The question of whether all student loans will be eligible for forgiveness has become a pressing concern for millions of borrowers, especially as the cost of higher education continues to rise and economic uncertainties persist. Recent policy changes, such as the Biden administration’s targeted loan forgiveness programs, have provided relief to specific groups, but the scope of eligibility remains limited. While initiatives like Public Service Loan Forgiveness (PSLF) and income-driven repayment plans offer pathways to forgiveness, they often come with stringent requirements and lengthy timelines. Advocates argue for broader forgiveness to address systemic issues in student debt, while critics raise concerns about fairness and fiscal responsibility. As debates continue, borrowers are left navigating a complex landscape, awaiting clarity on whether their loans will qualify for relief and what long-term solutions may emerge.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Not all student loans are eligible for forgiveness. |

| Federal Student Loans | Eligible for forgiveness under specific programs (e.g., PSLF, IDR, Biden's one-time relief). |

| Private Student Loans | Generally not eligible for federal forgiveness programs. |

| Income-Driven Repayment (IDR) | Forgiveness after 20–25 years of qualifying payments, depending on the plan. |

| Public Service Loan Forgiveness (PSLF) | Forgiveness after 10 years of qualifying payments while working full-time for a qualifying employer. |

| Biden's One-Time Relief (2022) | Up to $20,000 in forgiveness for Pell Grant recipients; $10,000 for others (income limits apply). |

| Loan Types Covered by Biden's Plan | Direct Loans, FFELP loans held by DOE, Perkins Loans. |

| Excluded Loan Types | Private loans, FFELP and Perkins loans not held by DOE. |

| Income Limits (Biden's Plan) | $125,000 for individuals, $250,000 for married couples (based on 2020/2021 tax returns). |

| Current Status (as of Oct 2023) | Biden's plan is paused due to legal challenges; IDR and PSLF remain active. |

| Future Forgiveness Programs | Uncertain; depends on legislative and legal developments. |

| State-Specific Forgiveness | Some states offer forgiveness for specific professions (e.g., teachers, healthcare workers). |

| Tax Implications | Forgiveness may be tax-free under the American Rescue Plan Act (through 2025). |

Explore related products

What You'll Learn

![]()

Federal vs. Private Loans

Federal and private student loans diverge sharply in their eligibility for forgiveness programs, a critical distinction borrowers must grasp. Federal loans, backed by the government, often qualify for income-driven repayment plans, Public Service Loan Forgiveness (PSLF), and temporary relief measures like those introduced during the COVID-19 pandemic. For instance, the Biden administration’s 2022 forgiveness plan targeted federal loans, offering up to $20,000 in relief for Pell Grant recipients. Private loans, however, are excluded from these programs. Lenders like Sallie Mae or SoFi operate independently, prioritizing profit over public policy, leaving borrowers with fewer options for forgiveness or repayment flexibility.

To navigate this landscape, borrowers should first identify their loan type. Federal loans include Direct Subsidized, Unsubsidized, PLUS, and Perkins loans, while private loans are issued by banks, credit unions, or online lenders. A practical tip: log into the National Student Loan Data System (NSLDS) to confirm federal loan status. If private, contact the lender directly for repayment options, which may include refinancing but rarely forgiveness. Consolidating private loans into a federal Direct Consolidation Loan could open doors to forgiveness programs, but this step is irreversible and requires careful consideration.

The analytical takeaway is clear: federal loans offer a safety net, while private loans demand self-reliance. For example, a borrower with $50,000 in federal loans under an income-driven plan might pay as little as $0 monthly if their income is low, with forgiveness after 20–25 years. Conversely, a private loan borrower with the same balance faces fixed payments and no forgiveness pathway. This disparity underscores the importance of choosing federal loans when possible and exhaustively exploring forgiveness options before turning to private lenders.

Persuasively, borrowers should prioritize federal loans for their built-in protections. Private loans may offer lower upfront rates to high-credit individuals, but these rates can escalate, and terms are non-negotiable post-signing. For instance, a 4.99% private loan rate might seem attractive compared to a 5.5% federal rate, but federal loans cap interest and offer deferment or forbearance in hardship. The long-term security of federal loans far outweighs the short-term savings of private options, especially given the uncertainty of future financial circumstances.

