The debate surrounding student loan forgiveness has intensified, with critics arguing that widespread cancellation could be deemed illegal under current U.S. law. Opponents claim that such action would overstep executive authority, as it lacks explicit congressional approval and could violate the separation of powers. Additionally, legal challenges suggest that forgiving student debt en masse might unfairly redistribute taxpayer funds, potentially infringing on the rights of those who have already repaid their loans or chose not to pursue higher education. These concerns highlight the complex intersection of policy, law, and equity, raising questions about the constitutionality and fairness of broad-scale student loan forgiveness.

| Characteristics | Values |

|---|---|

| Legal Authority | Critics argue the Biden administration lacks explicit congressional authority to forgive student loans under the HEROES Act of 2003, which is limited to modifying loans during national emergencies. |

| Separation of Powers | Forgiveness is seen as overstepping executive authority, infringing on Congress’s constitutional power to control spending and legislation. |

| Tax Implications | Forgiven debt may be considered taxable income, creating financial burdens for borrowers unless explicitly exempted by Congress. |

| Economic Impact | Opponents claim it could increase inflation, national debt, and unfairly benefit higher-income borrowers. |

| Legal Challenges | Multiple lawsuits have been filed, with courts blocking implementation due to procedural and statutory violations (e.g., lack of notice-and-comment rulemaking). |

| Equity Concerns | Critics argue it disproportionately benefits college-educated individuals, potentially exacerbating inequality for non-borrowers. |

| Moral Hazard | Forgiveness may incentivize future borrowing or reduce accountability for loan repayment. |

| Statutory Limits | The HEROES Act is interpreted as allowing only temporary loan modifications, not permanent forgiveness. |

| Political Opposition | Republican-led states and lawmakers have challenged the policy, citing it as an unlawful executive overreach. |

| Judicial Precedent | Courts have cited the Major Questions Doctrine, requiring clear congressional authorization for significant policy changes. |

| Implementation Hurdles | Legal battles and procedural errors have delayed or halted the program’s rollout. |

| Public Perception | Polls show divided opinions, with some viewing it as unfair to taxpayers who did not attend college or already repaid loans. |

Explore related products

What You'll Learn

- Constitutional Challenges: Does loan forgiveness violate the Appropriations Clause or separation of powers

- Taxpayer Burden: Is forgiving loans an unfair redistribution of taxpayer money

- Contract Law: Does it breach existing loan agreements between borrowers and lenders

- Executive Overreach: Is the President exceeding authority without congressional approval

- Legal Precedent: Are there past cases that challenge the legality of debt forgiveness

![]()

Constitutional Challenges: Does loan forgiveness violate the Appropriations Clause or separation of powers?

The debate over student loan forgiveness often hinges on whether such actions overstep constitutional boundaries, particularly concerning the Appropriations Clause and the separation of powers. At the heart of this issue is the question of authority: who has the power to allocate and forgive federal funds? The Appropriations Clause of Article I, Section 9 of the U.S. Constitution explicitly grants Congress the power to appropriate funds. Critics argue that executive actions to forgive student loans, without explicit congressional authorization, usurp this legislative authority. For instance, the Biden administration’s 2022 loan forgiveness plan faced legal challenges on the grounds that it bypassed Congress, potentially setting a precedent for unchecked executive spending.

To understand the constitutional challenge, consider the mechanics of the Appropriations Clause. Congress must authorize any expenditure of federal funds, ensuring accountability and preventing the executive branch from unilaterally redirecting taxpayer money. Loan forgiveness, in this context, can be seen as a form of spending—eliminating debt obligations effectively reduces the government’s expected revenue. If the executive branch can forgive loans without congressional approval, it raises concerns about the erosion of legislative power. This is not merely a theoretical concern; it has practical implications for fiscal responsibility and the balance of power between branches.

A comparative analysis of past executive actions provides insight. For example, the Trump administration’s pause on student loan payments during the COVID-19 pandemic was justified under the Higher Education Relief Opportunities for Students (HEROES) Act, which grants the Secretary of Education authority to modify loan terms during national emergencies. However, large-scale forgiveness goes beyond this scope, as it involves canceling debt rather than temporarily adjusting terms. This distinction highlights the importance of statutory limits and the need for clear congressional authorization for significant financial decisions.

