Understanding the normal interest rate for a student loan is crucial for borrowers as it directly impacts the total cost of repayment. Interest rates on student loans can vary widely depending on factors such as the type of loan (federal or private), the borrower’s credit history, and current market conditions. Federal student loans typically offer fixed rates set by the government, which are often lower than private loans and do not require a credit check. For the 2023-2024 academic year, federal undergraduate loans have rates ranging from 5.5% to 7.53%, while private loans can range from 3% to 14% or higher, depending on the lender and the borrower’s financial profile. Knowing these averages helps students and their families make informed decisions about financing education and managing debt effectively.

| Characteristics | Values |

|---|---|

| Federal Student Loan Rates (2023-2024) | |

| Undergraduate Borrowers | 5.5% |

| Graduate Borrowers | 7.05% |

| PLUS Loans (Parents/Grad Students) | 8.05% |

| Private Student Loan Rates (Average) | |

| Fixed Rates | 4.5% - 12% (depending on creditworthiness) |

| Variable Rates | 1.29% - 12% (depending on creditworthiness and market conditions) |

| Loan Type | |

| Subsidized Federal Loans | Interest does not accrue while in school |

| Unsubsidized Federal Loans | Interest accrues immediately |

| Repayment Terms | 10-25 years (varies by lender and plan) |

| Credit Requirements | Federal loans: No credit check; Private loans: Good credit required |

| Loan Limits | Federal: $31,000 (dependent undergrad); $138,500 (grad/professional) |

| Origination Fees | Federal: 1.057% (2023); Private: Varies by lender |

| Repayment Plans | Standard, Graduated, Income-Driven, etc. |

| Interest Capitalization | Occurs at end of grace period for unsubsidized and private loans |

| Grace Period | 6 months (federal); Varies for private loans |

Explore related products

What You'll Learn

![]()

Federal vs. Private Loan Rates

When considering student loans, understanding the difference between federal and private loan rates is crucial. Federal student loans, which are issued by the U.S. Department of Education, typically offer fixed interest rates that are set by Congress. For the 2023-2024 academic year, undergraduate students can expect to pay 5.5% for Direct Subsidized and Unsubsidized Loans. Graduate students face slightly higher rates, with 7.05% for Direct Unsubsidized Loans, and PLUS Loans for parents and graduate students are set at 8.05%. These rates are generally lower than private loans and come with more flexible repayment options, including income-driven repayment plans and loan forgiveness programs.

Private student loans, on the other hand, are offered by banks, credit unions, and other financial institutions. Their interest rates can be either fixed or variable, and they are often based on the borrower’s creditworthiness. As of recent data, private student loan rates typically range from about 4% to 13%, depending on the lender and the borrower’s credit profile. While some private loans may offer lower rates than federal loans for borrowers with excellent credit, they lack the borrower protections and repayment options that federal loans provide. For instance, private loans rarely offer income-driven repayment plans or loan forgiveness programs.

One key advantage of federal loans is their consistency and predictability. Federal loan rates are standardized and do not fluctuate based on individual financial circumstances, making them accessible to a broader range of students. Additionally, federal loans do not require a credit check for most types of loans, which is particularly beneficial for students with limited or poor credit history. In contrast, private loans often require a credit check, and students with no credit history may need a cosigner to qualify for a competitive rate.

Another important factor to consider is the repayment terms. Federal loans offer a grace period after graduation, typically six months, before payments begin. They also provide deferment and forbearance options in case of financial hardship. Private loans may offer some flexibility, but terms vary widely by lender, and they are generally less forgiving. For example, private lenders are not required to offer income-driven repayment plans, which can make managing loan payments more challenging for borrowers with lower incomes.

In summary, federal student loans generally offer lower, fixed interest rates and more borrower protections compared to private loans. While private loans can sometimes provide lower rates for well-qualified borrowers, they come with higher risks and fewer benefits. Students should exhaust federal loan options before considering private loans, as federal loans provide a safety net that can be invaluable during repayment. Always compare rates, terms, and benefits carefully to make an informed decision that aligns with your financial situation and long-term goals.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Explore related products

![]()

Fixed vs. Variable Interest Rates

When considering student loans, one of the most critical decisions borrowers face is choosing between fixed and variable interest rates. As of recent data, the normal interest rate for federal student loans ranges from 4.99% to 7.54%, depending on the loan type and disbursement date. Private student loans, however, can vary widely, with fixed rates typically ranging from 4% to 12% and variable rates starting as low as 1% to 2% but potentially rising over time. Understanding the difference between fixed and variable rates is essential to making an informed decision.

