Student loan interest rates have been steadily increasing over the past few years, leaving many borrowers wondering why. The rising rates can be attributed to a combination of factors, including changes in federal monetary policy, inflation, and shifts in the credit market. As the Federal Reserve raises interest rates to combat inflation, student loan rates, which are often tied to these benchmark rates, also increase. Additionally, lenders may adjust their rates based on market conditions and their assessment of borrower risk. This trend has significant implications for students and graduates, as higher interest rates can lead to increased borrowing costs and longer repayment periods. Understanding the reasons behind these rate hikes is crucial for borrowers to make informed decisions about their student loans and financial futures.

| Characteristics | Values |

|---|---|

| Loan Type | Federal student loans, private student loans |

| Interest Rate Type | Fixed interest rates, variable interest rates |

| Economic Factors | Inflation, changes in the Federal Reserve's interest rates |

| Loan Demand | Increased demand for higher education, rising tuition costs |

| Credit Risk | Perceived risk of lending to students, creditworthiness of borrowers |

| Government Policies | Changes in government subsidies, interest rate caps, or loan forgiveness programs |

| Market Conditions | Fluctuations in the bond market, changes in investor sentiment |

| Loan Servicing Costs | Administrative costs, collection costs, and other servicing expenses |

| Profit Margins | Lenders' desire to maintain or increase profit margins on student loans |

| Regulatory Environment | Changes in regulations affecting student loan lending and servicing |

Explore related products

What You'll Learn

- Inflation: Rising inflation rates lead to increased borrowing costs, impacting student loan interest rates

- Federal Reserve Policies: Changes in monetary policy, such as interest rate hikes, affect student loan rates

- Market Demand: Increased demand for student loans can drive up interest rates due to higher risk perceptions

- Government Funding: Reductions in government subsidies or funding for student loans can result in higher interest rates

- Credit Risk: Perceived higher credit risk among borrowers can lead lenders to charge higher interest rates

![]()

Inflation: Rising inflation rates lead to increased borrowing costs, impacting student loan interest rates

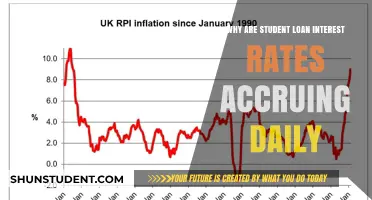

The recent surge in student loan interest rates can be directly attributed to the broader economic phenomenon of inflation. As inflation rates rise, the cost of borrowing money increases, which in turn affects the interest rates on student loans. This relationship is rooted in the way central banks, like the Federal Reserve in the United States, respond to inflation. To combat rising prices, central banks often increase the federal funds rate, which is the interest rate banks charge each other for overnight loans. This increase in the federal funds rate leads to higher interest rates across the board, including those on student loans.

For students and recent graduates, this means that the cost of borrowing for education is becoming more expensive. Variable-rate student loans, in particular, are sensitive to changes in the federal funds rate and can see significant increases in interest charges over time. Fixed-rate loans, while not immediately affected by rate hikes, may also see increases in future borrowing costs as lenders adjust their rates to reflect the higher cost of funds.

The impact of inflation on student loan interest rates is further compounded by the fact that wages are often not keeping pace with rising prices. This means that students may be facing higher loan payments at the same time that their earning potential is not increasing proportionally. This can lead to increased financial strain and difficulty in managing student loan debt.

To mitigate the effects of rising interest rates, students and borrowers should consider strategies such as refinancing their loans to fixed-rate options, making extra payments to reduce the principal balance, and exploring income-driven repayment plans that can adjust monthly payments based on income and family size. Additionally, policymakers may need to consider measures to address the root causes of inflation and its impact on borrowing costs, such as implementing fiscal policies to reduce government spending or increase revenue, and working to improve supply chain resilience to reduce price pressures.

In conclusion, the rise in student loan interest rates is a direct consequence of broader economic trends, particularly inflation. Understanding this relationship can help borrowers make informed decisions about managing their student loan debt and can inform policy discussions aimed at addressing the underlying causes of rising borrowing costs.

