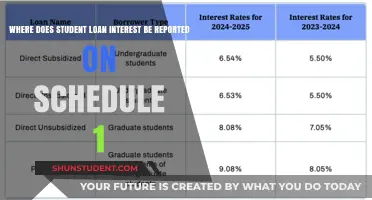

When filing your tax return, knowing where to report student loan interest can help you claim valuable deductions and reduce your taxable income. For U.S. taxpayers, student loan interest is typically reported on Schedule 1 (Form 1040) under the Additional Income and Adjustments to Income section. Specifically, you’ll enter the amount of interest paid during the tax year on line 21 of Schedule 1, labeled Student loan interest deduction. This deduction can lower your adjusted gross income (AGI) by up to $2,500, depending on your income level and eligibility. After completing Schedule 1, transfer the deduction amount to line 10 of your Form 1040. Be sure to have Form 1098-E from your loan servicer, which details the interest paid, to accurately report this information. Consulting IRS guidelines or a tax professional can ensure you maximize this benefit while staying compliant with tax laws.

| Characteristics | Values |

|---|---|

| Tax Form to Use | IRS Form 1040 or Form 1040-SR (Schedule 1 is no longer required as of 2023) |

| Line Number on Form 1040 | Line 13 (Above-the-line deduction for student loan interest) |

| Maximum Deduction Amount | $2,500 per year (phase-outs apply based on income) |

| Income Phase-Out Limits (Single) | Begins at $75,000 AGI, phases out completely at $90,000 AGI |

| Income Phase-Out Limits (Married) | Begins at $150,000 AGI, phases out completely at $180,000 AGI |

| Eligible Loans | Qualified education loans used for tuition, fees, and other education expenses |

| Eligibility Requirement | Taxpayer must be legally obligated to pay the interest |

| Documentation Needed | Form 1098-E (Student Loan Interest Statement) from the lender |

| Filing Status Restriction | Cannot claim if married filing separately |

| Carryover of Unused Interest | Not allowed; unused interest cannot be carried forward to future years |

| Refundability | Non-refundable (reduces taxable income but does not generate a refund) |

| Tax Year Applicability | Tax year 2023 and beyond (check IRS updates for changes) |

Explore related products

What You'll Learn

![]()

Form 1098-E: Reporting Interest Received

When it comes to reporting student loan interest on your tax return, Form 1098-E plays a crucial role. This form is specifically designed to report the amount of interest you paid on qualified student loans during the tax year. Lenders are required to send you a 1098-E if you paid $600 or more in student loan interest. If you don’t receive this form but believe you’ve paid the required amount, contact your loan servicer immediately to request it. The 1098-E includes important details such as the lender’s name, your account number, and the exact amount of interest paid, which you’ll need to accurately report on your tax return.

To add student loan interest to your tax return using Form 1098-E, you’ll need to transfer the interest amount from the 1098-E to Schedule 1 (Form 1040). On Schedule 1, look for line 21, labeled "Student loan interest deduction." Enter the interest amount reported on your 1098-E here. This deduction is an adjustment to income, meaning you can claim it even if you don’t itemize deductions. Ensure the amount matches exactly what’s on the 1098-E to avoid discrepancies that could trigger an IRS review. If you paid interest to multiple lenders, add up all the amounts from each 1098-E and report the total on line 21.

It’s important to note that not all student loan interest qualifies for this deduction. The interest must be on a qualified student loan, which is a loan taken out solely to pay for higher education expenses for you, your spouse, or your dependent. Additionally, there are income limits for claiming this deduction. For the 2023 tax year, for example, the deduction begins to phase out for single filers with modified adjusted gross income (MAGI) above $70,000 and is completely phased out at $85,000. For married filing jointly, the phaseout range is $140,000 to $170,000. Ensure you meet these criteria before claiming the deduction.

If you’re unsure about any part of Form 1098-E or the deduction process, consider using tax software or consulting a tax professional. These resources can help you navigate the specifics of your situation and ensure you’re maximizing your deduction while staying compliant with IRS rules. Remember, the student loan interest deduction can reduce your taxable income by up to $2,500, so it’s worth taking the time to report it correctly.

Finally, keep a copy of your Form 1098-E and any related documentation with your tax records. This will be useful in case of an audit or if you need to refer back to the information in the future. Properly reporting student loan interest on your tax return not only helps you take advantage of available deductions but also ensures you’re meeting your tax obligations accurately and efficiently.