Fixed interest rates remain constant throughout the life of the loan, meaning the borrower pays the same rate from the first payment to the last. This predictability is a significant advantage, as it allows borrowers to budget effectively without worrying about fluctuations in monthly payments. For example, if you take out a loan with a fixed rate of 6%, that rate will not change, regardless of economic conditions or market trends. This stability is particularly appealing for risk-averse borrowers who prefer knowing exactly how much they will owe each month. However, fixed rates are often higher than the initial rates offered for variable loans, which can make them more expensive in the short term.

On the other hand, variable interest rates are tied to an index, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate, and can fluctuate over time based on market conditions. Initially, variable rates are often lower than fixed rates, making them an attractive option for borrowers seeking to minimize upfront costs. For instance, a variable rate might start at 2%, significantly lower than a fixed rate of 6%. However, this comes with the risk that the rate could increase over time, potentially leading to higher monthly payments. Borrowers who choose variable rates must be comfortable with uncertainty and prepared for the possibility of rising costs, especially in a rising interest rate environment.

The choice between fixed and variable rates often depends on the borrower’s financial situation, risk tolerance, and expectations about future interest rates. If you expect to pay off the loan quickly or believe interest rates will remain low or decline, a variable rate might be advantageous. Conversely, if you plan to take a longer time to repay the loan or anticipate rising interest rates, a fixed rate provides security and peace of mind. It’s also worth noting that some private lenders offer the option to refinance loans later, which can allow borrowers to switch from a variable to a fixed rate or vice versa if their circumstances change.

In summary, fixed interest rates offer stability and predictability, making them ideal for borrowers who prioritize consistent monthly payments. Variable rates, while initially lower, carry the risk of increasing over time, making them better suited for those who are comfortable with uncertainty or expect to pay off their loans quickly. When deciding between the two, borrowers should carefully consider their financial goals, the current interest rate environment, and their tolerance for risk. Understanding these differences ensures that you choose the option that best aligns with your long-term financial strategy.

Understanding the Maximum Interest Rates on Student Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Current Average Student Loan Rates

