The question of when the Supreme Court will decide on the fate of student loan forgiveness has become a pressing concern for millions of borrowers across the United States. Following the Biden administration's announcement of a plan to cancel up to $20,000 in federal student debt for eligible borrowers, the initiative has faced numerous legal challenges, halting its implementation. The case has now reached the Supreme Court, which is expected to rule on the constitutionality and legality of the program. With oral arguments already heard, borrowers, policymakers, and advocates are eagerly awaiting the Court’s decision, which could come as early as June 2023. The outcome will not only determine the financial future of millions but also set a precedent for executive authority in debt relief measures.

| Characteristics | Values |

|---|---|

| Expected Decision Date | No official date announced; anticipated in late June or early July 2023. |

| Case Name | Biden v. Nebraska and Department of Education v. Brown. |

| Issue | Legality of President Biden's student loan forgiveness plan. |

| Plan Details | Up to $20,000 in forgiveness for Pell Grant recipients; $10,000 for others. |

| Legal Basis | HEROES Act of 2003, which allows loan modifications during national emergencies. |

| Current Status | Oral arguments completed in February 2023; awaiting Supreme Court ruling. |

| Key Arguments | Government's authority vs. separation of powers and standing of plaintiffs. |

| Potential Outcomes | Plan upheld, struck down, or modified; impact on millions of borrowers. |

| Political Implications | Significant for Biden administration and 2024 elections. |

| Last Update | As of October 2023, no decision has been publicly announced. |

Explore related products

What You'll Learn

![]()

Timeline for Decision Announcement

The Supreme Court's decision on student loan forgiveness is a highly anticipated event, with millions of borrowers eagerly awaiting the outcome. While the Court has not yet announced a specific date for the decision, historical trends and procedural rules provide some insight into the potential timeline. Typically, the Supreme Court hears oral arguments in the fall and spring terms, with decisions released by the end of June. Given that oral arguments for this case were heard in February 2023, it is reasonable to expect a decision by late June 2023. However, the Court may expedite or delay the decision based on the complexity of the case and its docket priorities.

Analyzing past cases involving significant policy issues, such as *Obergefell v. Hodges* (2015) and *National Federation of Independent Business v. Sebelius* (2012), reveals that high-profile decisions often come down to the wire in June. This pattern suggests that the student loan forgiveness case could follow a similar trajectory. Borrowers should remain vigilant and monitor official Court announcements, as the decision will have immediate implications for loan repayment plans and financial strategies.

For those directly affected, preparing for various outcomes is crucial. If the Court rules in favor of forgiveness, borrowers should be ready to verify their eligibility and understand the scope of debt relief. Conversely, if the program is struck down, revisiting repayment options and exploring alternative relief programs, such as income-driven repayment plans or public service loan forgiveness, becomes essential. Financial advisors recommend creating a contingency plan to manage potential changes in monthly obligations.

Comparing this timeline to other major Court decisions highlights the importance of patience and proactive planning. Unlike lower court rulings, Supreme Court decisions are final and carry broad implications, necessitating a thoughtful approach. Borrowers can use the waiting period to gather necessary documentation, such as loan statements and income verification, to streamline the post-decision process. Staying informed through reliable sources, such as the Court’s official website or trusted legal news outlets, ensures timely action once the ruling is announced.

Instructively, the timeline for the decision announcement underscores the need for borrowers to balance anticipation with practical preparation. While the exact date remains uncertain, historical patterns and procedural norms suggest a June 2023 release. By understanding this timeline and taking proactive steps, individuals can navigate the outcome with greater confidence and clarity, regardless of the Court’s ruling.

Are Federal Student Loans Forgiveable or a Scam?

You may want to see also

Explore related products

![]()

Potential Legal Arguments Review

The Supreme Court's decision on student loan forgiveness hinges on a complex interplay of constitutional and statutory arguments. One key legal contention revolves around the HEROES Act, the law invoked by the Biden administration to justify broad loan cancellation. Critics argue that the Act, designed to provide relief to military service members, does not grant the executive branch authority to forgive loans en masse without explicit congressional approval. Proponents counter that the Act’s language allows for modifications to loan terms during national emergencies, such as the COVID-19 pandemic. This debate will likely center on the scope of executive power and the limits of statutory interpretation, with justices scrutinizing whether the administration overstepped its authority.

Another critical argument focuses on standing, a procedural hurdle that could derail the case entirely. For the Supreme Court to rule on the merits, plaintiffs must demonstrate concrete harm caused by the loan forgiveness program. Challengers, including states and individual borrowers, argue that the program reduces tax revenue or creates financial inequities. However, the Court may question whether these injuries are sufficiently direct and traceable to the policy. If standing is denied, the case could be dismissed without a ruling on the program’s legality, leaving the issue unresolved and potentially delaying relief for millions of borrowers.