Understanding When Student Loan Interest Rates Are Determined Annually

You may want to see also

Explore related products

![]()

Line 21 (Form 1040): Interest Deduction Entry

When filing your federal tax return, you may be eligible to deduct the interest paid on your student loans, which can reduce your taxable income. This deduction is reported on Line 21 of Form 1040, titled "Interest Deduction Entry." To claim this deduction, you must meet certain eligibility criteria, such as having a qualified student loan and not exceeding specific income limits. The student loan interest deduction allows you to deduct up to $2,500 of the interest paid during the tax year, depending on your income and filing status.

To add student loan interest on Line 21 (Form 1040), start by gathering your Form 1098-E, which is provided by your loan servicer and details the amount of interest you paid during the year. If you did not receive this form but paid at least $600 in student loan interest, you should still be able to claim the deduction. Enter the total eligible interest paid on Line 21 of your Form 1040. This line is specifically designated for the student loan interest deduction and is part of the "Adjusted Gross Income" section of the form. Ensure you do not include any loan payments or capitalized interest—only the actual interest paid qualifies for this deduction.

Before completing Line 21, verify that you meet the IRS requirements for claiming the student loan interest deduction. For instance, the loan must have been used for qualified higher education expenses, and you must be legally obligated to pay the interest. Additionally, your income must fall within the phase-out limits set by the IRS. For tax year 2023, the deduction begins to phase out for single filers with modified adjusted gross income (MAGI) above $70,000 and is completely phased out at $85,000. For married filing jointly, the phase-out range is $145,000 to $175,000. If you qualify, proceed to enter the deductible amount on Line 21.

It’s important to note that the student loan interest deduction is an "above-the-line" deduction, meaning you can claim it even if you do not itemize your deductions. This makes it a valuable tax benefit for many taxpayers. After entering the eligible interest on Line 21, the amount will reduce your adjusted gross income, potentially lowering your overall tax liability. Double-check your calculations and ensure the amount matches the interest reported on your Form 1098-E or other documentation.

If you are unsure about how to calculate or report the deduction, consider using tax software or consulting a tax professional. They can help ensure you maximize your deduction while complying with IRS rules. Properly completing Line 21 (Form 1040) for student loan interest can provide significant tax savings, so take the time to review your eligibility and accurately report the information. This small step can make a meaningful difference in your tax return.

Understanding Unpaid Interest on Student Loans: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Eligibility Criteria for Deduction Limits

When determining where to add student loan interest on your tax return, understanding the eligibility criteria for deduction limits is crucial. The IRS allows taxpayers to deduct a portion of the interest paid on qualified student loans, but this benefit is subject to specific rules. To be eligible, the loan must have been taken out solely for qualified higher education expenses, such as tuition, fees, books, supplies, and room and board, for the taxpayer, their spouse, or dependents. The loan must also have been used for education provided at an eligible institution, which includes most accredited colleges, universities, and vocational schools.

One key eligibility criterion for the student loan interest deduction is the taxpayer’s income level. The deduction is phased out for taxpayers with modified adjusted gross income (MAGI) above certain thresholds. For the tax year 2023, the phaseout begins at $75,000 for single filers and $150,000 for married couples filing jointly. The deduction is completely phased out at $90,000 for single filers and $180,000 for married couples filing jointly. If your income falls within these ranges, your deduction amount will be reduced proportionally. It’s important to calculate your MAGI accurately to determine if you qualify for the full deduction or a partial one.

Another eligibility requirement is that the taxpayer must be legally obligated to pay the interest on the student loan. This means that if a parent takes out a loan for their child’s education, the parent—not the child—is eligible for the deduction, provided they meet the income criteria. Additionally, the student must have been enrolled at least half-time in a degree, certificate, or other program leading to a recognized educational credential during the academic period covered by the loan. This ensures that the loan is directly tied to qualified educational expenses.

The deduction limit for student loan interest is capped at $2,500 per year, and it is claimed as an adjustment to income on Form 1040 or Form 1040-SR. This means you do not need to itemize deductions to claim this benefit. However, you cannot claim the deduction if you are married but filing a separate return, or if someone else can claim you as a dependent on their tax return. These restrictions ensure that the deduction is targeted toward eligible taxpayers who directly benefit from the loan and meet the specified criteria.

Lastly, the student loan interest deduction cannot be claimed for loans from related parties, such as family members, or for qualified tuition plans (529 plans). The interest must be on a loan made or guaranteed by a qualified lender, such as a bank, credit union, or the federal government. Keeping detailed records of your loan payments and interest statements is essential to accurately report the deduction on your tax return. By understanding these eligibility criteria and deduction limits, you can ensure compliance with IRS rules and maximize your potential tax savings.

