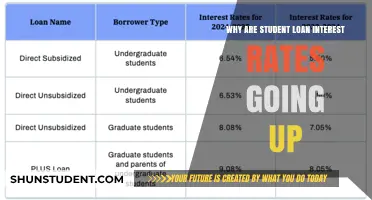

Student loans begin accruing interest as soon as the funds are disbursed, which is a common practice among lending institutions. This is because the loan is considered to be in repayment status from the moment the borrower receives the money. The interest accrues daily and is typically capitalized, meaning it is added to the principal balance of the loan, increasing the total amount owed over time. This can lead to a significant increase in the cost of the loan if not managed properly. It's important for borrowers to understand the terms of their loan and to make payments as soon as possible to minimize the amount of interest that accrues.

| Characteristics | Values |

|---|---|

| Loan Type | Federal or private student loans |

| Interest Accrual | Continuous, even during deferment or forbearance |

| Impact on Principal | Increases the total amount owed |

| Repayment Options | Various, including income-driven repayment plans |

| Potential Consequences | Financial strain, credit score impact |

| Relief Programs | Loan forgiveness or refinancing options available |

Explore related products

What You'll Learn

- Interest Accrual During Grace Periods: Understand how interest accumulates even during grace periods after graduation

- Variable vs. Fixed Interest Rates: Explore the differences between variable and fixed interest rates on student loans

- Compounding Interest: Learn how interest is calculated and compounded over time, increasing the total debt

- Deferment and Forbearance: Discover how deferment and forbearance options affect interest accrual on student loans

- Strategies to Minimize Interest: Find out about strategies to minimize interest, such as paying interest during school or refinancing

![]()

Interest Accrual During Grace Periods: Understand how interest accumulates even during grace periods after graduation

Even during grace periods after graduation, interest continues to accrue on student loans. This is a critical aspect of student loan management that many borrowers may not fully understand. The grace period, typically six months after graduation, is designed to give new graduates time to find employment and get settled before they need to start making loan payments. However, it's important to note that interest does not stop accruing during this time.

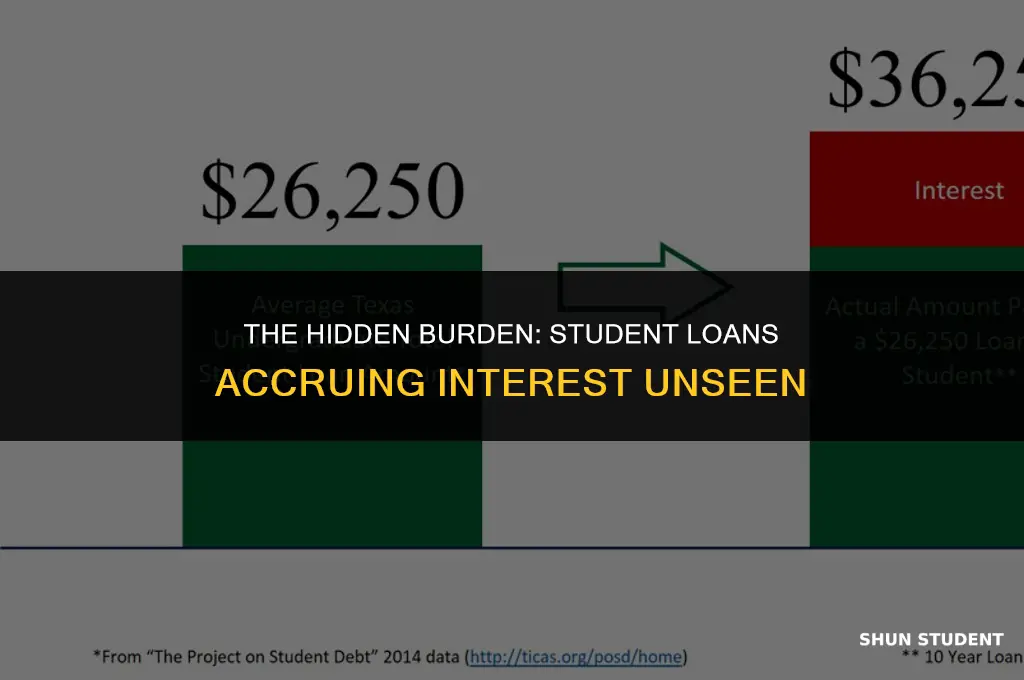

The accrual of interest during the grace period can significantly impact the total amount of debt a borrower will need to repay. For example, if a borrower has a $30,000 loan with a 5% interest rate, the interest that accrues during a six-month grace period could add an additional $750 to the loan balance. This means that when the borrower begins making payments, they will owe more than the original loan amount.

