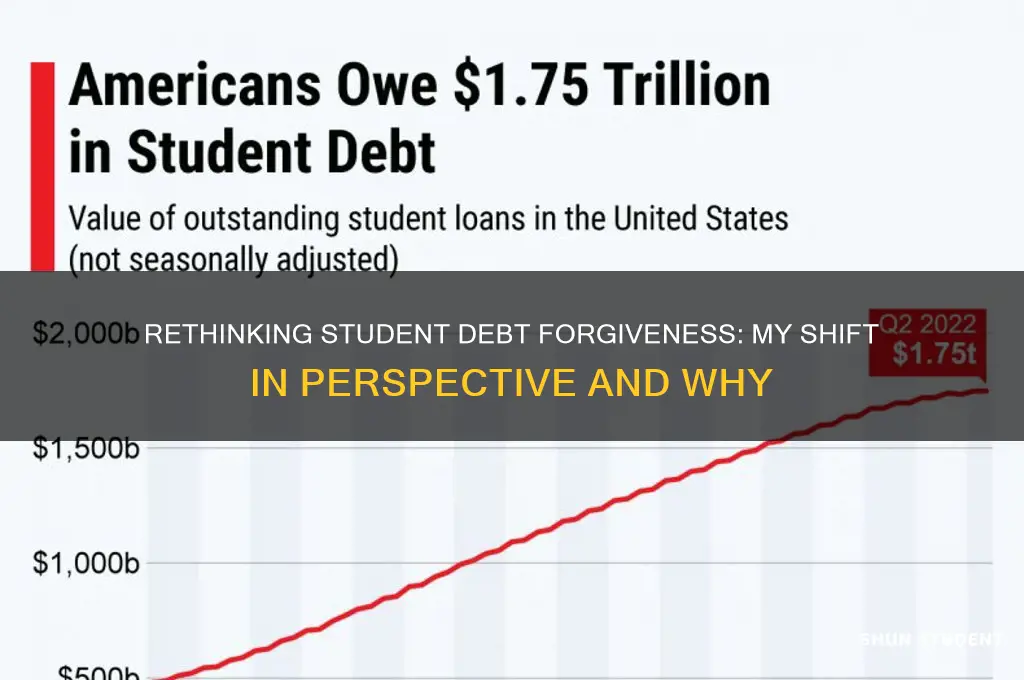

For years, I was skeptical about the idea of widespread student debt forgiveness, believing it to be an unfair solution that rewarded individual choices at the expense of taxpayers. However, after witnessing the systemic failures of the higher education system, the skyrocketing costs of tuition, and the disproportionate burden placed on marginalized communities, I’ve reconsidered my stance. The reality is that student debt has become a crippling crisis, trapping millions in financial limbo and stifling economic mobility. While personal responsibility is important, the scale of this issue demands a collective response. I now see debt forgiveness not as a handout, but as a necessary step toward addressing systemic inequities and investing in a more equitable future.

| Characteristics | Values |

|---|---|

| Economic Impact | Concerns about inflation and economic burden shifted towards targeted relief for low-income borrowers. |

| Moral Hazard | Initially feared it would discourage responsible borrowing; now seen as necessary for systemic fairness. |

| Equity Concerns | Recognized disproportionate impact of debt on marginalized communities, necessitating forgiveness. |

| Political Feasibility | Initially skeptical due to partisan divide; now supported by growing public and bipartisan momentum. |

| Long-Term Benefits | Shifted focus from short-term costs to long-term economic growth and reduced wealth inequality. |

| Targeted vs. Universal Forgiveness | Moved from opposing broad forgiveness to supporting income-driven or capped forgiveness plans. |

| Accountability for Institutions | Emphasis on holding predatory colleges accountable rather than penalizing borrowers. |

| Public Sentiment | Changed stance due to increased public support and personal stories highlighting debt struggles. |

| Legal and Policy Challenges | Initially doubted legality; now supported by executive actions and legislative proposals. |

| Intergenerational Fairness | Acknowledged burden on younger generations, shifting from opposition to support for relief. |

Explore related products

What You'll Learn

- Economic Impact: Analyzes how debt forgiveness affects GDP, consumer spending, and economic recovery

- Moral Hazard Concerns: Explores arguments about incentivizing future borrowing and fairness to non-borrowers

- Political Shifts: Discusses changing public and political attitudes toward debt relief policies

- Targeted vs. Universal Relief: Compares benefits of broad forgiveness versus income-based or need-specific approaches

- Long-Term Consequences: Examines potential effects on higher education costs and student borrowing behavior

