Writing about outstanding interest on student loans requires a focus on individuals who are deeply impacted by this financial burden, such as recent graduates, long-term borrowers, and those in low-income professions. These individuals often face challenges in managing accruing interest, which can significantly increase the total repayment amount over time. Highlighting their stories not only sheds light on the systemic issues within student loan programs but also emphasizes the need for policy reforms, interest relief options, and financial literacy initiatives. By addressing their struggles and successes, the narrative can advocate for solutions that alleviate the long-term financial strain of student debt.

Explore related products

What You'll Learn

- Understanding Interest Accrual: How daily or monthly interest compounds on unpaid student loan balances

- Capitalized Interest Explained: When unpaid interest is added to the loan principal

- Avoiding Outstanding Interest: Strategies like in-school payments or interest-only plans

- Impact on Loan Repayment: How outstanding interest increases total repayment amounts over time

- Federal vs. Private Loans: Differences in interest rates, capitalization rules, and repayment options

![]()

Understanding Interest Accrual: How daily or monthly interest compounds on unpaid student loan balances

Understanding how interest accrues on student loans is crucial for borrowers to manage their debt effectively. Interest accrual refers to the process by which interest is added to the unpaid balance of a loan over time. For student loans, this process can occur daily or monthly, depending on the terms of the loan. When interest compounds, it means that the interest itself earns interest, leading to exponential growth in the total amount owed if the loan is not paid down. This compounding effect can significantly increase the overall cost of the loan, making it essential for borrowers to grasp how it works.

Daily interest accrual is common on many student loans, particularly unsubsidized federal loans and private loans. With daily accrual, the interest is calculated based on the outstanding principal balance each day. For example, if a borrower has a $10,000 loan with a 5% annual interest rate, the daily interest rate would be approximately 0.0137% (5% divided by 365 days). Each day, this percentage is applied to the unpaid balance, and the resulting interest is added to the total amount owed. Over time, this daily compounding can cause the balance to grow rapidly, especially if payments are not made regularly. Borrowers should be aware that even small delays in payment can lead to substantial increases in the total debt due to this daily compounding effect.

Monthly interest accrual is less common but still exists in some loan agreements. In this case, interest is calculated once a month based on the principal balance at the beginning of the month. While monthly compounding grows more slowly than daily compounding, it still adds up over time. For instance, a $15,000 loan with a 6% annual interest rate would accrue approximately $75 in interest each month (6% divided by 12 months, then multiplied by $15,000). If payments do not cover this monthly interest, the unpaid interest is capitalized, meaning it is added to the principal balance, and future interest calculations are based on this new, higher amount. This capitalization further accelerates the growth of the loan balance.

To mitigate the impact of compounding interest, borrowers should prioritize making payments that cover at least the accrued interest each month. For those with daily accrual, even small payments can help reduce the principal balance and slow the growth of interest. Additionally, borrowers should explore options like income-driven repayment plans, loan consolidation, or refinancing to lower their interest rates or manage payments more effectively. Understanding the specific terms of their loan, including whether interest compounds daily or monthly, empowers borrowers to make informed decisions and minimize the long-term cost of their student loans.

In conclusion, interest accrual and compounding are key factors in the growing burden of student loan debt. Daily compounding, in particular, can lead to rapid increases in the total amount owed if payments are insufficient or delayed. By comprehending how interest is calculated and added to their balances, borrowers can take proactive steps to manage their loans more effectively. Regular payments, strategic repayment plans, and staying informed about loan terms are essential strategies to combat the effects of compounding interest and work toward financial stability.

Where to File Student Loan Interest: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Capitalized Interest Explained: When unpaid interest is added to the loan principal

Capitalized interest is a critical concept for student loan borrowers to understand, as it directly impacts the total cost of their loans. In simple terms, capitalized interest occurs when unpaid interest is added to the principal balance of a loan. This means the borrower not only owes the original amount borrowed but also the accumulated interest, which then accrues additional interest over time. For student loans, this often happens during periods when payments are deferred, such as during in-school deferment, grace periods, or forbearance. Understanding how and when capitalization occurs is essential to managing student loan debt effectively.

