Student debt interest is compounded daily, which means that interest is calculated and added to the principal balance every day. This can significantly increase the total amount of debt over time, making it more difficult for students to pay off their loans. The daily compounding of interest is a common practice among lenders, as it allows them to charge more interest on the outstanding balance. This can lead to a snowball effect, where the interest accrues rapidly and the student ends up paying back much more than they originally borrowed. Understanding how student debt interest is compounded daily is crucial for students who are considering taking out loans, as it can help them make informed decisions about their financial future.

Explore related products

$8.34 $19

What You'll Learn

- Daily Accrual: Interest accumulates daily, increasing the total debt over time

- Compound Effect: Daily compounding multiplies the interest, leading to exponential growth

- Grace Periods: Some loans offer grace periods where interest doesn't compound until after graduation

- Repayment Strategies: Paying more than the minimum can reduce the impact of daily compounding

- Loan Terms: Understanding the terms of your loan, including the interest rate and compounding frequency, is crucial

![]()

Daily Accrual: Interest accumulates daily, increasing the total debt over time

Interest on student debt accrues daily, which means that the total amount owed increases every day. This is a critical aspect of understanding why student debt can feel overwhelming and difficult to manage. The daily accrual of interest contributes to the snowball effect, where the debt grows rapidly over time, making it challenging for borrowers to make significant progress in paying it off.

To illustrate this concept, consider a hypothetical scenario where a student borrows $30,000 at a fixed interest rate of 6%. Assuming the interest is compounded daily, the total amount owed after one year would be approximately $31,836. This represents an increase of $1,836 in just one year, solely due to the daily accrual of interest. Over a longer period, such as 10 years, the total amount owed could balloon to over $40,000, with a significant portion of that increase attributable to the daily compounding of interest.

The daily accrual of interest on student debt can have several implications for borrowers. Firstly, it can make it difficult to keep up with the growing balance, especially for those who are struggling to make ends meet. Secondly, it can lead to a sense of hopelessness and frustration, as borrowers may feel like they are making little progress in paying off their debt. Finally, the daily accrual of interest can impact borrowers' credit scores, as a high debt-to-income ratio can be a red flag for lenders.

One strategy that borrowers can use to mitigate the effects of daily accrual is to make more frequent payments. By paying more often, borrowers can reduce the principal balance more quickly, which in turn reduces the amount of interest that accrues. Additionally, borrowers may want to consider refinancing their student loans to a lower interest rate, which can also help to reduce the total amount owed over time.

In conclusion, the daily accrual of interest on student debt is a significant factor that contributes to the overall burden of student loan debt. By understanding how this process works and taking proactive steps to manage their debt, borrowers can work towards a more stable financial future.

Maximize Your Tax Return: Where to Deduct Student Loan Interest

You may want to see also

Explore related products

$15.99 $20

![]()

Compound Effect: Daily compounding multiplies the interest, leading to exponential growth

The concept of compound interest is a powerful force in finance, and it plays a significant role in the accumulation of student debt. When interest is compounded daily, it means that the interest earned or charged is added to the principal balance every day, and then the next day's interest is calculated based on this new, higher balance. This process creates a snowball effect, where the amount of interest grows exponentially over time.

To illustrate this, let's consider an example. Suppose a student takes out a loan of $10,000 with an annual interest rate of 6%. If the interest is compounded daily, the student will owe more than $11,900 after just one year. This is because the interest is being calculated and added to the balance every day, rather than just once a year. Over the course of a typical 10-year repayment period, the total amount paid could be significantly higher than the original loan amount, largely due to the compounding effect.

The daily compounding of interest can have a profound impact on the overall cost of student debt. It's important for students and borrowers to understand this concept and to be aware of how it can affect their financial obligations. By making informed decisions about borrowing and repayment strategies, individuals can better manage their student debt and minimize the long-term impact of compound interest.

One strategy to mitigate the effects of daily compounding is to make regular, consistent payments towards the principal balance. This can help to reduce the overall amount of interest that accrues over time. Additionally, borrowers may want to consider refinancing their loans to a lower interest rate or exploring other repayment options that can help them pay off their debt more quickly.