![]()

Economic Impact: Analyzes how debt forgiveness affects GDP, consumer spending, and economic recovery

Student debt forgiveness isn't just a moral or political issue—it's an economic lever. When millions of borrowers are relieved of monthly payments, the ripple effects are immediate and measurable. Consider this: the average student loan payment is around $400 per month. For a borrower earning $50,000 annually, that’s 9.6% of their pre-tax income. Freeing up this cash doesn’t just pad savings accounts; it fuels the economy. Every dollar not spent on debt is a dollar that can be spent on groceries, rent, or even a new car. This shift in spending power is why economists often compare debt forgiveness to a stimulus package—one that targets a demographic with a high propensity to consume.

To understand the GDP impact, let’s break it down. If $10,000 in debt is forgiven for 10 million borrowers, that’s $100 billion injected into the economy. But the multiplier effect is key. For every dollar spent, the economy grows by $1.50 to $2.50, depending on how quickly the money circulates. In a post-pandemic recovery, where consumer confidence is fragile, this infusion could be a game-changer. Take the example of a 28-year-old teacher in Ohio. With $30,000 in debt forgiven, she might spend $200 more per month on local businesses, invest in a home improvement project, or even start a family—all activities that stimulate growth. Multiply that by millions, and you’re looking at a significant boost to GDP.

However, the devil is in the details. Not all debt forgiveness programs are created equal. A blanket $50,000 forgiveness plan, for instance, could cost over $1 trillion. Without careful targeting, such a policy risks inflationary pressures, especially if the economy is already running hot. A smarter approach? Means-tested forgiveness, focusing on borrowers earning under $75,000 annually. This ensures the money goes to those most likely to spend it immediately, rather than high earners who might save or invest it. Pairing forgiveness with incentives for rural or underserved areas could further amplify the economic impact, creating jobs and revitalizing communities.

Critics argue that debt forgiveness punishes responsible savers and shifts the burden to taxpayers. But this misses the bigger picture. A thriving economy benefits everyone, not just those with forgiven debt. For instance, a surge in consumer spending could lead to higher tax revenues, offsetting some of the program’s cost. Moreover, reducing the debt burden on young adults could increase homeownership rates, currently at a 50-year low for millennials. This, in turn, would stabilize the housing market and create demand for related industries like construction and retail.

In conclusion, student debt forgiveness isn’t just about alleviating individual hardship—it’s a strategic tool for economic recovery. By freeing up disposable income, it can stimulate consumer spending, boost GDP, and create a ripple effect across industries. But success hinges on design. Targeted, well-structured programs maximize benefits while minimizing risks like inflation or moral hazard. As policymakers weigh the pros and cons, one thing is clear: done right, debt forgiveness could be the spark the economy needs.

Can Private Student Loans Be Discharged in Bankruptcy?

You may want to see also

Explore related products

![]()

Moral Hazard Concerns: Explores arguments about incentivizing future borrowing and fairness to non-borrowers

One of the most persistent arguments against student debt forgiveness is the moral hazard it allegedly creates. Critics argue that canceling debt for current borrowers sends a signal to future students: borrow without restraint, because the government might bail you out later. This line of thinking assumes that individuals will act irrationally, prioritizing short-term gains over long-term financial responsibility. However, this perspective overlooks the systemic issues that drive students to borrow excessively in the first place, such as skyrocketing tuition costs and limited access to affordable education. Blaming borrowers for a broken system is like faulting a drowning person for swallowing water.

Consider the fairness argument often paired with moral hazard concerns: why should non-borrowers—those who paid off their loans, chose less expensive schools, or avoided debt altogether—bear the indirect costs of debt forgiveness? This question resonates with those who sacrificed to fulfill their financial obligations. Yet, it frames the issue as a zero-sum game, where one group’s gain is another’s loss. In reality, widespread debt forgiveness could stimulate the economy, benefiting everyone through increased consumer spending and reduced default rates. For instance, a 2021 study by the Roosevelt Institute estimated that canceling $1.4 trillion in student debt could add $1.5 trillion in GDP over 10 years. This reframes fairness not as individual retribution but as collective economic uplift.

To address moral hazard concerns practically, policymakers could implement safeguards to prevent reckless future borrowing. For example, capping loan amounts based on expected post-graduation earnings or requiring financial literacy courses for borrowers could mitigate risk. Additionally, tying forgiveness to public service or income-driven repayment plans would ensure that relief is targeted rather than universal. These measures would balance accountability with compassion, addressing critics’ fears without perpetuating a cycle of debt.