In conclusion, the federal vs. private loan debate hinges on forgiveness eligibility and borrower protections. Federal loans provide structured pathways to relief, while private loans leave borrowers largely on their own. By understanding these differences, borrowers can make informed decisions, avoid pitfalls, and maximize their chances of managing or eliminating student debt effectively. Always review loan terms, explore federal options first, and seek professional advice when uncertain.

Student Loan Forgiveness Through Nelnet: Reality or Myth?

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans

Income-driven repayment (IDR) plans are a lifeline for borrowers struggling to manage federal student loan payments. These plans cap monthly payments at a percentage of discretionary income, typically 10% to 20%, depending on the plan. For example, the Revised Pay As You Earn Repayment Plan (REPAYE) sets payments at 10% of discretionary income for all borrowers, while the Income-Based Repayment Plan (IBR) caps payments at 10% or 15% based on when the borrower took out their first loan. This structure ensures payments remain manageable relative to earnings, providing immediate financial relief.

The true value of IDR plans lies in their pathway to loan forgiveness. After 20 or 25 years of qualifying payments, any remaining balance is forgiven. For instance, a borrower earning $40,000 annually with $50,000 in loans under the REPAYE plan might pay around $200 monthly, with forgiveness kicking in after 240 payments. However, this benefit isn’t automatic; borrowers must recertify their income and family size annually to remain eligible. Failure to do so can result in a return to the standard repayment plan, potentially increasing monthly payments.

Critics argue that IDR plans can lead to borrowers paying more in interest over time, as lower monthly payments often mean slower principal reduction. For example, a borrower with $100,000 in loans at 6% interest could accrue over $40,000 in interest over 25 years under an IDR plan. To mitigate this, borrowers should consider making extra payments when financially feasible, targeting the highest-interest loans first. Additionally, forgiven amounts may be taxable as income, though the American Rescue Plan Act of 2021 temporarily exempts student loan forgiveness from taxation through 2025.

Despite these considerations, IDR plans remain a critical tool for borrowers seeking eventual loan forgiveness. They are particularly beneficial for those pursuing Public Service Loan Forgiveness (PSLF), as IDR payments count toward the 120 required for PSLF. For instance, a teacher with $80,000 in loans could combine an IDR plan with PSLF, achieving forgiveness in 10 years instead of 20 or 25. Borrowers should carefully evaluate their eligibility and long-term goals before enrolling, as switching plans can reset the forgiveness clock.

In summary, income-driven repayment plans offer a structured path to loan forgiveness while providing immediate payment relief. By understanding their mechanics, potential pitfalls, and strategic applications, borrowers can maximize their benefits. Whether aiming for PSLF or standard IDR forgiveness, these plans are a cornerstone of federal student loan management, offering hope to millions burdened by educational debt.

Why Canceling Student Debt Isn't the Solution We Need

You may want to see also

Explore related products

![]()