From a persuasive standpoint, proponents of loan forgiveness often argue that it serves a greater public good, such as alleviating economic hardship for millions. However, this rationale does not address the constitutional question. Even well-intentioned policies must adhere to the framework established by the Constitution. Ignoring the Appropriations Clause or separation of powers could lead to a dangerous expansion of executive authority, undermining the checks and balances that safeguard democracy. For instance, if the executive branch can forgive student loans without Congress, what prevents it from canceling other types of debt or allocating funds for unrelated purposes?

In conclusion, the constitutional challenges to student loan forgiveness are rooted in the principles of limited government and separation of powers. While the policy’s goals may be commendable, its implementation must respect the boundaries set by the Constitution. Practical steps to address this issue include Congress passing explicit legislation to authorize loan forgiveness, ensuring transparency and accountability. Alternatively, policymakers could explore targeted relief measures that align with existing statutory authority. By adhering to constitutional norms, the government can pursue equitable solutions without compromising the integrity of the nation’s legal framework.

Student Loan Forgiveness: Answering Borrowers' Top Questions and Concerns

You may want to see also

Explore related products

![]()

Taxpayer Burden: Is forgiving loans an unfair redistribution of taxpayer money?

The debate over student loan forgiveness often hinges on the question of taxpayer burden. Critics argue that canceling student debt amounts to an unfair redistribution of wealth, forcing those who never attended college or already paid off their loans to subsidize others’ education. This perspective raises a critical ethical and economic question: should taxpayers bear the cost of individual financial decisions?

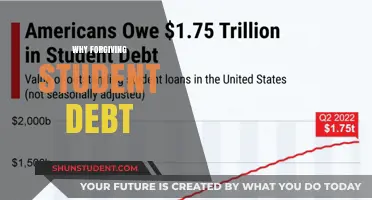

Consider the numbers. As of 2023, outstanding student loan debt in the U.S. exceeds $1.7 trillion, held by approximately 43 million borrowers. A blanket forgiveness program, say $10,000 per borrower, would cost taxpayers roughly $430 billion. Proponents argue this is an investment in economic mobility, but opponents counter that it disproportionately benefits higher-income earners, such as doctors and lawyers, who are more likely to have substantial debt due to graduate studies. For instance, 40% of student debt is held by households in the top 20% of income distribution, according to the Brookings Institution. This skews the narrative of forgiveness as a tool for equity, as lower-income borrowers often carry smaller balances but face higher default rates.

From a comparative standpoint, other countries handle education financing differently, reducing the need for such debates. In Germany, public universities are tuition-free, funded directly through taxation. In contrast, the U.S. relies on individual loans, creating a system where forgiveness becomes a contentious bailout. This structural difference highlights a key issue: forgiving loans addresses a symptom, not the root cause of rising tuition costs. Taxpayers might reasonably ask why they should fund a solution that doesn’t prevent future generations from falling into the same debt trap.

Practically, the taxpayer burden argument also intersects with generational fairness. Baby boomers, many of whom benefited from affordable tuition and robust job markets, now face the prospect of their tax dollars funding the debts of younger generations. For example, a 60-year-old taxpayer who worked multiple jobs to pay off their $5,000 degree in the 1980s might resent subsidizing a $200,000 law degree today. This tension underscores the need for targeted solutions, such as income-driven repayment plans or public service loan forgiveness, which tie relief to specific contributions or needs rather than broad cancellations.

In conclusion, the taxpayer burden argument against student loan forgiveness is not merely about dollars and cents but about principles of fairness and accountability. While forgiveness may provide temporary relief, it risks alienating those who feel their hard-earned money is being misallocated. Policymakers must balance empathy for borrowers with the legitimate concerns of taxpayers, perhaps by pairing any forgiveness program with reforms that address the skyrocketing cost of higher education. Without such a dual approach, the debate will remain mired in accusations of unfair redistribution.