To mitigate the impact of interest accrual during the grace period, borrowers should consider making interest-only payments if possible. This will help to reduce the overall cost of the loan and prevent the balance from growing further. Additionally, borrowers should be aware of their loan terms and understand when the grace period ends to avoid any surprises when it comes time to start making full payments.

It's also worth noting that not all student loans offer a grace period. For example, some private loans may require immediate repayment, while others may offer a shorter grace period. Borrowers should carefully review their loan agreements to understand the specific terms and conditions of their loans.

In conclusion, understanding how interest accrues during grace periods is essential for effective student loan management. By being aware of this process and taking steps to mitigate its impact, borrowers can better manage their debt and avoid unnecessary financial strain.

Top Private Student Loans: Lowest Interest Rates Compared

You may want to see also

Explore related products

![]()

Variable vs. Fixed Interest Rates: Explore the differences between variable and fixed interest rates on student loans

Understanding the difference between variable and fixed interest rates is crucial when navigating the complexities of student loans. A fixed interest rate remains constant throughout the life of the loan, providing predictability in your monthly payments. This stability can be beneficial for budgeting purposes, as you'll know exactly how much you owe each month. On the other hand, variable interest rates fluctuate based on market conditions, which means your monthly payments can increase or decrease over time. This unpredictability can make it challenging to plan your finances effectively.

One key factor to consider is the current economic climate. In a low-interest-rate environment, variable rates may be lower than fixed rates, potentially saving you money in the short term. However, if interest rates rise, your variable rate loan could become more expensive. Fixed rates, while possibly higher initially, offer protection against future rate increases. This trade-off between immediate savings and long-term stability is a critical decision point for borrowers.

Another aspect to examine is the length of your loan term. If you plan to pay off your loan quickly, a variable rate might be more advantageous, as you could benefit from lower rates without being exposed to significant risk. Conversely, if you anticipate a longer repayment period, a fixed rate may provide more security, ensuring that your payments remain manageable even if market rates climb.

Your personal financial situation and risk tolerance also play a significant role in this decision. If you have a stable income and can absorb potential increases in your loan payments, a variable rate might be a suitable choice. However, if you're on a tight budget or have other financial commitments, the predictability of a fixed rate could be more appealing.

In conclusion, the choice between variable and fixed interest rates on student loans depends on a variety of factors, including market conditions, loan term, and your individual financial circumstances. By carefully weighing these considerations, you can make an informed decision that aligns with your financial goals and risk tolerance.

When Do Federal Student Loans Start Accruing Interest?

You may want to see also

Explore related products

![]()

Compounding Interest: Learn how interest is calculated and compounded over time, increasing the total debt

Imagine you've just taken out a student loan, and you're wondering why the balance seems to be growing faster than you can pay it down. This is due to a powerful financial force known as compounding interest. Here's how it works: when you borrow money, you're charged interest on the principal amount. But as time goes on, the interest itself becomes part of the principal, and you're charged interest on that too. This creates a snowball effect where the amount you owe grows exponentially over time.

Let's break it down with an example. Say you take out a $10,000 loan with a 5% annual interest rate. After one year, you'll owe $10,500 – the original $10,000 plus $500 in interest. But in the second year, you're not just charged interest on the original $10,000; you're charged interest on the new balance of $10,500. So, you'll owe $11,025 after two years. As you can see, the amount you owe is growing faster than the interest rate itself.

Compounding interest can be particularly problematic for student loans because these loans often have long repayment terms, giving interest plenty of time to accumulate. Additionally, many student loans compound interest daily or monthly, which can significantly increase the total amount owed over the life of the loan.

To minimize the impact of compounding interest on your student loans, it's important to make payments as early and as often as possible. Even small payments can help reduce the principal balance and slow the growth of interest. You may also want to consider refinancing your loans to a lower interest rate or consolidating them into a single loan with a lower overall balance.

In conclusion, compounding interest is a major factor in why student loan balances can grow so quickly. By understanding how it works and taking steps to manage it, you can take control of your student loan debt and work towards a more secure financial future.

Understanding Student Loan Interest Rates: Types, Factors, and Impact

You may want to see also

Explore related products

![]()

Deferment and Forbearance: Discover how deferment and forbearance options affect interest accrual on student loans

Deferment and forbearance are two options available to student loan borrowers who are struggling to make their monthly payments. While both options can provide temporary relief, they have different implications for interest accrual on the loan. Deferment allows borrowers to temporarily postpone their payments without accruing additional interest, while forbearance allows borrowers to reduce or pause their payments but does not prevent interest from accruing.

To qualify for deferment, borrowers must meet certain eligibility criteria, such as being enrolled in school at least half-time, being unemployed, or experiencing economic hardship. Deferment can be a useful option for borrowers who are experiencing short-term financial difficulties and need a temporary break from their loan payments. However, it is important to note that deferment does not forgive any of the loan's principal or interest, and borrowers will need to resume making payments once the deferment period ends.