In conclusion, the daily compounding of student debt interest can lead to exponential growth in the amount owed. Understanding this concept and taking proactive steps to manage debt can help borrowers minimize the financial impact and achieve greater financial stability.

Should Interest Rates Influence Your Student Loan Application Decision?

You may want to see also

Explore related products

![]()

Grace Periods: Some loans offer grace periods where interest doesn't compound until after graduation

A grace period on a student loan is a temporary reprieve from the compounding of interest. This means that during the grace period, which typically lasts for six months after graduation, the interest on the loan does not accumulate. This can be a significant benefit for borrowers, as it gives them a chance to get on their feet financially before they have to start worrying about the interest on their loans.

However, it is important to note that not all student loans offer grace periods. Additionally, the length of the grace period can vary depending on the type of loan and the lender. For example, federal student loans typically offer a six-month grace period, while private student loans may offer shorter or longer grace periods, or no grace period at all.

During the grace period, the borrower is not required to make any payments on the loan. However, it is important to keep in mind that the interest on the loan will still accrue during this time, even though it is not compounding. This means that the borrower will have to pay back the interest that accrued during the grace period, in addition to the principal amount of the loan.

One strategy that borrowers can use to minimize the amount of interest that accrues during the grace period is to make payments on the loan during this time. Even if the borrower is not required to make payments, making even small payments can help to reduce the amount of interest that accumulates. Additionally, borrowers can consider consolidating their loans or refinancing them to a lower interest rate, which can also help to reduce the amount of interest that accrues over time.

In conclusion, a grace period on a student loan can be a valuable tool for borrowers, as it gives them a chance to get on their feet financially before they have to start worrying about the interest on their loans. However, it is important to understand the terms and conditions of the grace period, and to make payments on the loan during this time if possible. By doing so, borrowers can minimize the amount of interest that accrues and make it easier to pay back their loans over time.

Empowering Futures: My Journey to Becoming a Student Ambassador

You may want to see also

Explore related products

![]()

Repayment Strategies: Paying more than the minimum can reduce the impact of daily compounding

One effective strategy to mitigate the effects of daily compounding on student debt is to pay more than the minimum monthly payment. By doing so, borrowers can reduce the principal balance more quickly, which in turn decreases the amount of interest accrued each day. For example, if a student loan has a principal balance of $10,000 with an annual interest rate of 6%, paying the minimum monthly payment of $100 would result in approximately $2,000 in interest paid over the life of the loan. However, by increasing the monthly payment to $200, the borrower could save around $1,000 in interest and pay off the loan about 5 years sooner.

Another approach is to make extra payments whenever possible, such as using tax refunds, bonuses, or other windfalls to chip away at the principal balance. Even small, irregular payments can add up over time and help reduce the overall cost of the loan. Borrowers can also consider refinancing their student loans to a lower interest rate, which would decrease the amount of interest compounded daily. However, this strategy may not be feasible for everyone, as it often requires a good credit score and may involve additional fees.

It's also important for borrowers to understand the specifics of their loan repayment plan and how daily compounding affects their individual situation. By reviewing their loan documents and using online calculators or consulting with a financial advisor, borrowers can gain a better understanding of how much interest they are accruing each day and how different repayment strategies could impact their overall debt burden.

In conclusion, while daily compounding can significantly increase the cost of student debt, there are strategies that borrowers can employ to reduce its impact. By paying more than the minimum monthly payment, making extra payments when possible, and exploring options like refinancing, borrowers can take control of their student debt and work towards a more financially stable future.

Lower Interest Rates: Which Student Loan Type Fits Your Needs?