Student Loan Forgiveness: A Catalyst for Economic Growth and Recovery

You may want to see also

Explore related products

![]()

Contract Law: Does it breach existing loan agreements between borrowers and lenders?

The legality of student loan forgiveness hinges significantly on whether it violates existing loan agreements between borrowers and lenders. Contract law, which governs these agreements, emphasizes the sanctity of contracts, meaning both parties are bound by the terms they agreed to at the time of signing. When the government intervenes to forgive loans, it raises questions about whether such actions breach the contractual obligations outlined in these agreements. For instance, most student loan contracts explicitly state that borrowers must repay the principal amount plus interest, with specific terms for deferment, forbearance, or repayment plans. Forgiveness programs, by waiving these obligations, could be seen as altering the contract unilaterally, potentially violating the lender’s rights.

Analyzing this issue requires understanding the principle of *impairment of contracts*. Under the U.S. Constitution’s Contract Clause, states are prohibited from passing laws that impair contractual obligations. While this clause typically applies to state actions, the concept extends to federal interventions that retroactively change the terms of private agreements. For example, if a lender agreed to provide a loan based on the expectation of repayment, a forgiveness program could be argued to impair the lender’s right to receive the agreed-upon amount. Courts have historically upheld the importance of contractual stability, suggesting that any government action must carefully balance public policy goals with respect for existing agreements.

However, proponents of student loan forgiveness argue that such programs often fall under the government’s authority to regulate in the public interest. They point to examples like the Higher Education Relief Opportunities For Students (HEROES) Act, which allows the Secretary of Education to modify student loan terms during national emergencies. This act provides a legal framework for forgiveness programs, suggesting they do not inherently breach contracts but rather operate within statutory authority. Critics counter that this interpretation stretches the law’s intent, as it was designed for temporary relief, not widespread debt cancellation.

A comparative analysis of other debt forgiveness programs, such as those for medical or credit card debt, reveals a key distinction: student loans are often backed by the federal government, which complicates the contractual relationship. In cases where the government is both the lender and the regulator, the line between contractual obligation and public policy becomes blurred. For private lenders, however, the breach of contract argument holds more weight, as they rely on repayment to maintain financial stability. Borrowers, on the other hand, may argue that forgiveness programs are necessary to address systemic issues like skyrocketing tuition costs and limited job prospects, which were not anticipated at the time of signing.

In practical terms, lenders and borrowers can protect themselves by carefully reviewing loan agreements and staying informed about legislative changes. Lenders might include clauses addressing potential government interventions, while borrowers should explore existing repayment options before relying on forgiveness programs. Ultimately, the legality of student loan forgiveness under contract law depends on the specific terms of the agreement and the legal authority invoked by the government. As debates continue, both parties must navigate this complex intersection of law and policy, balancing individual obligations with broader societal needs.

Burger King Student Loan Forgiveness: Step-by-Step Registration Guide

You may want to see also

Explore related products

![]()

Executive Overreach: Is the President exceeding authority without congressional approval?

The debate over student loan forgiveness has ignited a critical examination of executive power, particularly whether the President can unilaterally cancel debt without congressional approval. At the heart of this issue lies the question of constitutional authority and the separation of powers. The President’s ability to act independently hinges on the interpretation of existing laws, specifically the Higher Education Act and the HEROES Act. While the HEROES Act grants the Secretary of Education authority to modify student loans during national emergencies, critics argue that mass forgiveness exceeds this scope, amounting to legislative action disguised as executive enforcement.

Consider the scale of the proposed forgiveness: up to $20,000 per borrower, totaling an estimated $400 billion. Such a sweeping financial decision typically requires congressional budgeting and approval. The Constitution vests Congress with the power to allocate funds and create laws, yet the executive branch’s unilateral action bypasses this process. This raises concerns about overreach, as the President effectively rewrites policy without legislative input. For instance, the Supreme Court’s 2023 ruling in *Biden v. Nebraska* struck down the forgiveness plan, citing the Major Questions Doctrine, which requires explicit congressional authorization for transformative actions.