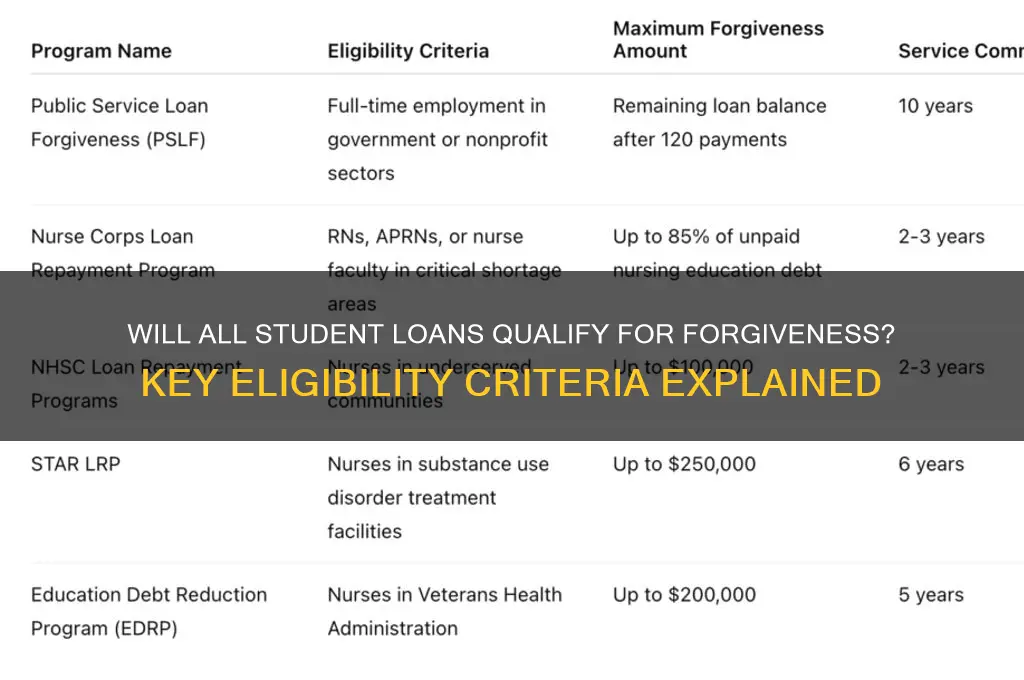

Public Service Loan Forgiveness

Consider the steps to qualify for PSLF: first, ensure your employer qualifies by using the Department of Education’s Employer Search Tool. Second, consolidate your loans into a Direct Loan if necessary, as only this type is eligible. Third, enroll in an income-driven repayment plan to lower monthly payments and align with PSLF requirements. Finally, submit the Employment Certification Form annually to track progress. Missing any of these steps can derail your path to forgiveness, so meticulous attention to detail is crucial.

One of the most compelling aspects of PSLF is its potential to forgive the remaining balance of your loans after 120 qualifying payments, tax-free. This contrasts sharply with income-driven repayment plans, which may forgive debt after 20–25 years but treat the forgiven amount as taxable income. For example, a borrower with $100,000 in debt could save tens of thousands of dollars by pursuing PSLF instead of relying on standard forgiveness timelines. However, this benefit is contingent on consistent, qualifying employment and payments, leaving no room for error.

Critics argue that PSLF’s complexity and strict requirements exclude many who could benefit. For instance, payments made under the wrong repayment plan or while working for a non-qualifying employer do not count toward the 120-payment threshold. Additionally, the program’s limited scope means it does not address the broader issue of student loan debt for millions of borrowers outside public service. Despite these limitations, PSLF remains a lifeline for those who navigate its intricacies successfully, offering a clear path to financial freedom for dedicated public servants.

Student Loan Forgiveness Deadline: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

Loan Type Eligibility Criteria

Not all student loans are created equal, and this disparity becomes glaringly apparent when discussing loan forgiveness eligibility. Federal student loans, particularly Direct Loans, dominate the conversation around forgiveness programs. These include Direct Subsidized and Unsubsidized Loans, PLUS Loans, and Consolidation Loans. Notably, the Public Service Loan Forgiveness (PSLF) program and income-driven repayment (IDR) plans primarily cater to borrowers with Direct Loans. If you have Federal Family Education Loans (FFEL) or Perkins Loans, you’re not automatically out of luck, but you must consolidate them into a Direct Consolidation Loan to qualify for most forgiveness programs. Private student loans, however, are almost universally excluded from federal forgiveness initiatives, leaving borrowers with limited options beyond refinancing or negotiating with lenders directly.

Understanding the eligibility criteria for loan forgiveness requires a deep dive into the specifics of each program. For instance, PSLF mandates 120 qualifying payments while working full-time for a government or nonprofit organization. Income-driven repayment plans, such as PAYE or REPAYE, offer forgiveness after 20–25 years of payments, but the forgiven amount may be taxed as income. Temporary programs like the limited PSLF waiver (which expired in October 2022) expanded eligibility by counting previously ineligible payments, but such opportunities are rare and time-sensitive. Borrowers must meticulously track their payment history and employment certifications to ensure compliance with program rules.