The process of capitalization increases the overall loan balance, making it more expensive to repay. For example, if a borrower has a $10,000 loan with $500 in accrued interest and that interest is capitalized, the new principal balance becomes $10,500. Moving forward, interest will be calculated on this higher amount, resulting in higher total interest costs over the life of the loan. This is particularly concerning for federal student loans, where interest rates can be substantial, and for private loans, which often have even higher rates and less flexible repayment terms. Borrowers must be aware of when capitalization is likely to occur to minimize its impact.

Capitalization typically happens at specific points in the loan lifecycle. For federal student loans, it often occurs at the end of the grace period after graduation, when a deferment period ends, or when a forbearance period concludes. For private loans, capitalization terms vary by lender but can occur under similar circumstances. To avoid or reduce capitalized interest, borrowers can make interest payments during deferment or forbearance periods, even if they are not required. For federal loans, choosing an income-driven repayment plan or consolidating loans may also help manage interest capitalization, depending on the borrower’s eligibility and circumstances.

It’s important for borrowers to review their loan agreements and understand the terms related to interest capitalization. Federal student loans, for instance, may capitalize interest differently depending on the type of loan (e.g., Direct Subsidized vs. Unsubsidized Loans). Private loans often have less favorable terms, and borrowers should carefully examine their contracts to know when capitalization will occur and how much it could add to their debt. Proactive communication with loan servicers can also provide clarity and help borrowers explore options to limit the impact of capitalized interest.

In summary, capitalized interest is a significant factor in the growing burden of student loan debt. By adding unpaid interest to the principal balance, it increases the total amount owed and the overall cost of borrowing. Borrowers can mitigate this by making voluntary interest payments during non-repayment periods, understanding their loan terms, and exploring repayment strategies that minimize capitalization. Awareness and proactive management are key to avoiding the long-term financial consequences of capitalized interest on student loans.

Understanding Student Loans: Types, Interests, and Repayment Strategies

You may want to see also

Explore related products

![]()

Avoiding Outstanding Interest: Strategies like in-school payments or interest-only plans

When it comes to managing student loan debt, avoiding outstanding interest is crucial to prevent the overall cost of borrowing from spiraling out of control. One effective strategy to minimize interest accrual is to make in-school payments, even if they're small. Many students assume that they don't need to start paying back their loans until after graduation, but interest begins accruing as soon as the loan is disbursed. By making payments while still in school, you can significantly reduce the amount of interest that capitalizes and gets added to the principal balance. For instance, paying just $20-$50 per month on a subsidized or unsubsidized loan can save hundreds or even thousands of dollars in interest over the life of the loan.

Another strategy to avoid outstanding interest is to enroll in an interest-only payment plan while in school or during the grace period. This type of plan allows you to pay only the interest that accrues each month, rather than the full principal and interest payment. By doing so, you can prevent interest from capitalizing and keep your loan balance from growing. Interest-only plans are particularly useful for students who have unsubsidized loans, as the government does not pay the interest on these loans while the borrower is in school. By making interest-only payments, you can stay on top of the accruing interest and avoid a larger bill once the grace period ends.

For students who are unable to make full payments while in school, considering a combination of in-school payments and interest-only plans can be a viable option. For example, you could make small in-school payments on subsidized loans, where the government pays the interest, and enroll in an interest-only plan for unsubsidized loans. This hybrid approach allows you to prioritize payments on the loans that are accruing interest at a faster rate, while still making progress on all your loans. Additionally, some lenders offer automatic debit discounts, which can lower your interest rate by 0.25% to 0.50% if you sign up for automatic payments, further reducing the overall cost of borrowing.