From a practical standpoint, executive overreach in this context sets a precedent for future administrations to bypass Congress on major policy issues. If a President can unilaterally cancel debt, what stops them from enacting other large-scale financial measures without legislative oversight? This erodes the checks and balances system, concentrating power in the executive branch. Advocates of forgiveness argue it addresses a pressing crisis, but critics counter that such actions undermine democratic processes and fiscal responsibility. The takeaway is clear: while executive action can be swift, it must operate within the boundaries set by Congress to preserve constitutional integrity.

To navigate this issue, stakeholders should focus on collaborative solutions. Congress could pass targeted legislation to address student debt, ensuring accountability and transparency. Alternatively, the executive branch could work within existing legal frameworks to provide relief without overstepping authority. For borrowers, understanding these legal nuances is crucial. While forgiveness may seem appealing, its legality and long-term implications warrant scrutiny. Ultimately, the debate highlights the need for a balanced approach that respects both executive authority and congressional prerogative.

Unlocking Debt Relief: A Guide to Securing Student Loan Forgiveness

You may want to see also

![]()

Legal Precedent: Are there past cases that challenge the legality of debt forgiveness?

The legality of student loan forgiveness has been a contentious issue, often hinging on whether such actions align with established legal principles. To assess this, examining past cases that challenge debt forgiveness is crucial. One notable example is the legal battles surrounding the Public Service Loan Forgiveness (PSLF) program, where borrowers faced denials due to technicalities in program requirements. These cases highlight the tension between administrative discretion and statutory interpretation, setting a precedent for how courts evaluate debt forgiveness initiatives.

Analyzing these cases reveals a recurring theme: the importance of statutory authority. Courts have consistently scrutinized whether debt forgiveness programs exceed the powers granted by Congress. For instance, in *Bauer v. DeVos* (2020), borrowers challenged the Department of Education’s management of the PSLF program, arguing it violated the Administrative Procedure Act. While the case focused on procedural issues, it underscored the need for agencies to act within their legal boundaries. This precedent suggests that any broad student loan forgiveness initiative must have explicit congressional authorization to withstand legal challenges.

Another critical precedent comes from cases involving private student loans. Unlike federal loans, private lenders are not bound by government forgiveness programs, and attempts to discharge such debt through bankruptcy have historically faced stringent hurdles. The *Brunner test*, established in *Brunner v. New York State Higher Education Services Corp.* (1987), requires borrowers to prove "undue hardship," a standard so high that few succeed. While this case pertains to bankruptcy, it illustrates the legal system’s reluctance to absolve debt obligations without extraordinary circumstances, a principle that may influence challenges to broad forgiveness programs.

Practical takeaways from these precedents are clear: any student loan forgiveness initiative must navigate a complex legal landscape. Policymakers must ensure programs are grounded in statutory authority, and borrowers should understand the limitations of existing legal frameworks. For instance, if pursuing PSLF, meticulously document qualifying payments to avoid technical denials. Similarly, those with private loans should explore alternatives like refinancing or settlement negotiations, as bankruptcy remains an uphill battle. By learning from past cases, stakeholders can better anticipate and address legal challenges to debt forgiveness.

Forgiving ITT Student Loans from 2009: What Borrowers Need to Know

You may want to see also

Frequently asked questions

Student loan forgiveness is not inherently illegal, but some argue it violates the Appropriations Clause of the U.S. Constitution, which states that Congress must authorize spending. Critics claim that forgiving loans without explicit congressional approval oversteps executive authority.

The legality of the Biden administration's plan is debated. Opponents argue it exceeds presidential power and lacks congressional authorization, while supporters claim it falls under the Higher Education Act's authority to modify loan terms during national emergencies.

Yes, student loan forgiveness can be challenged in court, and it has been. Legal challenges often focus on whether the executive branch has the authority to forgive loans without explicit congressional approval or if it violates separation of powers principles.

Some states argue that student loan forgiveness is illegal because it unfairly redistributes taxpayer funds and violates the rights of those who have already paid off their loans. They also claim it oversteps federal authority and infringes on state sovereignty.