You may want to see also

Explore related products

![]()

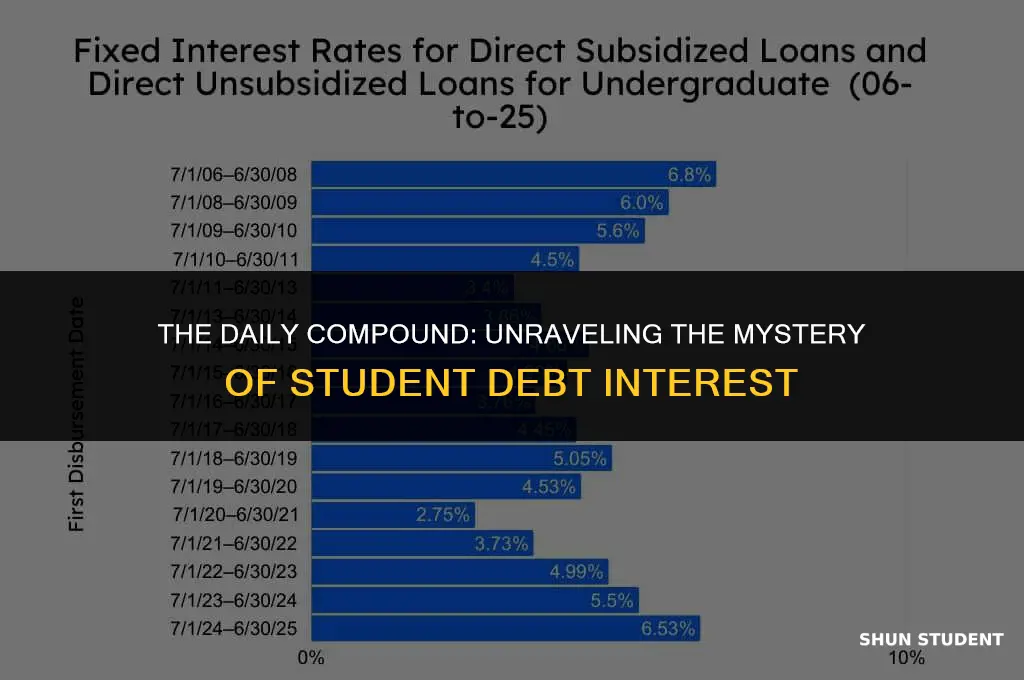

Loan Terms: Understanding the terms of your loan, including the interest rate and compounding frequency, is crucial

Understanding the terms of your loan is essential to managing your debt effectively. One of the most critical aspects to grasp is how interest is calculated and compounded. Daily compounding, a common practice in student loans, can significantly impact the total amount you owe over time.

To break it down, compounding frequency refers to how often the interest on your loan is calculated and added to the principal balance. Daily compounding means that interest is accrued every day, based on the outstanding balance. This might seem like a minor detail, but it can lead to a substantial increase in the total interest paid over the life of the loan compared to less frequent compounding methods, such as monthly or annually.

For instance, if you have a $10,000 loan with a 5% annual interest rate, daily compounding would result in approximately $5,116 in interest over 10 years, whereas monthly compounding would yield about $4,950, and annual compounding would be around $4,790. That's a difference of over $300 just due to the compounding frequency.

To mitigate the effects of daily compounding, it's crucial to make consistent, on-time payments and consider paying more than the minimum due each month. Additionally, understanding your loan terms empowers you to explore options like refinancing or consolidating your loans to potentially secure a lower interest rate or more favorable compounding terms.

In conclusion, while daily compounding can be a disadvantage, being informed about your loan terms and taking proactive steps can help you navigate and manage your student debt more effectively.

Why Students Lose Interest in Science: Uncovering the Turning Point

You may want to see also

Frequently asked questions

Student debt interest is compounded daily to calculate the total amount owed more accurately. This method accounts for the interest accrued each day, which is then added to the principal balance, resulting in a more precise calculation of the debt over time.

Daily compounding can significantly increase the total amount of student debt over time. Since interest is calculated and added to the principal balance every day, the debt grows at a faster rate compared to interest compounded monthly or annually.

The impact of daily compounding on student loan repayment is that borrowers may end up paying more in interest over the life of the loan. This can lead to higher monthly payments and a longer repayment period, making it more challenging for borrowers to pay off their student debt.

Yes, there are ways to reduce the effect of daily compounding on student debt. Borrowers can make extra payments towards the principal balance, which can help reduce the amount of interest accrued. Additionally, refinancing student loans to a lower interest rate or consolidating multiple loans into one with a lower rate can also help mitigate the impact of daily compounding.