The type of loan you hold can significantly impact your forgiveness strategy. For example, Parent PLUS Loans are eligible for forgiveness under PSLF, but only if the parent, not the child, is employed in a qualifying public service role. Similarly, borrowers with FFEL or Perkins Loans must act swiftly to consolidate into a Direct Loan to access forgiveness programs. Private loans, which often carry higher interest rates and fewer protections, remain the most challenging to address. Borrowers with private loans may explore state-based forgiveness programs or employer-sponsored repayment assistance, but these options are far less comprehensive than federal initiatives.

Practical steps for maximizing forgiveness eligibility include regularly reviewing your loan type and repayment plan. If you have multiple loan types, prioritize consolidating FFEL or Perkins Loans into a Direct Consolidation Loan. Keep detailed records of your payments and employment certifications, especially for PSLF. For private loan holders, research state-specific programs or negotiate with lenders for reduced payments or settlements. Stay informed about policy changes, as legislative shifts can open new avenues for forgiveness. While not all loans are eligible, strategic planning can help borrowers navigate the complex landscape and secure the relief they need.

Debt Forgiveness for College Students: Fair Solution or Unfair Burden?

You may want to see also

Explore related products

![]()

Forgiveness Program Limitations

Not all student loans are created equal, and this disparity becomes glaringly apparent when examining forgiveness programs. Federal student loans, particularly those held by the Department of Education, often have access to forgiveness initiatives like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans. However, private student loans, which constitute roughly 8% of the total student debt market, are typically excluded from these programs. This fundamental divide underscores a critical limitation: forgiveness is not a universal solution but a targeted one, contingent on the type of loan and its holder.

Consider the eligibility criteria for PSLF, a program designed to forgive remaining loan balances after 120 qualifying payments for borrowers working in public service. While the program’s intent is noble, its requirements are stringent. Payments must be made under a qualifying repayment plan, such as an IDR plan, and the borrower must be employed full-time by a qualifying employer, like a government agency or nonprofit. Even minor missteps, like consolidating loans at the wrong time or missing a payment, can disqualify borrowers. For instance, a teacher with $50,000 in Direct Loans might assume eligibility but could be denied if their payments were made under a graduated repayment plan instead of an IDR plan. This highlights the program’s complexity and the need for meticulous adherence to its rules.

Another limitation lies in the scope of forgiveness programs. IDR plans, for example, promise forgiveness after 20–25 years of payments, but the forgiven amount is treated as taxable income. A borrower with $100,000 in forgiven debt could face a tax bill of $20,000 or more, depending on their tax bracket. This “forgiveness tax” can offset the perceived benefits, particularly for borrowers in higher income brackets. Additionally, IDR plans often result in lower monthly payments by extending the repayment term, meaning borrowers may pay more in interest over time despite the promise of eventual forgiveness.

Finally, political and administrative hurdles further constrain forgiveness programs. Proposals for widespread loan forgiveness, such as the Biden administration’s $10,000 cancellation plan, face legal challenges and congressional opposition. Even when implemented, these programs are often temporary or limited in scope. For example, the COVID-19 payment pause provided relief but did not address underlying debt issues. Borrowers must navigate this uncertain landscape, balancing hope for future forgiveness with the reality of current repayment obligations. Practical steps, such as enrolling in IDR plans, tracking qualifying payments for PSLF, and consulting tax professionals, can mitigate these limitations but cannot eliminate them entirely.

Income-Based Student Loans: Forgiveness Eligibility and What You Need to Know

You may want to see also

Frequently asked questions

No, not all student loans are eligible for forgiveness. Only specific types of loans, such as federal Direct Loans, qualify for programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. Private loans and certain federal loans (e.g., FFEL or Perkins Loans not consolidated into Direct Loans) are generally ineligible.

As of now, there are no confirmed plans to expand forgiveness to all student loans, including private loans. Proposals and discussions about broader forgiveness exist, but they remain subject to legislative and policy changes. Borrowers should monitor official announcements for updates.

No, forgiveness programs like PSLF or IDR forgiveness apply only to eligible federal loans. Private student loans are not covered by these programs and typically require repayment in full unless the lender offers a separate forgiveness or settlement option.