Ultimately, the moral hazard argument against student debt forgiveness rests on a flawed assumption: that borrowers are motivated solely by self-interest rather than necessity. It fails to acknowledge the broader structural failures that trap millions in debt. By focusing on fairness to non-borrowers, critics ignore the systemic inequities that make borrowing unavoidable for many. Instead of penalizing individuals for a broken system, the focus should shift to reforming higher education financing to prevent future crises. Debt forgiveness isn’t just about erasing numbers on a balance sheet—it’s about recalibrating a system that has long prioritized profit over people.

SSI and Student Debt Forgiveness: Exploring Options for Relief

You may want to see also

Explore related products

![]()

Political Shifts: Discusses changing public and political attitudes toward debt relief policies

Public opinion on student debt forgiveness has swung like a pendulum, influenced by economic crises, generational divides, and shifting political narratives. In 2019, only 27% of Americans supported broad student debt cancellation. Fast forward to 2022, and that number jumped to 55% among likely voters, according to a Morning Consult poll. This shift wasn’t accidental—it coincided with the pandemic’s economic fallout, where millions faced unemployment and mounting debt. The Biden administration’s initial $10,000 forgiveness proposal (later struck down by the Supreme Court) capitalized on this sentiment, framing debt relief as a moral imperative rather than a handout. Yet, the backlash from critics who labeled it regressive—benefiting higher-earning graduates more than low-income borrowers—highlighted the policy’s complexities. This tug-of-war between empathy and equity reveals how external events can reshape public attitudes overnight.

Politically, student debt forgiveness has become a litmus test for party loyalty, but even these lines are blurring. Democrats once championed forgiveness as a progressive cause, but internal fractures emerged when moderates like Senator Joe Manchin questioned its fairness. Meanwhile, Republicans, traditionally opposed to such measures, faced pressure from younger, debt-burdened voters in their base. Take Senator Marco Rubio’s 2022 proposal to cap interest rates on student loans—a tacit acknowledgment that ignoring the issue was no longer tenable. These cracks in partisan unity signal a broader recalibration: debt relief is no longer a fringe idea but a policy with cross-aisle appeal, albeit in watered-down forms. The lesson? Political survival now demands engagement with the issue, even if solutions remain divisive.

Generational politics has further accelerated this shift. Millennials and Gen Z, who hold the majority of student debt, are reshaping the narrative from one of personal responsibility to systemic failure. Their activism—amplified through social media campaigns like #CancelStudentDebt—has forced politicians to address the $1.7 trillion crisis. Consider this: 45% of Gen Z voters in the 2022 midterms cited student debt as a top concern, per Pew Research. This demographic pressure has pushed even reluctant lawmakers to propose alternatives, such as income-driven repayment plans or public service loan forgiveness expansions. The takeaway is clear: ignoring young voters’ financial realities is a political liability, and their influence will only grow as they age into peak voting years.

Finally, the legal battles over debt forgiveness have inadvertently educated the public on its intricacies, further shifting attitudes. When the Supreme Court blocked Biden’s forgiveness plan in 2023, citing lack of congressional authority, it sparked a national conversation about the limits of executive power. Paradoxically, this setback may have softened opposition by exposing the policy’s legal fragility rather than its merits. Polls post-ruling showed 60% of Americans believed Congress should act on debt relief, up from 50% pre-ruling. This suggests that while broad forgiveness remains contentious, targeted reforms—like cracking down on predatory lending practices or expanding Pell Grants—could gain bipartisan traction. The court’s intervention, unintended though it was, has reframed the debate from “if” to “how” relief should be structured.

In sum, the political landscape on student debt forgiveness is no longer static but dynamic, shaped by economic shocks, generational activism, and legal pushback. What was once a fringe issue is now a policy puzzle demanding creative solutions. As attitudes continue to evolve, one thing is certain: the next chapter in this debate will be written not just by lawmakers, but by the millions of borrowers whose voices are louder—and more organized—than ever.

Forgiving Student Loans for Disabled Borrowers: What You Need to Know

You may want to see also

Explore related products

$14.95 $14.95

![]()

Targeted vs. Universal Relief: Compares benefits of broad forgiveness versus income-based or need-specific approaches

The debate over student debt forgiveness often hinges on whether relief should be universal or targeted. Universal forgiveness, while appealing in its simplicity, risks benefiting those who may not need it, such as high-earning professionals. For instance, forgiving all student debt would mean a doctor earning $250,000 annually receives the same relief as a teacher earning $45,000, despite their vastly different financial realities. This approach, though equitable in theory, can dilute the impact of relief for those most burdened by debt.