Understanding the New 1040: Student Loan Interest Reporting Explained

You may want to see also

Explore related products

![]()

Federal Reserve Policies: Changes in monetary policy, such as interest rate hikes, affect student loan rates

The Federal Reserve, often referred to as the Fed, plays a crucial role in the United States' monetary policy. One of its primary tools is adjusting interest rates, which can have a ripple effect throughout the economy. When the Fed raises interest rates, it typically aims to curb inflation or slow down economic growth. However, this policy change can also impact student loan rates, making them more expensive for borrowers.

Student loans are often tied to the prime interest rate, which is directly influenced by the Fed's actions. When the Fed increases the federal funds rate, banks and other financial institutions may raise their prime rates in response. This, in turn, can lead to higher interest rates on variable-rate student loans. For example, if the Fed raises the federal funds rate by 0.25 percentage points, the prime rate might increase by a similar amount, causing the interest rate on a variable-rate student loan to rise accordingly.

Moreover, the Fed's policies can also affect the availability of credit and the overall borrowing environment. When interest rates are higher, it becomes more expensive for lenders to offer loans, which can lead to stricter lending criteria and reduced loan options for students. This can be particularly challenging for those with lower credit scores or limited financial resources.

It's important to note that not all student loans are affected equally by the Fed's policies. Fixed-rate student loans, for instance, are not directly impacted by changes in the federal funds rate. However, the overall borrowing environment and the cost of credit can still influence the rates offered by lenders for these loans.

In conclusion, the Federal Reserve's monetary policy decisions, particularly interest rate hikes, can have a significant impact on student loan rates. Borrowers should be aware of these potential changes and consider their options carefully when taking out student loans. It may be beneficial to explore fixed-rate loan options or to borrow during periods when interest rates are lower. Additionally, staying informed about the Fed's policies and their potential effects on the economy can help borrowers make more informed decisions about their financial future.

When Will Normal Student Loan Interest Rates Resume? Key Dates Explained

You may want to see also

Explore related products

$15.91 $37.99

![]()

Market Demand: Increased demand for student loans can drive up interest rates due to higher risk perceptions

The rising demand for student loans has a direct impact on interest rates, primarily due to the increased perception of risk among lenders. As more students seek financial assistance to pursue higher education, the pool of borrowers expands, which can lead to a higher default risk. Lenders mitigate this risk by charging higher interest rates, ensuring they can recoup their investments even if a significant number of borrowers fail to repay their loans.

This phenomenon is particularly pronounced in the private student loan market, where lenders are not backed by government guarantees. Without the safety net of federal support, private lenders must rely on credit scores and other financial indicators to assess the creditworthiness of borrowers. As demand increases, lenders may become more selective, offering higher interest rates to those with lower credit scores or less financial stability.

Furthermore, the increased demand for student loans can also drive up interest rates in the federal loan program. While federal loans are subsidized by the government and typically offer lower interest rates than private loans, the sheer volume of borrowers can still put upward pressure on rates. This is especially true if the government decides to reduce subsidies or increase the cost of borrowing to manage the growing demand.

In addition to the direct impact on interest rates, the increased demand for student loans can also have broader economic implications. For instance, higher interest rates can lead to increased borrowing costs, which can burden students and their families for years to come. This, in turn, can affect consumer spending and economic growth, as graduates may need to allocate a larger portion of their income to loan repayments.

To mitigate the effects of rising demand on student loan interest rates, policymakers and lenders can explore various strategies. For example, expanding access to financial aid and scholarships can help reduce the reliance on loans. Additionally, implementing more robust credit counseling and financial literacy programs can help borrowers make more informed decisions about their financial futures.

In conclusion, the increased demand for student loans is a significant factor driving up interest rates. By understanding the underlying causes and potential consequences of this trend, stakeholders can work together to develop solutions that promote affordable access to higher education while minimizing the financial burden on students and their families.

When Does Interest Capitalize on Student Loans Under IBR Plans?

You may want to see also

Explore related products

![]()

Government Funding: Reductions in government subsidies or funding for student loans can result in higher interest rates

Reductions in government subsidies or funding for student loans can have a direct impact on interest rates. When the government decreases its financial support for student loans, lenders may increase interest rates to compensate for the reduced funding. This can lead to higher borrowing costs for students, making it more difficult for them to afford their education.

