The topic of student loan forgiveness has sparked intense debate, particularly regarding its potential impact on taxpayers. Proponents argue that forgiving student debt would stimulate the economy by freeing up disposable income for millions of borrowers, while critics contend that it could place a significant financial burden on taxpayers, who may ultimately foot the bill for the forgiven loans. As the federal government considers various forgiveness plans, questions arise about the fairness of redistributing the cost to taxpayers, many of whom did not attend college or have already paid off their loans, and the long-term economic consequences of such a policy. This discussion highlights the complex interplay between debt relief, fiscal responsibility, and social equity.

Explore related products

What You'll Learn

![]()

Direct Cost to Taxpayers

Student loan forgiveness, while beneficial to borrowers, directly shifts the financial burden to taxpayers. The immediate cost arises from the government absorbing the forgiven debt, which reduces federal revenue. For instance, forgiving $10,000 per borrower for 43 million eligible individuals totals $430 billion—a sum that would otherwise be repaid with interest. This shortfall must be offset through reduced spending, increased taxes, or additional borrowing, all of which impact taxpayers directly or indirectly.

Consider the mechanics of funding such a program. If the government opts to borrow to cover the cost, it issues Treasury bonds, effectively deferring the expense to future taxpayers. Alternatively, if existing budgets are reallocated, programs like infrastructure, healthcare, or education may face cuts. For example, a $430 billion forgiveness plan could equate to roughly $1,300 per taxpayer, assuming 330 million taxpayers. This direct cost underscores the trade-offs involved, as funds diverted to loan forgiveness are unavailable for other public priorities.

Critics argue that the regressive nature of broad forgiveness exacerbates the taxpayer burden. High-earning borrowers, who are more likely to repay their loans, benefit disproportionately, while lower-income taxpayers—many of whom did not attend college—bear the cost. A targeted approach, such as income-driven repayment plans or Pell Grant recipient forgiveness, could mitigate this inequity. However, such measures require careful design to avoid creating new fiscal challenges.

Practical implications extend beyond immediate costs. Forgiving loans reduces future cash flow to the government, impacting long-term fiscal planning. For taxpayers, this could mean higher taxes or reduced services as the government adjusts to the revenue loss. Policymakers must weigh these trade-offs, ensuring that any forgiveness program aligns with broader economic goals and minimizes adverse effects on taxpayers. Balancing relief for borrowers with fiscal responsibility remains a complex, yet critical, task.

Indiana's Tax on Student Loan Forgiveness: Unpacking the Controversial Decision

You may want to see also

Explore related products

![]()

Impact on Federal Budget Deficit

Student loan forgiveness, while offering relief to millions of borrowers, directly impacts the federal budget deficit by reducing government revenue from loan repayments. The Congressional Budget Office (CBO) estimates that forgiving $10,000 per borrower could cost approximately $377 billion, while $50,000 in forgiveness could exceed $1 trillion. These figures are not abstract—they represent funds that would otherwise flow into federal coffers, offsetting other expenditures or reducing the deficit. When such a significant sum is removed from the revenue stream, the deficit widens, necessitating either spending cuts, tax increases, or increased borrowing to balance the budget.

Consider the mechanics of deficit financing. The federal government borrows by issuing Treasury bonds, which investors purchase with the expectation of repayment. If student loan forgiveness increases the deficit, the government must issue more bonds to cover the shortfall. This additional borrowing competes with private sector loans for investor dollars, potentially driving up interest rates. Higher interest rates ripple through the economy, affecting mortgage rates, business loans, and consumer credit. For taxpayers, this translates to a double burden: not only do they indirectly fund the forgiveness through increased borrowing costs, but they may also face higher taxes if the government seeks to recoup lost revenue.

A comparative analysis highlights the trade-offs. For instance, the $1.9 trillion American Rescue Plan of 2021, which included direct stimulus payments and expanded unemployment benefits, was funded through deficit spending. Similarly, student loan forgiveness would be another large-scale expenditure added to the deficit. However, unlike stimulus measures designed to boost short-term economic activity, loan forgiveness is a one-time cancellation of debt with long-term fiscal implications. While it alleviates financial strain for borrowers, it shifts the burden to taxpayers and future generations, who must bear the cost of a larger national debt.

To mitigate the impact on the federal budget deficit, policymakers could explore targeted forgiveness programs rather than blanket cancellation. For example, income-driven repayment plans or forgiveness tied to public service could limit costs while still providing relief to those most in need. Additionally, pairing forgiveness with reforms to reduce the cost of higher education could address the root cause of student debt. Taxpayers would benefit from a more sustainable approach that balances immediate relief with long-term fiscal responsibility, ensuring that the deficit does not spiral out of control.