It's also essential to explore income-driven repayment plans, which can provide temporary relief from high monthly payments and help you avoid default. These plans calculate your monthly payment based on your income and family size, and may result in a lower payment than the standard 10-year repayment plan. While income-driven plans can be helpful, it's crucial to understand that they may result in more interest accruing over time, as the lower payments may not cover the full amount of interest that accrues each month. To avoid this, consider making extra payments whenever possible to reduce the principal balance and minimize interest accrual.

Lastly, staying informed about your loan terms, interest rates, and repayment options is key to avoiding outstanding interest. Make sure to review your loan agreements, understand the differences between subsidized and unsubsidized loans, and keep track of your loan servicer's contact information. By being proactive and taking advantage of strategies like in-school payments, interest-only plans, and income-driven repayment options, you can effectively manage your student loan debt and minimize the impact of outstanding interest on your finances. Remember, the earlier you start making payments and exploring repayment options, the more you can save in interest over the life of your loans.

Understanding Typical Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

$29.97 $36.27

$19.97 $25.57

![]()

Impact on Loan Repayment: How outstanding interest increases total repayment amounts over time

Outstanding interest on student loans significantly impacts loan repayment by increasing the total amount borrowers must repay over time. When borrowers make minimum payments or defer payments, interest continues to accrue, adding to the principal balance. This process, known as capitalization, results in borrowers paying interest on top of interest, effectively increasing the overall cost of the loan. For example, if a borrower has a $30,000 loan with a 6% interest rate and makes only minimum payments, the interest accrues monthly, causing the total repayment amount to grow exponentially. Understanding this mechanism is crucial for borrowers to grasp how outstanding interest directly inflates their financial obligation.

The longer a borrower takes to repay their student loans, the more pronounced the impact of outstanding interest becomes. Compound interest means that interest is calculated not only on the original principal but also on the accumulated interest from previous periods. As a result, even small delays in repayment or periods of forbearance can lead to substantial increases in the total amount owed. For instance, a borrower who defers payments for a year on a $20,000 loan at 5% interest will see their balance grow by $1,000 in that year alone, assuming no payments are made. This additional amount then becomes part of the principal, further increasing the interest accrued in subsequent years.

Outstanding interest also affects the structure of loan repayments, often extending the repayment period. Many borrowers opt for income-driven repayment plans or extended repayment plans to manage their monthly payments. However, these plans typically result in lower monthly payments, which may not cover the accruing interest. When payments fail to cover the interest, the unpaid interest is capitalized, increasing the loan balance. Over time, this can lead to a situation where the borrower owes more than they originally borrowed, even after making consistent payments. This cycle makes it harder to pay off the loan, as more of each payment goes toward interest rather than reducing the principal.

To mitigate the impact of outstanding interest, borrowers should prioritize paying more than the minimum amount due each month. Even small additional payments can significantly reduce the total interest paid over the life of the loan. For example, paying an extra $50 per month on a $25,000 loan at 7% interest can save thousands of dollars in interest and shorten the repayment period by several years. Additionally, borrowers should explore options like interest rate reductions through autopay or refinancing to lower their interest rates, which can further reduce the total repayment amount.

In conclusion, outstanding interest on student loans has a profound impact on loan repayment by increasing the total amount owed over time. Through capitalization and compound interest, unpaid interest adds to the principal, leading to higher overall costs and potentially longer repayment periods. Borrowers must be proactive in managing their loans by making extra payments, exploring repayment strategies, and seeking ways to reduce their interest rates. By understanding how outstanding interest works, borrowers can take steps to minimize its impact and achieve financial stability more quickly.

When Does Interest Capitalize on Student Loans Under IBR Plans?