Targeted relief, on the other hand, focuses on income-based or need-specific criteria, ensuring resources are directed where they’re most needed. Programs like income-driven repayment (IDR) plans cap monthly payments at a percentage of discretionary income, often 10-20%, and forgive remaining balances after 20-25 years. For example, a borrower earning $35,000 annually might pay as little as $200 monthly under an IDR plan, with the potential for forgiveness after two decades. This approach prioritizes low- and middle-income borrowers, addressing the root of financial strain without subsidizing those who can comfortably repay their loans.

However, targeted relief isn’t without challenges. Implementing such programs requires robust administrative systems to verify income and need, which can be costly and complex. For instance, the Public Service Loan Forgiveness (PSLF) program, designed to forgive debt for public servants after 10 years, has been plagued by bureaucratic hurdles, with only 2% of applicants receiving forgiveness as of 2021. This highlights the need for streamlined processes to ensure targeted relief reaches its intended beneficiaries.

The choice between universal and targeted relief ultimately depends on the goals of forgiveness. If the aim is to stimulate the economy broadly, universal relief might be justified, as it injects cash into the system regardless of need. However, if the goal is to alleviate financial hardship for the most vulnerable, targeted relief is more effective. For example, forgiving $10,000 in debt for borrowers earning under $50,000 annually would provide immediate relief to those most at risk of default, while minimizing costs and ensuring fairness.

In practice, a hybrid approach could balance these considerations. For instance, universal relief could be capped at a certain income threshold, or targeted programs could be expanded with simplified eligibility criteria. By combining the broad reach of universal forgiveness with the precision of targeted relief, policymakers can maximize the impact of student debt forgiveness while addressing both economic and equity concerns.

Disabled Veterans: Do They Qualify for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Long-Term Consequences: Examines potential effects on higher education costs and student borrowing behavior

Student debt forgiveness, while offering immediate relief, could inadvertently fuel a cycle of rising tuition costs. Colleges, anticipating government bailouts, might feel less pressure to control expenses, passing the burden onto future students. This moral hazard could exacerbate the very problem forgiveness aims to solve, leaving the next generation of borrowers in an even deeper financial hole.

For instance, consider a scenario where a university, knowing a portion of its students' debt will be forgiven, raises tuition by 5% annually. Over a decade, this compounds to a staggering 63% increase, far outpacing inflation and wage growth.

The psychological impact of debt forgiveness on borrowing behavior is another critical consideration. Students, assuming future bailouts, might be more inclined to take on larger loans, choosing costlier institutions or programs without fully weighing the long-term consequences. This shift in risk perception could lead to a culture of over-borrowing, further inflating the student debt bubble. Imagine a student, emboldened by the possibility of future forgiveness, opting for a private college with a $60,000 annual tuition over a state school with a $20,000 price tag, reasoning that the debt will eventually be wiped clean.

However, a counterargument exists. Debt forgiveness, coupled with stringent regulations on college pricing and lending practices, could potentially break the cycle. Capping tuition increases, implementing income-driven repayment plans, and holding institutions accountable for graduate employment outcomes could mitigate the risk of cost escalation. Think of it as a two-pronged approach: providing relief to current borrowers while simultaneously addressing the systemic issues driving up costs.

A balanced approach, combining targeted forgiveness with structural reforms, is crucial to avoiding unintended consequences.

Ultimately, the long-term success of student debt forgiveness hinges on its ability to address the root causes of the crisis, not just its symptoms. Simply wiping away debt without addressing the underlying factors driving up costs and encouraging excessive borrowing will only provide temporary relief, setting the stage for a recurring cycle of debt and financial hardship.

Is New York State Taxing Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Frequently asked questions

I initially opposed student debt forgiveness because I believed it would be unfair to taxpayers who did not attend college or had already paid off their loans. I also thought it might encourage future borrowers to take on excessive debt with the expectation of forgiveness.

My perspective shifted after witnessing the disproportionate burden of student debt on low-income and minority communities, coupled with the systemic failures in the higher education financing system. I realized that forgiveness could address systemic inequities and provide economic relief to millions.

While some borrowers may have made poor financial decisions, many were misled by predatory lending practices or lacked access to affordable education options. Forgiveness is not about rewarding irresponsibility but addressing broader systemic issues that trap individuals in debt.

Student debt forgiveness can stimulate the economy by freeing up disposable income for borrowers, enabling them to invest in homes, start businesses, and contribute to consumer spending. It also reduces financial stress, improving mental health and productivity.