A third legal argument centers on the separation of powers and the role of Congress in fiscal policy. Opponents of the program contend that forgiving trillions in debt constitutes a legislative act, which, under the Constitution, is the exclusive domain of Congress. They argue that the executive branch cannot unilaterally redistribute wealth on such a massive scale. Supporters, however, point to historical precedents where the executive branch has exercised broad authority during crises, such as pandemic-related eviction moratoriums. The Court’s decision here will likely reflect its broader views on the balance of power between the branches.

Finally, the equal protection clause of the 14th Amendment could emerge as a peripheral but impactful argument. Some critics claim that loan forgiveness disproportionately benefits higher-income borrowers, creating an inequitable distribution of relief. While this argument is less central than others, it could sway justices concerned about fairness and the program’s broader societal implications. If the Court finds merit in this claim, it might require the administration to restructure the program to address disparities, further complicating its implementation.

In navigating these arguments, the Supreme Court’s decision will not only determine the fate of student loan forgiveness but also set precedents for executive authority, statutory interpretation, and the limits of federal power. Borrowers, policymakers, and legal scholars alike await a ruling that will reshape the landscape of education finance and constitutional law.

Will Student Loans Be Forgiven? Court Cases and Potential Outcomes

You may want to see also

Explore related products

![]()

Impact on Borrowers Nationwide

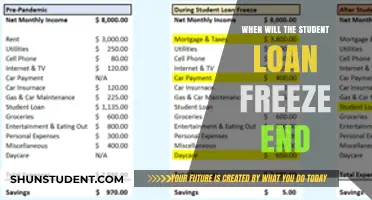

The Supreme Court’s decision on student loan forgiveness will reshape the financial trajectories of millions of borrowers nationwide. For those carrying balances under $12,000—a group representing nearly one-third of all federal student loan holders—full forgiveness could eliminate their debt entirely. This demographic, often comprising younger graduates or those in low-income brackets, would experience immediate relief, freeing up monthly income for essentials like rent, groceries, or savings. Conversely, borrowers with higher balances, such as graduate students or long-term debtors, would see partial relief but still face significant financial obligations. The ripple effect of this decision will vary dramatically based on individual debt levels, underscoring the need for borrowers to assess their balances and plan accordingly.

Consider the psychological impact of this ruling, which extends beyond mere numbers. For borrowers drowning in six-figure debt, even partial forgiveness could alleviate the constant stress of repayment, improving mental health and overall well-being. Studies show that student loan debt is linked to higher rates of anxiety and depression, particularly among younger adults aged 25–34. A favorable decision could lift this burden, enabling borrowers to focus on career growth, family planning, or entrepreneurship. Conversely, a ruling against forgiveness might exacerbate financial strain, potentially leading to defaults or delayed milestones like homeownership. Understanding this emotional dimension is crucial for borrowers preparing for either outcome.

Geographically, the impact will be uneven, reflecting disparities in educational costs and borrowing patterns. States with high tuition rates, such as New Hampshire and Connecticut, where average student debt exceeds $39,000, will see more pronounced effects compared to states like Utah or Wyoming, where averages hover around $19,000. Borrowers in urban areas, often burdened with higher living costs, may find forgiveness particularly transformative, while rural borrowers might experience more modest benefits. Policymakers and financial advisors should tailor resources to address these regional differences, ensuring equitable support for all borrowers.

Finally, the decision will influence long-term financial behaviors nationwide. Borrowers who receive forgiveness may redirect funds toward retirement accounts, emergency savings, or investments, fostering greater financial stability. For instance, a 30-year-old borrower saving $200 monthly post-forgiveness could accumulate over $250,000 by age 65, assuming a 7% annual return. Conversely, those without relief may need to adopt stricter budgeting strategies, such as the 50/30/20 rule (50% needs, 30% wants, 20% savings), to manage ongoing payments. Regardless of the outcome, borrowers should proactively review their financial plans, leveraging tools like debt calculators or consulting certified financial planners to navigate this pivotal moment.

Biden's Student Loan Forgiveness Plan: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Political and Economic Implications

The Supreme Court’s decision on student loan forgiveness will reshape the political landscape by forcing parties to redefine their stances on government intervention in personal debt. Democrats, who championed forgiveness as a tool for economic equity, risk losing a key campaign promise if the Court rules against them. Republicans, who framed forgiveness as fiscal irresponsibility, may capitalize on a favorable ruling to solidify their anti-spending narrative. However, a split decision could muddy the waters, leaving both parties scrambling to reinterpret the ruling for their base. This isn’t just about ideology—it’s about electoral strategy in 2024 and beyond.

