not financially prepared for payments to resume. This could lead to reduced discretionary spending, delayed home purchases, and increased reliance on credit cards. For younger borrowers, aged 25 to 34, who hold the largest share of student debt, the impact could be particularly severe, potentially delaying major life milestones.

In conclusion, the August 31, 2023 expiration date is more than just a deadline—it’s a call to action. Borrowers must act now to review their finances, explore repayment options, and advocate for lasting policy changes. While the pause has provided temporary relief, its end marks the beginning of a new phase in the student debt crisis, one that demands both individual preparedness and collective solutions.

Should You Register for Student Loan Forgiveness? A Quick Guide

You may want to see also

Explore related products

![]()

Potential Extensions by Government

The federal student loan payment pause, initially a temporary relief measure during the COVID-19 pandemic, has been extended multiple times, leaving borrowers in a state of uncertainty. As the current pause is set to expire, the possibility of further extensions by the government looms large, driven by economic, political, and social factors.

Economic Considerations: A Delicate Balancing Act

Extending the student loan payment pause can provide temporary financial relief to millions of borrowers, particularly those struggling with unemployment or underemployment. According to a 2022 survey by the Student Debt Crisis Center, 89% of fully employed borrowers and 93% of partially employed or unemployed borrowers reported that restarting payments would cause financial hardship. However, prolonging the pause also delays the flow of funds into the federal budget, potentially impacting other government programs. A targeted extension, perhaps with means-testing or partial payment requirements, could strike a balance between borrower relief and fiscal responsibility.

Political Maneuvering: A High-Stakes Game

The decision to extend the student loan payment pause is not merely economic but also deeply political. With midterm elections approaching, both parties are keenly aware of the issue's salience among young voters. Democrats, in particular, may view an extension as a way to shore up support among their base, while Republicans might criticize it as fiscally irresponsible. A strategic extension, timed to coincide with key electoral milestones, could become a bargaining chip in broader legislative negotiations.

Administrative Hurdles: Preparing for the Inevitable

Restarting student loan payments after an extended pause is no small feat. Loan servicers must update borrower accounts, recalculate interest, and communicate changes to millions of individuals. A sudden resumption of payments could overwhelm these systems, leading to errors and confusion. A phased extension, with a clear timeline and communication plan, would allow servicers to prepare adequately and minimize disruptions. For instance, a 3-month extension with a staggered restart plan could help borrowers and servicers alike.

Long-Term Implications: A Double-Edged Sword

While short-term extensions provide immediate relief, they also delay addressing the underlying issues of student loan affordability and accessibility. Each extension raises questions about the long-term viability of the current system. A more comprehensive approach, combining targeted extensions with reforms such as income-driven repayment plans or loan forgiveness programs, could offer a sustainable solution. For example, expanding the Public Service Loan Forgiveness program or introducing a means-tested forgiveness plan for low-income borrowers could alleviate the burden on vulnerable populations.

As the government weighs its options, borrowers must stay informed and prepared. Monitoring official announcements, understanding repayment options, and creating a budget for potential payments are essential steps. While the future of the student loan payment pause remains uncertain, a proactive and informed approach can help navigate the challenges ahead.

Student Loan Forgiveness for Clinical Medical Assistants: What You Need to Know

You may want to see also

Explore related products

![]()

Impact on Borrower Payments

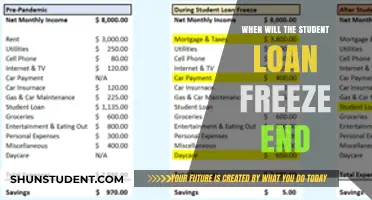

The end of the student loan forgiveness pause will trigger a cascade of financial adjustments for millions of borrowers. Payments, which have been suspended since March 2020, will resume, and interest will begin accruing again. This shift will require careful planning and budgeting, especially for those who have grown accustomed to allocating their income without this monthly obligation.

Consider the practical steps borrowers must take. First, review your loan servicer’s contact information and ensure your address and email are up to date. Next, reassess your budget to accommodate the reinstated payments. For example, if your monthly payment was $300 before the pause, factor that amount back into your expenses. Tools like budgeting apps or spreadsheets can help visualize where adjustments are needed. Prioritize cutting discretionary spending or redirecting funds from non-essential categories to cover the renewed obligation.

The impact varies widely depending on individual circumstances. Borrowers in lower-income brackets or those with multiple loans may face greater challenges. For instance, a borrower with $40,000 in debt at a 6% interest rate could see monthly payments of around $400. If they’ve been allocating that money toward rent or groceries during the pause, resuming payments could strain their finances. Conversely, higher-earning borrowers may find the transition smoother, especially if they’ve saved the equivalent of their monthly payments during the pause.

To mitigate the shock, explore repayment options proactively. Income-driven repayment plans, which cap payments at a percentage of discretionary income, can provide relief. For example, the Pay As You Earn (PAYE) plan limits payments to 10% of discretionary income for eligible borrowers. Additionally, consider refinancing if you have a stable job and good credit, though this forfeits federal benefits like forgiveness programs. Finally, stay informed about any extensions or policy changes, as last-minute adjustments could alter the timeline and impact your strategy.