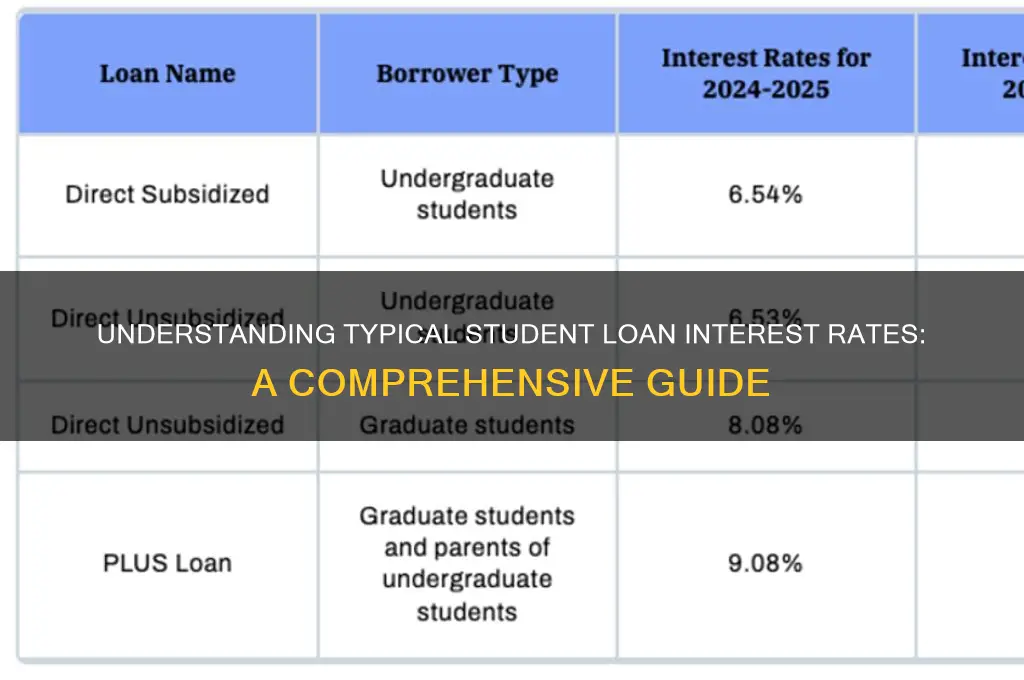

As of the most recent data, the current average student loan interest rates vary depending on the type of loan and the lender. For federal student loans, which are often considered the most borrower-friendly, the interest rates are set by Congress and are typically fixed for the life of the loan. For the 2023-2024 academic year, undergraduate students borrowing through the Direct Loan program can expect an interest rate of 4.99% for Direct Subsidized and Unsubsidized Loans. Graduate students face a higher rate of 6.54% for Direct Unsubsidized Loans, while parents and graduate students taking out PLUS loans are looking at a rate of 7.54%. These federal rates are generally lower than private loan rates and come with additional benefits like income-driven repayment plans and loan forgiveness options.

Private student loan interest rates, on the other hand, are determined by market conditions, the lender, and the borrower’s creditworthiness. As of recent trends, the average private student loan interest rates range from 4.50% to 14.50% for fixed-rate loans and 1.99% to 14.50% for variable-rate loans. Borrowers with excellent credit or a cosigner typically qualify for rates at the lower end of this spectrum, while those with limited credit history or lower credit scores may face significantly higher rates. It’s crucial for borrowers to shop around and compare offers from multiple lenders to secure the best possible rate.

For borrowers with existing student loans, refinancing can be an option to secure a lower interest rate, especially if their financial situation or credit score has improved since they initially took out the loan. Current refinancing rates for private student loans typically range from 4.00% to 9.00% for fixed-rate options and 1.99% to 8.00% for variable-rate options. However, refinancing federal loans into private loans means losing access to federal protections, so borrowers should weigh the pros and cons carefully.

Internationally, student loan interest rates vary widely. In countries like the UK, interest rates for student loans are tied to inflation and can change annually, currently ranging from 3.5% to 6.5%. In contrast, some European countries, such as Germany, offer student loans at very low or even zero interest rates as part of their higher education support systems. Understanding the global context can provide additional perspective for borrowers, especially those considering international study or loan options.

In summary, the current average student loan interest rates depend on the loan type, lender, and borrower’s financial profile. Federal student loans offer fixed rates ranging from 4.99% to 7.54% for the 2023-2024 academic year, while private loan rates vary more widely, typically between 4.50% and 14.50%. Borrowers should carefully consider their options, including refinancing, and explore all available resources to make informed decisions about managing their student loan debt.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Impact of Credit Score on Rates

When considering the normal interest rate for a student loan, it's essential to understand that these rates can vary significantly based on several factors, including the type of loan (federal or private) and the borrower's creditworthiness. Federal student loans, which are issued by the government, typically offer fixed interest rates that are set by Congress and are not dependent on the borrower's credit score. For the 2021-2022 academic year, for instance, the interest rate for undergraduate Direct Loans was 3.73%, while graduate Direct Loans were at 5.28%, and PLUS Loans (for parents and graduate students) were at 6.28%. These rates are generally lower than private loan rates and provide more flexible repayment options.

Private student loans, on the other hand, are heavily influenced by the borrower's credit score. Lenders use credit scores to assess the risk of lending to an individual. A higher credit score indicates a lower risk, which can lead to more favorable loan terms, including lower interest rates. Conversely, a lower credit score may result in higher interest rates or the need for a cosigner to secure the loan. The impact of a credit score on private student loan rates can be substantial, with differences of several percentage points between borrowers with excellent credit and those with fair or poor credit.

For individuals with excellent credit scores (typically above 720), private student loan interest rates can be as low as 3% to 5%, depending on the lender and market conditions. These borrowers are seen as low-risk and are often offered the best available rates. In contrast, borrowers with fair credit scores (around 630 to 689) might see rates ranging from 6% to 12%, while those with poor credit scores (below 630) could face rates of 12% or higher. Some lenders may even deny loans to applicants with very low credit scores, making it difficult for these individuals to secure private financing without a cosigner.