You may want to see also

Explore related products

![]()

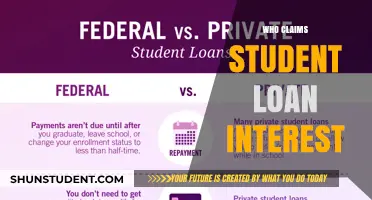

Federal vs. Private Loans: Differences in interest rates, capitalization rules, and repayment options

When addressing outstanding interest on student loans, it’s crucial to understand the differences between federal and private loans, particularly in terms of interest rates, capitalization rules, and repayment options. Interest rates are a primary differentiator. Federal student loans typically offer fixed interest rates set by Congress, which are often lower than private loan rates. For the 2023-2024 academic year, undergraduate federal loans carry a rate of 5.5%, while private loans can range from 4% to 13% or higher, depending on creditworthiness. Federal rates are standardized, whereas private rates are highly variable and influenced by market conditions and the borrower’s credit profile. This makes federal loans a more predictable and often more affordable option for managing interest accrual over time.

Capitalization rules further distinguish federal and private loans. Capitalization occurs when unpaid interest is added to the principal balance, increasing the total amount owed. Federal loans generally capitalize less frequently, such as when a borrower exits their grace period, switches repayment plans, or leaves an income-driven repayment plan. In contrast, private loans may capitalize interest more frequently, often monthly or quarterly, especially if payments are deferred or missed. This means private loan borrowers can see their balances grow faster due to outstanding interest, making it harder to manage debt. Understanding these rules is essential for borrowers to minimize the long-term cost of their loans.

Repayment options are another critical area where federal and private loans differ. Federal loans offer a variety of repayment plans, including income-driven repayment (IDR) plans, which cap monthly payments at a percentage of the borrower’s discretionary income and can lead to loan forgiveness after 20-25 years. Federal loans also provide options like deferment, forbearance, and public service loan forgiveness (PSLF). Private loans, however, rarely offer such flexibility. Repayment terms are typically fixed, and deferment or forbearance options are limited. Some private lenders may offer interest-only payments or temporary payment reductions, but these are not as comprehensive as federal programs. Borrowers with outstanding interest on private loans often face stricter terms, making it harder to manage financial hardship.

For borrowers dealing with outstanding interest, the type of loan they hold significantly impacts their strategy. With federal loans, enrolling in an income-driven plan can reduce monthly payments and prevent interest from overwhelming the borrower. Additionally, making extra payments toward the principal can help reduce capitalized interest over time. For private loans, borrowers should focus on paying more than the minimum to avoid frequent capitalization and explore refinancing options if their credit score has improved, potentially securing a lower interest rate. However, refinancing federal loans into private ones eliminates access to federal repayment benefits, so this decision should be made carefully.

In summary, the differences between federal and private loans in interest rates, capitalization rules, and repayment options have a profound impact on managing outstanding interest. Federal loans offer lower, fixed rates, less frequent capitalization, and flexible repayment plans, making them more borrower-friendly. Private loans, while sometimes necessary, come with higher variable rates, more frequent capitalization, and limited repayment options, requiring borrowers to be proactive in managing their debt. Understanding these distinctions is key to developing an effective strategy for addressing outstanding interest and minimizing the long-term financial burden of student loans.

Deferring Student Loan Interest: Smart Strategies to Save Money

You may want to see also

Frequently asked questions

Outstanding interest on student loans refers to the accumulated interest that has not yet been paid on the loan balance. This interest continues to grow until it is paid off, increasing the total amount owed.

You can find out the outstanding interest on your student loans by logging into your loan servicer's website or by contacting them directly. They will provide you with a breakdown of your loan balance, including the principal and accrued interest.

Yes, you may be able to deduct up to $2,500 of student loan interest paid during the tax year on your federal tax return, subject to certain income limits and eligibility requirements. This deduction can be claimed even if you don't itemize your deductions.

If you don't pay the outstanding interest on your student loans, it will continue to accrue and be capitalized, meaning it will be added to the principal balance of your loan. This can result in a larger loan balance and higher monthly payments over time.

To minimize outstanding interest, consider making interest payments while still in school, paying more than the minimum monthly payment, and exploring loan repayment plans that prioritize interest reduction. Additionally, refinancing your loans at a lower interest rate may also help reduce the total interest paid over the life of the loan.