In summary, the end of the student loan forgiveness pause demands immediate action and strategic planning. By updating your information, adjusting your budget, and exploring repayment options, you can navigate the transition with greater financial stability. The key is to act now, not later, to avoid being caught off guard when payments resume.

Stop Student Loan Forgiveness Calls: Effective Strategies to Remove Your Number

You may want to see also

Explore related products

![]()

Legal Challenges to the Pause

The student loan forgiveness pause, implemented under the CARES Act in response to the COVID-19 pandemic, has faced numerous legal challenges that threaten its continuation. These challenges stem from lawsuits filed by states and organizations arguing that the pause exceeds executive authority or violates administrative procedures. For instance, in 2021, a coalition of Republican-led states sued the Biden administration, claiming the extension of the pause was unlawful. While this lawsuit was dismissed on procedural grounds, it highlighted the ongoing legal vulnerabilities of the policy. Understanding these challenges is crucial for borrowers, as they directly impact when—or if—payments will resume.

One of the primary legal arguments against the pause revolves around the Heroes Act of 2003, which grants the Secretary of Education the authority to waive certain provisions of federal student loan statutes during national emergencies. Critics contend that the repeated extensions of the pause stretch this authority beyond its intended scope. For example, the most recent extension in August 2022 was challenged by a group of student loan servicers, who argued that the Department of Education failed to provide adequate justification for the continued relief. This case underscores the importance of procedural compliance in administrative law, as courts often scrutinize whether agencies have followed proper rule-making processes.

Another significant challenge arises from the Major Questions Doctrine, a legal principle that requires explicit congressional authorization for actions with vast economic or political significance. Opponents of the pause argue that forgiving billions in student debt—even temporarily—constitutes a major question that cannot be resolved through executive action alone. This doctrine was central to the Supreme Court’s 2023 decision in *Biden v. Nebraska*, which struck down the administration’s broader student debt cancellation plan. While the pause itself was not directly addressed, the ruling set a precedent that could limit the government’s ability to extend relief without congressional approval.

For borrowers, these legal challenges create uncertainty about the future of the pause. Practical steps include monitoring court decisions, preparing for potential payment resumption, and exploring alternative relief options like income-driven repayment plans. Additionally, staying informed about legislative developments is key, as Congress could pass laws to codify or terminate the pause. While the legal battles continue, borrowers should remain proactive in managing their loans to avoid financial strain if the pause ends abruptly. The intersection of law and policy here serves as a reminder that even well-intentioned measures can face significant hurdles in implementation.

Married Couples and $20,000 Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Post-Pause Repayment Options

The end of the student loan payment pause, currently slated for October 2023, will trigger a wave of financial recalibration for millions of borrowers. As the dust settles, understanding your post-pause repayment options becomes paramount.

This isn't just about resuming payments; it's about strategizing for long-term financial health.

Assess Your Situation: Before diving into repayment plans, take stock. Has your income changed since the pause began? Are you carrying other debts? The Department of Education offers a variety of income-driven repayment (IDR) plans that adjust monthly payments based on your earnings and family size. Plans like Pay As You Earn (PAYE) and Revised Pay As You Earn (REPAYE) cap payments at a percentage of your discretionary income, potentially offering significant savings.

For borrowers with high debt relative to income, IDR plans can be a lifeline, preventing default and paving the way for eventual loan forgiveness after 20-25 years of qualifying payments.

Explore Refinancing: If your credit score has improved since you originally took out your loans, refinancing with a private lender could secure a lower interest rate. This can significantly reduce the total cost of your loan over time. However, refinancing federal loans means forfeiting access to IDR plans, loan forgiveness programs, and other federal borrower protections. Weigh the potential savings against the loss of these benefits carefully.

Consider Consolidation: Consolidating multiple federal loans into a single Direct Consolidation Loan can simplify repayment by combining payments. While it won't lower your interest rate (it's the weighted average of your existing loans), it can make managing your debt easier.

Prioritize High-Interest Debt: If you have multiple loans with varying interest rates, focus on paying down the highest-interest loans first. This minimizes the overall interest accrual, saving you money in the long run.

Stay Informed and Proactive: The student loan landscape is constantly evolving. Stay updated on policy changes, new repayment options, and potential forgiveness programs. Don't hesitate to reach out to your loan servicer for guidance and explore resources offered by the Department of Education. Remember, the end of the pause doesn't have to mean financial strain. By carefully evaluating your options and taking proactive steps, you can navigate the post-pause repayment period with confidence and work towards a debt-free future.

Student Loan Forgiveness Blocked: What Borrowers Need to Know Now

You may want to see also

Frequently asked questions

As of the latest updates, the student loan payment pause is set to end on October 1, 2023. Borrowers will need to resume payments starting in October 2023.

As of now, there are no official announcements of further extensions beyond October 1, 2023. Borrowers should prepare to resume payments unless new legislation or executive action is announced.

If you fail to make payments after the pause ends, your loans will go into delinquency, and eventually, default. This can negatively impact your credit score and result in additional fees or collection actions. It’s important to contact your loan servicer to discuss repayment options if needed.