The difference in interest rates based on credit score can significantly affect the total cost of the loan over its lifetime. For example, a $10,000 loan with a 5% interest rate paid over 10 years would result in total payments of approximately $12,748. In contrast, the same loan amount with a 12% interest rate would lead to total payments of about $17,969. This disparity highlights the importance of maintaining a good credit score to secure more affordable student loan options.

To mitigate the impact of a lower credit score, borrowers can take several steps. First, they can work on improving their credit score by paying bills on time, reducing credit card balances, and correcting any errors on their credit report. Additionally, finding a cosigner with a strong credit history can help secure a lower interest rate. Some lenders also offer rate reductions for actions like enrolling in automatic payments or making a certain number of on-time payments. Understanding the relationship between credit scores and interest rates empowers borrowers to make informed decisions and take proactive steps to manage their student loan debt effectively.

Understanding the Latest Interest Rate Changes for Student Loans

You may want to see also

Explore related products

$16.53 $22.99

![]()

Subsidized vs. Unsubsidized Loan Rates

When considering student loans, understanding the difference between subsidized and unsubsidized loan rates is crucial for managing your financial obligations effectively. Subsidized loans are a type of federal student loan available to undergraduate students with demonstrated financial need. The key advantage of subsidized loans is that the government pays the interest on the loan while the borrower is in school at least half-time, during the grace period after leaving school (typically six months), and during any approved deferment periods. This means the amount you owe does not increase during these times. As of recent data, the interest rate for subsidized loans is typically lower than private loans, with rates set annually by the federal government. For example, for the 2023-2024 academic year, the interest rate for Direct Subsidized Loans for undergraduate students was fixed at 5.5%.

On the other hand, unsubsidized loans are available to both undergraduate and graduate students, regardless of financial need. Unlike subsidized loans, the borrower is responsible for paying the interest on unsubsidized loans at all times—during school, the grace period, and deferment. If the borrower chooses not to pay the interest while in school, it accrues and is added to the principal amount of the loan, leading to higher overall costs over time. The interest rates for unsubsidized loans are also set by the federal government and are slightly higher than subsidized rates for undergraduate students but the same for graduate students. For instance, in the 2023-2024 academic year, the interest rate for Direct Unsubsidized Loans was 5.5% for undergraduates and 7.05% for graduate students.

The choice between subsidized and unsubsidized loans often depends on your financial situation and eligibility. Subsidized loans are generally more favorable due to the government’s interest coverage, making them a cost-effective option for eligible students. However, not all students qualify for subsidized loans, as they are need-based. Unsubsidized loans, while less advantageous due to accruing interest, provide a broader accessibility option for students who may not meet the financial need criteria or are pursuing graduate studies.

Another important factor to consider is the long-term cost of each loan type. Since unsubsidized loans accrue interest from the time of disbursement, the total amount repaid can be significantly higher than the original principal. For example, if you borrow $10,000 in unsubsidized loans and do not pay the interest while in school, the interest could capitalize and increase the total loan balance. In contrast, subsidized loans avoid this additional cost, making them a more financially prudent choice for those who qualify.

Lastly, it’s essential to explore all available options before committing to a loan. Federal student loans, both subsidized and unsubsidized, generally offer lower interest rates and more flexible repayment plans compared to private loans. Private student loans often have variable interest rates that can fluctuate over time, potentially leading to higher costs. By understanding the differences between subsidized and unsubsidized loan rates, you can make informed decisions that align with your financial goals and minimize long-term debt. Always review your eligibility, compare interest rates, and consider your repayment capacity before selecting a loan type.

Understanding New Zealand's Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Frequently asked questions

Federal student loan interest rates are set by the U.S. government and vary annually based on the 10-year Treasury note. For the 2023-2024 academic year, rates range from 5.5% for undergraduate Direct Loans to 7.05% for graduate PLUS Loans and 8.05% for parent PLUS Loans.

Private student loan interest rates vary widely depending on the lender, creditworthiness, and loan terms. As of 2023, rates typically range from 4% to 13% for fixed-rate loans and 1% to 12% for variable-rate loans. Borrowers with excellent credit may qualify for lower rates.

Student loan interest rates are generally lower than credit cards (15-25%) and personal loans (6-36%), but higher than mortgages (3-7%) or auto loans (4-8%). Federal student loans often offer more flexible repayment options and lower rates compared to private loans.