One reason for the increase in interest rates is that lenders need to make up for the lost revenue from reduced government subsidies. By charging higher interest rates, they can ensure that they continue to make a profit on the loans they provide. Additionally, when government funding is reduced, lenders may become more risk-averse and increase interest rates to account for the perceived higher risk of lending to students.

Another factor to consider is the impact of reduced government funding on the availability of student loans. When funding is limited, lenders may become more selective in who they lend to, potentially leading to higher interest rates for those who are deemed higher risk. This can create a situation where students who are already struggling to afford their education are faced with even higher borrowing costs.

It's important to note that the relationship between government funding and student loan interest rates is complex. While reduced funding can lead to higher interest rates, other factors such as market conditions and lender competition can also play a role. However, it's clear that government funding is a key factor in determining the cost of student loans, and reductions in funding can have significant consequences for borrowers.

In conclusion, reductions in government subsidies or funding for student loans can result in higher interest rates, making it more difficult for students to afford their education. Lenders may increase interest rates to compensate for lost revenue, account for perceived higher risk, or become more selective in who they lend to. While other factors can also influence interest rates, government funding is a critical component in determining the cost of student loans.

Deducting Student Loan Interest: Finding the Right Line on Form 1040

You may want to see also

Explore related products

![]()

Credit Risk: Perceived higher credit risk among borrowers can lead lenders to charge higher interest rates

Lenders assess credit risk when determining interest rates for loans, including student loans. Borrowers with a history of late payments, defaults, or high debt levels are considered higher risk. To compensate for this increased risk, lenders charge higher interest rates. This is a fundamental principle of lending: the higher the risk, the higher the return required to justify the loan.

In the context of student loans, several factors contribute to the perception of higher credit risk. Many students have limited credit histories, making it difficult for lenders to assess their creditworthiness. Additionally, student loan borrowers often have high debt-to-income ratios, as they are typically young and just starting their careers. This combination of factors can lead lenders to perceive student loan borrowers as higher risk, resulting in higher interest rates.

Furthermore, the rising cost of higher education has led to an increase in the average student loan debt. As students borrow more money to cover tuition and living expenses, their debt-to-income ratios continue to rise. This trend has contributed to the perception of higher credit risk among student loan borrowers, further driving up interest rates.

It's important to note that not all student loan borrowers are considered high risk. Borrowers with strong credit histories, stable employment, and manageable debt levels may be able to secure lower interest rates. However, the overall trend of increasing student loan debt and the associated credit risk has led to higher interest rates for many borrowers.

To mitigate the impact of higher interest rates, student loan borrowers can take steps to improve their creditworthiness. This includes making timely payments, keeping debt levels manageable, and maintaining a good credit history. By demonstrating responsible borrowing behavior, students can reduce their perceived credit risk and potentially qualify for lower interest rates on their loans.

When Student Loan Interest Payments Were Paused: A Timeline

You may want to see also

Frequently asked questions

Student loan interest rates are rising due to a combination of factors, including inflation, changes in federal monetary policy, and the increasing cost of higher education. As the Federal Reserve raises interest rates to combat inflation, the cost of borrowing for students and parents also increases.

Changes in federal monetary policy, such as adjustments to the federal funds rate by the Federal Reserve, directly impact student loan interest rates. When the Fed raises the federal funds rate, it becomes more expensive for lenders to borrow money, which in turn leads to higher interest rates on student loans.

Inflation contributes to the rising cost of student loans by decreasing the purchasing power of money. As the cost of living increases, so does the cost of higher education. This leads to higher tuition fees, which in turn increase the amount students need to borrow, resulting in higher overall interest payments.

Yes, there are several government programs and initiatives aimed at helping borrowers manage rising student loan interest rates. These include income-driven repayment plans, which adjust monthly payments based on income and family size, and loan forgiveness programs for certain public service and teaching positions.

Students and parents can take several steps to minimize the impact of rising interest rates on their student loans. These include:

- Borrowing only what is necessary to cover education expenses

- Exploring alternative funding sources, such as scholarships and grants

- Choosing a loan with a fixed interest rate, if possible

- Making regular payments to reduce the overall amount borrowed

- Considering refinancing options to secure a lower interest rate