Forbearance, on the other hand, is typically granted on a case-by-case basis and may be available to borrowers who are experiencing financial hardship or other extenuating circumstances. During a forbearance period, borrowers may be able to reduce their monthly payments or pause them altogether, but interest will continue to accrue on the loan. This can lead to a significant increase in the loan's total cost over time, as the accrued interest is added to the principal balance.

One key difference between deferment and forbearance is their impact on interest accrual. Deferment prevents additional interest from accruing during the deferment period, while forbearance does not. This means that borrowers who opt for forbearance may end up paying more in interest over the life of the loan than those who choose deferment.

When considering deferment or forbearance, it is important for borrowers to carefully weigh the pros and cons of each option. While both options can provide temporary relief from loan payments, they have different implications for interest accrual and the overall cost of the loan. Borrowers should also be aware that neither deferment nor forbearance will forgive any of the loan's principal or interest, and they will need to resume making payments once the deferment or forbearance period ends.

In conclusion, deferment and forbearance can be useful options for student loan borrowers who are struggling to make their monthly payments. However, it is important to understand the implications of each option for interest accrual and the overall cost of the loan. Borrowers should carefully consider their financial situation and long-term goals before deciding which option is right for them.

Fixed vs. Variable Interest Rates: Which Student Loan is Better?

You may want to see also

Explore related products

$24.55 $30.99

$20.99 $25.99

![]()

Strategies to Minimize Interest: Find out about strategies to minimize interest, such as paying interest during school or refinancing

One effective strategy to minimize interest on student loans is to make interest payments while still in school. This approach can significantly reduce the overall amount of interest that accrues over the life of the loan. For example, if a student borrows $10,000 at a 6% interest rate and makes no payments during a four-year education, they will graduate with an additional $2,400 in interest charges. However, by paying just the interest each month while in school, they can prevent this accumulation and save money in the long run.

Another strategy is to refinance student loans after graduation. Refinancing involves taking out a new loan at a lower interest rate to pay off the original loan. This can be particularly beneficial for those with high-interest rates or variable-rate loans. By securing a fixed-rate loan at a lower interest rate, borrowers can reduce their monthly payments and pay off their loans more quickly. For instance, refinancing a $30,000 loan from a 7% interest rate to a 4% interest rate could save the borrower over $10,000 in interest charges over the life of the loan.

Additionally, borrowers should consider making extra payments towards the principal balance of their loans whenever possible. Even small, consistent extra payments can add up over time and reduce the overall interest paid. This strategy is most effective when combined with other methods, such as refinancing or paying interest during school. By tackling the principal balance early on, borrowers can shorten the life of their loans and minimize the amount of interest that accrues.

It's also important for borrowers to be aware of the different repayment plans available for student loans. Income-driven repayment plans, for example, can lower monthly payments based on the borrower's income and family size. While these plans may not directly reduce interest rates, they can make it easier for borrowers to manage their payments and avoid defaulting on their loans. Borrowers should research and compare different repayment plans to find the one that best suits their financial situation and goals.

In conclusion, minimizing interest on student loans requires a proactive and strategic approach. By making interest payments during school, refinancing after graduation, making extra payments towards the principal, and choosing the right repayment plan, borrowers can significantly reduce the amount of interest they pay over the life of their loans. These strategies can help borrowers save money and achieve financial stability more quickly.

When Did Pandemic Student Loan Interest Hold End?

You may want to see also

Frequently asked questions

Student loans begin accruing interest as soon as the funds are disbursed, regardless of whether you are still enrolled in school. This is because the loan is considered to be in repayment status from the moment you receive the money, although you may not have to start making payments until after you graduate or drop below half-time enrollment.

The interest on your student loan is calculated based on the principal amount (the amount you borrowed), the interest rate (which is set by the lender or the government for federal loans), and the length of time the loan is in repayment. Interest is typically calculated daily and then capitalized (added to the principal balance) at regular intervals, such as quarterly or annually.

The accruing interest increases the total amount you will owe on your student loan by the time you graduate. This can make it more challenging to repay the loan, as you will have to pay back not only the principal amount but also the accumulated interest. Additionally, if you do not make any payments towards the interest while in school, it may capitalize and increase your monthly payment amount once you enter full repayment.

Yes, there are a few strategies you can consider to avoid or reduce the interest accruing on your student loan while in school. One option is to make interest-only payments during your enrollment period, which can prevent the interest from capitalizing and increasing your overall debt. Another strategy is to apply for a loan with a lower interest rate or to refinance your existing loan to a lower rate if possible. Additionally, some federal loans offer interest subsidies while you are in school, which can help reduce the amount of interest that accrues.