Ultimately, the impact of student loan forgiveness on the federal budget deficit is a question of priorities and trade-offs. While it offers a lifeline to borrowers, it also requires careful consideration of how the cost will be absorbed. Taxpayers, as both beneficiaries and funders of government programs, must weigh the benefits of debt relief against the risks of a growing deficit. Without a clear plan to offset the cost, forgiveness could exacerbate fiscal challenges, leaving future generations to navigate the consequences.

VA Disability and Student Loans: Can 100% Rating Erase Debt?

You may want to see also

Explore related products

![]()

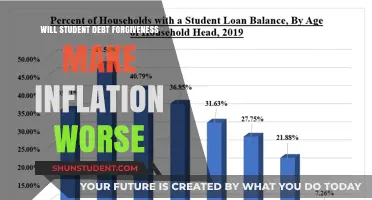

Redistribution of Tax Burden

Student loan forgiveness, while beneficial to borrowers, inherently shifts the financial responsibility from individuals to the collective taxpayer base. This redistribution of the tax burden raises critical questions about fairness, economic impact, and long-term consequences. For instance, forgiving $10,000 in student debt for an estimated 37 million borrowers could cost taxpayers approximately $370 billion. This figure, though significant, represents a fraction of the $7 trillion in annual federal spending but still prompts debate over whether such a redistribution aligns with broader fiscal priorities.

Consider the mechanics of this redistribution. When student loans are forgiven, the government absorbs the debt, effectively transferring the obligation to taxpayers. This means a retail worker in Ohio, earning $35,000 annually, could indirectly subsidize the debt relief of a graduate earning $70,000 in California. While the graduate benefits from reduced financial strain, the retail worker bears a proportional share of the cost without direct benefit. This dynamic underscores the regressive nature of the redistribution, as lower-income taxpayers often subsidize higher-income beneficiaries.

Proponents argue that this redistribution can stimulate economic growth by freeing up disposable income for borrowers, who may then spend more on goods and services. However, this assumes that the economic benefits outweigh the costs. For example, if forgiven loans lead to increased consumer spending, it could boost GDP, but if the program is funded through deficit spending, it may contribute to inflation, eroding purchasing power for all taxpayers. Balancing these trade-offs requires careful consideration of both immediate and long-term economic implications.

A practical approach to mitigating the regressive impact involves targeting relief to those most in need. For instance, capping forgiveness at incomes below $125,000 for individuals or $250,000 for households could reduce the burden on lower-income taxpayers. Additionally, pairing forgiveness with reforms to prevent future debt accumulation, such as lowering college tuition or expanding income-driven repayment plans, could address systemic issues rather than merely shifting costs. Such measures ensure that the redistribution of the tax burden is both equitable and sustainable.

Ultimately, the redistribution of the tax burden through student loan forgiveness is not inherently problematic but requires thoughtful design and implementation. Policymakers must weigh the benefits to borrowers against the costs to taxpayers, ensuring that the program aligns with broader economic and social goals. Without such balance, the initiative risks exacerbating inequality and undermining public trust in fiscal policy.

Student Loan Forgiveness: What Really Happened and Who Benefited?

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![]()

Long-Term Economic Effects

Student loan forgiveness, while providing immediate relief to borrowers, triggers a ripple effect across the economy, with taxpayers at the center of its long-term implications. One of the most debated outcomes is its impact on inflation. By injecting billions of dollars into the economy through debt cancellation, consumer spending could rise, particularly in sectors like housing and retail. However, this increased demand might outpace supply, driving prices upward. For instance, if 10 million borrowers suddenly have an extra $300 per month, the housing market could see a surge in demand, potentially raising rents and home prices. Taxpayers, as both consumers and property owners, would feel this inflationary pressure directly, eroding purchasing power over time.

Another critical long-term effect lies in the labor market dynamics. With reduced financial burden, borrowers might feel more empowered to pursue career changes, entrepreneurship, or public service roles that traditionally offer lower salaries. This shift could enhance productivity and innovation, as individuals align their careers with their passions rather than debt obligations. However, it also risks creating labor shortages in high-paying sectors like finance or tech, where workers might opt for less lucrative but more fulfilling roles. Taxpayers, as both employers and employees, would need to adapt to this evolving workforce landscape, potentially facing higher wages or skill gaps in certain industries.