Economically, the Court’s ruling will act as a shockwave through consumer spending and inflation. If forgiveness proceeds, an estimated $400 billion in canceled debt could free up monthly budgets for 40 million borrowers, potentially boosting discretionary spending in sectors like retail and housing. However, critics argue this could exacerbate inflation by injecting demand without increasing supply. Conversely, a rejection of forgiveness would leave borrowers with an average monthly payment of $200–$300, reducing disposable income and slowing economic growth. The Federal Reserve’s interest rate decisions will need to account for this outcome, adding a layer of complexity to monetary policy.

A lesser-discussed implication is the precedent this decision sets for executive power. If the Court upholds the Biden administration’s use of the HEROES Act to justify forgiveness, it could embolden future presidents to bypass Congress on other economic issues, from healthcare to climate policy. If struck down, it reinforces legislative supremacy, limiting presidential action in crises. This isn’t merely a legal footnote—it’s a blueprint for how much authority the executive branch can wield in economic emergencies, with ripple effects for decades.

Finally, the decision will expose the fault lines in generational and racial economic disparities. Black and Latino borrowers, who hold disproportionately higher student debt relative to income, stand to gain the most from forgiveness, narrowing the racial wealth gap. Younger voters, already skeptical of institutional efficacy, may view a rejection as further proof of systemic indifference to their financial struggles. Conversely, older generations, many of whom paid off loans without relief, might perceive forgiveness as unfair. The Court’s ruling won’t just determine economic outcomes—it’ll shape perceptions of fairness across demographic divides.

Student Loan Forgiveness: Who Bears the Hidden Costs?

You may want to see also

Explore related products

![]()

Historical Context of Loan Forgiveness

The concept of loan forgiveness is not a modern invention but a policy tool with deep historical roots, often employed to address societal inequities or stimulate economic growth. One of the earliest examples dates back to the 19th century, when the U.S. government forgave debts owed by farmers during economic depressions to prevent widespread bankruptcy and stabilize rural communities. This precedent set the stage for future forgiveness programs, demonstrating that debt relief could serve as both a moral and practical solution to systemic challenges.

During the 20th century, loan forgiveness evolved into a mechanism for incentivizing public service. The National Defense Education Act of 1958, for instance, offered loan forgiveness to students pursuing careers in education, science, and mathematics, a response to the Soviet Union’s launch of Sputnik and the subsequent push to strengthen American education and innovation. Similarly, the Public Service Loan Forgiveness (PSLF) program, established in 2007, aimed to encourage professionals to work in underserved areas by forgiving their student loans after 10 years of qualifying payments. These programs highlight how forgiveness has been strategically used to align individual career choices with national priorities.

The historical context also reveals the contentious nature of loan forgiveness. Critics have long argued that such programs unfairly burden taxpayers and create moral hazard, while proponents emphasize their role in addressing systemic inequalities. For example, the 1970s saw debates over whether forgiving loans for minority and low-income students would perpetuate dependency or serve as a corrective measure for historical injustices. These debates continue today, shaping the Supreme Court’s considerations in the current student loan forgiveness case.

A comparative analysis of international loan forgiveness programs offers additional insights. Countries like Germany and Norway have implemented tuition-free higher education, reducing the need for student loans altogether. In contrast, the U.S. has relied on a patchwork of forgiveness programs, often with stringent eligibility criteria. This comparison underscores the unique challenges of the American system, where student debt has ballooned to over $1.7 trillion, making forgiveness a pressing issue for millions of borrowers.

Practical tips for understanding the historical context include examining legislative records, presidential archives, and economic reports from key periods. For instance, the Federal Register provides detailed accounts of the PSLF program’s inception, while Congressional hearings from the 1970s offer firsthand perspectives on early debates. By studying these sources, one can trace the evolution of loan forgiveness and its shifting rationale—from economic stabilization to social equity to workforce development. This historical lens is crucial for predicting how the Supreme Court might rule on the current case, as it reflects broader trends in policy-making and societal values.

Alabama Tax Benefits: Student Loan Forgiveness Explained for Borrowers

You may want to see also

Frequently asked questions

The Supreme Court is expected to issue its decision on student loan forgiveness by the end of its current term, which typically concludes in late June or early July 2023.

The Supreme Court is reviewing the legality of the Biden administration’s student loan forgiveness program, which aims to cancel up to $20,000 in federal student loan debt for eligible borrowers.

If the Supreme Court rules against the program, the student loan forgiveness plan will likely be blocked, and borrowers will remain responsible for their existing loan balances. Payments and interest would resume as scheduled.