Tax-Deductible Student Loan Interest: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Schedule 1: Additional Income Adjustments

When filing your federal tax return, Schedule 1: Additional Income and Adjustments is a crucial form for reporting certain types of income and deductions, including student loan interest. This form is used to calculate your adjusted gross income (AGI) and is directly tied to your Form 1040. If you’ve paid interest on a qualified student loan during the tax year, you may be eligible to deduct up to $2,500 of that interest, which can reduce your taxable income. To claim this deduction, you’ll need to complete the Student Loan Interest Deduction section on Schedule 1.

To begin, locate Schedule 1 and scroll down to Line 21, which is labeled "Student loan interest deduction." This is where you’ll enter the amount of student loan interest you paid during the year. Before filling in this line, ensure you meet the eligibility criteria, such as having a qualified student loan and not exceeding the income phaseout limits. If you’re eligible, enter the deductible amount, up to $2,500, on Line 21. This amount will then be subtracted from your total income, reducing your AGI.

If you’re unsure of the exact amount of interest paid, refer to Form 1098-E, which your loan servicer should provide by January 31st. This form details the total interest paid on your qualified student loans during the tax year. Transfer the amount from Form 1098-E to Line 21 on Schedule 1. If you paid interest on multiple loans, ensure the total amount reported on Form 1098-E is accurately entered here.

After completing Line 21, the next step is to ensure this adjustment is carried over to your Form 1040. The total from Schedule 1 will be transferred to Line 11 of your Form 1040, which calculates your AGI. By properly reporting student loan interest on Schedule 1, you can maximize your tax benefits and potentially lower your tax liability.

Finally, double-check your entries on Schedule 1 to avoid errors. Mistakes in reporting student loan interest can delay your refund or result in an audit. If you’re using tax software, it will typically guide you through this process, but it’s still important to review the final forms for accuracy. Completing Schedule 1 correctly ensures you take full advantage of the student loan interest deduction while maintaining compliance with IRS rules.

When to Skip Claiming Student Loan Interest on Your Taxes

You may want to see also

Explore related products

$14.99 $6.99

![]()

TurboTax/Software: Where to Input Interest

When using TurboTax or similar tax software to input student loan interest on your tax return, the process is designed to be user-friendly and intuitive. After launching the software and selecting the appropriate tax year, you’ll typically start by entering your personal information and income details. Once you reach the deductions or credits section, look for the category labeled "Education" or "Student Loan Interest." TurboTax often guides you through this process with prompts, so keep an eye out for questions related to education expenses or loan payments. If you’re unsure where to begin, use the search function within the software and type "student loan interest" to locate the correct section quickly.

In TurboTax, the student loan interest deduction is usually found under the "Deductions & Credits" tab. After selecting this tab, you’ll be prompted to answer questions about your education expenses. When the software asks if you paid student loan interest during the tax year, respond affirmatively. TurboTax will then guide you to the specific field where you can input the exact amount of interest paid. This amount should be reported on the Form 1098-E you received from your loan servicer. Ensure you enter the correct figure, as it directly impacts your deductible amount.

If you’re using a different tax software, the process may vary slightly, but the general steps remain consistent. Look for sections titled "Adjustments to Income" or "Education Credits and Deductions." In these sections, you’ll find a dedicated field for student loan interest. Some software may require you to manually enter the information, while others might import it directly from your Form 1098-E if you’ve uploaded the document. Always double-check the entered amount to avoid errors that could affect your tax return.

For TurboTax users, the software often provides additional guidance to ensure you maximize your deduction. After inputting the interest amount, TurboTax may ask follow-up questions to determine your eligibility for the deduction, such as your income level and filing status. Answer these questions accurately, as they help the software calculate the correct deductible amount. Once completed, the software will automatically transfer the information to the appropriate line on your Form 1040, typically Schedule 1, Line 21.

Finally, before submitting your tax return, review the summary provided by TurboTax or your tax software to confirm that the student loan interest deduction has been correctly applied. If you notice any discrepancies, revisit the education or deductions section to make adjustments. By following these steps, you can confidently input your student loan interest and take full advantage of this valuable tax benefit.

Lower Interest Rates: Which Student Loan Type Fits Your Needs?

You may want to see also

Frequently asked questions

You report student loan interest on Schedule 1 (Form 1040), Line 8e. This amount is then transferred to Form 1040, Line 10, to claim the deduction.

Yes, for tax year 2023, you can deduct up to $2,500 of student loan interest paid during the year, subject to income limits. The deduction phases out for single filers with MAGI between $75,000 and $90,000, and for joint filers between $150,000 and $180,000.

Yes, your lender should send you Form 1098-E, which reports the amount of interest you paid during the year. You’ll need this form to accurately report the interest on your tax return. If you don’t receive it, contact your lender.