From a fiscal perspective, the long-term economic effects on taxpayers hinge on how the government funds student loan forgiveness. If financed through deficit spending, it could lead to higher national debt, necessitating future tax increases or spending cuts to balance the budget. For example, a $1 trillion forgiveness program spread over 10 years could translate to an additional $100 billion annually in government liabilities. Taxpayers might face higher income taxes, reduced social services, or both, as the government seeks to offset this burden. Alternatively, if funded through targeted tax increases on high-income earners or corporations, the impact on the average taxpayer could be minimized, though it would still ripple through the economy via reduced corporate investment or wage growth.

Lastly, the psychological and behavioral changes among borrowers could have understated but profound economic effects. Debt forgiveness might encourage future students to borrow more aggressively, assuming that another round of cancellation is possible. This moral hazard could inflate tuition costs further, as colleges raise prices in response to higher demand. Taxpayers, as both parents and contributors to public education funding, would indirectly subsidize this cycle, facing higher taxes to support both loan forgiveness and escalating education costs. Breaking this cycle requires not just forgiveness but structural reforms in higher education financing, a challenge that taxpayers will ultimately fund through policy decisions.

Student Loan Forgiveness: Boosting Financial Freedom and Quality of Life

You may want to see also

Explore related products

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![]()

Political and Social Implications

Student loan forgiveness, a policy often framed as a lifeline for borrowers, carries profound political and social implications that ripple far beyond individual relief. Politically, it serves as a litmus test for a party’s commitment to economic equity, with Democrats frequently championing it as a tool to address systemic inequality and Republicans criticizing it as fiscally irresponsible and unfair to non-borrowers. This divide reflects broader ideological clashes over the role of government in redistributing wealth and alleviating personal debt. For instance, the Biden administration’s 2022 proposal to forgive up to $20,000 in student debt sparked intense partisan debate, with critics arguing it would disproportionately benefit higher-income earners while supporters highlighted its potential to stimulate economic growth by freeing up disposable income.

Socially, student loan forgiveness reshapes public perceptions of fairness and responsibility. On one hand, it can foster solidarity among younger generations burdened by debt, reinforcing narratives of collective struggle against systemic barriers. On the other, it risks alienating those who paid off their loans or chose not to pursue higher education, fueling resentment and deepening generational divides. A 2023 Pew Research Center survey found that while 60% of adults under 30 supported broad loan forgiveness, only 35% of those over 65 agreed, underscoring the policy’s polarizing effect. This tension highlights the challenge of balancing empathy for borrowers with respect for those who perceive themselves as excluded from the benefits.

The policy also intersects with racial and economic justice movements, as Black and Latino borrowers, who disproportionately carry higher debt loads due to historical inequities, stand to gain the most from forgiveness. For example, data from the Brookings Institution shows that Black students owe an average of $7,400 more than their white peers upon graduation and default at rates three times higher. In this context, loan forgiveness becomes a tool for addressing racial wealth gaps, though its effectiveness depends on complementary policies like affordable college tuition and targeted financial literacy programs. Without such measures, forgiveness alone risks being a temporary bandage on a systemic wound.

Finally, the political feasibility of student loan forgiveness hinges on framing and implementation. Policymakers must navigate the optics of “handouts” versus “investments,” emphasizing long-term economic returns rather than short-term costs. For instance, framing forgiveness as part of a broader strategy to boost homeownership, entrepreneurship, and consumer spending could broaden its appeal. Practical steps, such as means-testing forgiveness to exclude high-income earners or capping eligibility at undergraduate debt, could mitigate criticisms of unfairness. Ultimately, the success of such policies will depend on their ability to bridge ideological divides while addressing the root causes of educational debt.

Physician Assistant Student Loan Forgiveness: 10-Year Timeline Explained

You may want to see also

Frequently asked questions

Student loan forgiveness itself does not directly increase taxes for taxpayers. However, if the forgiven amount is considered taxable income, the borrower may owe taxes on it, depending on current tax laws.

Student loan forgiveness could increase the federal deficit, which might indirectly affect taxpayers through potential future tax increases or reduced government spending in other areas to offset the cost.

Taxpayers without student loans may indirectly bear the cost of forgiveness through higher taxes or reduced government services if the program increases the federal deficit, though the direct impact varies based on policy decisions.

While taxpayers fund government programs, including student loan forgiveness, it doesn’t mean individuals are directly paying off others’ debts. The cost is spread across the tax base and depends on how the government finances the program.

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)